IoT Security Market Report Scope & Overview:

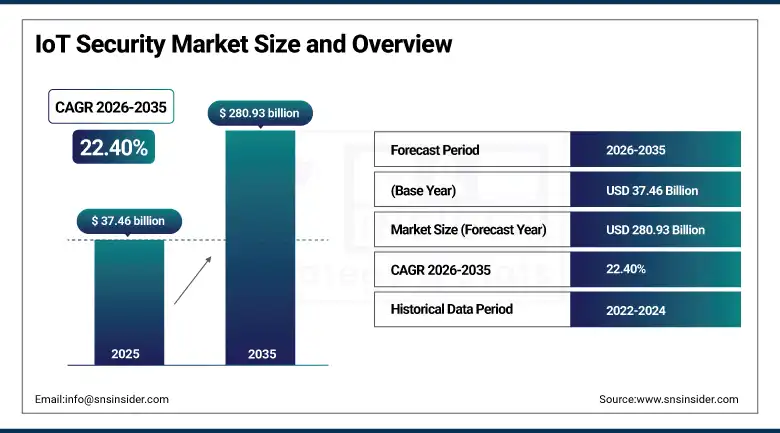

The IoT Security Market was valued at USD 37.46 Billion in 2025 and is expected to reach USD 280.93 Billion by 2035, growing at a CAGR of 22.40% from 2026–2035.

IoT security market around the world is witnessing phenomenal growth. The number of devices currently estimated worldwide has surpassed 15 billion and is set to reach a staggering number of 29 billion by 2030. Such an increase provides an incredibly large attack surface. IoT devices are intrinsically vulnerable. They are shipped with default passwords, lack any way of being updated and employ light weight firmware, which cannot accommodate traditional endpoint security software. Industries such as manufacturing facilities or even medical IoT are prime targets for cybercriminals. A ransomware attack in these industries can cripple their functioning and result in immediate losses. Regulations, such as the EU Cyber Resilience Act, NIST IoT security guidelines, and CISA’s critical infrastructures requirements are forcing companies into compliance procurement. Behavioral analytics using AI and zero trust device identification is the solution.

In Q2 2025, Fortinet partnered with Siemens to deliver integrated IoT security for smart factories, co-developing solutions for industrial IoT protection in smart manufacturing environments. The partnership targets the convergence of IT and OT networks in modern industrial facilities where a single compromised IoT device can cascade into operational shutdown. The collaboration reflects the commercial recognition that industrial IoT security requires both IT cybersecurity expertise and deep OT operational knowledge.

Market Size and Forecast

-

Market Size in 2026E: USD 45.85 Billion

-

Market Size by 2035: USD 280.93 Billion

-

CAGR: 22.40% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On IoT Security Market - Request Free Sample Report

IoT Security Market Trends

-

AI-powered behavioral analytics is improving threat detection by identifying anomalous device activity beyond traditional signature-based methods.

-

Growing adoption of zero-trust security architectures is strengthening protection against unauthorized access and lateral movement across IoT networks.

-

Device identity management and automated certificate lifecycle solutions are becoming essential for large-scale IoT deployments.

-

Increasing cybersecurity regulations are driving security-by-design implementation and compliance investments for connected devices.

-

IT-OT security convergence is accelerating demand for unified platforms that secure enterprise and industrial IoT environments through a single management framework.

U.S. IoT Security Market Outlook

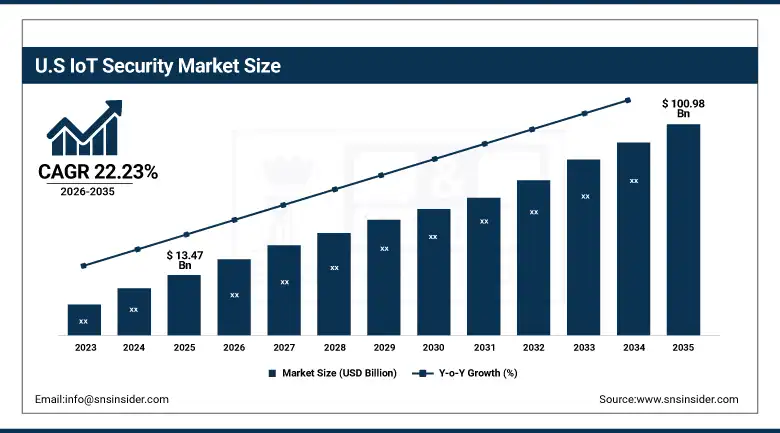

The U.S. IoT Security Market was valued at approximately USD 13.47 Billion in 2025 and is expected to reach approximately USD 100.98 Billion by 2035, growing at a CAGR of approximately 22.23%.

The U.S. is the world’s most commercially significant IoT security market. Nearly 50% of global ransomware attacks target U.S. organisations. MEITY data confirms that 98% of IoT device traffic is unencrypted, creating persistent systemic vulnerability. DHS awarded Tenable a USD 50 million contract in Q1 2025 for federal IoT device risk management, demonstrating government-level procurement urgency. Critical infrastructure sectors including energy, water, transportation, and healthcare are subject to mandatory security investment under CISA guidance. Palo Alto Networks, Cisco, Microsoft, and CrowdStrike are the dominant enterprise IoT security vendors, each offering integrated IoT security within broader security platform ecosystems.

In Q1 2025, the U.S. Department of Homeland Security awarded a USD 50 million contract to Tenable for IoT device risk management and vulnerability assessment services across federal IoT infrastructure. The contract validates federal government recognition of IoT vulnerability as a tier-one national security concern and creates institutional procurement momentum that extends into state and local government IoT security investment through reference case influence.

IoT Security Market Segment Analysis

-

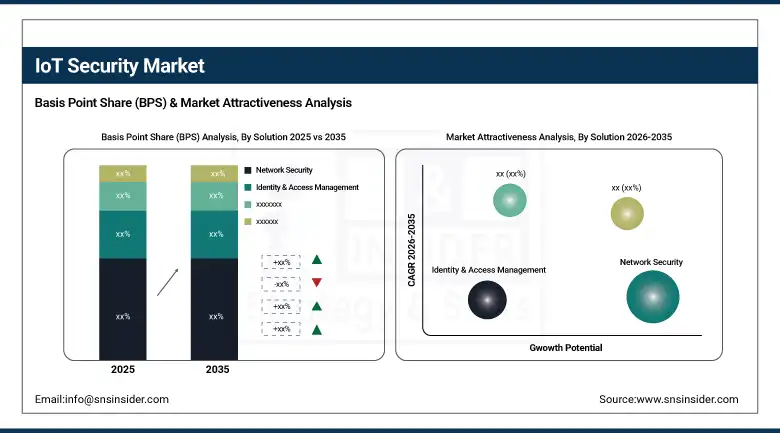

By Solution, network security segment dominated the IoT security market with approximately 36% market share in 2025, while the identity & access management segment is the fastest growing at a CAGR of 21.4% during 2026–2035.

-

By Deployment, cloud segment dominated the market with around 58% share in 2025, while the hybrid deployment segment is the fastest growing at a CAGR of 22.1% during 2026–2035.

-

By End User, manufacturing segment dominated the market with approximately 28% share in 2025, while the healthcare segment is the fastest growing at a CAGR of 23.3% during 2026–2035.

By Solution, network security dominates, IAM grows fastest

Network security retained the dominant solution position in the IoT security market in 2025. It is the most universally deployed security control because it operates at the network layer without requiring agents on individual IoT devices. IoT devices cannot run security software. Network-level monitoring is therefore the only viable approach for billions of resource-constrained devices. Deep packet inspection, network traffic analysis, and machine learning-based anomaly detection at network chokepoints enable security operations teams to identify compromised devices, block command-and-control communications, and segment vulnerable devices from critical enterprise systems without touching each individual endpoint.

Identity and access management is the fastest-growing segment because zero-trust architecture adoption requires every IoT device to have a verified, manageable identity. Legacy IoT deployments used shared credentials, hardcoded passwords, and no formal identity management. Modern deployments require PKI-based certificate issuance, automated certificate rotation, and revocation capability for millions of devices. The commercial scale of this capability gap is driving investment in specialised IoT IAM platforms that automate device identity lifecycle management at the operational scale that manual processes cannot serve.

By End User, manufacturing dominates, healthcare grows fastest

Manufacturing retained the dominant end user position in the IoT security market in 2025. Manufacturing facilities deploy the highest density of OT-connected IoT devices of any industry sector. Industrial robots, CNC machines, quality sensors, SCADA systems, and predictive maintenance devices collectively create an enormous attack surface. A successful ransomware attack on a manufacturing IoT system can shut down an entire production line, creating quantifiable losses of USD millions per day. This operational risk creates strong procurement motivation that is independent of regulatory mandate.

Healthcare is the fastest-growing end user because connected medical devices are life-safety systems. Infusion pumps, patient monitors, imaging equipment, and clinical IoT devices that are compromised can directly harm patients. FDA guidance requires medical device manufacturers to address cybersecurity throughout the device lifecycle. Hospitals face regulatory penalties and accreditation risk from inadequate IoT security. These combined clinical and compliance pressures create the most urgent and fastest-growing institutional IoT security procurement environment of any industry vertical.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America IoT Security Market Insights

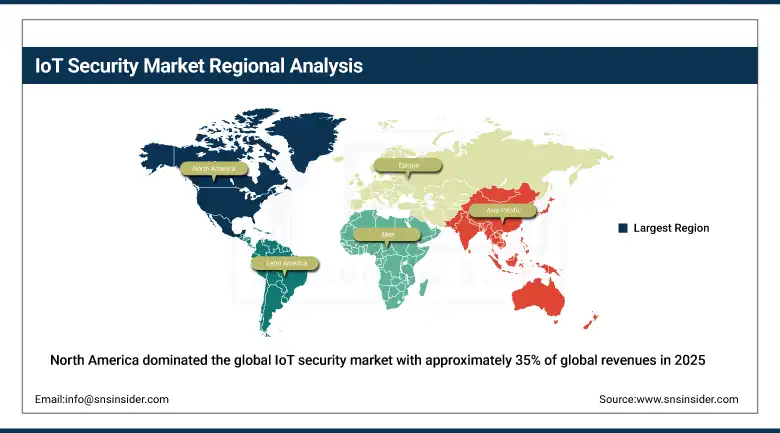

North America dominated the global IoT security market with approximately 35% of global revenues in 2025. The U.S. accounts for approximately 87.4% of North American revenues. The country’s combination of the highest critical infrastructure IoT deployment density, the most comprehensive regulatory framework, and the headquarters concentration of leading IoT security vendors creates the world’s most commercially advanced market. CISA mandatory reporting, the FCC’s IoT labelling programme, and sector-specific security requirements collectively create compliance-driven investment at scale.

Canada contributes approximately 12.6% of North American revenues through its energy sector’s OT security investment, financial services IoT security procurement, and federal government IoT security guidelines that create public sector demand aligned with U.S. standards.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe IoT Security Market Insights

Europe is a rapidly growing IoT security market where the EU Cyber Resilience Act’s mandatory security-by-design requirements for connected products, NIS2 Directive’s critical infrastructure security obligations, and GDPR’s IoT data processing security requirements collectively create the most comprehensive IoT security regulatory framework of any global region. Germany accounts for approximately 22.3% of European revenues through its industrial IoT manufacturing sector, Siemens and Bosch’s connected factory investment, and the BSI’s active IoT security standards development.

The United Kingdom, France, and the Netherlands are significant secondary markets. The UK PSTI Act creates mandatory security requirements for consumer IoT products. France’s critical infrastructure IoT security investment under ANSSI guidance and the Netherlands’ port and industrial IoT security programmes create structured demand that sustains consistent European market growth.

Asia Pacific IoT Security Market Insights

Asia Pacific is the fastest-growing regional IoT security market. The region contains the world’s largest and fastest-growing industrial IoT deployment base across China, India, South Korea, Japan, and Southeast Asia. China accounts for approximately 44.8% of Asia Pacific revenues through its massive smart manufacturing, smart city, and connected infrastructure investment. China’s National IoT Security Standards and the MIIT’s IoT security regulations create domestic compliance procurement that sustains market growth alongside voluntary adoption.

India and Southeast Asia are the most commercially dynamic emerging markets. India’s Digital India programme is deploying IoT infrastructure at national scale across smart cities, agriculture, and industrial manufacturing. The growing awareness of IoT attack risk is creating first-time security investment across organisations that previously deployed connected devices without security investment.

MEA & Latin America IoT Security Market Insights

The Middle East and Africa and Latin America are growing IoT security markets where smart city, energy, and industrial IoT deployments are creating structured security demand. UAE leads MEA revenues at approximately 38.4% through its smart city infrastructure programme, oil and gas sector OT security investment, and the UAE National Cybersecurity Strategy’s explicit IoT security requirements.

Brazil leads Latin American revenues at approximately 44.2% through its manufacturing sector’s industrial IoT investment, energy sector OT security, and LGPD data protection requirements that create IoT data security procurement motivation across regulated industry sectors.

Growth Drivers: IoT device proliferation expanding attack surface, regulatory mandates creating compliance-driven procurement, and ransomware targeting of industrial IoT creating quantifiable financial risk motivation

IoT device proliferation is the market’s most structurally certain growth driver. Each new connected device deployed without adequate security adds to the exploitable attack surface. The commercial scale of this growth is extraordinary. Over 15 billion IoT devices are connected today. Each represents a potential entry point. Security investment that scales with deployment growth creates a structurally growing market whose revenue is directly linked to the technology adoption that IoT security vendors cannot prevent and can only defend against.

Regulatory mandates are creating non-discretionary procurement across multiple markets simultaneously. The EU Cyber Resilience Act, NIST IoT guidance, FCC IoT labelling, and sector-specific security requirements collectively mandate security investment that organisations must demonstrate regardless of discretionary budget constraints. Each regulatory deadline creates a compliance procurement wave whose commercial scale reflects the number of affected organisations and the penalty risk of non-compliance.

Restraints: Heterogeneous device landscape complexity limiting universal solution deployment, limited computational resources on constrained IoT devices, and skills shortage in OT security expertise

IoT device heterogeneity is the market’s most significant technical restraint. Connected devices span a range from industrial PLCs to consumer smartwatches with fundamentally different operating systems, communication protocols, and security capability. No single security solution addresses this full spectrum. Organisations deploying multi-vendor IoT environments must manage multiple security tools whose integration complexity creates operational overhead that limits effective coverage.

OT security expertise scarcity creates implementation quality challenges. Industrial control system security requires knowledge of both IT cybersecurity and operational technology engineering that few practitioners possess. The Fortinet-Siemens partnership reflects the commercial recognition that IT security vendors alone cannot serve industrial IoT requirements without OT domain expertise partnerships.

Opportunities: AI-native IoT security platforms, secure-by-design device manufacturing compliance, and managed IoT security services for SME market expansion

AI-native IoT security represents the most commercially differentiated capability direction. Traditional signature-based detection cannot protect IoT environments where devices cannot run security agents. AI platforms that learn normal device communication baselines and detect anomalies in real time without device-side agents are the only technically viable approach at IoT deployment scale. Vendors whose AI models achieve superior anomaly detection accuracy with lower false positive rates gain defensible competitive positions in enterprise procurement.

Managed IoT security services are creating the most commercially accessible market expansion pathway for SMEs. Small manufacturers, healthcare facilities, and retailers deploy IoT devices without dedicated security teams. Managed service providers who bundle IoT device discovery, continuous monitoring, and incident response into affordable subscription packages serve the long tail of the market whose aggregate volume substantially exceeds large enterprise procurement.

Recent Developments:

-

2025: Fortinet partnered with Siemens in Q2 2025 to deliver integrated security solutions for industrial IoT in smart factory environments, co-developing IT-OT converged security capabilities that protect industrial control systems from threats exploiting connected manufacturing infrastructure.

-

2025: The U.S. Department of Homeland Security awarded a USD 50 million contract to Tenable in Q1 2025 for IoT device risk management and vulnerability assessment services across federal IoT infrastructure, validating government recognition of IoT security as a tier-one national security investment priority.

-

2024: Check Point Software launched Quantum IoT Protect for enterprise networks in Q2 2024, providing automated IoT device discovery, risk assessment, and segmentation policy enforcement for enterprise environments deploying diverse connected device populations across campus and industrial settings.

IoT Security Market Key Players:

-

Cisco Systems, Inc.

-

Palo Alto Networks, Inc.

-

Fortinet, Inc.

-

Check Point Software Technologies Ltd.

-

IBM Corporation

-

Microsoft Corporation

-

Broadcom Inc. (Symantec)

-

Trend Micro Incorporated

-

Honeywell International Inc.

-

Schneider Electric SE

-

Thales Group

-

Nozomi Networks Inc.

-

Claroty Ltd.

-

Forescout Technologies, Inc.

-

Armis Security Ltd.

-

Zscaler, Inc.

-

CrowdStrike Holdings, Inc.

-

Sophos Ltd.

-

Kaspersky Lab

-

AT&T Cybersecurity (LevelBlue)

IoT Security Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.46 Billion |

| Market Size by 2035 | USD 280.93 Billion |

| CAGR | CAGR of 22.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Network Security, Identity & Access Management, Device Authentication, Data Encryption, Intrusion Detection, Others) • By Deployment (Cloud, On-Premises, Hybrid) • By End User (Manufacturing, Healthcare, Energy & Utilities, Government, Retail, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cisco Systems, Inc., Palo Alto Networks, Inc., Fortinet, Inc., Check Point Software Technologies Ltd., IBM Corporation, Microsoft Corporation, Broadcom Inc. (Symantec), Trend Micro Incorporated, Honeywell International Inc., Schneider Electric SE, Thales Group, Nozomi Networks Inc., Claroty Ltd., Forescout Technologies, Inc., Armis Security Ltd., Zscaler, Inc., CrowdStrike Holdings, Inc., Sophos Ltd., Kaspersky Lab, and AT&T Cybersecurity (LevelBlue) |

Frequently Asked Questions

North America dominated the IoT Security Market in 2025 with approximately 35% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Network Security dominated the IoT Security Market in 2025.

Growth drivers include rapid IoT device proliferation, increasing cybersecurity regulations and compliance requirements, and rising ransomware and cyberattack risks targeting connected industrial and enterprise IoT environments.

The IoT Security Market was valued at USD 37.46 Billion in 2025.

The IoT Security Market is expected to grow at a CAGR of 22.40% from 2026 to 2035.

Get in Touch