Flexible PCB Market Report Scope & Overview:

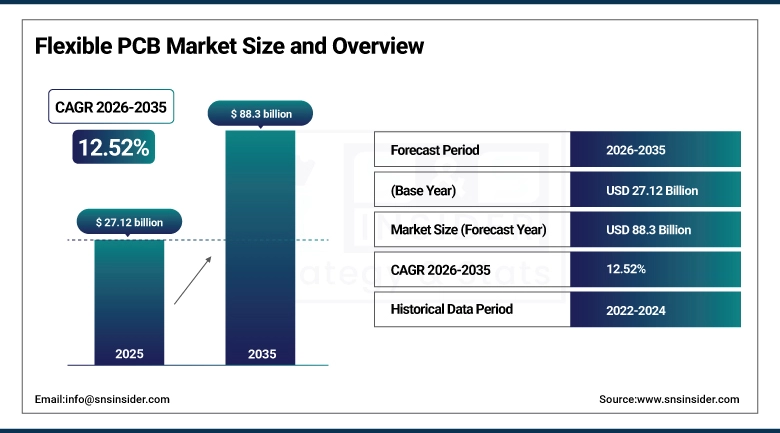

The Flexible PCB Market was valued at USD 27.12 billion in 2025 and is expected to reach USD 88.3 billion by 2035, growing at a CAGR of 12.52% from 2026–2035.

The Flexible PCB Market is experiencing growth due to the rise in the demand for smaller, lighter, and more efficient electronic components used in various products ranging from consumer goods to automobiles and healthcare industries. FPCBs are becoming an integral component of mobile phones, watches, flexible phones, and even sophisticated electronic components such as autonomous driving assistance system and batteries for electric vehicles. Technologies such as 5G, IoT, and AI have opened up new areas where they can be used while technologies like additive printing and laser direct imaging are enhancing their efficiency and reducing manufacturing costs.

Additionally, industry insights indicate that flexible PCBs are gaining preference over rigid printed circuit boards in electronics design with limited space, especially when it comes to miniaturizing electronic devices.

Flexible PCB Market Size and Forecast

-

Market Size in 2025: USD 27.12 Billion

-

Market Size by 2035: USD 88.3 Billion

-

CAGR: 12.52% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Flexible PCB Market - Request Free Sample Report

Flexible PCB Market Trends

-

Fast pace of miniaturization in consumer electronics products increasing demand for flexible PCBs that can be thin and light.

-

High usage of flexible PCBs in battery packs of electric vehicles, advanced driver-assistance systems, and infotainment systems boosting market growth in the automotive industry.

-

Constructions of new 5G networks and deployment of millions of Internet-of-Things devices stimulating demand for flexible PCBs in the telecom infrastructure.

-

Usage of flexible PCBs in various wearable healthcare devices, medical implants, and portable diagnostic equipment driving market growth in the medical industry.

-

Recent developments in the manufacturing process of multi-layer flexible PCBs leading to high density of circuits and efficient thermal management.

-

Increased usage of rigid-flexible PCBs in aerospace and defense industries due to their high performance in harsh conditions.

-

Massive investments in additive manufacturing and laser direct imaging technologies cutting down production costs.

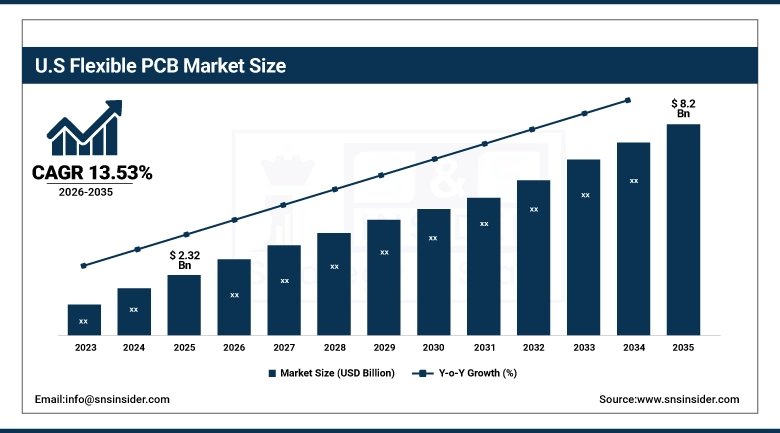

U.S. Flexible PCB Market was valued at USD 2.32 billion in 2025 and is expected to reach USD 8.2 billion by 2035, registering a CAGR of 13.53% during 2026–2035.

The U.S. Flexible PCB market is among the rapidly growing markets within the region, owing to the rise in demand from aerospace and defense, medical devices, 5G telecommunication infrastructures, and highly advanced automotive electronic products. The major defense manufacturers such as Lockheed Martin and Raytheon Technologies are increasingly using rigid-flexible PCBs in their military systems, whereas companies like Cisco Systems and Qualcomm Technologies are propelling the demand for high-end FPCBs in next generation telecommunication and Internet of Things (IoT) products.

Growing investments by U.S.-based technology companies in research & development activities on wearable health monitors, autonomous vehicles, and edge computing AI enabled devices are anticipated to drive the demand for flexible PCB components during the forecast period.

Flexible PCB Market Segment Insights

-

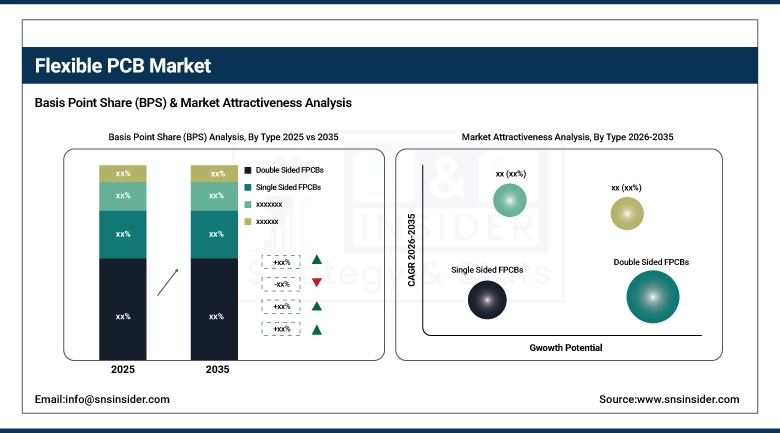

Based on Type, Double Sided FPCBs accounted for the largest market share (~42%) in 2025; Multilayer FPCBs expected to be the fastest-growing segment (CAGR).

-

Based on End Use, Consumer Electronics accounted for the largest market share (~49%) in 2025; IT & Telecom expected to be the fastest-growing segment (CAGR).

Flexible PCB Market Segment Analysis

By Type, Double Sided FPCBs dominate the Flexible PCB Market, Multilayer FPCBs segment expected to grow fastest

The Double Sided FPCB segment dominated the market in terms of share in 2025 with approximately 42% of the market. Flexible circuits featuring two sides of complex electronic design in addition to cost efficiency are popular due to their ability to facilitate high levels of circuit integration on either side of the material, and at the same time, their affordability and space-saving capabilities make them ideal for consumer electronics, automotive assemblies, and industrial applications. Their ease of manufacturing, capability to perform and low cost of production make them perfect for large-scale assembly in electronics industry.

Multilayer FPCB segment is estimated to witness the fastest CAGR over 2026 to 2035 forecast period. The requirement of miniaturization of products coupled with electrical efficiency and thermal stability in small products like smart phones, medical gadgets, aircrafts and communication equipment like 5G technology makes multilayer flexible PCBs extremely suitable for use in these applications.

By End Use, Consumer Electronics segment dominates the Flexible PCB Market, IT & Telecom segment expected to grow fastest

The Consumer Electronics segment led the Flexible PCB market in 2025 with approximately 49% of total market revenue. The unrelenting consumer demand for thinner, lighter, and more feature-rich devices such as smartphones, tablets, laptops, smartwatches, and foldable displays is the primary driver. As consumer electronics manufacturers continue to push the boundaries of device form factors, flexible PCBs have become a foundational enabling technology, providing reliable electrical connections in highly compact and often curved or foldable form factors. The continued evolution toward smart wearable terminals is expected to sustain strong FPCB demand across this segment.

The IT & Telecom market is expected to exhibit the highest CAGR between 2026 and 2035 due to the extensive installation of 5G technology across the world, rising spending on data centers, and growing demand for high-speed communication products. The development of 5G base stations, small cells, and network hardware involves the use of flexible PCBs that can handle higher frequencies and signal complexities. Furthermore, the growing use of Internet of Things (IoT) devices and edge computing networks is continuously generating demand for FPCBs.

Flexible PCB Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~82% |

|

Europe |

Germany |

~28% |

|

Asia Pacific |

China |

~58% |

|

Middle East & Africa |

UAE |

~33% |

|

Latin America |

Brazil |

~50% |

Asia Pacific Flexible PCB Market Insights

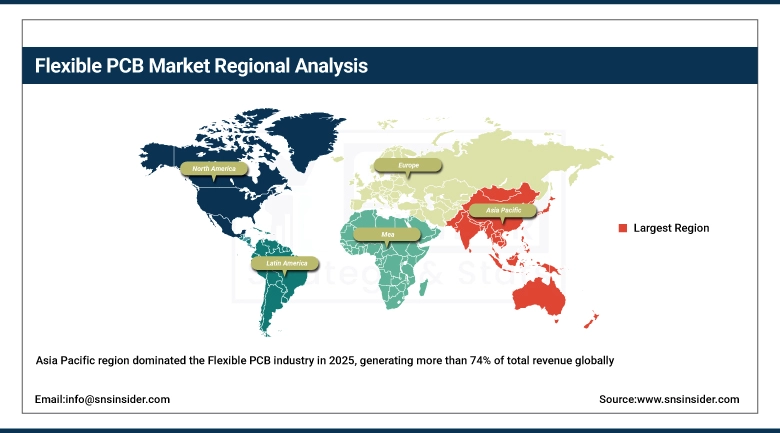

The Asia Pacific region dominated the Flexible PCB industry in 2025, generating more than 74% of total revenue globally. This is largely due to the presence of a well-integrated electronics manufacturing base that includes the top manufacturers of flexible printed circuit boards in China, Japan, South Korea, and Taiwan. Samsung Electronics, Sony, and Foxconn, among others, depend on flexible PCBs imported from the region to manufacture their most advanced consumer electronic products, such as mobile phones, smartwatches, and OLED displays. The burgeoning development of electric vehicles, along with rising domestic demand for wearable technologies in China, Japan, and South Korea, is set to continue boosting the dominance of Asia Pacific as the world's biggest producer and consumer of flexible PCBs during the projected 2026-2035 timeframe.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Flexible PCB Market Insights

North America will be registering the highest CAGR compared to other regions for the period from 2026 to 2035, driven by continuous growth in the aerospace and defense sectors, sophisticated medical equipment, 5G technology, and next-generation electronics in automobiles. The United States is the largest source of revenue generation in the region, which is facilitated by high investment in research and development by technology, defense, and health sector companies. Efforts for onshoring of electronic products along with support from governments in terms of various programs to boost semiconductors and electronics industries will boost local production of FPCBs.

Europe Flexible PCB Market Insights

Europe held a significant share of the Flexible PCB market in 2025, with Germany leading regional demand on the strength of its world-class automotive manufacturing sector and advanced industrial electronics base. European automakers and Tier-1 automotive suppliers are among the largest consumers of high-reliability flexible and rigid-flex PCBs for ADAS, EV power electronics, and in-vehicle infotainment systems. The region's strong aerospace and defense industry, particularly in Germany, France, and the UK, is also a notable driver. Stringent environmental regulations are encouraging the adoption of lead-free and RoHS-compliant flexible PCB materials, driving innovation among European manufacturers.

Middle East & Africa and Latin America Flexible PCB Market Insights

The Middle East & Africa and Latin America segments for flexible printed circuit boards are at a relatively early stage of development compared to others, although they are expected to experience steady growth up to 2035. These segments will be driven by the increase in the use of consumer electronics products, increasing telecommunications infrastructure investments, and efforts towards modernization of the industry. The major markets in the Middle East & Africa segment are expected to be the UAE and Saudi Arabia due to their smart cities projects and increasing demand for electronics products in the energy and industrial sectors.

Flexible PCB Market Growth Drivers:

-

Rising demand for miniaturized, high-performance electronics across consumer, automotive, and medical sectors

The main driver that stimulates the development of the Flexible PCB market is constantly emerging demand for the reduction in the size of electronic devices. The desire for smaller smartphones, folding displays, and wearable devices makes consumer electronics producers utilize flexible circuit boards enabling them to be curved and installed in non-planar spaces. Growth of the electric vehicles market, advanced driver assistance system (ADAS), and telematics leads to a higher content of FPCB per vehicle since there is a need for high-density wiring not provided by rigid PCBs. Additionally, implantable medical devices, wearable diagnostics, and portable health monitoring devices require flexible PCBs for implementation.

Statistics on FPCB per device reveal the tendency of the increasing number of flexible PCBs per unit in all applications. Thus, the number of flexible PCBs per smartphone rises due to growing capabilities of devices. Also, the transition from traditional harness wiring of the automotive industry to flexible printed circuits is predicted to reduce vehicle weight and enhance production efficiency.

Flexible PCB Market Restraints

-

High manufacturing complexity and elevated production costs compared to rigid PCB alternatives

An important factor limiting the growth in the flexible PCB industry is the relatively higher manufacturing difficulty and expense involved in producing FPCBs than that of rigid PCBs. Special materials used in flexible circuit boards include polyimide substrates, adhesive-free laminate, and flexible copper foils, which tend to be significantly more expensive than conventional FR-4 rigid printed circuit board materials. Furthermore, the manufacture of flexible circuit boards also calls for strict control in process, special equipment handling, and inspection procedures to avoid any damage in the manufacturing process. This would result in higher capital expenses for flexible PCB manufacturers and hinder the rapid expansion of their capacity, especially for smaller companies. In certain price-sensitive industries, the premium over rigid PCBs could become an obstacle to adoption.

Flexible PCB Market Opportunities

-

Expanding applications in flexible hybrid electronics, medical implants, and next-generation foldable devices

The synergy of developments in flexible circuit boards with other technological trends like FHE, stretchable electronics, and new foldable consumer electronics is one of the most promising growth factors in the industry's future development. The growing popularity of foldable mobile phones, rollable displays, and flexible OLED displays means that there will be an ever-increasing demand for flexible PCBs that maintain their performance at millions of flex operations with no decline in signal quality. In the healthcare segment, the expansion of flexible and bioelectronic devices such as neural interfaces, wearable ECG monitors, and glucose monitors creates a very profitable niche where flexible boards can generate more revenues than in conventional consumer electronics segments. Finally, current government-funded research aimed at developing flexible and printed electronics in the sphere of military applications, aerospace, and smart fabrics is also a possible source of orders for flexible PCBs before 2035.

Recent Developments:

-

2025 (July): Sumitomo Electric Industries (SEI) allocated USD 27.4 million in two projects in relation to its manufacturing process of flexible circuit boards in Hanoi, Vietnam via SEI Electronic Components (Vietnam) Co., Ltd. Such allocation involved the development of its export-oriented production capacity as a response to the increased demand for HDI flexible PCBs.

-

2024 (November): In relation to Murrietta Circuits, Excellon Cobra Hybrid Laser System was introduced into their manufacturing processes to improve precision when drilling microvias for HDI flexible PCBs with the help of two lasers.

Flexible PCB Market Key Players

Some of the Flexible PCB Market Companies are:

-

Nippon Mektron

-

Zhen Ding Technology Holding Ltd.

-

Sumitomo Electric Industries

-

Interflex Co. Ltd.

-

Career Technology (Mfg.) Co., Ltd.

-

Ichia Technologies Inc.

-

Multi-Fineline Electronix, Inc. (MFLEX)

-

NewFlex Technology Co., Ltd.

-

FLEXium Interconnect, Inc.

-

Daeduck GDS

-

SIFlex Co., Ltd.

-

BHflex Co., Ltd.

-

Interconnect Systems Inc.

-

Samsung Electro-Mechanics

-

Nitto Denko Corporation

Flexible PCB Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.12 Billion |

| Market Size by 2035 | USD 88.3 Billion |

| CAGR | CAGR of 12.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Single Sided FPCBs, Double Sided FPCBs, Multilayer FPCBs, Rigid-Flex PCBs, Others) • By End Use (Industrial Electronics, Aerospace & Defense, IT & Telecom, Automotive, Consumer Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Nippon Mektron, Zhen Ding Technology Holding Ltd., Sumitomo Electric Industries, Interflex Co. Ltd., Career Technology (Mfg.) Co., Ltd., Ichia Technologies Inc., Multi-Fineline Electronix, Inc. (MFLEX), NewFlex Technology Co., Ltd., FLEXium Interconnect, Inc., Daeduck GDS, SIFlex Co., Ltd., BHflex Co., Ltd., Interconnect Systems Inc., Samsung, Electro-Mechanics, Nitto Denko Corporation |

Frequently Asked Questions

Asia Pacific dominated the Flexible PCB Market in 2025, commanding over 74% of global market revenue, anchored by leading electronics manufacturing hubs in China, Japan, South Korea, and Taiwan.

The Consumer Electronics segment dominated the Flexible PCB Market in 2025, accounting for approximately 49% of total market revenue.

The Double Sided FPCBs segment dominated the Flexible PCB Market in 2025.

The rising demand for miniaturized, lightweight, and high-performance electronics across consumer devices, electric vehicles, ADAS systems, 5G infrastructure, and medical devices.

The Flexible PCB Market was valued at USD 27.12 billion in 2025.

The Flexible PCB Market is expected to grow at a CAGR of 12.52% from 2026 to 2035.

Get in Touch