Laboratory Developed Tests Market Report Scope & Overview:

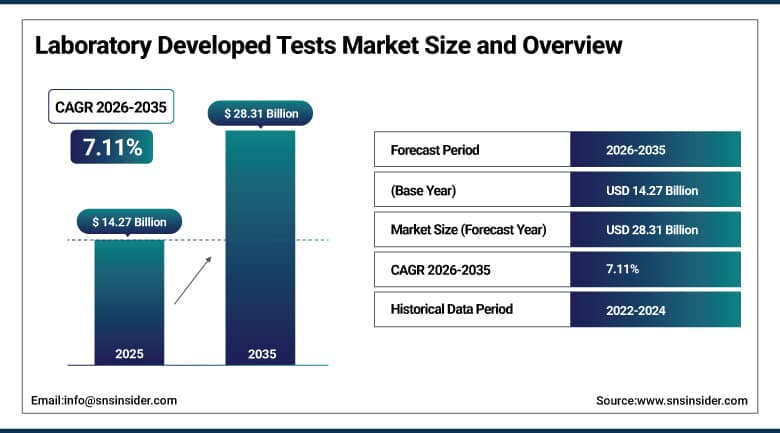

The Laboratory Developed Tests Market was valued at USD 14.27 Billion in 2025 and is expected to reach USD 28.31 Billion by 2035, growing at a CAGR of 7.11% from 2026–2035.

The global laboratory developed tests market is experiencing significant growth fueled by the rising need for customized medicine and advanced diagnostic products that commercially available FDA-cleared assays cannot address. Laboratory developed tests are in-vitro diagnostic tests designed, manufactured, and used within a single laboratory for patient diagnosis, monitoring, and treatment guidance across oncology, infectious diseases, rare genetic disorders, and other complex clinical presentations. Market development is driven by the increasing prevalence of cancer and genetic disorders, advances in molecular diagnostics and immunoassay technologies, and the growing adoption of next-generation sequencing and AI-driven diagnostic platforms.

In February 2025, Molecular Instruments, Inc. introduced a groundbreaking advancement in dermatological diagnostics with its HCR Pro RNA-ISH technology, in collaboration with Yale School of Medicine's Department of Dermatology. MI developed novel LDTs featuring a four-biomarker panel to accurately differentiate psoriasis and atopic dermatitis (eczema) in skin biopsies, addressing a long-standing diagnostic challenge where clinical and histopathological features overlap sufficiently to cause diagnostic uncertainty that affects treatment selection across the estimated 125 million psoriasis and 230 million atopic dermatitis patients globally.

Market Size and Forecast:

-

Market Size in 2026E: USD 15.28 Billion

-

Market Size by 2035: USD 28.31 Billion

-

CAGR: 7.11% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Laboratory Developed Tests Market - Request Free Sample Report

Laboratory Developed Tests Market Trends:

-

Integration of next-generation sequencing (NGS) technologies is expanding the use of LDTs for comprehensive genomic profiling, particularly in precision oncology and personalized medicine applications

-

Growing development of liquid biopsy-based LDTs is enabling minimally invasive cancer detection, treatment monitoring, and disease surveillance through blood-based testing

-

AI and machine learning tools are improving LDT interpretation by enhancing diagnostic accuracy, streamlining variant classification, and supporting clinical decision-making

-

Advancements in CRISPR-based diagnostic technologies are creating opportunities for highly sensitive and specific LDTs in infectious disease detection and genetic disorder testing

-

Increasing regulatory oversight and compliance requirements are driving investments in validation, quality management systems, and clinical evidence generation among LDT providers

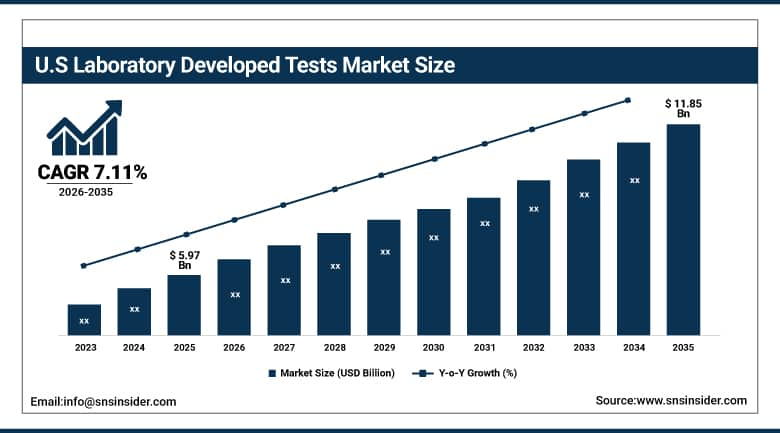

U.S. Laboratory Developed Tests Market Outlook:

The U.S. Laboratory Developed Tests Market was valued at approximately USD 5.97 Billion in 2025 and is expected to reach approximately USD 11.85 Billion by 2035, growing at a CAGR of approximately 7.11%.

The U.S. is the world's most commercially significant LDT market within North America's dominant regional position. The FDA's LDT Final Rule, published in May 2024, creates the most significant regulatory transformation in the U.S. LDT market's history by phasing in medical device oversight requirements across a four-year timeline, creating compliance investment that sustains established laboratory operators’ competitive advantage over smaller entrants. The precision oncology market's demand for comprehensive genomic profiling, the hereditary cancer risk assessment market, and the expanding pharmacogenomics testing adoption collectively creates the most commercially sophisticated LDT procurement environment globally.

In 2024, Foundation Medicine launched FoundationOne Liquid CDx enhancements incorporating expanded tumour mutation burden quantification and microsatellite instability assessment from circulating tumour DNA, enabling oncologists to access comprehensive liquid biopsy genomic profiling in patients where tissue biopsy is contraindicated or technically challenging, simultaneously supporting companion diagnostic co-labelling for multiple FDA-approved targeted therapies across solid tumour indications.

Laboratory Developed Tests Market Segment Analysis:

-

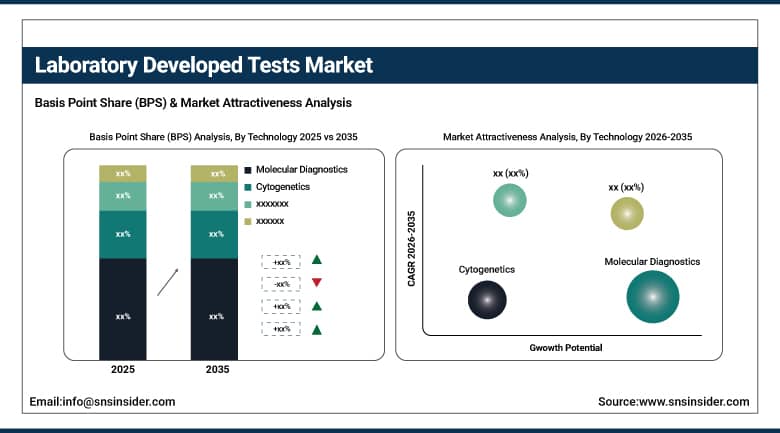

By Technology, the Molecular Diagnostics segment dominated the Laboratory Developed Tests Market with approximately 26.3% share in 2025, while the Next-Generation Sequencing sub-segment is the fastest growing.

-

By Test Type, the Molecular Tests segment dominated the Laboratory Developed Tests Market with approximately 38% share in, while the Cytogenetic Tests segment is the fastest growing.

-

By Disease Area, the Oncology segment dominated the Laboratory Developed Tests Market with approximately 34% share in 2025, while the Rare & Genetic Disorders segment is the fastest growing.

-

By End User, the Hospital-Based Laboratories segment dominated the Laboratory Developed Tests Market with approximately 42% share in 2025, while the Independent/Reference Laboratories segment is the fastest growing.

-

By Sample Type, the Blood segment dominated the Laboratory Developed Tests Market with approximately 38% share in 2025, while the Liquid Biopsy/ctDNA segment is the fastest growing.

By Technology, molecular diagnostics dominates, NGS grows fastest

Molecular diagnostics retained the dominant technology position with approximately 26.3% of the laboratory developed tests market in 2025. The technology's commercial primacy reflects the extraordinary clinical utility breadth of PCR, quantitative RT-PCR, ddPCR, FISH, and NGS methodologies across oncology, infectious disease, hereditary disorder, and pharmacogenomics LDT categories. Each clinical question that requires genetic or molecular-level diagnostic precision creates a molecular diagnostics LDT procurement need that immunological and biochemical testing alternatives cannot address with equivalent precision.

NGS is the fastest-growing technology sub-segment because comprehensive genomic profiling's clinical utility in oncology companion diagnostic testing, hereditary risk assessment, and rare disease diagnosis is creating above-average adoption across hospital and reference laboratory settings. Each new targeted therapy approval that specifies NGS-based companion diagnostic testing creates a structured LDT procurement requirement that drives NGS platform adoption in clinical laboratories. Foundation Medicine's FoundationOne CDx, Quest Diagnostics' tumour profiling panels, and Mayo Clinic's Expanded Carrier Screening LDTs demonstrate the commercial scale of NGS-based LDT deployment.

By Disease Area, oncology dominates, rare & genetic disorders grow fastest

Oncology retained the dominant disease area position with approximately 34% of the laboratory developed tests market in 2025. The commercial primacy of oncology LDTs reflects the intersection of clinical urgency, per-test commercial value, and treatment decision dependence that creates the most commercially compelling LDT procurement environment. Each tumour comprehensive genomic profiling order, each minimal residual disease monitoring assessment, and each pharmacogenomics test guiding oncology drug selection creates LDT procurement whose per-test commercial value substantially exceeds equivalent non-oncology diagnostic testing. The precision oncology paradigm's systematic requirement for tumour molecular characterization before targeted therapy initiation creates a structural clinical LDT demand that grows proportionally with oncology drug approval rates.

Rare and genetic disorders is the fastest-growing disease area because NGS-based exome and genome sequencing has fundamentally changed the diagnostic capability for rare disease presentations that previously required years-long diagnostic odysseys without genetic testing access. The NIH's Undiagnosed Diseases Network, the newborn screening programme expansions adopting NGS-based metabolic disorder screening, and the hereditary cardiovascular disorder testing market collectively create above-average rare disease LDT procurement. Each state newborn screening programme that adds an NGS-based condition creates structured LDT procurement whose clinical pathway development creates long-duration laboratory procurement relationships.

By End User, hospital labs dominate, reference labs grow fastest

Hospital-based laboratories retained the dominant end-user position with approximately 42% of the laboratory developed tests market in 2025. Their commercial primacy reflects the direct integration with clinical care that hospital laboratories provide, enabling institution-specific assay development for complex patient populations, rapid result turnaround that urgent clinical decision-making requires, and the ability to modify testing protocols in response to institutional patient care programme changes without external send-out logistics. Academic medical Centre laboratories whose LDT development programme’s create novel assays that diffuse into clinical practice through publication and standardization represent the most commercially significant single sub-category within hospital-based LDT operations.

Independent and reference laboratories are the fastest-growing end user because centralized high-throughput NGS operations, national send-out testing network scale economies, and the progressive concentration of complex molecular testing in specialist reference laboratory environments create above-average commercial volume growth. Quest Diagnostics’ and LabCorp’s national laboratory networks, whose combined annual testing volume exceeds 300 million accessions, create the platform scale that sustains investment in premium NGS and molecular LDT capability beyond the financial reach of individual hospital laboratory programme’s.

By Sample Type, blood dominates, liquid biopsy grows fastest

Blood retained the dominant sample type position with approximately 38% of the laboratory developed tests market in 2025. As the most accessible, highest-volume, and most informative clinical specimen type, blood enables LDT applications across hematological malignancy morphology and molecular testing, infectious disease serology, therapeutic drug monitoring, pharmacogenomics genotyping, and circulating biomarker measurement. Each clinical encounter that generates a venipuncture creates potential multiple LDT testing opportunities whose commercial aggregate across the global healthcare system creates blood's dominant sample type position. The high sample volume, standardized pre-analytical protocols, and established transport logistics infrastructure for blood specimens create the lowest operational complexity of any sample type for both hospital and reference laboratory LDT operations.

Liquid biopsy and circulating tumour DNA are the fastest-growing sample type because tumour genomic profiling from peripheral blood provides minimally invasive access to cancer molecular characterization that tissue biopsy's procedure burden, access limitations, and sampling heterogeneity create demand to supplement or replace. Each oncology patient whose treatment monitoring requires serial genomic assessment creates liquid biopsy LDT procurement whose frequency advantage over repeat tissue biopsy creates above-average per-patient test volume. Foundation Medicine's FoundationOne Liquid CDx and Guardant Health's Guardant360 demonstrate the commercial scale of liquid biopsy LDT adoption in oncology care.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Laboratory Developed Tests Market Insights

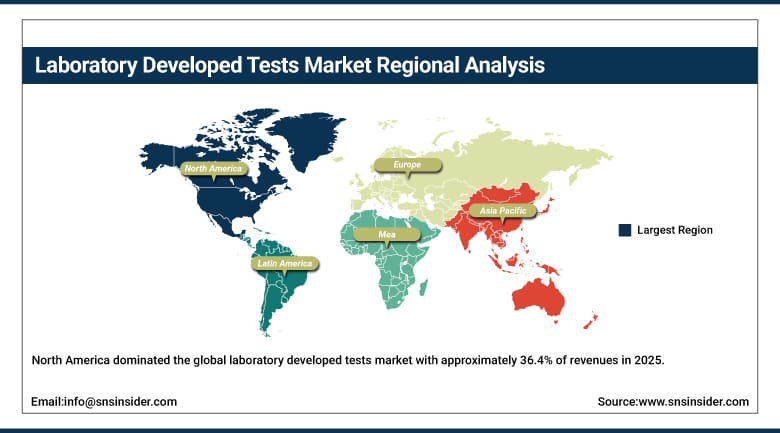

North America dominated the global laboratory developed tests market with approximately 36.4% of revenues in 2025, driven by advanced healthcare infrastructure, substantial investment in genomics research, a well-established regulatory framework, and high levels of private and government healthcare spending on precision diagnostics. The United States accounts for approximately 87.4% of North American revenues through Quest Diagnostics, LabCorp, Mayo Clinic Laboratories, Foundation Medicine, and Myriad Genetics’ commercial operations.

Canada contributes approximately 12.6% of North American revenues through its publicly funded healthcare system's laboratory testing investment, the academic medical Centre LDT programme network, and the growing precision oncology market's genomic profiling adoption.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Laboratory Developed Tests Market Insights

Europe is a technically sophisticated LDT market where the EU In Vitro Diagnostics Regulation 2017/746’s progressive implementation creates a compliance environment that sustains above-average quality investment in LDT programmes. Germany accounts for approximately 22.3% of European revenues through its academic hospital laboratory programme strength, the pharmaceutical industry’s companion diagnostic development partnerships, and the genetic disorder testing market's hereditary disease prevalence.

The United Kingdom, France, and the Netherlands are significant secondary markets where NHS genomic medicine programme investment, Institut Curie’s oncology LDT capabilities, and the Erasmus MC's reference laboratory network create consistent LDT commercial demand. Eurofins Genomics’ European operations and Sonic Healthcare’s European laboratory network sustain regional supply infrastructure.

Asia Pacific Laboratory Developed Tests Market Insights

Asia Pacific is the fastest-growing regional LDT market, driven by China’s oncology precision medicine investment, India's growing reference laboratory infrastructure, Japan’s advanced molecular diagnostics adoption, South Korea’s genomics innovation, and the regional cancer incidence burden that creates structured oncology LDT demand. China accounts for approximately 44.8% of Asia Pacific revenues through BGI Genomics’ and Burning Rock Biotech’s NGS-based oncology LDT operations, the government’s precision medicine initiative investment, and the extraordinary cancer patient volume whose genomic profiling requirement creates above-average oncology LDT procurement.

India represents the most commercially dynamic emerging market within Asia Pacific where the growing reference laboratory sector’s Metropolis Healthcare, Dr Lal PathLabs, and SRL Diagnostics’ molecular testing expansion, combined with the oncology testing market’s systematic NGS adoption, create above-average LDT market growth from a rapidly expanding commercial base.

MEA & Latin America Laboratory Developed Tests Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s healthcare modernization investment, King Faisal Specialist Hospital’s established LDT programme, and the precision oncology market’s rapidly growing genomic testing adoption. The UAE’s expanding genomics and personalized medicine infrastructure investment adds substantial complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through Fleury Medicina e Saúde’s molecular diagnostics operations, the growing oncology testing market, and the genetic disorder testing sector. Mexico’s growing reference laboratory infrastructure and Argentina’s academic medical LDT programmes collectively sustain regional market development through 2035.

Market Dynamics:

Growth Drivers: Precision oncology adoption and FDA LDT regulatory framework creating quality-differentiated market structure

Precision oncology's systematic requirement for comprehensive tumour molecular profiling before targeted therapy initiation is the LDT market's most commercially significant structural growth driver. Each FDA approval of a targeted therapy whose indication requires companion diagnostic genomic testing creates a structured LDT procurement pathway in laboratories not yet equipped with the FDA-approved companion diagnostic assay, sustaining LDT utilization while companion diagnostic availability catches up with drug approval. The extraordinary pace of oncology drug approval, with the FDA approving 50-70 oncology drugs annually in recent years, creates proportional companion diagnostic and genomic profiling demand that sustains oncology LDT market growth.

The FDA's LDT Final Rule, published in May 2024 and phasing in medical device regulatory requirements over a four-year timeline, creates compliance investment that elevates the technical and documentary standard for LDT market participation. The regulatory framework simultaneously creates competitive barriers for smaller laboratory operators whose compliance investment capacity limits and creates quality differentiation opportunities for established reference and hospital laboratory operators whose compliance programme investment sustains premium pricing and sends-out testing relationships.

Restraints: FDA regulatory compliance burden and reimbursement coverage uncertainty

FDA regulatory compliance burden under the LDT Final Rule creates operational cost increases for laboratory operators whose LDT portfolio breadth requires extensive analytical validation, clinical validity demonstration, and quality system documentation investment. Each novel LDT whose regulatory submission pathway creates engineering, analytical, and clinical data generation costs that single-laboratory commercial economics may not justify creates potential market consolidation pressure that reduces LDT variety in niche testing categories.

Reimbursement uncertainty for novel molecular LDTs, particularly NGS-based comprehensive genomic profiling panels whose multi-gene analysis creates coding and coverage determination complexity across Medicare, Medicaid, and private payer systems, creates revenue uncertainty that limits laboratory operator investment in novel assay development. Each coverage determination process that delays LDT reimbursement from assay launch to payer coverage creates a revenue gap period whose financing requirement moderates the pace of novel LDT commercial introduction.

Opportunities: Pharmacogenomics testing expansion and CRISPR-based diagnostic development

Pharmacogenomics testing expansion represents the most commercially accessible near-term LDT market growth opportunity whose systematic medication safety and efficacy optimization application creates consistent LDT procurement across primary care, oncology, psychiatry, and cardiology clinical settings. Each healthcare system that adopts preemptive pharmacogenomics testing creates LDT procurement whose per-patient test panel generates results applicable to lifetime medication management, creating above-average long-term institutional value from single LDT investments.

CRISPR-based diagnostic development represents the most commercially transformative emerging technology opportunity whose target-specific nucleic acid detection capability at room temperature without sophisticated laboratory instrumentation creates point-of-care LDT potential beyond conventional laboratory-confined molecular diagnostics. The technology's programmable target recognition and visual read-out capability creates decentralized diagnostic applications whose simplicity advantage over PCR sustains development investment.

Recent Developments:

-

2025: Molecular Instruments, Inc. introduced HCR Pro RNA-ISH technology LDTs in February 2025 featuring a four-biomarker panel for accurate differentiation of psoriasis and atopic dermatitis in skin biopsies, developed in collaboration with Yale School of Medicine's Department of Dermatology.

-

2024: Foundation Medicine launched FoundationOne Liquid CDx enhancements in 2024 incorporating expanded tumour mutation burden quantification and MSI assessment from circulating tumour DNA, enabling comprehensive liquid biopsy genomic profiling for oncology patients where tissue biopsy is contraindicated.

-

2024: The FDA published the LDT Final Rule in May 2024, phasing in medical device regulatory requirements for laboratory-developed tests over a four-year timeline, fundamentally changing the regulatory compliance framework for the U.S. LDT market and creating structured quality investment across the laboratory industry.

-

2023: Quest Diagnostics expanded its oncology LDT portfolio in 2023 with new comprehensive tumour mutation burden and homologous recombination deficiency testing panels, enabling oncologists to identify patients most likely to respond to PARP inhibitors and immune checkpoint inhibitor therapies across multiple solid tumour types.

-

2023: In May 2023, Bio-Techne launched Kappa and Lambda RNAscope ISH Probes as Analyte Specific Reagents for detecting immunoglobulin kappa and lambda light chain mRNA in B-cells, supporting LDT development for B-cell clonality assessment in lymphoma diagnosis with high sensitivity in FFPE tissue specimens.

Laboratory Developed Tests Market Key Players:

-

Quest Diagnostics Incorporated

-

Laboratory Corporation of America (LabCorp)

-

Mayo Clinic Laboratories

-

Foundation Medicine Inc.

-

Myriad Genetics Inc.

-

BioReference Laboratories Inc. (GenPath Oncology)

-

Ambry Genetics (Konica Minolta)

-

ARUP Laboratories

-

Sonic Healthcare Ltd.

-

Eurofins Genomics

-

Guardant Health Inc.

-

Tempus AI Inc.

-

NeoGenomics Laboratories Inc.

-

Invitae Corporation

-

Genomic Health (Exact Sciences)

-

BGI Genomics Co. Ltd.

-

Burning Rock Biotech Ltd.

-

Natera Inc.

-

Pacific Biosciences of California Inc.

-

Veracyte Inc.

Laboratory Developed Tests Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.27 Billion |

| Market Size by 2035 | USD 28.31 Billion |

| CAGR | CAGR of 7.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Technology (Molecular Diagnostics, Immunoassay/Serology, Cytogenetics, Biochemistry, Hematology, Microbiology & Culture, Others) • by Test Type (Molecular Tests, Immunological Tests, Cytogenetic Tests, Biochemical Tests, Microbiological Tests, Others) • by Disease Area (Oncology, Infectious Diseases, Rare & Genetic Disorders, Cardiovascular Diseases, Neurological Disorders, Autoimmune Diseases, Others) • by End User (Hospital-Based Laboratories, Independent/Reference Laboratories, Physician Office Laboratories, Academic & Research Institutions, Others) • by Sample Type (Blood, Tissue Biopsy, Urine, Saliva, Liquid Biopsy/ctDNA, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Quest Diagnostics Incorporated, Laboratory Corporation of America (LabCorp), Mayo Clinic Laboratories, Foundation Medicine Inc., Myriad Genetics Inc., BioReference Laboratories Inc. (GenPath Oncology), Ambry Genetics (Konica Minolta), ARUP Laboratories, Sonic Healthcare Ltd., Eurofins Genomics, Guardant Health Inc., Tempus AI Inc., NeoGenomics Laboratories Inc., Invitae Corporation, Genomic Health (Exact Sciences), BGI Genomics Co. Ltd., Burning Rock Biotech Ltd., Natera Inc., Pacific Biosciences of California Inc., Veracyte Inc. |

Frequently Asked Questions

The Laboratory Developed Tests Market is expected to grow at a CAGR of 7.11% from 2026 to 2035.

The Laboratory Developed Tests Market was valued at USD 14.27 Billion in 2025.

Precision oncology's systematic requirement for comprehensive tumour molecular profiling creating structured NGS-based LDT procurement, and the FDA's LDT Final Rule creating regulatory compliance investment that differentiates established laboratory operators and sustains premium market positioning.

Molecular Diagnostics dominated the Laboratory Developed Tests Market with approximately 26.3% share in 2025, while NGS is the fastest growing sub-segment.

North America dominated the Laboratory Developed Tests Market with approximately 36.4% of revenues in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch