Heart Failure POC & LOC Devices Market Report Scope & Overview:

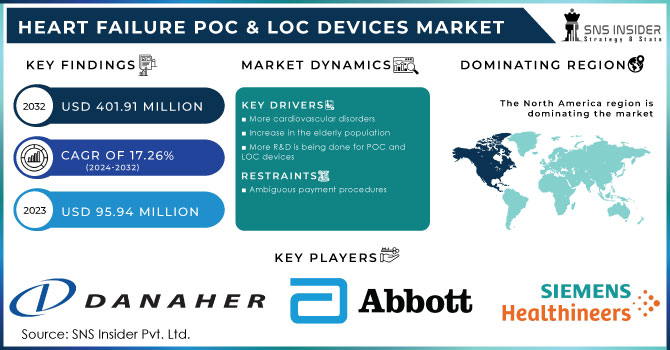

The Heart Failure POC & LOC Devices Market was valued at USD 95.94 million in 2023 and is expected to reach USD 401.91 million by 2032, growing at a CAGR of 17.26% over the forecast period 2024-2032.

The Heart Failure Point-of-Care (POC) and Lab-on-Chip (LOC) Devices market is witnessing accelerated growth, driven by the rising global burden of cardiovascular diseases. According to the American Heart Association (AHA), approximately 6.2 million adults in the U.S. alone have heart failure, with the prevalence projected to increase by 46% by 2030. The economic burden is equally concerning, with annual healthcare costs for heart failure expected to surpass USD 70 billion by 2035. These statistics underscore the urgent need for innovative, cost-effective diagnostic and monitoring solutions.

Get more information on Heart Failure POC & LOC Devices Market - Request Sample Report

Technological advancements are reshaping the market landscape. For instance, Abbott's i-STAT handheld system allows rapid blood analysis for cardiac markers, providing results within minutes. Similarly, Roche Diagnostics’ cobas h 232 POC system offers real-time measurements of NT-proBNP, a critical biomarker for diagnosing heart failure. These devices are essential for decentralized healthcare delivery, particularly in remote and resource-limited settings. Moreover, the integration of artificial intelligence (AI) and the Internet of Things (IoT) in POC devices, such as portable ECG monitors equipped with cloud-based data sharing, is enhancing diagnostic accuracy and personalized care.

Demographic trends further propel market growth. The aging global population, expected to reach 1.5 billion people aged 65 and older by 2050, is particularly vulnerable to cardiovascular conditions. POC devices, such as the CardioMEMS HF System by Abbott, enable continuous monitoring of heart failure patients, reducing hospital readmissions by up to 37% as per clinical studies.

Emerging economies also present substantial opportunities. In India, where cardiovascular diseases account for over 28% of deaths annually, affordable POC solutions are being introduced to improve early diagnosis and access to care. Government initiatives, like the National Health Protection Scheme (NHPS), further support the adoption of such technologies.

With leading companies like Abbott, Roche, and Siemens Healthineers investing in innovation, and the global focus shifting toward precision medicine and early diagnosis, the Heart Failure POC and LOC Devices market is poised to grow significantly, addressing critical healthcare challenges worldwide.

Market Dynamics

Drivers

-

Rising demand for early detection, AI integration, and decentralized care fuels market expansion

A major driver is the rising demand for early detection and continuous monitoring of heart failure patients. As heart failure is a chronic and recurrent condition, early intervention plays a crucial role in reducing hospitalizations and improving patient outcomes. POC and LOC devices deliver real-time results, enabling healthcare providers to make swift and informed treatment decisions.

Another factor fueling market growth is the advancement in device miniaturization and the development of user-friendly designs. These improvements have made POC devices more accessible across various healthcare settings, including outpatient clinics, emergency care units, and home care. Such innovations not only enhance patient compliance but also ease the burden on traditional healthcare infrastructure, benefiting both developed and emerging markets. The incorporation of artificial intelligence (AI) and machine learning into heart failure monitoring is also contributing to market expansion. These technologies improve predictive capabilities, allowing for more proactive management of heart failure and reducing the risk of adverse events. AI-powered devices can process large datasets to anticipate heart failure episodes and trigger timely interventions.

The shift toward decentralized and home-based care is another significant driver. As healthcare costs rise and there is an increasing preference for at-home treatments, POC devices are becoming essential for patients to monitor their conditions outside clinical settings, offering greater convenience and cost-efficiency. Lastly, heightened awareness of heart failure and the focus on strengthening cardiovascular healthcare systems globally are fueling the market. Public and private investments are accelerating the development and adoption of these devices, further driving growth.

Restraints

-

High Costs and Accessibility Issues

The initial high costs of Heart Failure POC & LOC devices, along with the challenges in making these technologies accessible in low-resource settings, can limit widespread adoption, especially in emerging markets.

-

Regulatory Challenges and Device Approval Delays

Stringent regulatory requirements and lengthy approval processes for medical devices can delay the launch of new products and hinder market growth, particularly in regions with complex regulatory frameworks.

Key Segmentation

By Test Type

Proteomic testing was the dominant segment in the Heart Failure POC & LOC Devices market in 2023, accounting for a significant share of the market. This dominance can be attributed to the increasing recognition of biomarkers in the early diagnosis and management of heart failure. Proteomic tests help identify specific proteins in blood or tissues, which can reveal the presence, severity, and prognosis of heart failure. The ability to monitor protein levels for more personalized care is a major driver behind the widespread adoption of proteomic testing. In 2023, this segment contributed approximately 53.0% to the overall market due to the growing demand for precision medicine and the need for non-invasive diagnostic methods.

Genomic testing emerged as the fastest-growing segment throughout the forecast period, fueled by the expanding knowledge of genetic factors in heart failure. This testing approach offers the potential for personalized treatment by identifying genetic predispositions and enabling more accurate predictions of disease progression. As genetic research becomes increasingly integrated into clinical practice, the adoption of genomic testing in heart failure management has accelerated, with a growing number of healthcare providers incorporating genetic analysis into their diagnostic procedures.

By Technology

Microfluidics technology dominated the Heart Failure POC & LOC Devices market in 2023, holding a substantial share. This technology enables the miniaturization of diagnostic tests, allowing for quick, affordable, and accurate results. By using small sample volumes, microfluidics-based devices are ideal for point-of-care and lab-on-chip applications, making them widely adopted in heart failure management. The growing demand for rapid, in-situ diagnostics in both hospital and home care settings contributed to the strong market presence of microfluidics technology.

Array-based systems represent the fastest-growing technology segment, as they allow for the simultaneous analysis of multiple biomarkers, providing more comprehensive diagnostic results. This capability makes them particularly useful in complex conditions like heart failure, where multiple factors need to be considered for effective management. As healthcare providers continue to adopt multi-marker testing to enhance diagnostic accuracy and speed, the demand for array-based systems has surged, making it the fastest-growing technology in the market.

Regional Analysis

North America held the largest market share, driven by robust healthcare systems, high healthcare spending, and widespread adoption of advanced diagnostic technologies. The United States, in particular, is a key player, with a high prevalence of heart failure and a growing aging population. The increasing demand for early diagnosis, home-based care, and precision medicine further boosts the adoption of POC & LOC devices. Additionally, the region benefits from strong regulatory frameworks and high investments in medical device research and development.

Europe followed closely, with countries like Germany, the UK, and France seeing a growing adoption of heart failure management solutions. The region’s focus on improving cardiovascular care, along with initiatives aimed at reducing hospital readmissions, drives demand for real-time monitoring devices. Moreover, the push towards decentralized healthcare and home care solutions is fueling market growth in Europe.

In the Asia-Pacific (APAC) region, the market is expanding rapidly due to the rising burden of cardiovascular diseases, an aging population, and improving healthcare infrastructure. Countries like China and India are investing heavily in healthcare technologies, making the region a hotspot for growth. The increasing demand for affordable and accessible healthcare solutions in urban and rural areas is expected to accelerate the adoption of POC & LOC devices.

Need any customization research on Heart Failure POC & LOC Devices Market - Enquiry Now

Key Players

1. Abbott

-

i-STAT System

-

Freestyle Libre

-

Radiometer

-

Cepheid

-

Atellica Solution

-

Immulite 2000 XPi

4. F. Hoffmann-La Roche Ltd.

-

Cobas h232

5. Quidel Corporation

-

Triage BNP Test

6. bioMérieux S.A.

-

VITEK 2

7. Trinity Biotech

-

Point-of-Care Immunoassays

8. Instrumentation Laboratory

-

GEM Premier 4000

9. Abaxis, Inc.

-

VetScan

10. Becton, Dickinson and Company

-

BD FACSPresto

11. BioTelemetry, Inc.

-

CardioNet

12. Masimo Corporation

-

Rad-97

13. Novartis AG

-

Entresto

14. Stryker Corporation

-

LifePak

Recent Development

-

In November 2024, Emory University Hospital became the first in the U.S. to perform a surgical implantation of a novel ventricular assist device (VAD) designed for patients with heart failure.

-

In August 2024, researchers developed a point-of-care electrochemical biosensor prototype for heart failure screening. This device, resembling a lateral flow test, can measure two biomarkers for heart failure from a drop of saliva in just 15 minutes, improving access to screening, particularly in underserved areas.

-

In April 2024, Roche Diagnostics India launched its Heart Failure Test for Diabetics on its point-of-care device, providing faster and more accessible testing for heart failure in diabetic patients. This development aims to improve early detection and timely intervention, enhancing patient outcomes in India.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 95.94 million |

| Market Size by 2032 | US$ 401.91 million |

| CAGR | CAGR of 17.26% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Test Type (Proteomic testing, Metabolomic testing, Genomic testing) • By Technology (Microfluidics, Array-based systems, Others) • By End-Use (Clinics, Hospitals, Homes, Assisted living healthcare facilities, Laboratory) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Abbott, Danaher Corporation, Siemens Healthineers, F. Hoffmann-La Roche Ltd., Quidel Corporation, bioMérieux S.A., Trinity Biotech, Instrumentation Laboratory, Abaxis, Inc., Becton, Dickinson and Company, BioTelemetry, Inc., Masimo Corporation, Novartis AG, Stryker Corporation |

| Key Drivers | • Rising demand for early detection, AI integration, and decentralized care fuels market expansion |

| Restraints | • High Costs and Accessibility Issues • Regulatory Challenges and Device Approval Delays |

Frequently Asked Questions

Proteomic Testing, Metabolomic Testing, and Genomic Testing are sub segments of by test type of the Heart Failure POC & LOC Devices Market.

Due to the large market players in North America who are fostering significant organic revenue growth in the worldwide heart failure POC & LOC devices market, the region led the revenue share

Heart Failure POC & LOC Devices Market is divided into three segments and they are By Test Type, By Technology, and By End User

Increased investment in the study of cardiovascular and heart diseases, Creation of more recent, suitable POC and LOC heart failure biomarkers are the opportunities of the market.

The Heart Failure POC & LOC Devices Market is growing at a CAGR of 17.26% over the forecast period 2024-2032.

Get in Touch