Kidney Function Tests Market Report Scope & Overview:

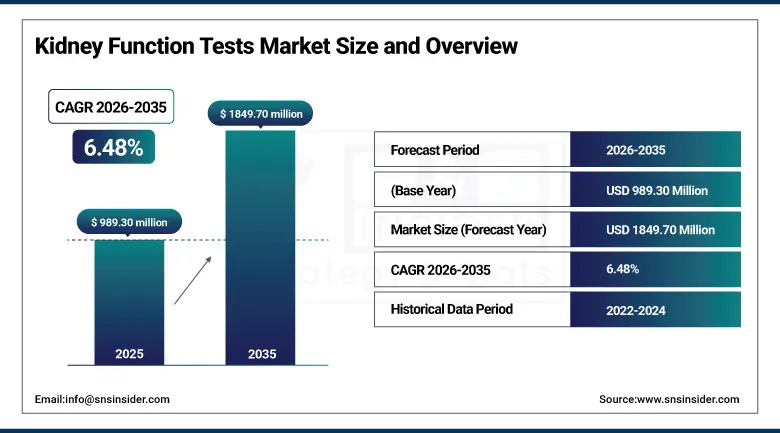

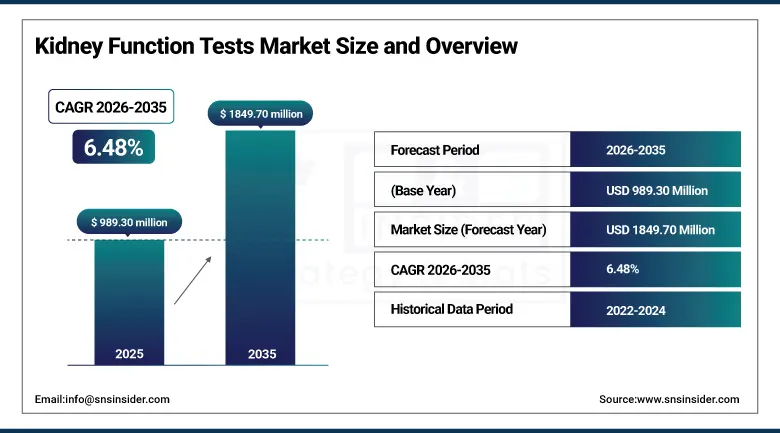

The Kidney Function Tests Market was valued at USD 989.30 Million in 2025 and is expected to reach USD 1,849.70 Million by 2035, growing at a CAGR of 6.48% from 2026–2035.

Kidney function tests are a group of diagnostic procedures used to evaluate how effectively the kidneys filter blood, remove waste products, and maintain fluid and electrolyte balance. These tests play a critical role in the detection, diagnosis, staging, and monitoring of kidney-related disorders, including chronic kidney disease (CKD), acute kidney injury, and end-stage renal disease. Commonly measured biomarkers include serum creatinine, blood urea nitrogen (BUN), estimated glomerular filtration rate (eGFR), and urine albumin-to-creatinine ratio (UACR), along with electrolyte assessments. Growing prevalence of diabetes, hypertension, and kidney disorders is driving demand for routine kidney function testing across healthcare settings worldwide.

In 2024, Roche Diagnostics launched an enhanced cobas EGFR assay panel for automated clinical analyser platforms, providing nephrologists and primary care physicians with a validated, reproducible estimated glomerular filtration rate calculation from serum creatinine and cystatin C inputs whose dual-biomarker approach improves eGFR accuracy in the CKD 3a range where single-biomarker creatinine-based eGFR is least reliable and where accurate staging most critically determines treatment intensity and referral decisions.

Market Size and Forecast

-

Market Size in 2026E: USD 1,053.40 Million

-

Market Size by 2035: USD 1,849.70 Million

-

CAGR: 6.48% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

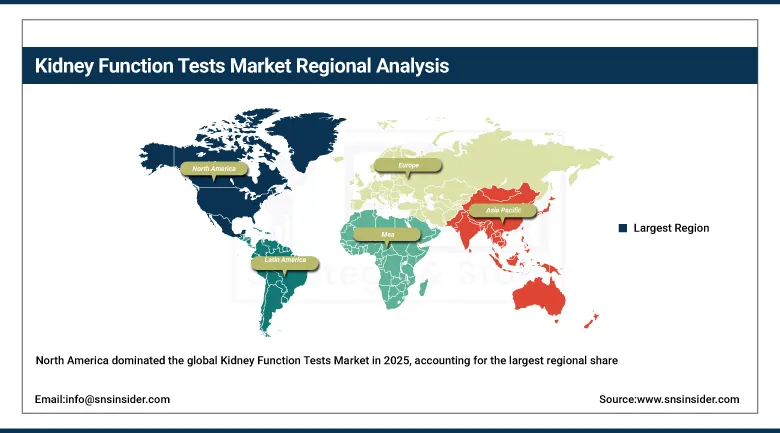

Largest Region: North America

To Get more information on Kidney Function Tests Market - Request Free Sample Report

Kidney Function Tests Market Trends

-

Point-of-care kidney function testing is expanding access to rapid creatinine and eGFR assessment in primary care, emergency, and remote healthcare settings

-

Novel biomarkers such as cystatin C, NGAL, and KIM-1 are improving early detection of kidney disease before traditional markers indicate significant damage

-

Automated urinalysis systems are gaining adoption by providing faster, standardized, and high-throughput kidney function screening and monitoring

-

Home-based kidney monitoring technologies are enabling patients to track renal health remotely through connected testing devices and digital health platforms

-

Artificial intelligence is enhancing kidney function test interpretation by supporting automated disease staging, trend analysis, and clinical decision-making processes

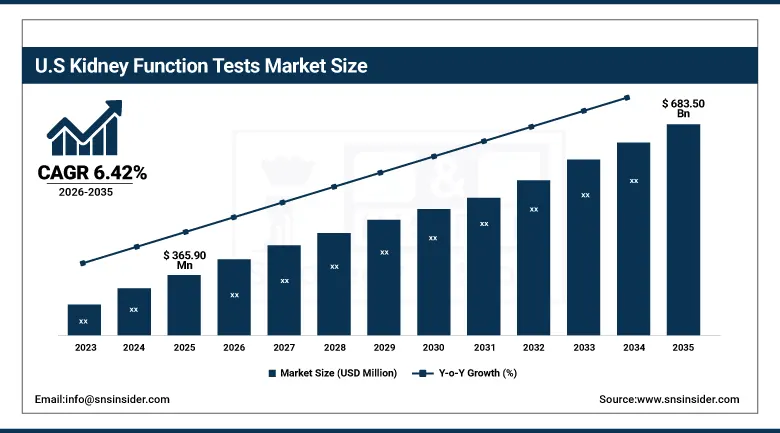

U.S. Kidney Function Tests Market Outlook

The U.S. Kidney Function Tests Market was valued at approximately USD 365.90 Million in 2025 and is expected to reach approximately USD 683.50 Million by 2035, growing at a CAGR of approximately 6.42%.

The United States kidney function tests market is driven by the extraordinary scale of the domestic chronic kidney disease burden, where the CDC estimates 37 million Americans live with CKD and a further 40 million are at elevated risk, creating both the clinical urgency and the insurance-covered diagnostic utilisation that sustains the world's largest national kidney function test market. The KDIGO CKD management guidelines' recommendation of annual kidney function monitoring for all diabetic and hypertensive patients creates a structurally large and guideline-mandated testing volume whose compliance across the U.S. primary care population generates consistent laboratory test procurement.

In 2025, Siemens Healthineers expanded its ADVIA laboratory analyser portfolio with an enhanced kidney function biomarker panel incorporating cystatin C, beta-2 microglobulin, and urinary albumin alongside standard creatinine and BUN assays, enabling clinical laboratories to provide comprehensive CKD staging and monitoring from a single automated test run.

Kidney Function Tests Market Segment Analysis

-

By Test Type, the Blood Tests segment dominated the Kidney Function Tests Market with approximately 64.80% share in 2025, while the Urine Tests segment is the fastest growing.

-

By Product, the Reagents & Kits segment dominated the Kidney Function Tests Market with approximately 68.50% share in 2025, while the Instruments & Analysers segment is the fastest growing.

-

By End User, the Hospitals segment dominated the Kidney Function Tests Market with approximately 47.00% share in 2025, while the Diagnostic Laboratories segment is the fastest growing.

By Test Type, blood tests dominate, urine tests grow fastest

Blood tests retained the dominant test type position in 2025, reflecting the foundational clinical status of serum creatinine measurement as the universal initial kidney function assessment whose ordering frequency across primary care, emergency medicine, pre-operative assessment, and nephrology clinic encounters creates the highest test volume of any kidney function biomarker category. Blood tests encompass serum creatinine whose concentration directly determines eGFR calculation, blood urea nitrogen whose ratio to creatinine provides differential diagnostic information about pre-renal versus intrinsic renal azotemia, comprehensive metabolic panel electrolyte assessment whose sodium, potassium, and bicarbonate values reveal tubular dysfunction in advanced CKD, and the growing cystatin C measurement whose improved eGFR accuracy in elderly and low muscle mass patients is progressively becoming standard for CKD confirmation staging in clinical nephrology.

Urine tests are growing fastest as the expanded clinical recognition of proteinuria as both an early CKD detection marker and an independent cardiovascular risk factor is driving guidelines across diabetes, hypertension, and nephrology care programmes to mandate annual urine albumin-to-creatinine ratio testing in all at-risk patients. Point-of-care urine test strips providing semi-quantitative protein and creatinine measurements within minutes are expanding urine testing from central laboratory settings into primary care offices and community pharmacy settings where accessibility and immediacy improve screening programme participation rates among patient populations with limited specialist access.

By End User, hospitals dominate, diagnostic laboratories grow fastest

Hospitals retained the dominant end user position with approximately 47% of the kidney function tests market in 2025. Their commercial leadership reflects the volume concentration of kidney function testing in inpatient settings where comprehensive metabolic panel ordering is standard admission assessment across medical, surgical, and critical care specialties whose patient populations include the highest-acuity CKD and acute kidney injury presentations requiring intensive monitoring. Hospital-based nephrology departments managing haemodialysis programmes, kidney transplant recipients, and complex CKD patients create specialised testing demand whose analytical breadth and frequency per patient exceeds what primary care monitoring generates, sustaining hospital laboratory procurement as the highest per-facility value kidney function testing market.

Diagnostic laboratories are the fastest-growing end user because the progressive shift of routine healthcare from inpatient to outpatient delivery, combined with growing patient preference for convenient standalone diagnostic service access without hospital registration requirements, is creating volume migration from hospital to independent laboratory settings whose operational efficiency, competitive pricing, and extended access hours attract both physician referral and direct patient utilisation. The growth of chronic disease management programmes for diabetes and hypertension whose kidney function monitoring protocols generate recurring annual test orders is creating a predictable recurring revenue stream for diagnostic laboratories whose operational economics are well-suited to high-volume standardised testing.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Kidney Function Tests Market Insights

North America dominated the global Kidney Function Tests Market in 2025, accounting for the largest regional share. The United States accounts for approximately 82.5% of North American revenues through the combination of the world's highest CKD prevalence among major economies, driven by the epidemic scales of type 2 diabetes and hypertension that constitute the leading CKD risk factors, the most comprehensive third-party insurance reimbursement for preventive kidney function monitoring, and the commercial concentration of major clinical analyser and assay manufacturers whose U.S. sales sustain regional market leadership.

Canada contributes supplementary demand through its provincial health system's kidney disease management programmes whose annual creatinine and urinalysis monitoring for diabetic and hypertensive patients creates consistent test volume across primary care networks.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Kidney Function Tests Market Insights

Europe held a significant share of the global Kidney Function Tests Market in 2025. Germany, France, the United Kingdom, Italy, and Spain are the leading national markets whose universal healthcare coverage, well-developed nephrology clinical infrastructure, and CKD disease management programmes create consistent and clinically guideline-driven kidney function test demand.

Germany accounts for approximately 28.5% of European revenues through its large clinical laboratory network, the commercial presence of Siemens Healthineers and Roche Diagnostics whose European headquarters sustain regional market development, and the German nephrology specialty's active CKD early detection programme adoption.

The European Renal Best Practice guidelines' quantitative targets for CKD monitoring frequency and eGFR-based staging create a regulatory and clinical standard framework that sustains kidney function test volume across European healthcare systems independent of individual country healthcare budget variability. The EU's growing population of elderly individuals with multiple comorbidities including diabetes and cardiovascular disease creates an expanding CKD-risk population whose annual monitoring requirements sustain above-GDP kidney function test market growth across member states.

Asia Pacific Kidney Function Tests Market Insights

Asia Pacific is the fastest-growing regional Kidney Function Tests Market, driven by the world's largest and fastest-growing diabetic population whose CKD risk creates an enormous kidney function monitoring requirement that is progressively being served by expanding diagnostic laboratory infrastructure, increasing health insurance coverage, and growing awareness of CKD as a preventable condition whose early detection changes clinical outcomes.

China accounts for approximately 38.5% of Asia Pacific revenues through its estimated 130 million CKD patients representing the world's largest national CKD population, the progressive expansion of clinical laboratory testing access across tier 2 and tier 3 city hospital networks, and the growing adoption of health examination packages that include comprehensive metabolic panel testing.

India is the most commercially dynamic emerging market within Asia Pacific where the rapid expansion of diagnostic laboratory chains including Dr Lal PathLabs, Metropolis Healthcare, and Thyrocare is progressively providing standardised, quality-accredited kidney function testing at accessible pricing across urban populations whose growing health awareness and insurance coverage are creating above-average diagnostic test utilisation growth.

MEA & Latin America Kidney Function Tests Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its world-class hospital infrastructure, the Dubai Health Authority's preventive health screening programmes that include kidney function assessment, and the large expatriate population whose health insurance coverage includes comprehensive metabolic panel testing as standard annual check-up components. Saudi Arabia contributes growing demand through its high diabetes and hypertension prevalence among its adult population and the Vision 2030 healthcare investment programme whose disease management focus includes non-communicable disease monitoring.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through the large diabetes and hypertension patient populations whose CKD risk creates substantial kidney function monitoring demand across both the public SUS health system and the growing private health insurance sector. Mexico and Colombia are growing secondary markets where expanding diagnostic laboratory networks, increasing health insurance penetration, and growing chronic disease management programme adoption are creating above-regional-average kidney function test market growth.

Market Dynamics

Growth Drivers: Global chronic kidney disease epidemic driven by diabetes and hypertension creating non-discretionary monitoring demand

The kidney function tests market is experiencing sustained growth due to the rising global prevalence of chronic kidney disease (CKD), which is closely linked to increasing rates of diabetes, hypertension, obesity, and aging populations. As these risk factors continue to expand worldwide, a growing number of individuals require routine kidney health assessments for early disease detection and ongoing monitoring. Clinical guidelines recommending regular kidney function testing for high-risk populations are further contributing to consistent demand across healthcare systems.

Another major growth driver is the increasing emphasis on early diagnosis and preventive care. Early identification of kidney dysfunction enables timely treatment interventions that can slow disease progression and reduce the risk of end-stage renal disease. Growing adoption of advanced therapies for kidney disease, combined with expanding screening programs and improved healthcare awareness, is encouraging wider use of kidney function tests in hospitals, diagnostic laboratories, and primary care settings.

Restraints: Limited CKD awareness in primary care settings and diagnostic infrastructure gaps in low-resource healthcare environments constraining early detection and monitoring programme implementation

An important obstacle that needs to be overcome in the case of the kidney function test industry is the under-diagnosis of chronic kidney disease even though there is substantial clinical evidence that early diagnosis is critical. Patients may discover they have the condition only after they reach the advanced stage of kidney damage. The lack of proper screening guidelines, the inconsistency in following such guidelines, and the lack of monitoring in at-risk groups can significantly limit the effectiveness of such screening programs.

Another problem is the limited access to the necessary infrastructure in rural areas or other regions that lack the capacity. Geographic barriers, lack of laboratories to perform the tests, and insufficient healthcare infrastructure can make it difficult for individuals to undergo regular tests for kidney function.

Opportunities: Point-of-care kidney function testing expansion and novel biomarker adoption enabling earlier CKD detection than creatinine-based testing currently achieves

One promising growth opportunity for the market is the introduction of point-of-care kidney function testing which facilitates quick evaluation of creatinine and eGFR from unconventional settings. Portable testing machines make it possible for primary care facilities, urgent care clinics, community pharmacies, as well as rural healthcare centers to conduct tests and provide rapid diagnostic services. Such an expansion may contribute to early disease detection and increased engagement in screening.

Advanced renal biomarkers that provide more accurate diagnosis and early detection of renal damage represent another potential area for growth for the industry. Such biomarkers include cystatin C, neutrophil gelatinase-associated lipocalin (NGAL), and kidney injury molecule-1 (KIM-1). These tests have shown promise for diagnosing kidney dysfunction prior to changes in traditional markers. With growing body of evidence, the adoption of biomarker tests among labs and providers would result in new business opportunities in the field.

Recent Developments:

-

2025: Siemens Healthineers expanded its ADVIA analyser kidney function biomarker panel with cystatin C, beta-2 microglobulin, and urinary albumin alongside standard creatinine and BUN assays, enabling comprehensive CKD staging from a single automated test run and addressing creatinine-only eGFR accuracy limitations in elderly patients.

-

2024: Roche Diagnostics launched an enhanced cobas EGFR assay panel providing dual-biomarker eGFR calculation from serum creatinine and cystatin C inputs whose improved accuracy in the clinically critical 45-60 mL/min/1.73m² range addresses the diagnostic gap where CKD staging most critically determines treatment intensity decisions.

-

2023: Abbott Laboratories introduced the i-STAT Alinity point-of-care creatinine testing panel for emergency department and critical care settings, enabling bedside eGFR assessment within 10 minutes for acute kidney injury evaluation and drug dosing adjustment in time-sensitive clinical scenarios where central laboratory turnaround is insufficient.

Kidney Function Tests Market Key Players

-

Roche Diagnostics (Roche Holding AG)

-

Siemens Healthineers AG

-

Abbott Laboratories

-

Thermo Fisher Scientific Inc.

-

Danaher Corporation (Beckman Coulter)

-

bioMérieux SA

-

Sysmex Corporation

-

QIAGEN NV

-

Randox Laboratories Ltd.

-

Arkray Inc.

-

Nova Biomedical Corporation

-

Ortho Clinical Diagnostics (QuidelOrtho)

-

Radiometer Medical ApS (Danaher)

-

EKF Diagnostics Holdings PLC

-

Mindray Medical International Ltd.

-

Dirui Industrial Co. Ltd.

-

Contec Medical Systems Co. Ltd.

-

IDEXX Laboratories Inc.

-

Clinical Diagnostic Solutions Inc.

-

Urit Medical Electronic Co. Ltd.

Kidney Function Tests Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 989.30 Million |

| Market Size by 2035 | USD 1849.70 Million |

| CAGR | CAGR of 6.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Test Type (Blood Tests, Urine Tests, Imaging Tests, Biopsy Tests) • by Product (Reagents & Kits, Instruments & Analysers, Services) • by End User (Hospitals, Diagnostic Laboratories, Research Laboratories & Institutes, Home Care Settings) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Roche Diagnostics (Roche Holding AG), Siemens Healthineers AG, Abbott Laboratories, Thermo Fisher Scientific Inc., Danaher Corporation (Beckman Coulter), bioMérieux SA, Sysmex Corporation, QIAGEN NV, Randox Laboratories Ltd., Arkray Inc., Nova Biomedical Corporation, Ortho Clinical Diagnostics (QuidelOrtho), Radiometer Medical ApS (Danaher), EKF Diagnostics Holdings PLC, Mindray Medical International Ltd., Dirui Industrial Co. Ltd., Contec Medical Systems Co. Ltd., IDEXX Laboratories Inc., Clinical Diagnostic Solutions Inc., Urit Medical Electronic Co. Ltd. |

Frequently Asked Questions

The Kidney Function Tests Market is expected to grow at a CAGR of 6.48% from 2026 to 2035.

Global CKD epidemic driven by type 2 diabetes and hypertension creating non-discretionary annual monitoring demand.

The Blood Tests segment dominated the Kidney Function Tests Market with the largest share in 2025.

North America dominated the Kidney Function Tests Market in 2025, with the United States accounting for approximately 82.5% of North American revenues.

Get in Touch