Injection Pen Market Report Scope & Overview:

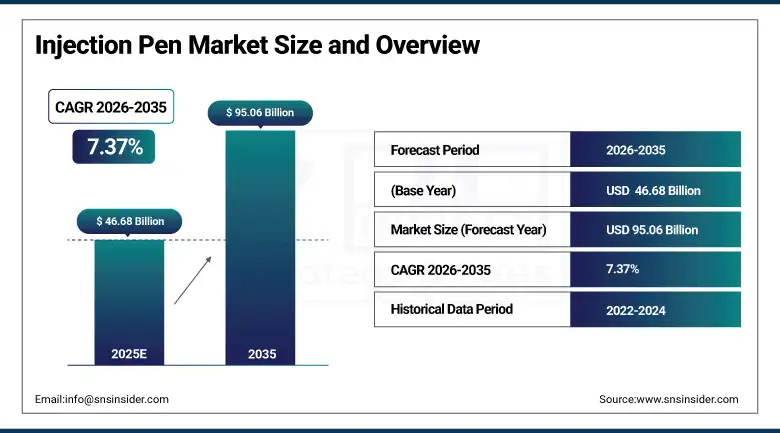

The Injection Pen Market size was valued at USD 46.68 Billion in 2025 and is projected to reach USD 95.06 Billion by 2035, growing at a CAGR of 7.37% during 2026–2035.

Injection pens have become a preferred drug delivery format for patients managing chronic conditions that call for regular self-dosing chiefly diabetes, but also osteoporosis, growth hormone deficiency, and autoimmune disease. Unlike conventional syringes, these devices let patients dial in precise doses and inject with minimal discomfort, which tends to translate into better day-to-day adherence. The market has benefited from two converging forces: a sharp increase in the number of people living with Type 2 diabetes worldwide, and a wave of new biologic and biosimilar therapies that need a reliable subcutaneous delivery mechanism. Manufacturers are now layering in connectivity features dose logging, Bluetooth pairing with smartphone apps to build out a more complete patient management picture.

Injection Pen Market Size and Forecast:

-

Market Size in 2025: USD 46.68 Billion

-

Market Size by 2035: USD 95.06 Billion

-

CAGR: 7.37% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Injection Pen Market - Request Free Sample Report

Injection Pen Market Key Trends:

-

Connected injection pens are gaining adoption: Manufacturers are introducing devices with automatic dose logging and app connectivity, enabling better monitoring of patient adherence and treatment data.

-

Disposable pens lead market volume: Single-use injection pens dominate sales due to convenience, while reusable pens are expanding in cost-sensitive and sustainability-focused markets.

-

Growth in biologic therapies: Increasing approvals of biologics such as GLP-1 agonists and advanced insulin therapies are driving demand for pen-based subcutaneous drug delivery.

-

User-friendly designs for aging patients: Manufacturers are improving ergonomics, larger dose displays, and audible dose confirmation to support elderly patients using injection pens.

-

Home healthcare driving demand: Rising preference for at-home chronic disease treatment has increased injection pen sales through retail pharmacies and direct-to-patient distribution channels.

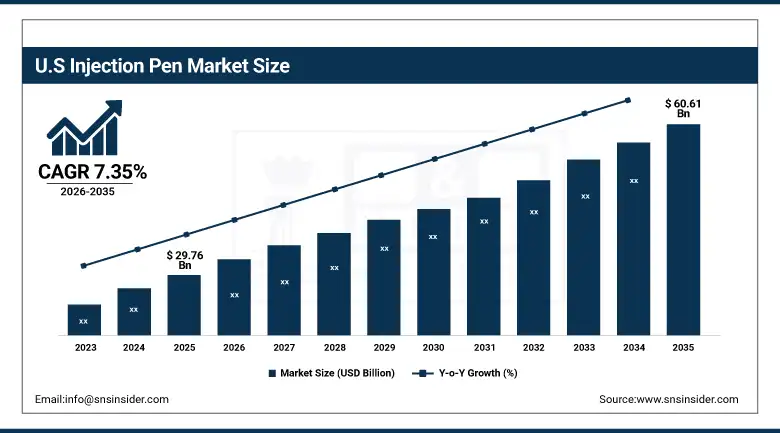

The U.S. Injection Pen Market has been valued at USD 29.76 Billion in 2025 and is expected to reach USD 60.61 Billion by 2035, growing at an estimated CAGR of 7.35% from 2026 to 2035. Growth of the U.S. Injection Pen Market is driven by the increasing prevalence of diabetes and other chronic diseases, rising adoption of self-injection drug delivery devices, expanding use of biologic therapies, and continuous advancements in smart and connected injection pen technologies.

Injection Pen Market Key Drivers:

-

Diabetes prevalence is the single biggest demand driver.

The IDF estimates more than 500 million adults currently live with diabetes globally, and insulin-requiring patients form the core user base for injection pens. As incidence climbs in South and Southeast Asia and sub-Saharan Africa, the addressable population keeps expanding.

Beyond diabetes, national healthcare programs in the US, UK, Germany, and Japan have tightened treatment guidelines for osteoporosis and growth disorders in a way that routes more patients toward injectable therapy. That has pulled fresh prescription volume into the pen category that did not exist a decade ago.

On the supply side, the biosimilar insulin wave has lowered the per-unit drug cost enough to make self-injection therapy economically viable in mid-income markets. Device makers who have aligned their pen platforms with the leading biosimilar insulin brands are seeing volume follow.

Injection Pen Market Key Restraints:

-

Device cost and reimbursement gaps are the biggest brakes on growth.

A smart connected pen can cost ten to twenty times more than a basic disposable. In countries where reimbursement covers only the drug, not the delivery device, patients often absorb that difference out of pocket and many don't.

Combination drug-device products face a more complicated regulatory path than standalone drugs. Getting a pen bundled with a new biologic through both drug and device review adds time and cost to development. That complexity has kept some smaller biosimilar manufacturers from launching their own pen platforms, instead relying on third-party devices.

In some geographies particularly rural areas of low-income countries the cold chain requirements for insulin and basic needle availability remain unsolved. A sophisticated pen device does not help much if the drug that goes in it cannot be stored safely.

Injection Pen Market Key Opportunities:

-

Digital dose management and the GLP-1 boom represent the two clearest near-term opportunities.

GLP-1 receptor agonists already the fastest-growing drug class in diabetes and obesity are overwhelmingly delivered by pen. Every new approval in that class brings device volume with it, and manufacturers with established GLP-1 pen platforms are well-positioned to capture that growth.

On the digital side, payers and employers are beginning to pay for adherence management platforms. Connected pens sit at the data layer of those platforms. Companies that can demonstrate a clinical or cost outcome tied to their dose-logging capability have a credible reimbursement argument that goes beyond the device itself.

In emerging markets particularly India, Indonesia, and Brazil local manufacturers are undercutting global brands on price and building out distribution networks. That opens a different kind of opportunity for established players: co-manufacturing or licensing arrangements that get their pen platform into markets where they cannot compete on cost alone.

Injection Pen Market Segments:

-

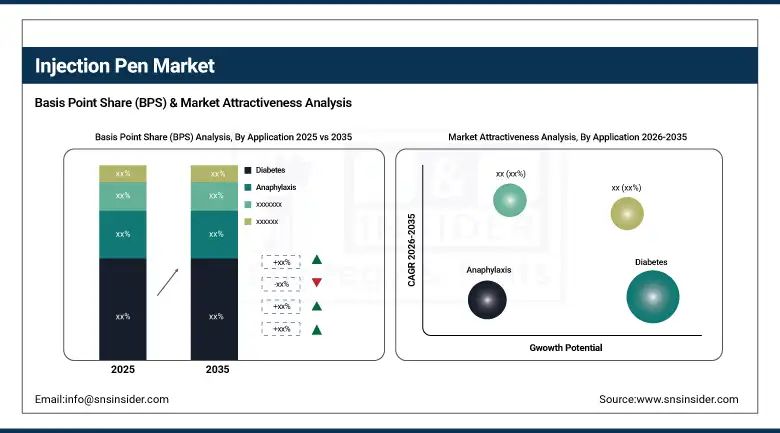

By Product: In 2025, Disposable dominated with 68% share; Reusable fastest growing segment during 2026-2035

-

By Application: In 2025, Diabetes dominated with 72% share; Osteoporosis fastest growing segment during 2026-2035

-

By End Use: In 2025, Hospital dominated with 60% share; Home Care Settings fastest growing segment during 2026-2035

Injection Pen Market Segment Analysis:

By Product: Disposable Leads, Reusable Catching Up

Disposable pens hold the larger share for straightforward reasons they ship prefilled, require no patient assembly, and eliminate cross-contamination risk between injections. For insulin users dosing once or twice daily, they are simply easier. The tradeoff is ongoing cost: every pen goes in the bin after the cartridge is empty.

Reusable pens have a loyal following among patients who inject daily over many years and want to reduce both costs and plastic waste. Several European markets have begun including sustainability metrics in procurement decisions for public health systems, and reusable devices score better on that front. Expect their share to inch up as drug cartridge compatibility broadens.

By Application: Diabetes Is the Core, Osteoporosis Is Growing Fast

Diabetes accounts for the bulk of injection pen volume and will continue to do so. The combination of insulin-dependent Type 1 patients, the large and growing pool of Type 2 patients moving to injectable therapy, and the GLP-1 class for weight management means this application segment is not going to cede its lead anytime soon.

Osteoporosis has emerged as the surprise growth segment. Teriparatide and romosozumab both injectable have become standard of care for severe osteoporosis in most developed markets, and diagnosis rates are improving as bone density screening becomes more routine. The patient population tends to be older, which has pushed manufacturers to invest specifically in pen designs that are easier to use with arthritic hands.

By End-Use: Hospitals Dominant, Home Care Settings Fast Growing

Hospitals and specialist clinics are where most patients get their first injection pen a physician or diabetes nurse demonstrates the device, and the patient takes it home. Institutional procurement numbers are large, but they do not capture how the product is actually used.

Home care is now the fastest-growing end-use category because that is where the volume of injections actually happens. Retail pharmacy, mail-order, and direct-to-patient channels are picking up share from traditional hospital dispensing. Device makers that have historically focused on hospital tenders are revisiting their commercial models accordingly.

Injection Pen Market Regional Analysis:

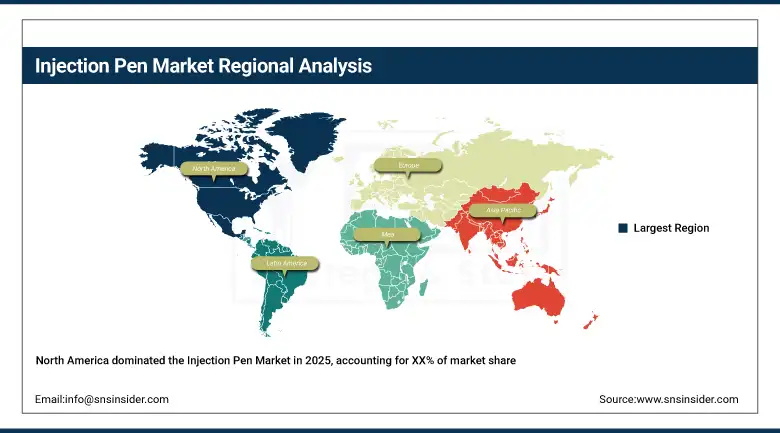

North America Injection Pen Market Insights:

North America is the largest single market, and the US drives most of that. Insulin prices have been a political flashpoint for years, and the Inflation Reduction Act's cap on Medicare insulin cost-sharing has pushed more patients into therapy which feeds pen demand. The US also has the most advanced commercial infrastructure for connected pen devices and digital diabetes management.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Injection Pen Market Insights:

Europe is a mature market with high pen penetration in Northern and Western countries. Germany, France, and the UK collectively represent the lion's share of European volume. Regulatory pressure around combination products from the EU MDR has created some turbulence, but manufacturers that cleared the compliance hurdle are in a stronger competitive position.

Asia-Pacific Injection Pen Market Insights:

Asia-Pacific is the fastest-growing region and is not particularly close. China and India each have diabetic populations larger than most countries, and both governments have listed insulin access as a public health priority. Japan has a strong domestic medical device industry with competitive local pen platforms. Across the region, the scale of the unmet need is enormous large parts of the diabetic population in lower-income APAC countries still use syringes because pens remain out of reach on price.

Latin America Injection Pen Market Insights:

Brazil and Mexico are the two markets that matter most in this region. Both have national diabetes programs that cover insulin, and pen device adoption has followed drug coverage. Argentina has a sizeable private health insurance sector that tends to adopt new delivery formats faster than the public system.

Middle East & Africa (MEA) Injection Pen Market Insights:

The GCC countries Saudi Arabia, UAE, Kuwait in particular have high diabetes prevalence and healthcare budgets large enough to cover modern delivery devices. Sub-Saharan Africa lags considerably, with device access limited to urban private clinics in most countries. South Africa is the exception, with a more developed pharmacy and insurance infrastructure.

Injection Pen Market Competitive Landscape:

Novo Nordisk A/S (founded 1923, Denmark) is the clear market leader its FlexPen and FlexTouch platforms ship with most of the company's insulin and GLP-1 product lines, and its device installed base runs into the hundreds of millions of users. Novo's scale gives it an R&D and manufacturing cost advantage that is difficult for pure-play device manufacturers to match.

-

In 2024, Novo Nordisk rolled out updated delivery devices for its semaglutide and next-generation insulin portfolio, with particular attention to dose accuracy at the lower end of the dosing range.

Sanofi S.A. (France) holds a large installed base through its SoloStar pen, one of the most widely dispensed insulin delivery devices in history. Sanofi's challenge is that its insulin franchise has faced generic and biosimilar competition, which puts pressure on device volumes tied to branded drugs.

-

In 2024, Sanofi made incremental updates to the SoloStar platform to maintain compatibility as it extended its biosimilar insulin partnerships.

Becton, Dickinson and Company (BD, USA) approaches the market differently rather than selling drug-device combinations, BD sells pen needles, pen components, and complete device platforms to pharmaceutical manufacturers who package them with their own drugs. This B2B model gives BD exposure across many drug brands simultaneously.

-

In 2024, BD expanded its pen needle range and formalized co-development agreements with several biosimilar manufacturers looking for pen platforms for their subcutaneous biologics.

Injection Pen Market Key Players:

-

Novo Nordisk A/S

-

Sanofi S.A.

-

Eli Lilly and Company

-

Becton, Dickinson and Company

-

Ypsomed AG

-

Owen Mumford Ltd.

-

Gerresheimer AG

-

SHL Medical AG

-

Haselmeier GmbH

-

Nemera Development S.A.

-

Terumo Corporation

-

Jiangsu Delfu Medical Device Co., Ltd.

-

Jiangsu Wanhai Medical Devices Co., Ltd.

-

Biocorp Production S.A.

-

Phillips-Medisize

-

West Pharmaceutical Services, Inc.

-

AptarGroup, Inc.

-

Kaleo, Inc.

-

Consort Medical Plc

-

Bespak

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 46.68 Billion |

| Market Size by 2035 | USD 95.06 Billion |

| CAGR | CAGR of 7.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product: (Disposable, Reusable) • By Application: (Diabetes, Anaphylaxis, Osteoporosis, Growth Hormone Deficiency, Arthritis, Others) • By End-Use: (Hospital, Clinics, Home Care Settings) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novo Nordisk A/S, Sanofi S.A., Eli Lilly and Company, Becton, Dickinson and Company (BD), Ypsomed AG, Owen Mumford Ltd., Gerresheimer AG, SHL Medical AG, Haselmeier GmbH (Medmix), Nemera Development S.A., Terumo Corporation, Jiangsu Delfu Medical Device Co., Ltd., Jiangsu Wanhai Medical Devices Co., Ltd., Biocorp Production S.A., Phillips-Medisize (Molex LLC), West Pharmaceutical Services, Inc., AptarGroup, Inc., Kaleo, Inc., Consort Medical Plc (Recipharm AB), Bespak (Recipharm AB). |

Frequently Asked Questions

The Injection Pen Market is expected to grow at a CAGR of 7.37% during 2026–2035.

The market was valued at USD 46.68 Billion in 2025 and is projected to reach USD 95.06 Billion by 2035.

The key drivers of the Injection Pen Market include rising diabetes prevalence, increasing biologic drug usage, demand for self-administration devices, growing home healthcare adoption, and technological advancements in smart injection pens

The Disposable segment dominated during the projected period.

North America dominated the Injection Pen Market in 2025.

Get in Touch