Data Center Blade Server Market Report Scope & Overview:

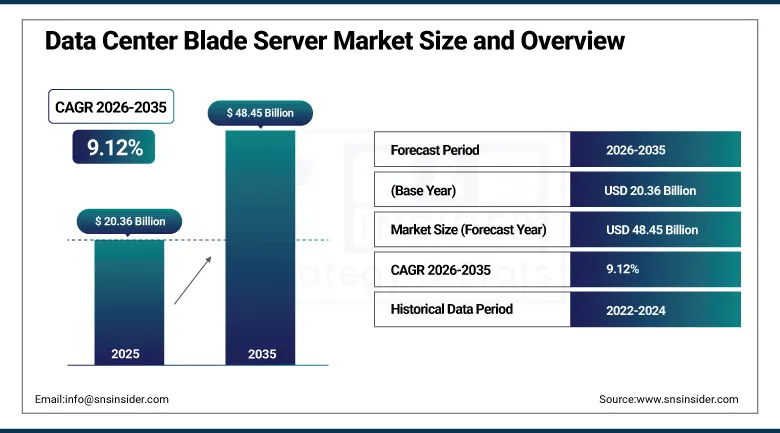

The Data Center Blade Server Market was valued at USD 20.36 Billion in 2025 and is expected to reach USD 48.45 Billion by 2035, growing at a CAGR of 9.12% from 2026 to 2035.

The global data center blade server market is growing at a strong and consistent pace as the exponential growth in enterprise data volumes, the extraordinary expansion of cloud computing infrastructure, the proliferation of AI and machine learning workloads, and the systematic migration of enterprise applications to virtualized environments. The market is propelled by the rising demand for high-performance scalable data storage solutions, blade servers’ superior power efficiency reducing operational costs through shared chassis power supply and cooling systems, the increasing data center expansions, and AI and machine learning workloads whose training and inference processing intensity creates compelling use cases for blade server density and interconnect advantages.

In 2024, HPE announced its ProLiant BL460c Gen11 server blade with fourth-generation AMD EPYC processor integration for HPE BladeSystem chassis, delivering above-40% performance improvement over prior generation for virtualization, cloud infrastructure, and AI inference workloads. The product refresh demonstrates the blade server market's continuing investment cycle whose performance generation transitions sustain above-commodity server market growth as data center operators upgrade blade chassis content to access the processor generation performance improvements that their virtualized workload density economics justify.

Market Size and Forecast

-

Market Size in 2026E: USD 22.22 Billion

-

Market Size by 2035: USD 48.45 Billion

-

CAGR: 9.12% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Data Center Blade Server Market - Request Free Sample Report

Data Center Blade Server Market Trends

-

AI-optimized blade servers integrate GPUs and high-bandwidth interconnects to support intensive AI training and inference workloads.

-

Liquid cooling adoption enables higher blade density by efficiently managing increasing processor and memory heat loads.

-

Open architecture blade systems reduce vendor lock-in through interoperable infrastructure and flexible component integration capabilities.

-

Software-defined infrastructure enhances centralized provisioning, workload orchestration, and power management across blade server environments.

-

Edge computing deployments drive demand for compact, high-density blade servers in distributed and space-constrained locations.

The U.S. Data Center Blade Server Market Outlook

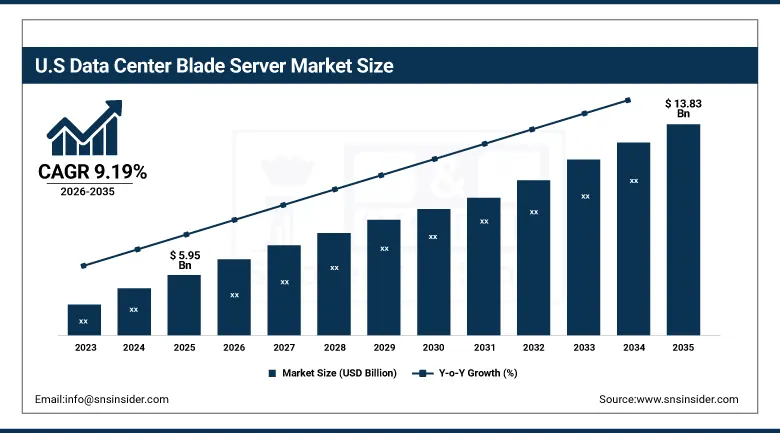

The U.S. data center blade server market was valued at approximately USD 5.95 Billion in 2025 and is expected to reach approximately USD 13.83 Billion by 2035, growing at a CAGR of approximately 9.19%.

The U.S. is the world's most commercially significant data center blade server market. The extraordinary scale of U.S. hyperscale data center investment from AWS, Microsoft Azure, Google Cloud, and Meta creates the most commercially intensive single-country blade server procurement environment. The U.S. federal government's IT modernization programmes, the financial services sector's high-performance computing investment, and the healthcare sector's digital infrastructure expansion create structured enterprise blade server procurement beyond hyperscale cloud operator demand. The CHIPS Act's data center investment incentives and domestic semiconductor manufacturing expansion create additional procurement channels that sustain U.S. market leadership through the forecast period.

In 2023, Cisco launched the Cisco UCS X-Series Modular System Gen 3 with enhanced AI workload acceleration capability, introducing next-generation Intel Xeon Scalable processor blades with up to 8 TB of memory capacity per compute node for in-memory database and AI inference applications. The launch reflects the commercial direction of blade server architecture toward AI workload optimization.

Data Center Blade Server Market Segment Analysis

-

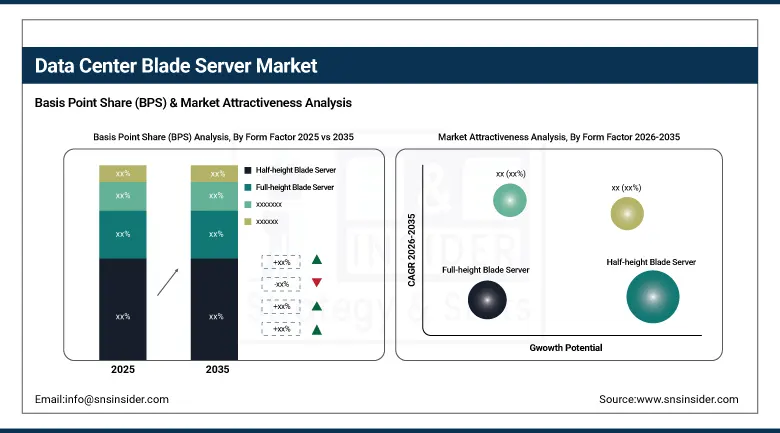

By Form Factor, the half-height blade server segment dominated the market with approximately 50% share in 2025, while the full-height blade server segment is the fastest growing.

-

By Channel, the direct segment dominated the market with approximately 51% share in 2025, while the reseller segment is the fastest growing.

-

By Application, the virtualization and cloud computing segment dominated the market with over 33% share in 2025, while the AI and machine learning workloads segment is the fastest growing at approximately 11.82% CAGR.

-

By End-use, the IT & telecom segment dominated the market with the largest share in 2025, while the healthcare segment is the fastest growing.

By Form Factor, half-height dominates, full-height grows fastest

Half-height blade servers retained the dominant form factor position with approximately 50% of the data center blade server market in 2025. The half-height form factor's commercial primacy reflects its balanced performance-density-cost trade-off that makes it the appropriate specification for the majority of enterprise virtualization, cloud infrastructure, and standard compute workloads whose processing requirements are efficiently served by dual-socket CPU blade configurations without the expanded resources that full-height alternatives provide at proportionally higher cost. Each data center capacity planning exercise that evaluates compute density per watt, per rack unit, and per dollar of investment creates half-height specification preference for general-purpose virtualization workloads whose standard VM density requirements align with half-height blade performance characteristics.

Full-height blade servers are the fastest growing form factor at approximately 10.34% CAGR because the extraordinary growth of AI model training, in-memory database applications, and high-performance technical computing creates workload profiles that require the above-standard processor socket count, expanded DIMM capacity, and GPU accommodation that full-height blade modules provide within chassis-shared power and cooling infrastructure. Each AI infrastructure deployment that integrates GPU-equipped full-height blade modules within a shared chassis creates procurement whose per-blade commercial value substantially exceeds equivalent half-height alternatives while maintaining the chassis management and density advantages that make blade architecture preferable to equivalent rack-mounted GPU server alternatives.

By Application, virtualization dominates, AI & ML grows fastest

Virtualization and cloud computing retained the dominant application position with over 33% of the data center blade server market in 2025. The fundamental alignment between blade server architecture and virtualized workload characteristics creates the most established and commercially mature blade server application. Blade chassis shared networking fabric enables rapid VM migration between blades without traffic interruption, shared storage access creates VM mobility across the chassis, and centralized chassis management simplifies the blade provisioning that virtualization administrators require for dynamic workload placement. Each enterprise migration from physical server to virtualized infrastructure creates blade server procurement whose density advantage over equivalent rack server configurations creates floor space and operational efficiency improvement that sustains specification preference.

AI and machine learning workloads are the fastest growing application at approximately 11.82% CAGR because the extraordinary commercial and research investment in AI infrastructure creates blade server procurement whose per-workload computational intensity creates above-standard blade hardware specification investment. Each enterprise AI programme that deploys GPU-accelerated blade infrastructure for model training, inference serving, and data pipeline processing creates procurement whose commercial value scales with AI workload intensity rather than general VM density metrics. NVIDIA GPU-equipped HPE and Cisco blade modules for enterprise AI workload deployment demonstrate the commercial scale of AI workload-driven blade server procurement whose growth rate substantially exceeds virtualization workload infrastructure growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Data Center Blade Server Market Insights

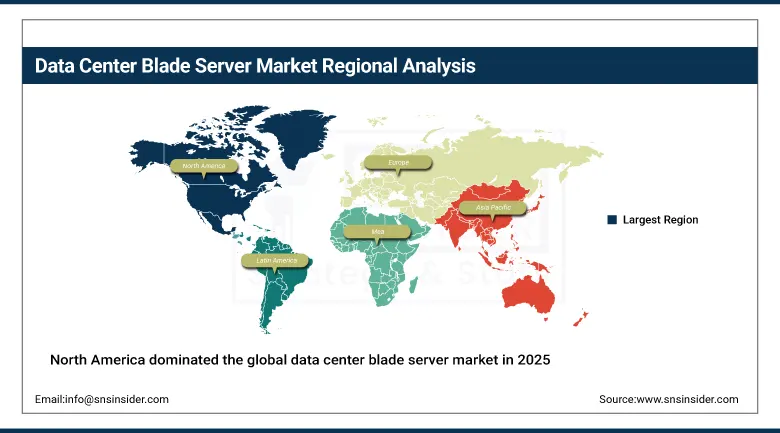

North America dominated the global data center blade server market in 2025, driven by hyperscale cloud infrastructure investment from AWS, Microsoft Azure, and Google Cloud, the enterprise sector's comprehensive IT modernization investment, and the commercial headquarters presence of HPE, Dell Technologies, Cisco Systems, and IBM. The United States accounts for approximately 87.4% of North American revenues through its extraordinary data center investment scale and enterprise IT modernization spending.

Canada contributes approximately 12.6% of North American revenues through its growing data center construction programme in Ontario and British Columbia, the financial services sector's computing infrastructure investment, and the federal government's digital services modernization creating blade server procurement from public sector IT programmes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Data Center Blade Server Market Insights

Europe is a technically sophisticated data center blade server market where GDPR data sovereignty requirements, the EU's digital infrastructure investment under the Digital Compass 2030 programme, and the financial services and manufacturing sectors’ high-performance computing create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its financial services sector's computing infrastructure, Deutsche Telekom's and SAP's data center investment, and the automotive sector's engineering computing requirements.

The United Kingdom, France, and the Netherlands are significant secondary markets where London's financial services computing infrastructure, Paris's hyperscale data center growth, and Amsterdam's Internet Exchange-adjacent data center cluster create consistent procurement. Lenovo’s and IBM’s European server operations sustain regional supply.

Asia Pacific Data Center Blade Server Market Insights

Asia Pacific is the fastest growing regional data center blade server market, driven by China's extraordinary data center construction programme, India's IT sector infrastructure investment, Japan's enterprise computing modernization, South Korea's advanced technology sector, and Southeast Asia's cloud infrastructure development. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary data center investment scale, the government's digital infrastructure programme, and the technology sector's AI computing infrastructure deployment.

India represents the most commercially dynamic emerging market within Asia Pacific where the IT and business process outsourcing sector's data center expansion, the financial sector's computing infrastructure investment, and the government's digital India programme creating public sector IT procurement create above-average blade server market growth from a rapidly expanding commercial base.

MEA & Latin America Data Center Blade Server Market Insights

The UAE leads MEA revenues at approximately 31.2% through its smart city data center infrastructure, the financial services sector's high-performance computing, and ADNOC's digital transformation creating structured blade server procurement. Saudi Arabia's NEOM data infrastructure and Aramco's digital transformation add complementary Gulf demand.

Brazil leads Latin American revenues at approximately 44.2% through its financial services sector's data center investment, the IT services sector's computing infrastructure, and the government's digital transformation programme. Mexico's IT outsourcing sector and Colombia's cloud adoption collectively sustain regional growth through 2035.

Market Dynamics

Growth Drivers: AI workload growth and hyperscale cloud infrastructure expansion

AI and machine learning workload growth is the data center blade server market's most commercially premium structural growth driver whose per-server hardware investment substantially exceeds equivalent virtualization workload infrastructure. Each large language model deployment whose GPU-accelerated infrastructure requirements create full-height GPU blade procurement at above-standard server pricing creates commercial momentum that sustains premium blade server market growth above the baseline virtualization infrastructure procurement rate. The extraordinary investment in enterprise AI from financial services, healthcare, manufacturing, and retail creates diverse institutional AI infrastructure procurement that compounds with hyperscale cloud AI service investment to sustain above-overall-IT-market blade server growth.

Cloud computing expansion creates the most commercially consistent structural blade server demand whose hyperscale data center construction creates large-volume blade server procurement from AWS, Microsoft Azure, Google Cloud, and emerging cloud operators whose combined annual infrastructure investment runs to hundreds of billions of dollars. Each new hyperscale data center that achieves power-on creates blade server procurement whose scale creates the most commercially concentrated individual customer purchase events in the server market.

Restraints: High energy consumption and legacy system compatibility challenges

Blade server energy consumption at scale, while more efficient than equivalent standalone server deployments on a per-compute-unit basis, creates significant absolute power demand in large-scale chassis deployments whose total facility power impact requires substantial cooling infrastructure investment. Each data center capacity expansion whose blade server deployment increases facility power density beyond air-cooled cooling system capability creates infrastructure investment that moderates the pace of blade deployment scale-up. Rising electricity costs and sustainability commitments from major data center operators create operational cost sensitivity that sustains investment in energy efficiency improvement but limits the pace of pure capacity expansion.

Compatibility issues between new blade server generations and existing chassis infrastructure create upgrade investment requirements that moderates the pace of blade refresh cycles in organisations whose capital budget constraints require multi-year amortization of chassis infrastructure investment. Each blade generation transition whose processor architecture change creates chassis component incompatibility creates capital planning complexity that sustains longer refresh cycles in cost-constrained enterprise data center environments.

Opportunities: AI workload specialized blade development and edge computing blade deployment

AI workload specialized blade development represents the most commercially premium near-term market opportunity whose GPU integration, high-bandwidth memory, and specialized fabric interconnect create blade server product categories with above-general-purpose server commercial value. Each AI infrastructure programme that deploys purpose-built GPU blade modules creates procurement whose per-blade commercial value creates above-market average revenue that sustains vendor differentiation investment. HPE’s and Cisco’s AI-optimized blade module development demonstrates the commercial investment in this highest-value blade server market segment.

Edge computing blade deployment represents the most geographically distributed near-term expansion opportunity whose telecommunications edge, industrial IoT, and retail analytics deployments create blade server procurement at locations where full data center infrastructure is impractical. Each 5G mobile edge computing site that deploys blade servers for ultra-low latency application processing creates procurement that compounds with 5G network deployment and edge computing workload migration.

Recent Developments:

-

2025: Hewlett Packard Enterprise introduced next-generation ProLiant Gen12 servers with enhanced AI acceleration, energy efficiency, and high-density compute capabilities for modern data centers.

-

2025: Dell Technologies expanded its PowerEdge server portfolio with advanced liquid-cooling support and AI-optimized infrastructure designed for large-scale enterprise and cloud workloads.

-

2025: Cisco enhanced its Unified Computing System (UCS) platform with AI-driven infrastructure management and automated workload orchestration capabilities, improving data center operational efficiency.

-

2025: Lenovo launched upgraded ThinkSystem server solutions featuring accelerated computing, improved thermal management, and scalable architectures supporting AI, cloud, and edge deployments.

Data Center Blade Server Market key players are:

-

Hewlett Packard Enterprise Co. (HPE)

-

Dell Technologies Inc.

-

Cisco Systems Inc. (UCS)

-

IBM Corporation

-

Lenovo Group Ltd.

-

Fujitsu Limited

-

Huawei Technologies Co. Ltd.

-

Hitachi Ltd.

-

NEC Corporation

-

Bull SAS (Atos)

-

Inspur Group Co. Ltd.

-

Supermicro (Super Micro Computer Inc.)

-

Oracle Corporation

-

Nutanix, Inc.

-

Pure Storage, Inc.

-

Penguin Solutions, Inc.

-

Gigabyte Technology Co. Ltd.

-

ASUSTek Computer Inc.

-

Quanta Computer Inc.

-

Wistron Corporation

Data Center Blade Server Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.36 Billion |

| Market Size by 2035 | USD 48.45 Billion |

| CAGR | CAGR of 9.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form Factor (Half-height Blade Server, Full-height Blade Server, Quarter-height Blade Server) • By Channel (Direct, Reseller, Systems Integrator, Others) • By Application (Virtualization and Cloud Computing, High-performance Computing, Storage and Backup, Web Hosting, Database Management, AI and Machine Learning Workloads) • By End-use (BFSI, Healthcare, Energy, IT & Telecom, Government & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Hewlett Packard Enterprise Co. (HPE), Dell Technologies Inc., Cisco Systems Inc. (UCS), IBM Corporation, Lenovo Group Ltd., Fujitsu Limited, Huawei Technologies Co. Ltd., Hitachi Ltd., NEC Corporation, Bull SAS (Atos), Inspur Group Co. Ltd., Supermicro (Super Micro Computer Inc.), Oracle Corporation, Nutanix, Inc., Pure Storage, Inc., Penguin Solutions, Inc., Gigabyte Technology Co. Ltd., ASUSTek Computer Inc., Quanta Computer Inc., Wistron Corporation |

Frequently Asked Questions

The market is expected to grow at a CAGR of 9.12% from 2026 to 2035.

The market was valued at USD 20.36 Billion in 2025.

North America dominated the Data Center Blade Server Market in 2025.

AI and machine learning workload growth creating premium GPU-accelerated blade infrastructure demand above standard virtualization server pricing.

Half-height Blade Servers dominated with approximately 50% share in 2025.

Get in Touch