Genomic Medicine Market Report Scope & Overview:

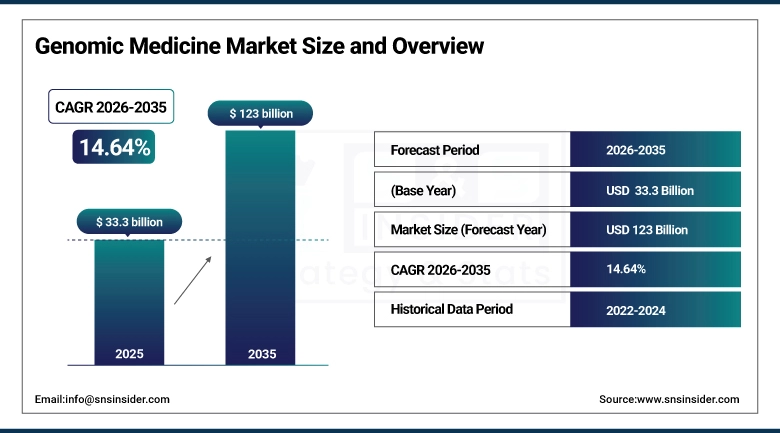

The Genomic Medicine Market was valued at USD 33.3 Billion in 2025 and is expected to reach USD 123 Billion by 2035, growing at a CAGR of 14.64% from 2026–2035.

The Genomic Medicine Market is experiencing growth owing to the rise in the utilization of personalized and precision medicine methodologies to improve disease detection and treatment efficacy. An increase in cancer cases, rare diseases, and chronic diseases is expected to drive demand for genomic testing and sequencing. The developments in next-generation sequencing, bioinformatics, and AI-based analysis are enabling better research opportunities. Also, the increased investments in healthcare, government support, and genomics integration in medical practices are leading to robust market growth.

Next-generation sequencing technology has gone from a research curiosity to a core clinical tool in less than 15 years. Over 70% of clinical genetic testing now relies on NGS platforms, making it the backbone of modern genomic medicine and a primary driver of market growth.

The collaboration between technology companies and pharmaceutical giants is reshaping the genomic medicine landscape. Partnerships like Thermo Fisher Scientific and Pfizer expanding NGS-based cancer testing to over 30 countries show how quickly genomic tools are becoming a global clinical standard rather than a specialty offering.

Genomic Medicine Market Size and Forecast:

-

Market Size in 2025: USD 33.3 Billion

-

Market Size by 2035: USD 123 Billion

-

CAGR: 14.64% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Genomic Medicine Market - Request Free Sample Report

Genomic Medicine Market Trends:

-

Rising demand for personalized and precision healthcare is driving the genomic medicine market.

-

Growing adoption of next-generation sequencing and advanced genetic testing is boosting market growth.

-

Expansion of applications in oncology, rare genetic disorders, and pharmacogenomics is fueling clinical integration.

-

Increasing focus on early disease detection, targeted therapy selection, and improved treatment outcomes is shaping adoption trends.

-

Advancements in bioinformatics, AI-driven genomic analysis, and high-throughput sequencing technologies are enhancing accuracy and speed.

-

Rising investments in genomics research and healthcare infrastructure are supporting market expansion.

-

Collaborations between biotech companies, pharmaceutical firms, and research institutions are accelerating innovation and global adoption.

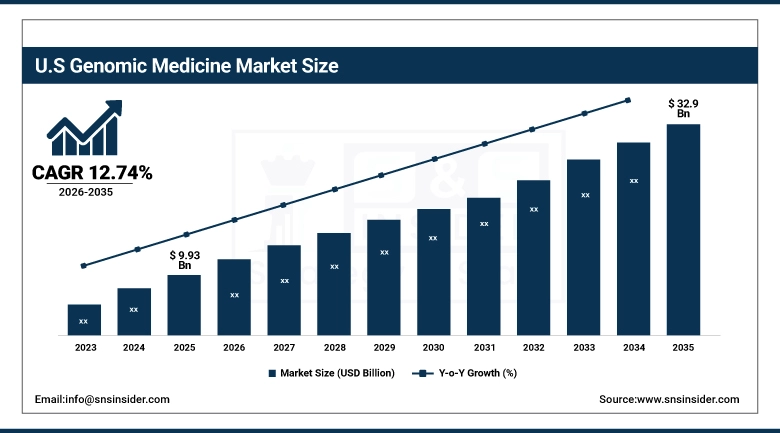

U.S. Genomic Medicine Market was valued at USD 9.93 billion in 2025 and is expected to reach USD 32.9 billion by 2035, growing at a CAGR of 12.74% from 2026 to 2035.

The Genomic Medicine Market in the United States is thriving owing to the increasing use of personalized medicine, high incidence rates of cancer and genetic diseases, and high demand for diagnostic tests. Furthermore, innovations in next-generation sequencing technology, favorable reimbursement policies, and high healthcare expenditure levels are contributing to the rapid growth of the market. Moreover, the presence of major biotechnology firms and extensive clinical trials are fueling the growth of this market.

Genomic Medicine Market Segment Insights:

-

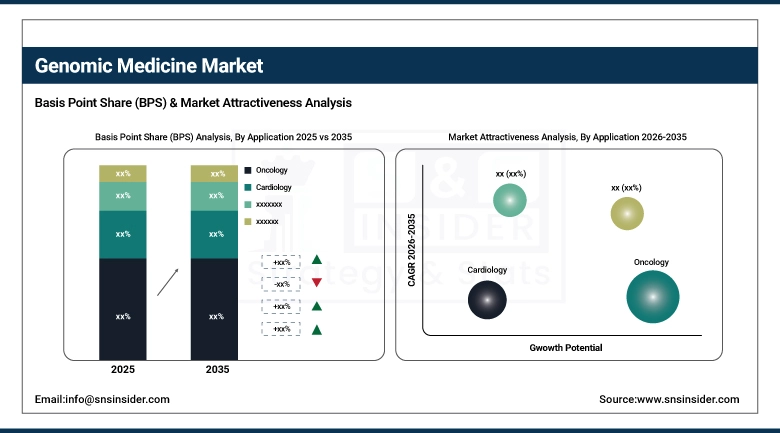

By Application, Oncology segment dominated the Genomic Medicine Market in 2025 with ~38% share; Rare Genetic Disorders segment fastest growing (CAGR).

-

By Products and Services, Instruments and Equipment segment dominated the Genomic Medicine Market in 2025 with ~44% share; Services segment fastest growing (CAGR).

-

By Technology, Next-Generation Sequencing (NGS) segment dominated the Genomic Medicine Market in 2025 with ~52% share; Microarray segment fastest growing (CAGR).

-

By End-User, Diagnostic Laboratories segment dominated the Genomic Medicine Market in 2025 with ~36% share; Pharmaceutical & Biotechnology Companies segment fastest growing (CAGR).

Genomic Medicine Market Segment Analysis:

By Application, Oncology segment dominates the Market, Rare Genetic Disorders segment expected to grow fastest

Oncology segment dominated the Market in 2025 because of the increasing prevalence of cancer and increasing applications of precision medicine in the early detection and targeted treatment of cancer. Genomics testing helps in the identification of genetic mutations and tumors that help in selecting targeted therapies. Increased investments for research on cancer, the use of more companion diagnostics, and demand for oncology drugs made the segment dominate the market globally.

The Rare Genetic Disorders segment is the fastest growing owing to the increasing awareness, advanced diagnostic abilities, and availability of more sophisticated testing for early detection of the condition. Growing trend of personalized care for rare diseases and government initiatives for rare diseases research have been fueling the adoption rate. Advanced technologies in genome sequencing and declining testing prices have also helped in increasing the adoption rate of this market.

By Products and Services, Instruments & Equipment segment dominates the Genomic Medicine Market, Services segment expected to grow fastest

Instruments & Equipment segment captured the largest market share in Genomic Medicine Market in 2025 owing to high demand for sequencing technologies, laboratory instrumentation, and analysis equipment used in genomic studies. The use of these technologies is essential for accurate sequencing, sample preparation, and analysis of data generated during the study. Technological developments, increased adoption of automation, and increased investment in genomic research have further fueled the growth of this segment.

The Services segment is expected to register the highest CAGR owing to the increasing demand for outsourced genomic tests, genomic test data analysis, and clinical trials services. The rising prevalence of precision medicine is contributing to the growing popularity of outsourced services for genomic studies. Growth in the demand for outsourced genomic test services is also fueled by growing pharmaceutical research activities.

By Technology, Next-Generation Sequencing (NGS) segment dominates the Market, Microarray segment expected to grow fastest

The Next-Generation Sequencing (NGS) market segment is projected to lead the Global Genomic Medicine market in 2025 owing to its high level of precision, scalability, and capability to carry out whole-genome analysis in a time- and cost-efficient manner. NGS is now preferred in diagnostics, cancer genomics, and identification of rare diseases. Technological developments, falling sequencing prices, and clinical implementation have contributed to its leading position in the market.

The microarray segment is the fastest-growing as the segment finds rising application in gene expression analysis, genotyping, and comparative genomics studies. Its cost efficiency and ability to analyze several genetic variants concurrently makes it ideal for large-scale screening purposes. Growing application of the segment in personalized medicine, pharmacogenomics, and agricultural genomics research are fueling the rapid growth of the segment.

By End-User, Diagnostic Laboratories segment dominates the Market, Pharmaceutical & Biotechnology Companies segment expected to grow fastest.

The Diagnostic Laboratories segment emerged as the leader in the Genomic Medicine Market during 2025 owing to its indispensable involvement in performing genomic tests, diagnosing diseases, and providing clinical reports. The surging demand among patients for precise diagnosis coupled with the enhanced infrastructure and the adoption of next-generation sequencing technologies has boosted their market leadership. The incorporation of genomics in diagnostic processes has been instrumental in augmenting their dominance.

The Pharmaceutical & Biotechnology Companies segment is the fastest-growing market segment because of the increased spending on drug discovery and development, biomarker identification, and precision medicine. The use of genomic information for accelerating clinical studies and discovering effective therapeutic drugs has enabled pharmaceutical and biotech companies to expand their business and boost revenue generation.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

78% |

|

Europe |

United Kingdom |

30% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

33% |

|

Latin America |

Brazil |

51% |

North America Genomic Medicine Market Insights

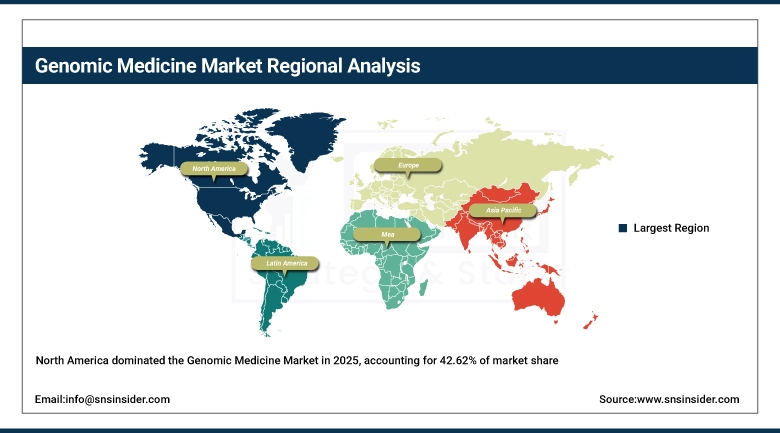

North America contributed to 42.62% of total genomic medicine market revenues in 2025 owing to the robust healthcare infrastructure in the region, early adaptation to the latest genomic technology, and heavy investments in precision medicine. The presence of key players, the availability of diagnostic labs, and the wide adoption of next-generation sequencing technologies in the region have boosted market growth. Other factors contributing to the growth of the market include favorable reimbursement frameworks, rising incidences of chronic and genetic disorders, and the increasing requirement for personalized therapies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Genomic Medicine Market Insights

Asia Pacific is the fastest-growing region in the genomic medicine market owing to several factors such as developments in healthcare infrastructure, investment in biotechnologies, and the growing trend of precision medicine. Rising cases of cancer and genetic disorders have led to increased demand for genomic diagnostic testing services. Other drivers include rising research activities, government initiatives, and growing availability of sequencing technologies. Awareness about personalized healthcare, increased spending on healthcare services, and large patient base are other factors accelerating the acceptance of genomic medicine solutions.

Europe Genomic Medicine Market Insights

Steady growth is observed in the Europe Genomic Medicine Market because of the presence of efficient healthcare facilities, the growing popularity of precision medicine, and increasing investments in genomic technology. Rising incidences of cancer and rare diseases have increased demand for better diagnostic and sequencing solutions. Favorable government policies, increasing clinical trial activity, and the participation of research organizations and biotechnology firms in genomic development are helping boost the market growth in the region.

Middle East & Africa and Latin America Genomic Medicine Market Insights

The Middle East & Africa and Latin America Genomic Medicine Market is experiencing steady growth due to the rising awareness about precision medicine, high incidences of chronic illnesses and genetic diseases, and improvements in the health care infrastructure. Growing investments in biotechnology research and adoption of modern diagnostic tools are contributing to the growth of the market. Health care reforms undertaken by the governments and collaborations with international genomics companies have helped improve the accessibility to testing services. High costs and inadequate infrastructure still hinder rapid adoption.

Genomic Medicine Market Growth Drivers

-

Increasing prevalence of cancer and rare genetic disorders driving demand for advanced genomic testing and molecular diagnostic solutions worldwide

The high prevalence of cancer, cardiovascular diseases, and rare genetic disorders worldwide is one of the critical factors that is fueling the expansion of the genomic medicine industry. The rising requirement for early and precise identification of diseases is leading to an increase in the demand for innovative genomic technology, including next-generation sequencing (NGS), polymerase chain reaction (PCR), and microarray technologies. In addition, healthcare organizations are increasingly adopting molecular diagnostics for detecting diseases by identifying genetic mutations responsible for causing diseases. Further, an increasing number of newborn and hereditary diseases testing is positively impacting the growth of the market.

Genomic Medicine Market Restraints

-

Ethical concerns, data privacy issues, and complex regulatory frameworks restricting seamless adoption of genomic data in clinical and research applications

Increasing apprehensions about issues associated with genetic data confidentiality, ethics, and data security are limiting the deployment of genomics-based medicine. The management of genetic data pertaining to patients carries risks linked with their potential abuse, theft, and discrimination. Regulatory policies concerning genetic screening and data sharing differ from one region to another, causing problems in their compliance by health care professionals and researchers. Ethical considerations about genetic manipulation, informed consent, and unexpected results make things more difficult for implementing genomics in the clinic. Global policies regulating the handling of genomic data are still not available, slowing down international collaborations in genomics research.

Genomic Medicine Market Opportunities

-

Expanding integration of artificial intelligence and big data analytics in genomics creating advanced opportunities for predictive healthcare and drug discovery innovation

The integration of AI, machine learning, and big data analytics into the field of genomics is offering substantial scope for innovation in the field of medicine and pharmaceuticals. The use of artificial intelligence in genomic medicine leads to more rapid discovery of diseases, genetic variations, and possible reactions to medicines. It has led to shorter development times for drugs and better drugs. Pharmaceutical companies are increasingly relying on genomics to create personalized medicines. Furthermore, predictive analysis is aiding risk assessment and preventive medicine. More cooperation between biotechnology organizations, universities, and IT firms is opening up even more avenues for genomics-based research and medicine.

Recent Developments:

-

2025: Illumina launched the NovaSeq X Plus sequencer with significantly higher throughput at lower cost per sample, making whole-genome sequencing more economically viable for population-scale programs and large clinical reference labs.

-

2023 (December): Vertex Pharmaceuticals and CRISPR Therapeutics received FDA approval for Casgevy, the world's first approved CRISPR-based gene therapy, for the treatment of sickle cell disease, marking a transformational moment for genomic therapeutics.

-

2023 (May): Thermo Fisher Scientific and Pfizer announced a partnership to expand NGS-based cancer testing access in more than 30 countries, combining Fisher's diagnostic instruments with Pfizer's commercial reach to accelerate global precision oncology adoption.

Key Players Genomic Medicine Market:

-

Thermo Fisher Scientific Inc.

-

Qiagen N.V.

-

F. Hoffmann-La Roche Ltd.

-

Oxford Nanopore Technologies plc

-

Pacific Biosciences of California, Inc.

-

PerkinElmer, Inc.

-

Myriad Genetics, Inc.

-

Invitae Corporation

-

Exact Sciences Corporation (Genomic Health)

-

Bio-Rad Laboratories, Inc.

-

23andMe, Inc.

-

Nebula Genomics

-

GenScript Biotech Corporation

-

Twist Bioscience Corporation

-

Eli Lilly and Company

-

Regeneron Pharmaceuticals, Inc.

-

Bluebird Bio, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 33.3 Billion |

| Market Size by 2035 | USD 123 Billion |

| CAGR | CAGR of 14.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Oncology, Cardiology, Paediatrics, Endocrinology, Respiratory Medicine, Rare Genetic Disorders, Infectious Diseases, Other Applications) • By Products And Services (Instruments and Equipment, Consumables, Services [Genomic Testing, Data Analysis, Interpretation, Genetic Counselling]) • By Technology (Next-Generation Sequencing [NGS], Polymerase Chain Reaction [PCR], Microarray, Sanger Sequencing, Others) • By End-User (Hospitals & Clinics, Academic Institutions, Research Institutions, Diagnostic Laboratories, Pharmaceutical & Biotechnology Companies, Other End-Users) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Illumina, Thermo Fisher Scientific, Qiagen, Agilent Technologies, F. Hoffmann-La Roche, Oxford Nanopore Technologies, PacBio, BGI Genomics, PerkinElmer, Myriad Genetics, Invitae, Genomic Health (Exact Sciences), Bio-Rad Laboratories, 23andMe, Nebula Genomics, GenScript Biotech, Twist Bioscience, Eli Lilly and Company, Regeneron Pharmaceuticals, Bluebird Bio, and other players. |

Frequently Asked Questions

Rising cancer incidence combined with expanding use of genomic-driven targeted therapies and government-funded national genomic programs.

North America dominates with about 42.62% of global revenue, led by the United States.

Oncology leads with approximately 38% market share, driven by widespread use of genomic tests for cancer diagnosis and treatment selection.

The market was valued at USD 33.3 billion in 2025.

The market is expected to grow at a CAGR of 14.64% from 2026 to 2035.

Get in Touch