Hydrogen Gas Market Report Scope & Overview:

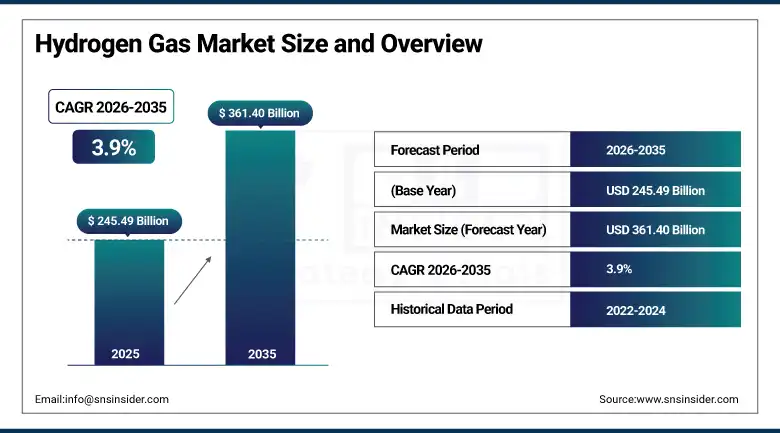

The Hydrogen Gas Market was valued at USD 245.49 Billion in 2025 and is expected to reach USD 361.40 Billion by 2035, growing at a CAGR of 3.9% from 2026–2035.

The global hydrogen gas market is advancing steadily as the world's most versatile industrial gas and an increasingly critical clean energy carrier. Hydrogen serves as a foundational raw material in ammonia synthesis, petroleum refining, and chemical manufacturing while simultaneously emerging as a clean energy vector whose fuel cell vehicles, power generation, and industrial decarbonisation applications are creating new commercial demand categories. The most significant market driver is the global shift toward cleaner energy systems focused on reducing carbon emissions. Green hydrogen, produced through renewable energy-powered electrolysis, is the fastest-growing segment driven by increasing sustainability initiatives and renewable energy integration.

In February 2025, Air Liquide and TotalEnergies announced a joint investment of over €1 billion to develop two large-scale low-carbon hydrogen production plants in the Netherlands, including a 200 MW electrolyzer in Rotterdam and a 250 MW electrolyzer in Zeeland. The investment demonstrates the commercial scale at which industrial hydrogen producers are committing to green hydrogen infrastructure whose economics are progressively approaching competitiveness with grey hydrogen as renewable electricity costs decline and electrolyzer capital costs reduce with manufacturing scale.

Market Size and Forecast

-

Market Size in 2026E: USD 255.06 Billion

-

Market Size by 2035: USD 361.40 Billion

-

CAGR: 3.9% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Hydrogen Gas Market - Request Free Sample Report

Hydrogen Gas Market Trends

-

Green hydrogen costs are declining due to falling renewable electricity prices and increasing electrolyzer manufacturing scale. This is improving the competitiveness of electrolytic hydrogen compared with conventional grey hydrogen production.

-

Blue hydrogen projects combining steam methane reforming with carbon capture and storage are gaining momentum. These projects provide a lower-carbon transition pathway while leveraging existing hydrogen infrastructure.

-

Commercial deployment of hydrogen fuel cell vehicles by automotive and truck manufacturers is creating new transportation-sector demand. Government and private investments in hydrogen refuelling infrastructure are further supporting market growth.

-

Industrial adoption of hydrogen in green steel production is increasing as manufacturers replace coal with hydrogen-based direct reduced iron processes. This transition is aligned with global decarbonization objectives for the steel industry.

-

National hydrogen strategies and funding programs across major economies are accelerating market development. Government support is encouraging private-sector investment in hydrogen production, infrastructure, and end-use applications.

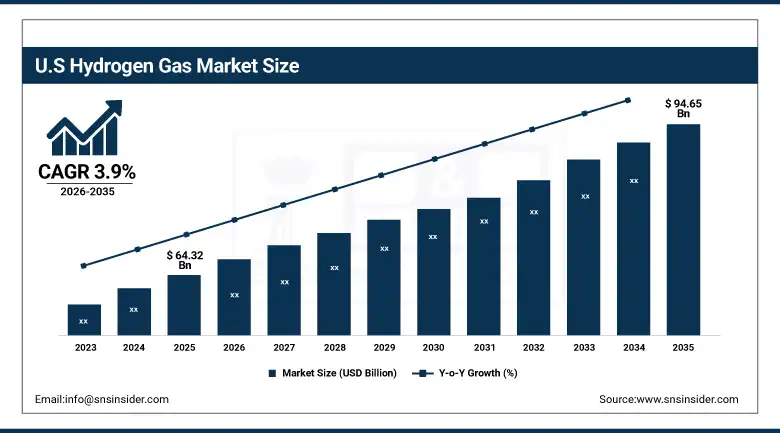

U.S. Hydrogen Gas Market Outlook

The U.S. Hydrogen Gas Market was valued at approximately USD 64.32 Billion in 2025 and is expected to reach approximately USD 94.65 Billion by 2035, growing at a CAGR of approximately 3.9%.

The U.S. is a commercially significant hydrogen gas market whose existing industrial hydrogen demand is anchored by petroleum refining's hydrocracking and desulfurisation requirements and ammonia production for fertiliser manufacturing. The IRA's clean hydrogen production tax credit of up to USD 3 per kilogram is creating above-average investment momentum in green and blue hydrogen infrastructure. DOE's Regional Clean Hydrogen Hubs programme with USD 7 billion in grants is establishing the geographic hydrogen economy nodes whose infrastructure investment attracts complementary private capital.

Air Products and Chemicals signed a USD 15 billion agreement with Saudi Arabia's NEOM project in 2024 for green hydrogen production and export, targeting the production of 600 tonnes per day of green hydrogen from 4 GW of renewable power for export as green ammonia. The landmark commitment represents the largest single green hydrogen infrastructure investment announced to date and demonstrates the commercial conviction of leading industrial gas companies in the green hydrogen market's long-term commercial viability.

Hydrogen Gas Market Segment Analysis

-

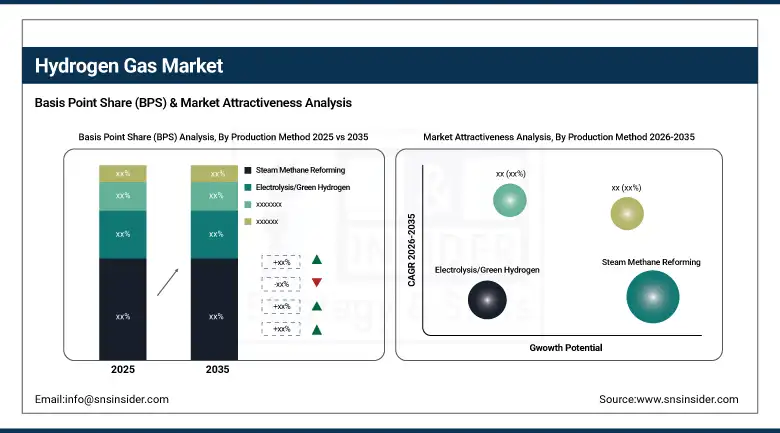

By Production Method, the Steam Methane Reforming segment dominated the Hydrogen Gas Market with approximately 48% share in 2025, while the Electrolysis/Green Hydrogen segment is the fastest growing with a CAGR of approximately 14.5%.

-

By Application, the Chemical Manufacturing segment dominated the Hydrogen Gas Market with approximately 55% share in 2025, while the Transportation segment is the fastest growing with a CAGR of approximately 12.8%.

-

By Distribution Mode, the Pipeline segment dominated the Hydrogen Gas Market with approximately 60% share in 2025, while the Cryogenic Liquid Tanker segment is the fastest growing.

-

By End User, the Chemical Industry/Oil Refining segment dominated the Hydrogen Gas Market with approximately 52% share in 2025, while the Power Generation segment is the fastest growing.

By Production Method, SMR dominates, green hydrogen grows fastest

Steam methane reforming retained the dominant production method position with approximately 48% of the hydrogen gas market in 2025. SMR's commercial primacy reflects its position as the world's lowest-cost large-scale hydrogen production technology at natural gas prices below approximately USD 10 per MMBtu in most markets. The existing global SMR installed base, encompassing hundreds of large-scale industrial hydrogen plants, creates production capacity whose replacement cost substantially exceeds the incremental operating cost of continued SMR operation. SMR's carbon intensity of approximately 9-12 kg CO2 per kg of hydrogen represents the current commercial reality of global hydrogen production whose majority will remain fossil fuel-based throughout the transition period.

Electrolysis and green hydrogen is the fastest-growing production method at approximately 14.5% CAGR because the convergence of declining renewable electricity costs, falling electrolyzer capital costs through manufacturing scale, and government production incentives including the IRA's USD 3/kg clean hydrogen tax credit are progressively improving green hydrogen's economics. Green hydrogen's carbon intensity below 1 kg CO2 per kg of hydrogen creates the lowest-carbon production pathway whose climate policy preference creates structured institutional and regulatory demand that sustains investment independent of pure economic competitiveness.

By Application, chemical manufacturing dominates, transportation grows fastest

Chemical manufacturing retained the dominant application position with approximately 55% of the hydrogen gas market in 2025. The Haber-Bosch ammonia synthesis process consumes approximately 55% of global hydrogen output in producing the nitrogen fertiliser that feeds 40% of the world's population. This foundational application creates non-discretionary hydrogen demand whose agricultural necessity creates procurement independent of hydrogen pricing and economic cycles. Methanol synthesis, petroleum hydroprocessing, and specialty chemical production collectively represent the balance of chemical manufacturing's hydrogen demand whose combined volume creates the commercial scale that sustains industrial hydrogen infrastructure investment.

Transportation is the fastest-growing application at approximately 12.8% CAGR because hydrogen fuel cell vehicles, hydrogen-powered trains, and maritime hydrogen fuel cell vessels are collectively creating new commercial hydrogen demand beyond the industrial base that has defined the market historically. Each new hydrogen refuelling station commissioned creates infrastructure that attracts additional fuel cell vehicle adoption in its catchment area, creating the self-reinforcing infrastructure and vehicle adoption cycle that EV charging networks demonstrated in the automotive market.

By Distribution, pipeline dominates, cryogenic liquid grows fastest

Pipeline distribution retained the dominant mode with approximately 60% of the hydrogen gas market in 2025. Dedicated hydrogen pipelines, primarily serving existing industrial clusters in the Gulf Coast, Rhine Valley, and Benelux industrial regions, create the most cost-efficient hydrogen transport for the high-volume, short-distance industrial supply relationships that define the majority of current hydrogen market commercial activity. Air Products, Linde, and Air Liquide operate the world's largest dedicated hydrogen pipeline networks whose integrated production and distribution infrastructure creates competitive supply economics that independent market entrants cannot easily replicate.

Cryogenic liquid tanker distribution is the fastest-growing mode because long-distance hydrogen transport and international export trade require liquid hydrogen's superior energy density relative to compressed gas tube trailer alternatives. Japanese, Korean, and Australian green hydrogen export programmes are investing in liquid hydrogen carrier vessels and terminal infrastructure whose commercial scale requires liquid hydrogen logistics capability that pipeline infrastructure cannot provide for intercontinental trade routes.

By End User, chemical/refining dominates, power generation grows fastest

Chemical industry and oil refining retained the dominant end user position with approximately 52% of the hydrogen gas market in 2025. Petroleum refineries require hydrogen for hydrocracking, hydrotreating, and desulfurisation whose combined consumption per refinery creates substantial procurement whose aggregate across the global refining fleet defines the majority of current merchant hydrogen market volume. Ammonia fertiliser producers represent the single largest individual hydrogen consumer category whose combined global consumption substantially exceeds petroleum refining's aggregate hydrogen requirement, sustaining chemical manufacturing's commercial dominance.

Power generation is the fastest-growing end user because hydrogen's role as a long-duration energy storage medium, a grid balancing fuel for hydrogen turbines, and a zero-carbon fuel for combined heat and power is creating new institutional demand from electricity sector operators whose decarbonisation obligations create structured long-term hydrogen procurement motivation. Each country with carbon neutrality legislation whose power sector hydrogen pathway creates demand certainty that sustains energy company and infrastructure fund investment in hydrogen power generation infrastructure.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

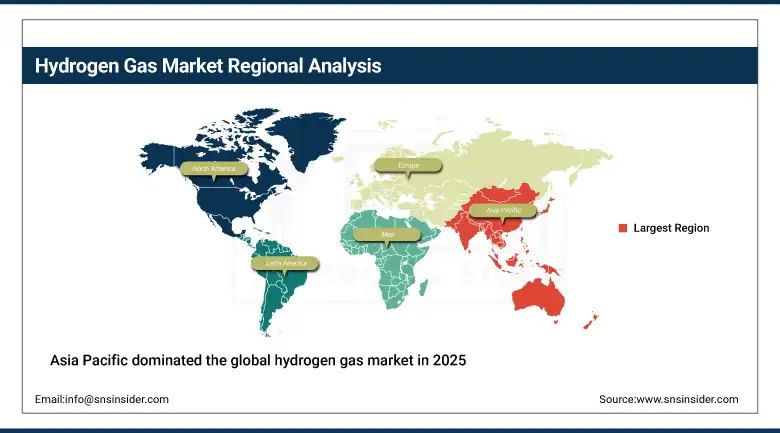

Asia Pacific Hydrogen Gas Market Insights

Asia Pacific dominated the global hydrogen gas market in 2025, driven by strong investments from China, Japan, and South Korea in hydrogen infrastructure, industrial hydrogen demand from chemical and refining sectors, and the region's ambitious clean hydrogen strategies. China accounts for approximately 54.6% of Asia Pacific revenues as the world's largest hydrogen producer and consumer whose industrial base creates the most commercially significant single-country hydrogen demand concentration globally. Japan and South Korea's active hydrogen economy programmes, including fuel cell vehicle deployment, hydrogen power generation, and green hydrogen import infrastructure, create sophisticated secondary markets whose technology adoption pace influences global commercial standards.

Australia represents a commercially significant emerging market within Asia Pacific as a potential green hydrogen export hub whose renewable energy resources, geographic proximity to Asian hydrogen import markets, and government investment in hydrogen export infrastructure create long-term commercial development opportunity. The Australia-Japan and Australia-Korea green hydrogen supply agreements represent the first commercial-scale international hydrogen trade programme whose implementation will demonstrate the economics of global hydrogen export.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Hydrogen Gas Market Insights

North America is a commercially significant hydrogen gas market anchored by the U.S. petroleum refining sector's industrial hydrogen demand and the rapidly growing clean hydrogen programme supported by IRA incentives and DOE's Regional Clean Hydrogen Hubs investment. The United States accounts for approximately 87.4% of North American revenues through Air Products, Air Liquide Americas, and Linde's U.S. operations whose combined infrastructure defines the North American hydrogen supply network.

Canada contributes approximately 12.6% of North American revenues through its oil sands upgrading hydrogen demand, natural gas hydrogen production potential in Alberta, and the federal government's clean hydrogen strategy whose production tax credit investment creates commercial hydrogen infrastructure development momentum aligned with the IRA's procurement attractiveness.

Europe Hydrogen Gas Market Insights

Europe is a technically sophisticated hydrogen market where the EU Hydrogen Strategy's 10 million tonne domestic green hydrogen production target by 2030, the IPCEI hydrogen infrastructure programme's €3.4 billion investment, and the European Hydrogen Bank's auction mechanism are collectively creating the most comprehensive government-backed hydrogen economy development programme of any global region. Germany accounts for approximately 22.3% of European revenues through its industrial hydrogen demand, the H2Global programme's international green hydrogen import programme, and Linde's and Air Liquide's European hydrogen operations.

The Netherlands and France are significant secondary European markets where the Rotterdam hydrogen hub's terminal infrastructure, Air Liquide and TotalEnergies's €1 billion electrolyzer investment, and France's national low-carbon hydrogen strategy create structured commercial hydrogen demand development. Air Liquide and TotalEnergies's February 2025 joint investment announcement reflects the commercial momentum of European green hydrogen infrastructure development.

MEA & Latin America Hydrogen Gas Market Insights

The Middle East and Africa and Latin America are growing hydrogen markets where green hydrogen export potential, industrial hydrogen demand, and government investment are creating commercial development. Saudi Arabia leads MEA revenues at approximately 31.2% through ARAMCO's refinery hydrogen demand, SABIC's chemical manufacturing hydrogen consumption, and the NEOM green hydrogen export programme whose USD 15 billion Air Products partnership represents the largest committed green hydrogen production infrastructure investment globally.

Brazil leads Latin American revenues at approximately 44.2% through its petroleum refining hydrogen demand, the growing fertiliser sector, and the federal government's National Green Hydrogen Programme whose renewable energy abundance creates competitive green hydrogen production economics. Brazil's Ceará hydrogen hub and multiple announced green hydrogen export projects reflect the country's ambition as a green hydrogen exporter to European markets.

Market Dynamics

Growth Drivers: Industrial decarbonisation creating clean hydrogen demand and government funding creating investment certainty

Industrial decarbonisation policy is the hydrogen gas market's most commercially transformative structural growth driver. Carbon pricing mechanisms, net zero legislation, and industrial sector emissions reduction targets are collectively creating demand for clean hydrogen as a replacement for fossil fuel-based industrial processes whose decarbonisation options are limited. Steel production's shift toward hydrogen direct reduction iron, ammonia production's transition to green hydrogen feedstock, and chemical manufacturing's clean hydrogen adoption collectively represent a demand wave whose commercial scale substantially exceeds the current hydrogen market's size.

Government funding commitment creates commercial investment certainty that private hydrogen capital requires before committing to the decade-scale infrastructure investment that hydrogen economy development involves. The IRA's USD 3/kg clean hydrogen production tax credit, the EU's €3.4 billion IPCEI hydrogen programme, Japan's USD 107 billion Green Innovation Fund hydrogen allocation, and Australia's hydrogen export infrastructure investment collectively create the policy foundation whose commercial certainty sustains private investment in hydrogen production, transport, and consumption infrastructure.

Restraints: High green hydrogen production cost versus grey hydrogen and hydrogen infrastructure buildout timeline

Green hydrogen's current production cost of USD 4-8 per kilogram substantially exceeds grey hydrogen's USD 1-2 per kilogram production cost in natural gas-abundant regions, creating an economics gap that prevents green hydrogen adoption in cost-competitive industrial applications without policy support. The cost reduction trajectory toward USD 1-2 per kilogram green hydrogen by 2030 that electrolyzer manufacturers and renewable energy developers project requires both manufacturing scale and renewable electricity price declines whose realisation depends on investment programme execution whose timeline creates commercial uncertainty.

Hydrogen infrastructure buildout timeline creates a chicken-and-egg commercial challenge where hydrogen demand development requires infrastructure that requires demand to justify investment. Pipeline networks, refuelling stations, and terminal infrastructure each require multi-year construction timelines whose completion must precede commercial demand realisation. This infrastructure requirement creates commercial risk that government funding is progressively de-risking through anchor customer commitments and offtake guarantees.

Opportunities: Green steel hydrogen demand and hydrogen export trade creating premium new commercial markets

Green steel production using hydrogen direct reduction iron represents the most commercially transformative near-term new hydrogen demand category. The steel industry's decarbonisation obligation requires a clean reducing agent to replace coking coal whose hydrogen DRI alternative creates substantial new hydrogen demand whose commercial scale compounds with the steel industry's progressive transition timeline. Each new green steel plant commissioned creates a hydrogen offtake anchor whose long-duration supply contract justifies dedicated green hydrogen production infrastructure.

International hydrogen export trade between renewable energy-abundant exporting regions and hydrogen-importing industrial economies represents the most commercially significant long-term market development opportunity. Australia-Japan, Chile-Germany, and Morocco-Netherlands hydrogen export programmes collectively demonstrate the commercial intent of multiple national governments to create intercontinental hydrogen trade whose infrastructure investment will sustain market growth across the 2026-2035 forecast period.

Recent Developments:

-

2025: Air Liquide and TotalEnergies announced a joint investment of over €1 billion in February 2025 to develop two large-scale low-carbon hydrogen production plants in the Netherlands including a 200 MW electrolyzer in Rotterdam and 250 MW in Zeeland, targeting green hydrogen supply for Dutch industrial decarbonisation.

-

2024: Air Products and Chemicals signed a USD 15 billion agreement with Saudi Arabia's NEOM project in 2024 for green hydrogen production and export, committing to the production of 600 tonnes per day of green hydrogen from 4 GW of renewable power for export as green ammonia to global markets.

-

2024: The U.S. DOE announced USD 7 billion in awards to seven Regional Clean Hydrogen Hubs across the United States in 2024, creating the geographic hydrogen economy node infrastructure whose public investment is designed to catalyse proportional private commercial hydrogen infrastructure investment across the U.S.

Hydrogen Gas Market Key Players

-

Air Liquide S.A.

-

Linde plc

-

Air Products and Chemicals Inc.

-

Messer Group GmbH

-

Praxair Inc. (Linde)

-

TotalEnergies SE

-

Royal Dutch Shell

-

BP plc

-

ExxonMobil

-

ENGIE S.A.

-

Siemens Energy

-

Nel Hydrogen

-

ITM Power

-

Plug Power Inc.

-

Ballard Power Systems

-

Bloom Energy

-

FuelCell Energy

-

Toyota Motor Corporation

-

Hyundai Motor Company

-

thyssenkrupp Nucera

Hydrogen Gas Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 245.49 Billion |

| Market Size by 2035 | USD 361.40 Billion |

| CAGR | CAGR of 6.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Production Method (Steam Methane Reforming, Electrolysis/Green Hydrogen, Coal Gasification, Partial Oxidation, Others) • by Application (Chemical Manufacturing, Petroleum Refining, Transportation, Power Generation, Metal Processing, Others) • by Distribution Mode (Pipeline, Cylinders/Packaged, Cryogenic Liquid Tanker) • by End User (Chemical Industry, Oil & Gas Refining, Automotive/Fuel Cell, Power Generation, Metal & Steel, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Air Liquide S.A., Linde plc, Air Products and Chemicals Inc., Messer Group GmbH, Praxair Inc., TotalEnergies SE, Royal Dutch Shell, BP plc, ExxonMobil, ENGIE S.A., Siemens Energy, Nel Hydrogen, ITM Power, Plug Power Inc., Ballard Power Systems, Bloom Energy, FuelCell Energy, Toyota Motor Corporation, Hyundai Motor Company, thyssenkrupp Nucera |

Frequently Asked Questions

The Hydrogen Gas Market is expected to grow at a CAGR of 3.9% from 2026 to 2035.

The Hydrogen Gas Market was valued at USD 245.49 Billion in 2025.

Global shift toward cleaner energy systems creating clean hydrogen demand for industrial decarbonisation, and government hydrogen strategies with substantial funding commitments creating investment certainty that sustains private infrastructure development in green and blue hydrogen production, transport, and consumption.

Steam Methane Reforming dominated the Hydrogen Gas Market with approximately 48% share in 2025, while Electrolysis/Green Hydrogen is the fastest growing with a CAGR of approximately 14.5%.

Asia Pacific dominated the Hydrogen Gas Market in 2025, driven by strong investments from China, Japan, and South Korea, with China accounting for approximately 54.6% of Asia Pacific revenues.

Get in Touch