Gaming Market Report Scope & Overview:

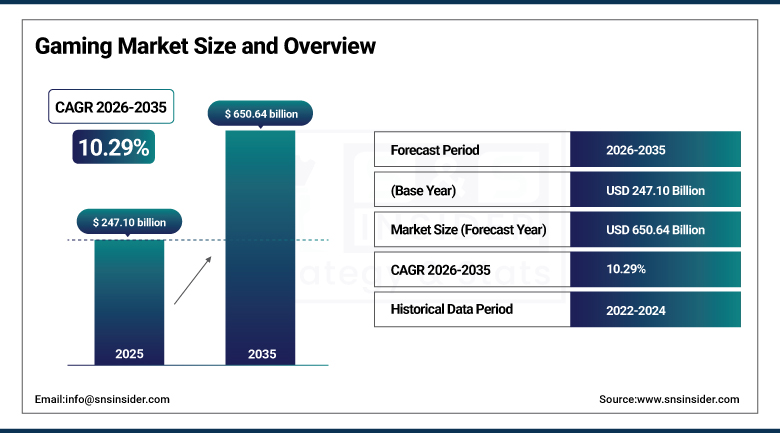

The Gaming Market was valued at USD 247.10 billion in 2025 and is expected to reach USD 650.64 billion by 2035, growing at a CAGR of 10.29% from 2026-2035.

The Gaming Market is witnessing healthy market growth as a result of rising consumer preferences towards immersive, accessible, and mobile-first gaming experiences. Advances in cloud gaming, augmented/ virtual reality, AI-based personalization, and improved distribution systems will keep driving gamer engagements across multiple channels including mobile, console, PC, and streaming. Rising worldwide demand for interactive content, professional gaming events, and connectivity will fuel continuous uptake of gaming activities among both casual gamers and hardcore professionals.

Worldwide, the number of gamers is projected to reach about 3.5-3.8 billion people within the period of 2025-2026, mostly owing to increased smartphone usage in developing countries, rising Internet access, and gaming acceptance as mainstream entertainment for everyone irrespective of age. Mobile gaming remains the primary entry point for most new gamer engagements.

Furthermore, the global esports landscape is witnessing steady growth, with esports viewership estimated to exceed around 650-700 million people within the period of 2025, fueled by rising sponsorships, partnerships with live-streaming platforms (e.g., Twitch, YouTube Gaming), and league tournaments of popular game genres including FPS, MOBA, and sport simulation games.

Gaming Market Size and Forecast

-

Market Size in 2025: USD 247.10 Billion

-

Market Size by 2035: USD 650.64 Billion

-

CAGR: 10.29% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Gaming Market - Request Free Sample Report

Gaming Market Trends

-

Mobile gaming remains the leader due to the low costs of smartphones and internet access, being the largest category globally.

-

Cloud gaming is rapidly gaining popularity as users embrace 5G technology, which allows for uninterrupted playing without costly hardware.

-

Esports have become popular due to professional tournaments and streaming events, contributing to additional income streams.

-

Game subscriptions have become increasingly popular, as evidenced by Xbox Game Pass and PlayStation Plus.

-

Gaming with AR and VR technology is becoming more common, opening up a new world of interactive entertainment.

-

The application of artificial intelligence in creating personalized gaming experiences for players is becoming increasingly important.

-

Cross-platform gaming, which allows gamers to interact on different platforms, is fast becoming the norm.

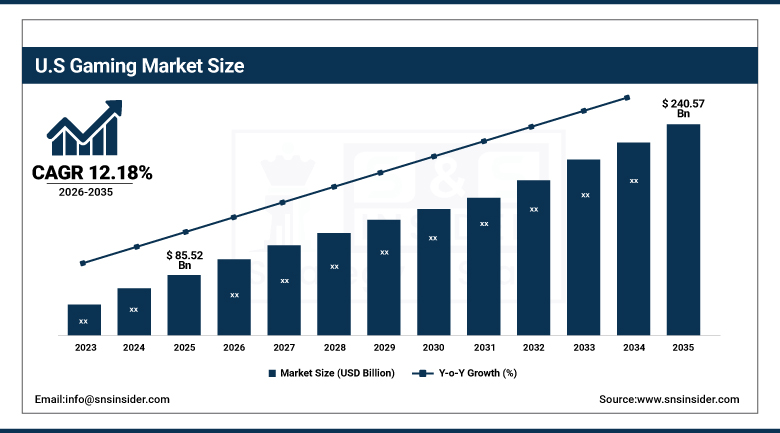

U.S. Gaming Market was valued at USD 85.52 billion in 2025 and is expected to reach USD 240.57 billion by 2035, growing at a CAGR of 12.18% from 2026-2035.

The US gaming market continues to be the largest gaming market in the world thanks to its well-developed digital infrastructure, significant purchasing capacity among consumers, and extensive console, PC, and subscription-based gaming models. Major ecosystem players include Microsoft (Xbox), Sony (PlayStation), Nintendo, Electronic Arts, Activision Blizzard (a Microsoft company), Epic Games, and Take-Two Interactive, which drive innovation in AAA game development and in live service gaming ecosystems.

Monetization frameworks that include subscription-based games (Xbox Game Pass, PlayStation Plus), in-game purchases, and free-to-play models supported by ads continue to drive rapid growth in revenues. The adoption of cloud-based gaming platforms (Xbox Cloud Gaming, NVIDIA GeForce NOW) is decreasing hardware requirements and making gaming available to consumers with lower spec machines. Such a trend is supported by an exceptionally engaged audience.

Video gaming in the US attracts about 65%-70% of adults, with mobile gaming being the main entrance gateway into video gaming, while consoles and PC games provide better opportunities for monetization of higher-value customers. Moreover, rising interest in esports and streaming on platforms like Twitch and YouTube Gaming is making video games less of a niche industry and more of a popular form of entertainment.

Gaming Market Segment Highlights

-

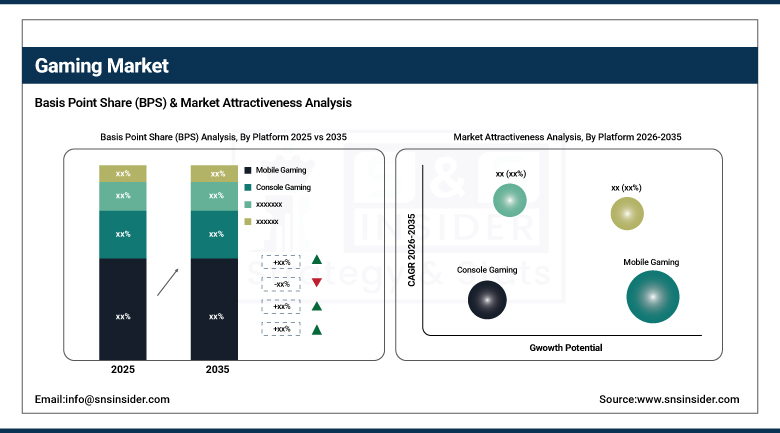

By Platform, Mobile Gaming dominated the Gaming Market with 72.36% share in 2025; Cloud Gaming fastest growing (CAGR).

-

By Revenue Model, Free-to-Play (F2P) dominated the Gaming Market with 68.49% share in 2025; In-App Purchases (IAPs) fastest growing (CAGR).

-

By Game Type, Action / Adventure dominated the Gaming Market with 24.68% share in 2025; Sports Games fastest growing (CAGR).

-

By Ecosystem, App Stores (Google Play, Apple App Store) dominated the Gaming Market with 74.82% share in 2025; Cloud Gaming Platforms (GeForce Now, Xbox Cloud) fastest growing (CAGR).

-

By End-User, Casual Gamers dominated the Gaming Market with 69.52% share in 2025; Esports Players fastest growing (CAGR).

Gaming Market Segment Analysis

By Platform, Mobile Gaming dominates the Gaming Market, while Cloud Gaming is the fastest-growing segment

The Mobile Gaming division held its dominance in the Gaming Market in 2025, with the revenue contribution of approximately 72.36%. The dominance of the Mobile Gaming division is primarily attributed to the ubiquitous presence of smartphones, low barrier to entry, and fast growth of mobile games that can be played without monetary investments. Mobile games still boast impressive user engagement indicators due to favorable distribution systems through apps, session format, and hyper-casual game monetization model.

Between 2026 and 2035, the Cloud Gaming division is projected to achieve the highest CAGR thanks to the growing popularity of subscription-based streaming services and the improvements in internet infrastructure globally. Cloud-based gaming platforms such as Xbox Cloud Gaming, NVIDIA GeForce NOW, and PlayStation Cloud Streaming make it possible for people to enjoy high-end gaming on their devices without investing in costly gaming computers.

By Revenue Model, Free-to-Play (F2P) dominates the Gaming Market, while In-App Purchases (IAPs) grow fastest

The F2P segment captured around 68.49% of total revenue in 2025, owing to its popularity in mobile, PC, and live-service console games. The high growth rate in the market is primarily attributed to large-scale acquisition, low barrier to entry, and efficient monetization through advertisements, battle passes, and microtransactions.

The IAPs segment is estimated to register the highest CAGR between 2026 and 2035, considering that there will be more emphasis on creating player loyalty and consistent revenues. This development will largely occur due to the growing trend of expanding virtual economies, cosmetic enhancements, seasonal updates, and downloadable expansions.

By Game Type, Action / Adventure dominates the Gaming Market, while Sports Games is the fastest-growing segment

In 2025, the Action / Adventure category had the biggest market share amounting to about 24.68%. The reason behind this was the ever-increasing demand across the globe for interactive stories, combat, and action games. The category enjoys solid franchises that include not only AAA games for consoles but also mobile games.

The Sports Games category will enjoy the highest CAGR between 2026 and 2035 owing to growing interest among players in games featuring open-world scenarios and customization, as well as story-driven gameplay. Increasingly popular MMORPG games and mobile RPG games are contributing to the trend as well.

By Ecosystem, App Stores dominate the Gaming Market, while Cloud Gaming Platforms are the fastest-growing

The App Store ecosystem (consisting of Google Play Store and Apple App Store) was responsible for about 74.82% of overall gaming distribution income in 2025 because of centralized discovery systems, payment solutions, and global presence on mobile platforms. They will continue being the main channel through which games get distributed to mobile users.

The Cloud Gaming Platform will be the fastest-growing segment between 2026 and 2035 due to increased reliance on device-agnostic gaming. There are already several cloud-based game platforms, including GeForce NOW and Xbox Cloud Gaming, that offer cross-device access to consoles, PC, and mobile games without requiring high-performance devices.

By End-User, Casual Gamers dominate the Gaming Market, while Esports Players grow fastest

Casual Gamers accounted for around 69.52% of gamers globally in 2025 due to the popularity of mobile games, easy-to-play game mechanisms, and short engagement duration. This segment makes up the backbone of global gamer consumption, especially among those who prefer mobile gaming.

For the period between 2026 and 2035, Esports Players is expected that the growth in terms of CAGR will be highest due to the fast growth of competitive gaming, establishment of franchises in leagues, sponsorship deals, and earnings on streaming platforms. The growth in esports players will lead to an organized sporting environment globally.

Gaming Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

83.66% |

|

Europe |

Germany |

28.34% |

|

Asia Pacific |

China |

49.57% |

|

Middle East & Africa |

UAE |

22.46% |

|

Latin America |

Brazil |

41.33% |

Asia Pacific Gaming Market Insights

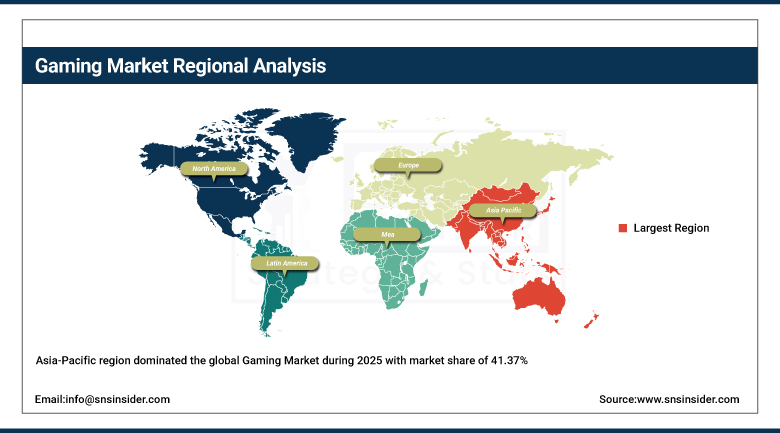

The Asia-Pacific region dominated the global Gaming Market during 2025 with market share of 41.37% and will continue fastest growing over the forecast period from 2026 to 2035 with CAGR of 10.79%, due to a large number of gamers in the region, strong inclination towards mobile games, thriving esport industry, and speedy development of digital infrastructures. China, Japan, India, South Korea, and other southeast Asian countries emerge as key regions of growth, among which China emerges as the leading regional revenue contributor due to a well-developed esport industry. In this regard, the development of smartphones, affordable mobile internet services, and rising disposable income are driving growth in the region.

At the same time, Japan and South Korea are innovation centers for console, mobile, and competitive gaming markets. South Korea sees an expansion of its esports infrastructure and the implementation of the cloud gaming ecosystem with 5G support. Moreover, in Japan, there is an increased focus on the development of new technologies in gaming, such as immersive gameplay engines, virtual reality features, and cross-platform gaming systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Gaming Market Insights

North America is expected to be one of the top performers in terms of growth rate within the global Gaming Market from 2026 to 2035 due to significant consumer expenditure on entertainment and high levels of penetration of high-end games and rapid proliferation of cloud gaming systems and subscription services. The United States dominates the region in terms of contribution due to the prevalence of several large-scale gaming organizations such as Microsoft, Electronic Arts, Take-Two Interactive, Epic Games, and Activision Blizzard.

Moreover, major gaming organizations are expanding their reach by investing in subscription systems and cloud gaming systems in the region. In 2025, for instance, Xbox Game Pass investment and first-day game availability were greatly enhanced by Microsoft alongside cloud gaming services through multiple devices like smart TVs. In recent years, there have been collaborations between Microsoft and LG Electronics to provide Xbox Cloud Gaming services on some LG smart TVs.

Europe Gaming Market Insights

The Europe region was responsible for maintaining a constant revenue share in the global Gaming Market owing to its extensive digital connectivity, substantial investments made in the consumption of gaming content, and developed environment for gaming through consoles, PCs, and mobiles. The countries such as Germany, UK, France, and Scandinavia form prominent markets in the region due to their mature gaming environments, developed broadband networks, and increased cloud gaming trends and subscriptions.

Further, shaping the future of the gaming market in Europe has been its comprehensive regulatory landscape. Initiatives made under the EU Digital Services Act (DSA) and privacy of data regulations under GDPR have increased transparency within the online gaming ecosystem, thereby ensuring better consumer protection, digital payments security, and efficient management of user data.

Middle East & Africa and Latin America Gaming Market Insights

Middle East and Africa and Latin American regions have shown steady growth within the global Gaming Market based on the rising adoption of smartphones, internet connectivity, greater engagement from the younger population, and increasing investments in digital entertainment ecosystems. In the MEA region, the UAE, Saudi Arabia, and South Africa are leading market expansion, mainly due to government policies focused on digital transformation, including the Vision 2030 program of Saudi Arabia, which is resulting in extensive investment in the gaming ecosystem.

To facilitate the above development, Saudi Arabia has emerged as one of the fastest-growing gaming and esports investments globally, with a series of massive projects carried out by Savvy Games Group and the Public Investment Fund. The Kingdom has been investing billions of dollars in gaming publishing companies, esports events, game studios, and various strategic partnerships with other companies as part of its vision of becoming a global gaming hub by 2030.

Cloud-based game providers and foreign game publishers have been targeting the Latin American countries by adopting various localization strategies, including regional servers and content in Spanish and Portuguese languages.

Gaming Market Growth Drivers:

-

Rising global gamer engagement, mobile-first entertainment consumption, and demand for immersive digital experiences driving expansion of the Gaming Market

The change in consumer behaviors from traditional consumption of media to a more interactive form of digital entertainment via gaming represents one of the most significant factors driving the Gaming Market in a positive direction. Gaming platforms offering engaging gameplay, instant social interaction, competition, and convenience through multiple device platforms such as smartphones, personal computers, game consoles, and cloud-based systems are preferred by consumers today. Games have transformed from an exclusive sub-industry into the dominant entertainment industry which includes casual games, esports, live streaming, creator economy, and virtual social interactions among others.

Driving this positive trend, participation in the gaming industry continues to increase globally, reaching close to 3.5 billion gamers by 2025 according to industry forecasts. Most of this increase will be facilitated by widespread adoption of smartphones and increased access to the Internet in emerging regions around the world. Mobile gaming accounts for the highest number of user acquisition, while console and PC gaming ecosystems produce high value engagement.

Gaming Market Restraints:

-

High game development costs, infrastructure investment requirements, and increasing content production complexity creating barriers for smaller gaming studios and emerging market participants

Financial constraints imposed by the growing need for funds in the current game development process are one of the key limiting factors in the expansion of the Gaming Market, especially for smaller game developers, medium-sized studios, and new gaming enterprises. The production of triple-A games has become more capital-intensive due to the increasing need for expensive graphics engines, artificial intelligence systems, open-world landscapes, cybersecurity systems, cloud computing, and live services. Many publishing houses spend hundreds of millions of dollars per year to create such products.

Gaming Market Opportunities:

-

Accelerating expansion of cloud gaming, AI-driven game development, and immersive digital ecosystems creating new growth opportunities across emerging markets and cross-platform gaming environments

The future of Gaming Market growth will revolve around making the market more accessible, less reliant on hardware and providing players with incredibly immersive gaming experiences through innovation in technology. With the fast pace at which cloud gaming is growing, consumers can play high-end games without having to spend on expensive consoles or gaming computers; thus, the consumer addressable market gets much wider, especially in developing countries that favor mobile phones and other devices. Investing in subscription-based cloud gaming services and cross-platform support allows companies to monetize their product across various devices.

Recent Developments:

-

2026: Tencent Games increased its presence around the world by focusing on investing more resources in cross-platform live-service games, artificial intelligence-driven game development techniques, and global publishing collaborations. The firm improved its mobile gaming and esports ecosystems in the Asia Pacific region and further developed its cloud gaming capabilities to accommodate rising user engagement across the globe.

-

2025: Microsoft Gaming sped up its ecosystem’s growth by incorporating Xbox Cloud Gaming and Game Pass subscription models into smart televisions, computers, and mobile devices. In addition, the organization extended its first-day game release strategy after integrating Activision Blizzard into its operations.

-

2025: Sony Interactive Entertainment grew its PlayStation ecosystem through increasing PlayStation Plus subscriptions, live-service game development, and cloud streaming. The firm also made more efforts to develop PC games to widen its customer base.

-

2025: Nintendo enhanced its video game lineup by continuing to leverage the success of the Nintendo Switch platform, as well as increasing investment into their own video game franchises. The company made strides in digital content delivery systems, online gaming, and family-friendly multiplayer games.

Gaming Market Key Players

Some of the Gaming Market Companies

-

Tencent Games

-

Microsoft Gaming

-

Sony Interactive Entertainment

-

Nintendo

-

Electronic Arts

-

Activision Blizzard (part of Microsoft)

-

Epic Games

-

Valve Corporation

-

NetEase Games

-

Take-Two Interactive

-

Bandai Namco

-

Ubisoft

-

Square Enix

-

Sega Sammy Holdings

-

Konami

-

Capcom

-

Roblox Corporation

-

Embracer Group

-

Nexon

-

Warner Bros. Games

Gaming Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 247.10 Billion |

| Market Size by 2035 | USD 650.64 Billion |

| CAGR | CAGR of 10.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Mobile Gaming, Console Gaming, PC Gaming, Cloud Gaming, Others), • By Revenue Model (Free-to-Play (F2P), In-App Purchases (IAPs), Premium/Paid Games, Subscription Gaming, Advertising-based Gaming, Others), • By Game Type (Action/Adventure, Shooter (FPS/TPS), Sports Games, Role-Playing Games (RPG), Simulation Games, Others), • By Ecosystem (App Stores [Google Play, Apple App Store], Digital Distribution Platforms [Steam, Epic Games], Physical Retail, Cloud Gaming Platforms [GeForce Now, Xbox Cloud], Others), • By End User (Casual Gamers, Hardcore/Professional Gamers, Esports Players, Streaming Audience, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tencent Games, Microsoft Gaming, Sony Interactive Entertainment, Nintendo, Electronic Arts, Activision Blizzard (part of Microsoft), Epic Games, Valve Corporation, NetEase Games, Take-Two Interactive, Bandai Namco, Ubisoft, Square Enix, Sega Sammy Holdings, Konami, Capcom, Roblox Corporation, Embracer Group, Nexon, Warner Bros. Games. |

Frequently Asked Questions

Asia Pacific dominated the Gaming Market in 2025.

The Mobile Gaming segment dominated the Gaming Market in 2025.

The gaming market is expanding because users want convenient, engaging, and community-driven experiences that fit into everyday life, supported by technological advances like 5G, AR/VR, and cloud gaming.

The Gaming Market was valued at USD 247.10 billion in 2025.

The Gaming Market is expected to grow at a CAGR of 10.29% from 2026 to 2035.

Get in Touch