Inverter Welding Equipment Market Report Scope & Overview:

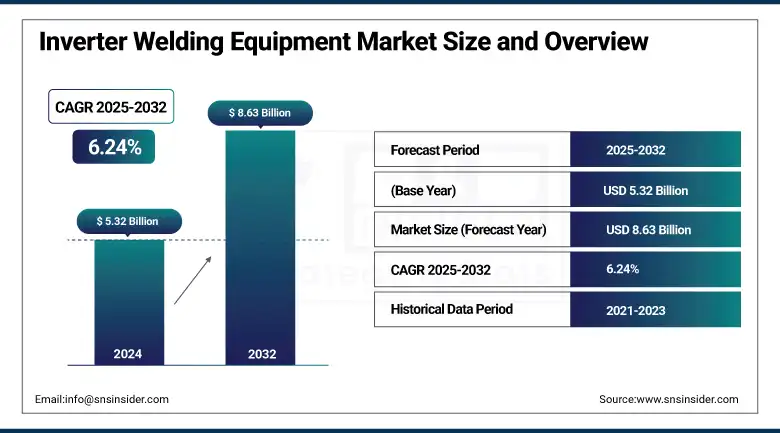

The Inverter Welding Equipment Market size was valued at USD 5.32 billion in 2024 and is expected to reach USD 8.63 billion by 2032, growing at a CAGR of 6.24% over the forecast period of 2025-2032.

The growing demand for compact, energy-efficient, and high-performance welding solutions is fueling the growth of the global Inverter Welding Equipment Market, specifically the Inverter Welder Market, Inverter welding machine market, and portable welding machines. These machines are popular for their lightweight construction, portability, low power consumption, and their ability to provide a uniform quality of weld for applications including automotive, construction, fabrication, and maintenance. Industrial Automation and the Need for Flexible and Reliable Welding Technologies are the Driving Factors of the Inverter Welding Equipment Market Growth.

To Get more information On Inverter Welding Equipment Market - Request Free Sample Report

Inverter-based systems provide accurate weld parameter control, smoother operation, and improved arc stability when compared to their traditional machine counterparts. This is also positively influencing the market growth, as more professionals and hobbyists are using portable welding machines. Advanced digital controls, pulse welding technology, and a smart interface enable users to monitor and adjust performance in real-time, thereby making it easier to control the inverter welder than anything on the market. Another area of innovation is the capability to offer multiple processes in a single machine, running TIG, MIG, and Stick capability in the same multi-process inverter welder. This not only enhances effectiveness and productivity but also minimizes downtime, resulting in the widespread popularity of inverter welders in contemporary welding applications.

In January 2025, Crossfire Welders identified five key innovations reshaping the welding industry. These include Collaborative Robots (Cobots) for enhanced precision, handheld laser welders like the HGLW 1500 for efficient, consumable-free operation, and advanced welding materials offering greater strength and flexibility. Also gaining traction are battery-powered welders for mobility and digital interfaces for real-time control. These technologies collectively boost efficiency, adaptability, and weld quality across sectors.

Inverter Welding Equipment Market Dynamics:

Drivers:

-

Surging Demand for Portable, Energy-Efficient Inverter Welding Machines Drives Innovation and Sustainability Across Key Industries

Rising use of portable inverter welding machines with low energy consumption in automotive and aerospace sectors, construction has opened new opportunities. Being lightweight and compact, these machines provide improved mobility and performance owing to their high-power efficiency. Most inverter systems have high-end controls to offer arc stability and efficiency across all welding processes, including high-frequency switching technology. In addition to this, increasing penetration of smart technologies and machinery automation in inverter welding equipment is further aiding precision and efficiency, in accordance with the larger mix of smart manufacturing. The trend can also be further propelled by the rising need to adopt sustainability and energy-efficient systems in the manufacturing process, as power consumption is relatively lower with inverter welding machines compared to the conventional ones, thus decreasing the overall operating cost and carbon footprint on the environment.

In October 2024 – The inverter welding equipment market is expanding rapidly, driven by demand for lightweight, portable, and energy-efficient machines in industries including automotive and construction. These welders offer precise control and up to 40% energy savings. Growth is supported by industrialization in emerging economies and the rise of electric vehicles.

Restraints:

-

High Initial Investment and Increased Maintenance Costs Pose Significant Adoption Challenges for Inverter Welding Equipment for Small and Medium-Sized Enterprises

The capital and operational expenditure on inverter welding equipment is high, which limits the ability of small and medium-sized enterprises (SMEs) to invest in such technologies. They have an initial cost that is higher than that of the traditional model, but this is compensated by the efficiency, they are more portable and they are more advanced machines. Furthermore, due to the special components and technology, maintenance costs are usually 15–20% higher. Some companies have also claimed as high as USD 303 of annual electricity savings per inverter, but the initial cost is a barrier for many SMEs. The mismatch between high data needs and low funding is especially acute in developing countries, where budget constraints are the tightest. Hence, the initial costs can put companies off inverter welding, even if the business case is there in the longer term.

Inverter Welding Equipment Market Segmentation Outlook:

By Type

Mechanized Arc Welding segment dominated the market and accounted for 80% of the Inverter Welding Equipment Market share. Advantages of higher productivity, consistent and accurate output are the key factors to drive the growth of this segment in robust industrial applications. Advanced mechanized welding requires inverter technology to control welding parameters, improve energy consumption, and enhance overall weld quality. Various industries, including automotive, aerospace, and shipbuilding, prefer mechanized arc welding to maintain continuous and automated processes, thereby optimizing efficiency and reducing labor costs, which, in turn, has contributed to sustained market strength.

Manual Arc Welding is the fastest-growing segment in the inverter welding equipment market due to its high efficiency in welding most materials, such as metals. The increasing demand for portable and compact welding appliances, which provide higher flexibility in the field, is driving this growth. Inverter-powered manual arc welding machines offer better control of the welding arc, high energy efficiency, stability of the arc, and ease of use, and are therefore suitable for small workshops, repairing jobs, and construction sites. This rising popularity, especially among small and medium-sized enterprises (SMEs), is largely attributable to their ability to adapt to different metals and thicknesses and to the relatively low initial investment required compared with more mechanized systems.

By Power Supply

The 1-phase power supply segment dominated with a market share of over 58% in 2024, owing to the availability of power, and its applicability for small to medium-scale welding operations. It is suited for big production units, shipbuilding, and the automotive industry, where the load is high and requires continuous welding processes. The larger machines can also run off a 3-phase supply, which in return provides a higher output, superior performance, and enhanced stability, which is ideal for high volume production and complex welding processes. Supported by industrial automation and increasing demand from the capital-intensive sector.

The 3-phase power supply segment is the fastest growing in the inverter welding market. The growth of the 3-phase power supply segment can be attributed to the higher efficiency and capability to carry out heavy-duty industrial welding applications. Ideal for high volume production units, shipbuilding, and automobile industries where high power loads would prevail, and the welding process is continuous. It is suited for high volume productions and complex welding processes, as the larger machines provide more output, enhanced performance and stability, and a 3-phase supply. It is driven by growing industrial automation and demand from heavy industries.

By End-Use

The aerospace segment dominated with a market share of over 32% in 2024. These elements have made the industry hold the highest quality and accuracy requirements, which has then resulted in this form of market dominance. For Aerospace welding, along with a purposeful novelty adhesives and great welder technique is crucially needed, and the exact will become a complement for just that need, basically because of inverter welders. The first mention of floating items hints at possible high-quality, high-duty welding equipment required to weld lightweight and high-strength materials, which are essential in aircraft manufacture and maintenance within the aerospace industry.

The automotive segment is the fastest-growing end-use segment for inverter welding equipment. The increasingly dynamic automotive industry, which is transforming itself to produce environmentally friendly electric vehicles (EVs), lightweight materials including aluminum and composites, and uses game-changing automated manufacturing processes, requires welding processes that are compact and flexible. Inverter welders are suited for assembly line and robotic welding applications as used in automotive plants. Light, but very precise and energy efficient. This segment benefits from the global growth of vehicle production and the shift toward inverter welding technology, owing to advantages, such as faster, cleaner, and more dependable welds.

Inverter Welding Equipment Market Regional Analysis:

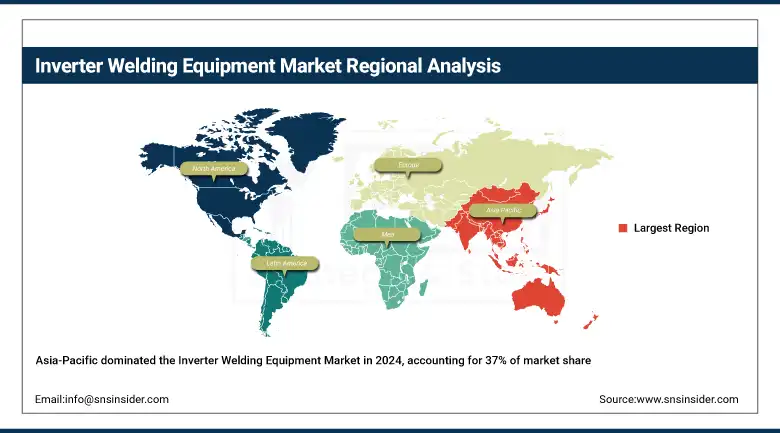

The Asia-Pacific region dominated with a market share of over 37% in 2024. The reason behind this predominance is the fast-emerging industries, especially in nations including China, India, and Japan. Continuous demand for portable and efficient welding solutions from the growing automotive, construction, and manufacturing industries in the region is driving the market. Furthermore, the robust growth of the market can be attributed to rising infrastructure projects and increasing government initiatives to enhance manufacturing capacities. Other factors supporting Asia-Pacific dominance in the global inverter welding market are the availability of skilled labor and many manufacturers of welding equipment.

Get Customized Report as per Your Business Requirement - Enquiry Now

China leads the Asia-Pacific inverter welding equipment market due to its large manufacturing base and rapid industrialization. The high demand for sophisticated welding technologies is due to the country's emphasis on infrastructure development and automotive manufacturing. Besides this, it also boosts the Chinese market in this region due to government support in modernization and the use of efficient welding machines.

North America is identified as the fastest-growing region in the inverter welding equipment market. Some of the factors contributing to this growth include the growth of technology, increasing adoption of automated welding systems, and growing investment in the infrastructure and aerospace sector. The U.S. and Canada are experiencing a demand for inverter welders owing to the enhanced efficiency, portability, and energy-saving benefits they provide. In addition, government policies supporting high-end manufacturing and electric energy-saving technologies stimulate the utilization of inverter welding machines, which are promoting the rapid expansion of the market in this region.

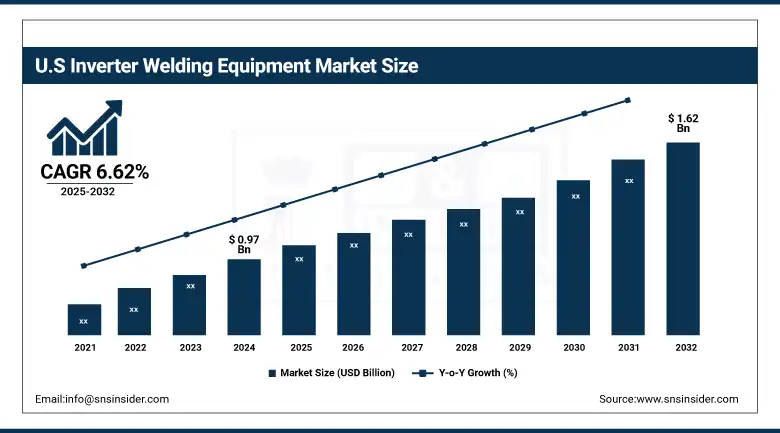

The U.S. inverter welding equipment market is expected to grow from USD 0.97 billion in 2024 to USD 1.62 billion by 2032, with a CAGR of 6.62%. The growth is mainly attributed to rising industrial automation, increasing demand for energy-efficient and portable Welders, along with the growing automotive and aerospace sectors. Increasing infrastructure development and adoption of advanced technology benefits the market.

Europe maintains a significant share of the inverter welding equipment market, supported by strong industrial bases in Germany, France, and the U.K. Automotive and aerospace sectors in the region have rigorous quality standards while precision welding is given due attention. Additionally, Europe is dedicated to sustainable manufacturing practices and energy-efficient processes, which drive the demand for inverter welding technology. There is a continuous design and innovation that leads to a steady demand. Europe is another prominent market due to the presence of leading welding equipment manufacturers and a rising degree of automation in various manufacturing sectors.

Inverter Welding Equipment Market Companies are:

ESAB, Fronius International GmbH, Kemppi Oy, Panasonic Industry Co., Ltd., Ador Welding Limited, The Lincoln Electric Company, Migatronic A/S, GYS, Miller Electric Mfg. LLC, and voestalpine Böhler Welding Group GmbH.

Recent Developments:

In August 2024, Kemppi participated in FinnMETKO 2024, Finland’s largest construction and forestry machinery exhibition held in Jämsä. They showcased their latest welding equipment, including the X3 FastMig and Minarc T 223 ACDC models. The event featured live demos and seminars, highlighting innovations in welding technology. FinnMETKO attracted over 30,000 visitors and 340 exhibitors, providing great industry networking opportunities.

In April 2025, Ador Welding Ltd. is driving innovation and sustainability by adopting digital welding technologies for better efficiency and predictive maintenance. They launched Rhino E, India’s first battery-powered electric welder, to reduce emissions and noise. Additionally, Ador patented a hybrid welding method that increases deposition rates without spatter, strengthening their leadership in welding technology.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.32 Billion |

| Market Size by 2032 | USD 8.63 Billion |

| CAGR | CAGR of 6.24% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Manual Arc Welding [MIG, TIG, Plasma], Mechanized Arc Welding [MIG, TIG, Plasma]) • By Power Supply (1 Phase, 3 Phase), By End Use (Aerospace, Automotive, Building & Construction, Energy, Oil & Gas, Marine, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ESAB, Fronius International GmbH, Kemppi Oy, Panasonic Industry Co., Ltd., Ador Welding Limited, The Lincoln Electric Company, Migatronic A/S, GYS, Miller Electric Mfg. LLC, voestalpine Böhler Welding Group GmbH. |

Frequently Asked Questions

The Asia-Pacific region dominated the Inverter Welding Equipment Market in 2024.

The “Mechanized Arc Welding” segment dominated the Inverter Welding Equipment Market.

Surging Demand for Portable, Energy-Efficient Inverter Welding Machines Drives Innovation and Sustainability Across Key Industries

The Inverter Welding Equipment market was USD 5.32 billion in 2024 and is expected to reach USD 8.63 billion by 2032.

The Inverter Welding Equipment market is expected to grow at a CAGR of 6.24% from 2025-2032.

Get in Touch