Data Privacy Software Market Report Scope & Overview:

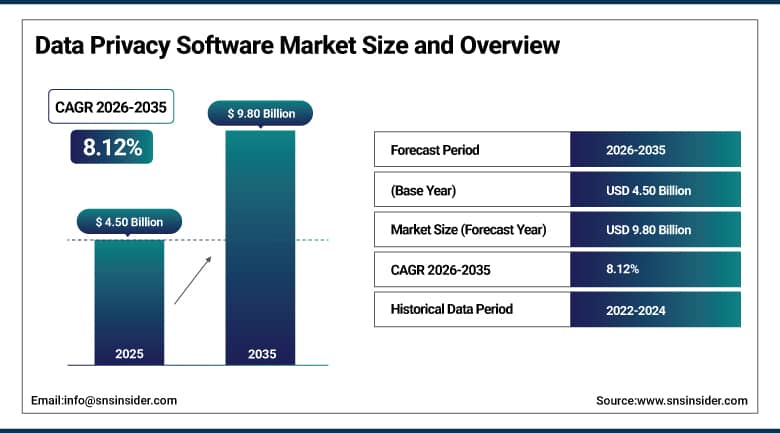

The Data Privacy Software Market was valued at USD 4.50 billion in 2025 and is expected to reach USD 9.80 billion by 2035, growing at a CAGR of 8.12% from 2026–2035.

The data privacy software market is witnessing rapid global growth due to rising demand for regulatory compliance and secure data governance. Across enterprises, adoption is increasing for data discovery, classification, consent management, and risk monitoring solutions. Growth is further supported by AI driven privacy automation and cloud based security frameworks. The data privacy software market is also driven by increasing deployment of enterprise wide governance platforms and integrated cybersecurity solutions. Industries such as BFSI, healthcare, retail, IT, and government are rapidly adopting privacy management systems. Rising focus on data protection and digital trust is accelerating market expansion. Additionally, increasing incidents of data breaches and cyber threats are pushing organizations to invest heavily in advanced privacy solutions.

Government initiatives related to data protection regulations, cybersecurity compliance, and digital governance are propelling the data privacy software market. Europe has strengthened GDPR enforcement, where strict data handling and consent regulations are mandated for organizations. The United States is expanding state level privacy laws like CCPA and CPRA. India is implementing the Digital Personal Data Protection framework, promoting stronger enterprise data governance and compliance adoption.

Market Size and Forecast

-

Market Size 2026E: USD 4.86 Billion

-

Market Size 2035: USD 9.80 Billion

-

CAGR (2026 - 2035): 8.12%

-

Fastest Growing Region: Asia Pacific

-

Largest Region : North America

To Get More Information On Data Privacy Software Market - Request Free Sample Report

Data Privacy Software Market Trends

-

-

Rapid adoption of AI driven data privacy tools enables automated data discovery classification and real time risk monitoring improving compliance efficiency.

-

Strong global regulations such as GDPR CCPA and DPDP are increasing enterprise demand for advanced privacy software solutions.

-

Expansion of cloud based privacy platforms supports scalable deployment and improves centralized data governance across hybrid environments.

-

Use of encryption tokenization and differential privacy enhances protection of sensitive data while maintaining operational usability.

-

Rising cyber threats and data breaches are accelerating adoption of zero trust security integrated with privacy management systems.

-

Growing focus on consent management is driving automated user data control and improving transparency across digital ecosystems.

-

Data Privacy Software Market Size Outlook:

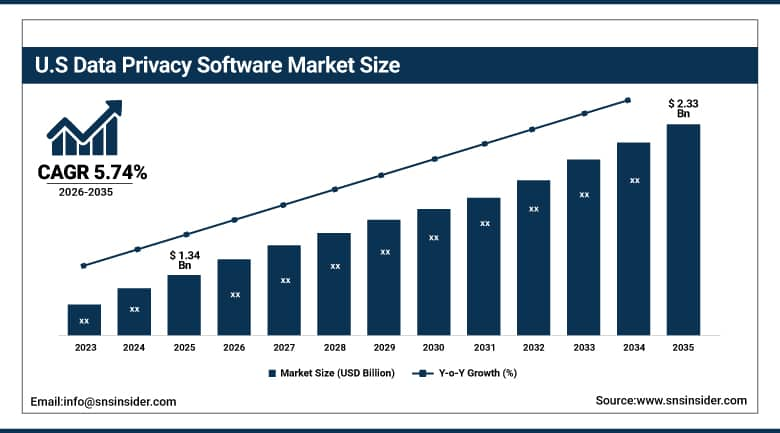

The U.S. Data Privacy Software Market was valued at USD 1.34 billion in 2025 and is expected to reach around USD 2.33 billion by 2035, growing at a CAGR of 5.74% from 2026–2035.

The U.S. data privacy software market is growing steadily due to rising demand for regulatory compliance and secure enterprise data governance across BFSI healthcare and IT sectors. Market expansion is driven by increasing adoption of AI based privacy tools cloud privacy platforms and automated data discovery solutions. Rising cyber threats data breaches and strict compliance requirements are major factors supporting growth. Organizations are also adopting zero trust security frameworks privacy enhancing technologies and real time monitoring systems to strengthen data protection, ensure compliance, and improve overall operational efficiency.

The United States data privacy software market is strongly influenced by strict regulatory frameworks such as CCPA and CPRA along with rapidly evolving state level privacy laws across multiple jurisdictions. The country is a major contributor to North America’s leadership in data privacy adoption, driven by strong enterprise demand in BFSI healthcare and IT sectors. Rising data breach incidents and increasing compliance penalties are pushing organizations to adopt AI driven privacy platforms and automated governance tools. Enterprises are also implementing zero trust security models and privacy enhancing technologies to strengthen data protection and ensure regulatory compliance.

Data Privacy Software Market Segment Analysis

-

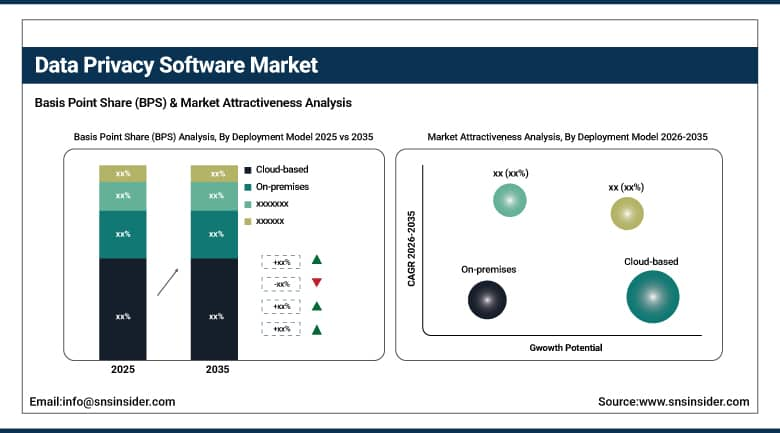

By Deployment Model, cloud-based dominated the data privacy software market with 63.45 % share in 2025 and it is also fastest growing segment.

-

By Organization Size, large enterprises dominated the data privacy software market with 58.47% share in 2025; while small and medium-sized enterprises (SMEs) is the fastest growing segment.

-

By Industry Vertical, healthcare dominated the data privacy software market with 31.85% share in 2025; while financial services is the fastest growing segment.

-

By Data Type, personal identifiable information (PII) dominated the data privacy software market with 55.63% share in 2025; while sensitive data is the fastest growing segment.

By Deployment Model, cloud-based segment dominates the data privacy software market and is also the fastest growing segment.

Cloud-based segment dominated the data privacy software market with the highest revenue share in 2025. This dominance is driven by strong enterprise shift toward scalable and cost efficient privacy solutions across multi cloud and hybrid IT environments. Organizations prefer cloud deployment for faster implementation centralized data governance and real time compliance monitoring. Integration with AI driven analytics automated data discovery and continuous regulatory updates further strengthens adoption across BFSI healthcare IT and government sectors.

It is also expected to grow at the fastest CAGR from 2026–2035 due to increasing demand for flexible deployment and remote accessibility across global enterprises. Rising digital transformation cloud migration and expansion of SaaS based applications are accelerating adoption. Organizations are prioritizing automated privacy management tools that ensure real time monitoring compliance and security across distributed data environments. Growing cyber threats and regulatory pressure are further driving continuous investment in advanced cloud based privacy platforms.

By Organization Size, large enterprises dominated the data privacy software market, while small and medium-sized enterprises (SMEs) is the fastest growing segment.

Large enterprises segment dominated the data privacy software market with the highest revenue share in 2025. This dominance is driven by their extensive data ecosystems and high volume of sensitive enterprise data across BFSI healthcare IT and government sectors. Large organizations have strong financial capacity to invest in advanced AI driven privacy platforms automated compliance systems and zero trust security frameworks. Increasing regulatory scrutiny and frequent audits further push enterprises to adopt robust data governance and privacy management solutions for risk mitigation and compliance assurance.

Small and medium-sized enterprises (SMEs) is expected to grow at the fastest CAGR from 2026-2035 due to rising digital adoption and increasing awareness of data protection regulations. SMEs are rapidly shifting toward affordable cloud based privacy solutions that offer easy deployment scalability and lower operational costs. Growing cybersecurity threats and regulatory requirements such as GDPR and DPDP are encouraging SMEs to invest in automated compliance tools. Expanding SaaS ecosystems and AI powered privacy platforms are further enabling SMEs to strengthen data security and meet evolving compliance standards efficiently.

By Industry Vertical, healthcare dominated the data privacy software market, while financial services is the fastest growing segment.

Healthcare segment dominated the data privacy software market in 2025 due to high volume of sensitive patient data generated across hospitals clinics and digital health platforms. Increasing adoption of electronic health records telemedicine and AI driven diagnostics requires strict compliance with privacy regulations. Strong regulatory frameworks like HIPAA GDPR and DPDP further drive continuous investment in advanced data privacy and protection solutions across healthcare organizations.

Financial services segment is expected to grow at the fastest CAGR from 2026 to 2035 due to rising digital banking fintech expansion and increasing online transactions. High exposure to cyber fraud identity theft and financial data breaches is pushing banks and insurance firms to adopt advanced privacy software. Regulatory compliance requirements along with customer trust concerns are driving rapid implementation of AI based privacy management encryption and real time data monitoring systems.

By Data Type, personal identifiable information (PII) dominated the data privacy software market, while sensitive data is the fastest growing segment.

Personal identifiable information (PII) segment dominated the data privacy software market with the highest revenue share in 2025. This dominance is driven by massive volume of personal data collected across digital platforms, banking systems, healthcare records, and e-commerce transactions. Increasing regulatory requirements such as GDPR, CCPA, and DPDP framework force enterprises to prioritize PII protection. Organizations focus heavily on securing identity data, customer records, and financial information.

Sensitive data segment is expected to grow at the fastest CAGR from 2026–2035 due to rising cyber threats and increasing exposure of critical enterprise information. This includes financial credentials, health records, intellectual property, and government classified data. Growing adoption of cloud computing and remote work increases vulnerability of sensitive datasets. Enterprises are rapidly investing in advanced encryption, zero trust security, and AI driven monitoring solutions to protect highly confidential and high risk data.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.35% |

|

Europe |

Germany |

19.50% |

|

Asia Pacific |

China |

21.35% |

|

Middle East & Africa |

UAE |

7.00% |

|

Latin America |

Brazil |

6.45% |

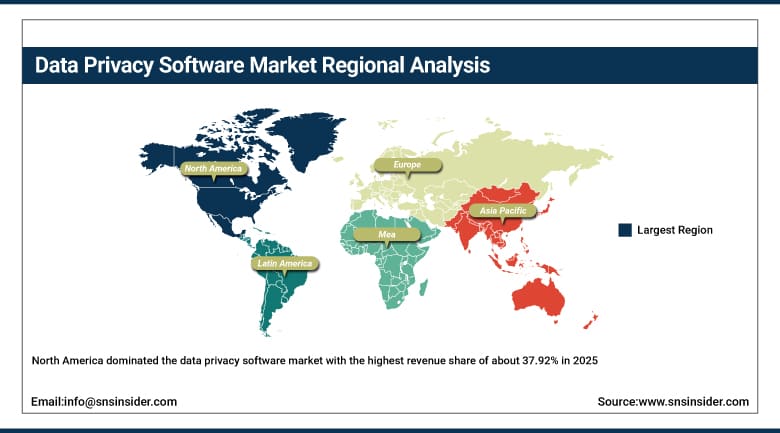

North America Data Privacy Software Market Insights.

North America dominated the data privacy software market with the highest revenue share of about 37.92% in 2025 due to strong demand from BFSI healthcare IT and government sectors along with rising adoption of cloud based privacy platforms AI driven compliance tools and automated data governance solutions. The region benefits from the strong presence of key players such as IBM Microsoft Oracle Salesforce and Informatica. Strict regulatory frameworks like CCPA CPRA and evolving state level privacy laws across the United States and Canada are further accelerating enterprise investments in advanced data privacy solutions. Rising cyber threats and frequent data breach incidents are also driving continuous adoption of privacy management technologies.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Data Privacy Software Market Insights.

Europe represents a highly regulated and mature data privacy software market with a revenue share in 2025 driven by strong enforcement of GDPR data protection laws and digital governance frameworks. Countries such as Germany France United Kingdom and Netherlands are actively adopting privacy management platforms consent management systems and zero trust security models. European regulations emphasize strict data usage transparency cross border data control and enterprise compliance obligations across industries.

Asia Pacific Data Privacy Software Market Insights.

Asia Pacific segment holds a revenue share of about 10.65% in 2025 and is expected to grow at the fastest CAGR from 2026–2035 due to rapid digital transformation increasing internet penetration and rising data protection regulations across China India Japan and South Korea. Growth is driven by expanding cloud adoption e commerce platforms and fintech ecosystems requiring strong privacy governance. Government initiatives such as China data security laws India DPDP framework and Japan privacy reforms are supporting market expansion. Increasing investments in digital infrastructure and growing cybersecurity awareness among enterprises are further accelerating adoption of advanced data privacy software solutions across the region.

Middle East & Africa and Latin America Data Privacy Software Market Insights.

Middle East & Africa and Latin America collectively hold a revenue share in 2025 due to increasing digitalization cloud adoption and rising cyber security threats across enterprises and government institutions. Countries such as UAE Saudi Arabia South Africa Brazil and Mexico are investing in data protection frameworks enterprise security solutions and regulatory compliance systems to strengthen digital trust. Rapid expansion of e commerce fintech platforms and cloud based services is increasing the need for secure data handling. Growing awareness of data privacy cross border data regulations and rising cyberattacks is driving steady market adoption across these regions.

Market Dynamics:

Growth Drivers: Rapid digital transformation and increasing volume of enterprise data across cloud and connected ecosystems

Increased digital transformation across different sectors is leading to creation of large amounts of both structured and unstructured data on the cloud, applications, and IoT environments. Companies are also increasingly relying on cloud-based solutions, remote working environments, and AI-enabled applications, hence need to be able to protect their data. This increasing complexity of data is pushing organizations towards automated tools that can discover, classify, encrypt and monitor risks associated with data. Enterprises are therefore increasingly looking for privacy solutions to enable them use their data securely.

Restraints: Lack of skilled professionals and technical expertise in data governance and privacy management systems

The successful deployment of data privacy software will necessitate the presence of competent professionals who are versed in data governance cybersecurity compliance. But in reality, there is often a lack of professionals that are well-trained enough to competently manage privacy software and AI powered compliance programs. Lack of competence results in poor usage and ineffective management of the software. There is constant need for professional training to adapt to the latest technology trends in the area. Lack of competent professionals becomes a major constraint in developing markets.

Opportunities: Integration of artificial intelligence and automation in next generation data privacy management solutions

The implementation of technologies like artificial intelligence and machine learning has created huge possibilities in the data privacy software market space. Artificial intelligence and machine learning help in automating data discovery, categorization, risk assessment, and real-time monitoring for regulatory compliance in the organization. With the use of these technologies, it helps organizations to increase accuracy and reduce manual efforts to make wise decisions concerning data management techniques. The implementation of intelligent data security tools and predictive analytics has allowed organizations to be able to identify potential threats related to data before it is too late.

Recent Developments

-

2026: OneTrust enhanced its AI driven privacy platform by improving automated data mapping, compliance monitoring, and real time regulatory reporting across global enterprises.

-

2026: Microsoft upgraded Microsoft Purview with advanced data classification, AI based compliance automation, and stronger security controls across hybrid and cloud environments.

-

2025: BigID improved its data security posture management with automated sensitive data discovery and classification across multi cloud systems.

-

2024: Oracle strengthened its cloud data privacy framework by enhancing compliance automation and secure enterprise data governance capabilities.

Data Privacy Software Market Key Players are:

-

OneTrust

-

TrustArc

-

BigID

-

Securiti.ai

-

Osano

-

Usercentrics

-

Didomi

-

WireWheel

-

Transcend

-

Privitar

-

Spirion

-

Varonis Systems

-

IBM

-

Oracle

-

SAP

-

Salesforce

-

Informatica

-

Collibra

Data Privacy Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.50 Billion |

| Market Size by 2035 | USD 9.80 Billion |

| CAGR | CAGR of 8.12% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment Model (Cloud-based, On-premises) • By Organization Size (Small and Medium-sized Enterprises (SMEs), Large Enterprises) • By Industry Vertical (Healthcare, Financial Services, Retail and E-commerce, Information Technology (IT) and Telecom, Manufacturing, Government and Public Sector) • By Data Type (Personal Identifiable Information (PII), Non-Personal Identifiable Information (Non-PII), Sensitive Data) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | OneTrust, TrustArc, BigID, Securiti.ai, DataGrail, Osano, Usercentrics, Didomi, WireWheel, Transcend, Privitar, Spirion, Varonis Systems, IBM, Microsoft, Oracle, SAP, Salesforce, Informatica, Collibra |

Frequently Asked Questions

The data privacy software market is expected to grow at a CAGR of 8.12% from 2026 to 2035.

The data privacy software market was valued at USD 4.50 billion in 2025.

Rising demand for regulatory compliance, secure data governance, and AI driven privacy automation is driving the market.

Cloud-based segment dominated the market in 2025 due to scalable deployment and centralized data governance.

North America dominated the market in 2025 due to strong adoption of privacy software and strict regulatory frameworks.

Get in Touch