DNA Manufacturing Market Report Scope & Overview:

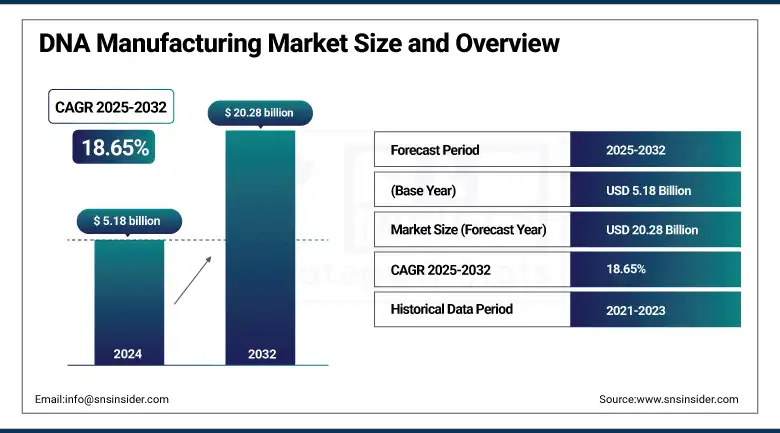

The DNA manufacturing market size was valued at USD 5.18 billion in 2024 and is expected to reach USD 20.28 billion by 2032, growing at a CAGR of 18.65% over the forecast period of 2025-2032.

The global DNA manufacturing market is growing fast, driven by the increasing applications of DNA in cell and gene therapy, vaccine development, and synthetic biology. Demand for high-quality plasmid and synthetic DNA across pharma, biotech, and research sectors is driving innovation and capacity. Automation, gene synthesis technologies, and GMP-grade manufacturing are improving scalability and speed. And biotech companies and CDMOs are investing to meet global therapeutic and research needs.

To Get more information On DNA Manufacturing Market - Request Free Sample Report

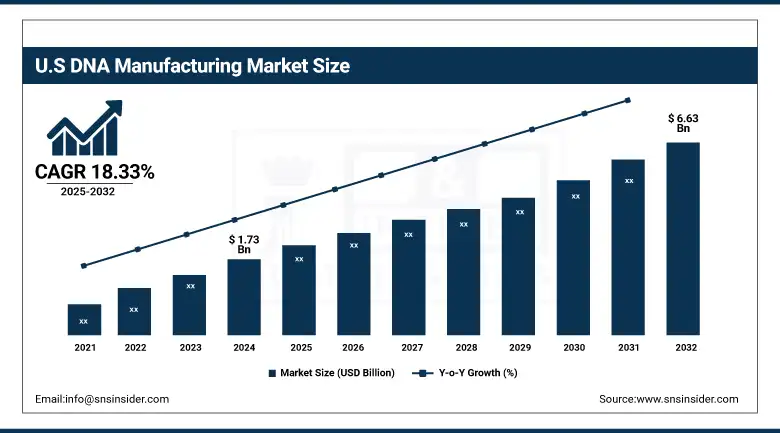

The U.S. DNA manufacturing market size was valued at USD 1.73 billion in 2024 and is expected to reach USD 6.63 billion by 2032, growing at a CAGR of 18.33% over the forecast period of 2025-2032.

The U.S. leads North America’s DNA manufacturing market due to its highly developed biotech infrastructure, strong academic and industrial research institutions, and federal support for genomics and gene therapy development. The concentration of key players such as IDT, Thermo Fisher Scientific, and Twist Bioscience, and extensive clinical and commercial applications such as mRNA vaccines and precision medicine, make it the dominant region.

Market Dynamics:

Drivers

- Expansion of Vaccine Development, Including mRNA Platforms, is Driving the Market Growth.

Global focus on rapid vaccine development, especially during and post-COVID-19 pandemic, has increased the need for high-quality DNA. Plasmid DNA is the template for RNA synthesis in mRNA vaccines. DNA vaccines, which deliver genetic material directly to cells to trigger an immune response, are gaining traction in human and veterinary medicine. As pharma companies and governments invest in faster and more scalable vaccine production technologies, demand for GMP-grade DNA used in these applications is rising globally.

In June 2025, IMUNON reported promising Phase 1 results for its DNA plasmid vaccine (IMNN-101) against COVID-19, showing six-month durability and advantages over mRNA vaccines in manufacturing and stability.

In early 2025, CEPI awarded USD 4.7 million to DNA Script to automate the enzymatic synthesis of DNA templates for mRNA vaccine production to speed up vaccine readiness, especially in the Global South regions.

- Technological Advancements in DNA Synthesis and Automation are Propelling the Market Growth

Innovations in synbio, such as enzymatic DNA synthesis, high-throughput gene assembly, and fully automated benchtop platforms (e.g., BioXp systems) have changed the DNA manufacturing landscape. These advancements mean faster turnaround times, higher sequence accuracy, and lower cost at scale. Automation reduces manual errors, increases reproducibility, and allows manufacturers to meet growing demand from multiple sectors, including therapeutics, diagnostics, and agriculture. As these technologies become more accessible and efficient, they are driving broader adoption of synthetic DNA across research and commercial use cases.

May 2025: Telesis Bio launched the Gibson SOLA enzymatic synthesis platform – an on-site reagent and software solution for high-fidelity DNA synthesis with automated workflows integrated into standard liquid-handling systems

Just a few months prior, DNA Script unveiled its SYNTAX benchtop platform for on-demand production of up to 96 oligos using enzymatic synthesis and automation to boost efficiency in research labs.

Restraint

- High Price of GMP-Grade DNA Production is Limiting the Growth of the Market

One of the major challenges of the DNA manufacturing market trends is the cost of manufacturing GMP-grade (Good Manufacturing Practice) DNA. Such DNA is crucial for clinical and commercial uses, such as some gene therapies, vaccines, and oligonucleotide drugs. Yet, the production of DNA under GMP is coupled with strict quality controls, extensive documentation, and validated cleanroom areas, and fulfills regulatory requirements through, e.g., the FDA or EMA. These demands have the effect of greatly raising production expenses relative to R&D quality DNA. As such, smaller biotech start-ups, academic institutions, and early-stage research efforts may be unable to afford or obtain GMP-grade DNA, with a contraction in market adoption and a lack of innovation, stemming from this price point challenge.

Segmentation Analysis:

By Type

The synthetic DNA segment dominated the DNA manufacturing market share in 2024, with a 71.25%, owing to its utility in genetic engineering, synthetic biology, diagnostics, and pharmaceutical research. Attention has been turned to synthetic DNA, which can be customized, more quickly manufactured, and easily scaled, making it critical for uses like vaccine production, CRISPR gene editing, and molecular diagnostics. Its use in the design of engineered DNA sequences for research and therapeutic pipelines has made it the de facto standard for laboratories and biotech firms across the globe, particularly in areas with established R&D infrastructure.

The plasmid DNA segment is anticipated to be the fastest-growing segment in the forecast period due to the rise in the application in cell & gene therapy, DNA vaccines, and mRNA production processes. With the increasing number of gene therapy clinical applications and the worldwide need for safe and effective gene delivery vectors, plasmid DNA is becoming increasingly popular in both research and commercial biomanufacturing. Prospective technologies for plasmid pcDNA or PAGE 1603 production and purification in association with the new pressure of regulatory focus on GMP quality plasmid DNA are driving adoption in pharmaceutical, biotech, or CDMO settings.

By Grade

The GMP grade segment dominated the DNA manufacturing market growth with a 68.50% market share in 2024. The dominance can be attributed to the rising requirements of clinical-grade DNA required in gene therapies, DNA vaccines, and other regulated therapeutic applications. Compliant with GMP (Good Manufacturing Practice) standards, they support high purity, safety, and traceability, crucial aspects for DNA applied to human use. Pharmaceutical and biotech companies depend on GMP-grade DNA for regulatory approval and for commercial output. The increasing number of late-stage clinical trials and commercial introductions of gene therapies also helped consolidate the dominance of this segment in the market.

The R&D Grade segment is anticipated to experience the fastest growth over the forecast period is mainly due to increased investment in early-stage research, drug discovery, and academic projects. R&D grade DNA/RNA is inexpensive and perfectly acceptable for non-clinical works; therefore often used by academic, research, or biotech start-up communities. Growing attention to synthetic biology, genome editing, and personalised medicine has driven this demand for flexible and quick-turnaround DNA synthesis solutions. With increasing innovation and research pipelines, demand for scalable, research-grade DNA synthesis is only going to continue to surge.

By Application

The DNA manufacturing market is dominated by cell & gene therapy segment in 2024 with a 46.20% market share, as the clinical and commercial demand for DNA constructs used in advanced therapies has exponentially increased. Raw materials such as plasmid and synthetic DNA are key ingredients for gene editing, viral vector production, and engineered cell therapies. The explosion of gene therapy trials and approvals around the world creates demand for high-quality, GMP-quality DNA. The pharma and biotech industries are still growing in this space, fostering cell and gene therapy’s status as the top application for DNA manufacturing.

The Oligonucleotide-based Drugs are expected to grow the fastest in the forecast years, owing to the increasing focus on precision medicine and RNA-targeted drugs. These drugs, including ASOs and siRNAs, need to be produced using custom-designed DNA templates. This segment is growing at an accelerated pace due to rising R&D investments, FDA approvals of oligo-based drugs, and widening applications in rare diseases and cancer. Further, improvements in DNA-synthesis technology are generally simplifying and speeding the manufacture of the complex oligos required for these next-generation therapeutics.

By End Use

The pharmaceutical and biotechnology companies segment accounted for the largest share of the DNA manufacturing market in 2024, with a 60.3% market share, as these are pioneers who developed and commercialized gene therapies, DNA-based vaccines, and personalized medicines. These firms need high-quality plasmid and synthetic DNA in large quantities for preclinical investigations, clinical trials, and commercial production. It is their substantial investment in R&D, their knowledge of regulatory processes, and their access to cutting-edge manufacturing technology platforms that allow them to incorporate DNA manufacturing as an integral part of their therapeutic development pipeline and therefore become the lead end-users of DNA products.

The contract research organizations (CROs) segment is expected to witness the fastest growth in the forecast years on account of the growing number of pharmaceutical and biotech companies that are outsourcing DNA manufacturing to specialized partners. CROs also provide cost-efficient and diverse services that align with short timelines for development (an important consideration in proof-of-concept work, early research, and clinical trial support). Growth of the DNA manufacturing market has also been spurred by an increasing complexity in such constructs and the requirement for GMP production, creating demand for CROs with specialisation in synthetic biology and gene therapy support, with them increasingly being adopted around the globe.

Regional Analysis:

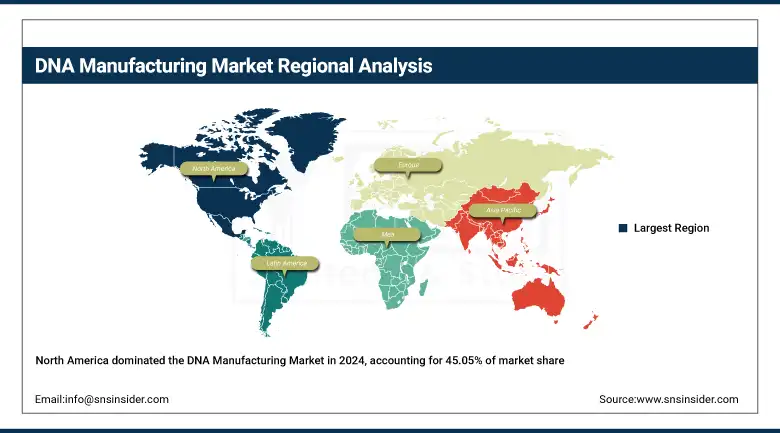

North America has led the DNA manufacturing market with a 45.05% market share in 2024, owing to the growth of the biotechnology industry in the region, the rise in investment in genetic studies, and the presence of key players such as Thermo Fisher Scientific, Integrated DNA Technologies, and Twist Bioscience. The area is heavily supported by the government, has high levels of clinical trials, and has well-defined regulations that accelerate the development and approval of DNA-based drugs. Furthermore, the widespread utilization of synthetic DNA and plasmid DNA in the field of gene therapy, vaccine development, and personalized medicine has promoted continuous requirements from both academia and commercial sectors.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific region is projected to be the fastest-growing region in the DNA manufacturing market with 19.58% CAGR during the forecast period, driven by the rising investments in life sciences, the growing biotechnology & biopharmaceutical industry in the region, and increased demand for gene-based therapies and vaccines. Other countries, including China, India, and South Korea, are quickly bolstering their strength in the field, bolstered by government policies and public-private partnerships. Expanding emphasis of the region on regionalized DNA production, in combination with an increased patient pool and augmenting clinical research, is driving the market growth in academic, pharmaceutical, and CRO spaces.

Europe is registering significant growth in the DNA manufacturing market, fueled by strong pharmaceutical and biotechnology sectors across Germany, the UK, and France. Catalent’s new plasmid DNA facility in Belgium and the installation of cutting-edge DNA synthesis platforms at Imperial College London exemplify regional expansion and academic-commercial collaboration. Key factors propelling this growth include supportive regulatory environments (e.g., EMA approvals), a robust research infrastructure at top-tier universities, and escalating demand for synthetic DNA in diverse applications such as gene therapy, diagnostics, and vaccine development. Projects such as Germany’s Elegen–GSK collaboration and the UK’s MHRA certification of 4basebio for GMP-grade DNA manufacturing further highlight Europe’s momentum in delivering advanced, high-quality DNA products.

Latin America reports moderate growth in the DNA manufacturing market analysis, which is in large part due to the growing demand for gene synthesis and molecular biology tools in academic and clinical research settings. The region is improving its biotechnology infrastructure and government-supported initiatives, which are stimulating innovation.

The Middle East and Africa are experiencing a steady growth in DNA manufacturing technologies, which is a result of increased interest in personalized medicine, synthetic biology, and genomics-based diagnostics. The growth is supported by the fact that local research institutions are teaming up with international biotech companies in countries such as the UAE, Saudi Arabia, and South Africa.

Key Market Players

DNA manufacturing companies, Thermo Fisher Scientific, Integrated DNA Technologies, GenScript Biotech Corporation, Eurofins Scientific, Twist Bioscience, Bioneer Corporation, LGC Biosearch Technologies, Quintara Biosciences, Eton Bioscience, Codex DNA (Telesis Bio Inc.), and other players.

Recent Developments

- June 2024 – GenScript Biotech Corporation, a leading synthetic biology and gene synthesis company globally, announced the release of its newest innovation, the GenScript FLASH Gene service. This extremely fast sequence-to-plasmid (S2P) platform is developed to satisfy the increasing requirement for fast, high-quality, cost-efficient gene construct delivery, further establishing GenScript's leading position in synthetic biology innovation.

- June 2024 – Thermo Fisher Scientific Inc. launched the Thermo Scientific™ KingFisher PlasmidPro Maxi Processor, the first and only complete automation solution for maxi-scale plasmid DNA purification. PlasmidPro provides end-to-end automation from mini through maxi scales, removing the requirement for manual preparation of columns while providing high-purity plasmid DNA, enabling efficient large-scale innovation in molecular biology procedures.

- October 2023 –Integrated DNA Technologies (IDT), a Danaher Corporation business, has completed its new Therapeutic Oligonucleotide Manufacturing plant in Coralville, Iowa. The plant is part of IDT's strategic growth to meet increasing global demand for next-generation nucleic acid-based therapeutics and provides high-quality manufacturing capabilities for commercial and clinical use.

DNA Manufacturing Market Report Scope:

Report Attributes Details Market Size in 2024 USD 5.18 Billion Market Size by 2032 USD 20.28 Billion CAGR CAGR of 18.65% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Type (Plasmid DNA, Synthetic DNA)

• By Grade (GMP Grade, R&D Grade)

• By Application (Cell & Gene Therapy, Vaccines, Oligonucleotide-based Drugs, Others)

• By End Use (Pharmaceutical and Biotechnology Companies, Academic & Research Institutes, Contract Research Organizations)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles Thermo Fisher Scientific, Integrated DNA Technologies, GenScript Biotech Corporation, Eurofins Scientific, Twist Bioscience, Bioneer Corporation, LGC Biosearch Technologies, Quintara Biosciences, Eton Bioscience, Codex DNA (Telesis Bio Inc.), and other players.

Frequently Asked Questions

Asia Pacific is experiencing the fastest growth in DNA manufacturing.

The “Synthetic DNA” segment dominated the DNA Manufacturing Market.

Technological advancements in DNA synthesis and automation are propelling the market growth.

The DNA Manufacturing Market was USD 5.18 billion in 2024 and is expected to reach USD 20.28 billion by 2032.

The DNA Manufacturing Market is expected to grow at a CAGR of 18.65% from 2025 to 2032.

Get in Touch