Isopropyl Alcohol Market Report Scope & Overview:

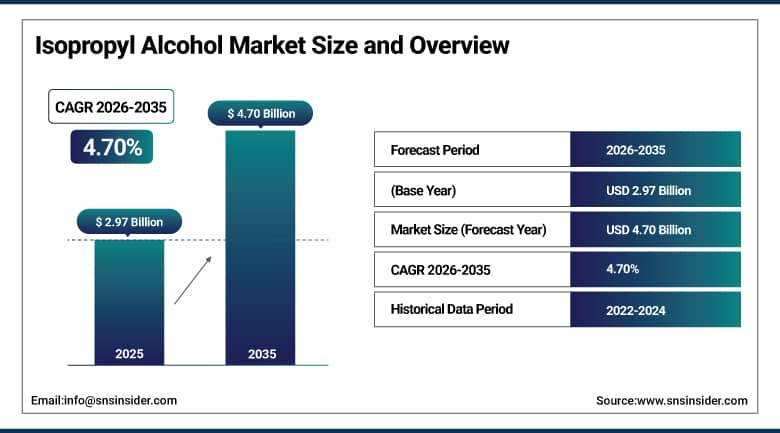

The Isopropyl Alcohol Market was valued at USD 2.97 Billion in 2025 and is expected to reach USD 4.70 Billion by 2035, growing at a CAGR of 4.70% from 2026 to 2035.

The Isopropyl Alcohol Market is growing steadily on account of high demand from the pharmaceutical industry, the healthcare sector, and even from industrial cleaning products. There has been increased demand due to its use as a disinfectant and antiseptic product in hospitals and laboratories, and hence, aiding the market's growth rate. Demand from the electronics sector for cleaning semiconductor components is another factor that has positively impacted demand. Furthermore, increasing demand from the cosmetics industry and even household cleaning products has been adding to demand.

Isopropyl alcohol consumption reached 2.1 million tons in 2025, driven by rising use in disinfectants, solvents, and cleaning applications across key industrial sectors.

According to the World Health Organization, Asia accounts for over 60% of the global infectious disease burden, driving strong consumption of disinfectants including IPA-based sanitizers across healthcare and public hygiene applications in the region.

Market Size and Forecast

-

Market Size in 2026E: USD 3.11 Billion

-

Market Size by 2035: USD 4.70 Billion

-

CAGR: 4.70% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Isopropyl Alcohol Market - Request Free Sample Report

Isopropyl Alcohol Market Trends

-

Rising demand for disinfectants, sanitizers, and cleaning agents is driving the isopropyl alcohol market.

-

Growing adoption across pharmaceuticals, healthcare, electronics, and cosmetics industries is boosting market growth.

-

Expansion of hygiene awareness and infection control practices is fueling product consumption.

-

Increasing use in industrial applications such as solvents, coatings, and chemical intermediates is shaping adoption trends.

-

Advancements in production efficiency and purification technologies are enhancing product quality and supply stability.

The U.S. Isopropyl Alcohol Market Outlook

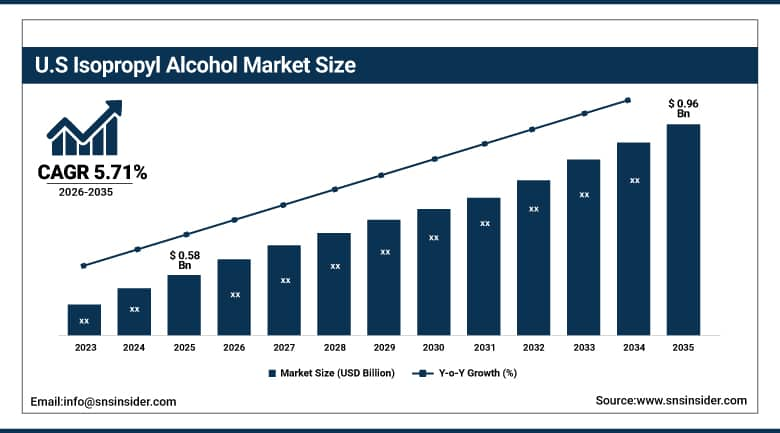

The U.S. Isopropyl Alcohol Market was valued at approximately USD 0.58 Billion in 2025 and is expected to reach approximately USD 0.96 Billion by 2035, growing at a CAGR of approximately 5.71%.

The United States is the world's largest pharmaceutical and electronics manufacturing economy and accordingly generates substantial IPA demand across both its healthcare and advanced manufacturing sectors. Domestic pharmaceutical manufacturers rely on IPA as both a process solvent in API synthesis and a validated cleaning agent for pharmaceutical equipment surfaces across GMP production environments. The CHIPS and Science Act has catalysed multi-billion dollar investments in domestic semiconductor fabrication facilities by Intel, TSMC, Samsung, and Micron whose operating requirements include significant ongoing consumption of electronic-grade IPA for wafer cleaning, photoresist stripping, and equipment maintenance.

The U.S. Food and Drug Administration enforces strict sterilisation and cleaning protocols in pharmaceutical and medical device manufacturing, where isopropyl alcohol is widely used. The U.S. CHIPS and Science Act (2022) allocates USD 52 billion to semiconductor expansion, boosting demand for ultra-high purity IPA in wafer cleaning processes.

Isopropyl Alcohol Market Segment Analysis

-

By Grade, Industrial Grade held the largest market share of 47.36% in 2025, while Pharmaceutical Grade is expected to grow at the fastest CAGR of 5.16% during 2026–2035.

-

By Production Process, Indirect Hydration dominated with a 58.67% share in 2025, while Direct Hydration is projected to expand at the fastest CAGR of 4.92% during the forecast period.

-

By Application, Solvent accounted for the highest market share of 35.82% in 2025, while Disinfectant is anticipated to record the fastest CAGR of 5.27% through 2026–2035.

-

By End Use Industry, Pharmaceuticals held the largest share of 32.41% in 2025, while Cosmetics & Personal Care is expected to grow at the fastest CAGR of 5.33% during 2026–2035.

By Grade, industrial grade segment dominates the market, pharmaceutical grade segment is the fastest growing

The Industrial Grade segment held the largest share in 2025 owing to its widespread utilization in chemical manufacturing, cleaning agents, and industrial processes. The high cost-effectiveness, availability, and suitability for commercial production make the Industrial Grade the top choice for various end-use sectors. In addition to this, a robust demand from manufacturing facilities, construction industry, and other industrial activities helped maintain dominance. Also, its usage as a base component for solvents and intermediates contributes towards its continued dominance in the market.

The Pharmaceutical Grade segment is the fastest growing due to the rising need for pure ingredients in drugs formulations, sterilization solutions, and healthcare applications. Increasing investments in healthcare around the world, growing pharmaceutical industry, and stringent requirements regarding purity of products are supporting the growth of this market segment. Moreover, this grade is increasingly used for injectables, antiseptic products, and other medicines. Growing biotechnology research and advanced pharmaceutical product manufacturing are further adding fuel to this growth.

By Production Process, indirect hydration process dominates the market, direct hydration process is the fastest growing

The Indirect Hydration process dominated the market in 2025 due to its successful industrial application, efficient work, and ability to provide stable production in large volumes. This technique is popular in commercial production due to its reliability and cost-effective operation mechanism. The integration into the chemical industry production system plays a significant role in its popularity. Moreover, the stability of the production results, as well as its ability to cope with bulk production needs, has contributed significantly to its popularity.

The Direct Hydration process is the fastest growing because of its high process efficiency, low energy expenses, and eco-friendly approach. The focus on new techniques and sustainability issues becomes the major reason for companies' interest in this technology. The companies are gradually introducing the direct hydration technique for increasing yield efficiency and reducing expenses. Also, the development of catalysts and process optimization techniques becomes the major driving factor of rapid development.

By Application, solvent segment accounts for the highest market share, disinfectant segment is the fastest growing

The Solvent segment accounted for the highest market share in 2025 owing to extensive usage in industrial cleaning, chemical synthesis, coatings, and formulation processes. High demand for solvents from manufacturing, pharmaceutical, and automotive industries played a major role in the segment's market domination. The segment finds wide application in dissolving, extracting, and processing chemical compounds, hence making it an important part of several applications. Moreover, constant expansion in the industry, together with demand from the end-users, helped in achieving dominance.

The Disinfectant segment is the fastest growing due to increasing consumer knowledge about hygiene, infection control, and sanitation in healthcare facilities, residential premises, and commercial establishments. Growing demand for hospital-grade disinfectants, sanitizers, and other related products is boosting the segment's growth rate. Consumer behavior following the pandemic outbreak, along with increased sanitation measures, has led to the rapid acceptance of the products.

By End Use Industry, pharmaceuticals segment dominates the market, cosmetics & personal care segment is the fastest growing

The Pharmaceuticals segment held the largest share in 2025 owing to increased consumption of chemical compounds in drugs, antiseptics, and health care applications. High demand for medicines, vaccines, and medical solutions along with rising production capabilities and quality standards is driving the segment towards dominance. Moreover, increase in the number of chronic disorders and investments in healthcare R&D are anticipated to bolster the market dominance of this segment.

The Cosmetics & Personal Care segment is the fastest growing due to increased consumer demands for hygiene, skincare, and beauty items. Rising incomes and shifting lifestyle preferences coupled with heightened personal grooming habits are leading to increased product consumption. Growing application of chemical compounds in the manufacture of skincare, hair care, and hygiene products are anticipated to fuel the growth of the segment. In addition, technological advancements in organic cosmetics are also aiding growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

46.28% |

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.63% |

|

Middle East & Africa |

Saudi Arabia |

22.84% |

|

Latin America |

Brazil |

43.72% |

Asia Pacific Isopropyl Alcohol Market Insights

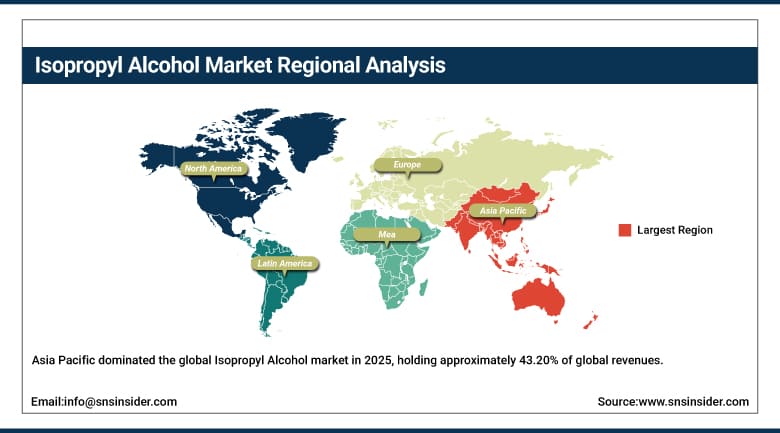

Asia Pacific dominated the global Isopropyl Alcohol market in 2025, holding approximately 43.20% of global revenues. China accounts for approximately 46.28% of Asia Pacific revenues as the world's largest IPA consumer across its massive pharmaceutical manufacturing, electronics production, paints and coatings, and personal care sectors. The country's domestic IPA production from Jilin Petrochemical, Shandong Dadi Chemical, and Zhejiang Xinhua Chemical serves both internal demand and regional export markets, though domestic consumption growth consistently outpaces production capacity expansion, sustaining import procurement from major Western and Japanese producers.

China’s National Bureau of Statistics reports pharmaceutical manufacturing output exceeding $500 billion annually, where isopropyl alcohol is widely used in formulation, purification, and sterilisation processes supporting large-scale drug production.

Electronics manufacturing across China, South Korea, Taiwan, and Japan accounts for over 70% of global semiconductor and component output, with IPA essential for precision cleaning in high-tech fabrication processes.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Isopropyl Alcohol Market Insights

North America is the fastest-growing regional Isopropyl Alcohol market, projected to expand at a CAGR of approximately 5.71% through 2035. The region's growth is powered by domestic semiconductor capacity expansion under CHIPS Act stimulus, sustained pharmaceutical manufacturing investment, and the permanent elevation of institutional disinfectant product consumption that post-pandemic healthcare protocols have established. The United States accounts for approximately 82.47% of North American revenues through its combination of large domestic production capacity and diversified end-use demand across multiple high-growth application sectors.

According to the U.S. Centers for Disease Control and Prevention, healthcare-associated infections affect about 1 in 31 hospital patients daily, driving continuous use of disinfectants including isopropyl alcohol. The U.S. Bureau of Labor Statistics reports over 1.5 million workers in pharmaceutical and chemical manufacturing, supporting strong industrial solvent demand.

Europe Isopropyl Alcohol Market Insights

Europe held approximately 17.84% of global Isopropyl Alcohol revenues in 2025. Germany, France, the United Kingdom, and the Netherlands are the primary national markets, each hosting pharmaceutical, chemical, cosmetics, and industrial manufacturing sectors with established IPA procurement programmes. The European pharmaceutical industry's strict pharmacopoeia compliance requirements sustain concentrated demand for pharmaceutical-grade IPA among certified-quality producers, creating a commercially insulated premium market within the broader European commodity IPA volume landscape that rewards suppliers with full GMP documentation and consistent analytical certification capabilities.

Cepsa announced construction of its first Spanish isopropyl alcohol chemical plant in June 2024, targeting 80,000 tonnes of annual production capacity for hydroalcoholic gel base supply to European personal hygiene and healthcare markets.

The European Centre for Disease Prevention and Control reports around 4.5 million healthcare-associated infection cases annually in Europe, driving strong demand for hospital-grade disinfectants including isopropyl alcohol across healthcare facilities and critical care environments.

The European Medicines Agency notes that Europe produces over 25% of global pharmaceutical output, where IPA is extensively used in drug manufacturing, equipment sterilisation, and cleanroom applications supporting strict regulatory compliance.

MEA & Latin America Isopropyl Alcohol Market Insights

Middle East and Latin America are growing IPA markets where expanding pharmaceutical manufacturing, healthcare infrastructure investment, and industrial sector development are creating new commercial demand. Saudi Arabia leads MEA revenues at approximately 22.84% of the regional total through its Vision 2030-aligned healthcare sector expansion and growing domestic pharmaceutical production ambitions supported by state investment programs. Brazil leads Latin American revenues at approximately 43.72% of the regional total through its large pharmaceutical manufacturing base, significant cosmetics and personal care manufacturing industry, and diversified industrial sector whose combined IPA consumption makes it the most commercially significant Latin American market by revenue.

According to the World Health Organization, infectious diseases remain a major health burden across Africa, with hospital hygiene compliance driving strong demand for disinfectants and infection-control solutions, including alcohol-based products used to improve sanitation standards in healthcare facilities across the African region WHO.

Ministry of Health reports rising healthcare facility expansion under Vision 2030, with hospital capacity growth exceeding 50 percent expansion targets in major urban regions supporting increased demand for clinical infrastructure, sterilisation systems, and medical service delivery enhancement across facilities.

Market Dynamics

Growth Drivers: Expanding pharma, electronics manufacturing, and hygiene investments driving sustained isopropyl alcohol demand growth globally.

The Isopropyl Alcohol market's durable growth is anchored by the structural expansion of two industries whose IPA consumption requirements are both large and largely non-substitutable. Global pharmaceutical manufacturing output is projected to grow at approximately 6% annually through 2035, driven by the biosimilar wave, ageing population demographics across developed economies, and the progressive healthcare system development of emerging markets whose growing insured populations are accessing pharmaceutical treatment at increasing rates. Global pharmaceutical manufacturing capacity is expanding at sustained rates as biosimilar development, generic drug pipeline growth, and vaccine manufacturing investment collectively drive production facility buildouts across Asia, Europe, and North America.

Isopropyl alcohol sales grew 5.2% in 2025, fueled by rising sanitizer production and increasing demand from pharmaceutical and electronics manufacturing industries.

Restraints: Propylene price volatility and strict environmental regulations increasing production costs and compliance pressures.

IPA production economics are directly linked to propylene prices, whose volatility reflects crude oil market dynamics, petrochemical industry operating rates, seasonal demand patterns, and competing propylene demand from polypropylene, acrylonitrile, acrylic acid, and other high-volume derivative markets that compete for the same steam cracker and refinery off-gas propylene feedstock base. Producers operating under long-term propylene supply agreements with integrated refinery or cracker partners have structurally superior feedstock cost stability relative to those purchasing propylene on spot markets, creating a two-tier competitive dynamic where feedstock-integrated producers can sustain profitability through commodity price cycles that margin-compress smaller buyers of open-market propylene.

Opportunities: Semiconductor demand and bio-based production innovations creating high-value growth opportunities in IPA market.

The commercial opportunity in electronic-grade IPA is technically and commercially distinct from commodity IPA markets. Semiconductor-grade IPA specifications require metallic impurity levels measured in parts per trillion, particle counts below defined thresholds per millilitre, and documentation packages that trace every step of the production, packaging, and distribution chain under cleanroom conditions. These specifications create a premium market segment whose supply qualification barriers are high and whose customer relationships, once established, are durable. Suppliers qualified for electronic-grade IPA supply to leading semiconductor manufacturers benefit from strong customer retention and above-commodity pricing that reflects the value of supply chain security and specification compliance in an application where contaminant-related yield loss carries extraordinary financial consequence for the semiconductor manufacturer.

Recent Developments:

-

2025: Dow showcased its Decarbia low-carbon isopropyl alcohol range at NYSCC Suppliers Day, establishing a commercially differentiated product tier for pharmaceutical and personal care customers whose sustainability commitments require reduced-carbon-intensity raw material sourcing documentation within their scope 3 emissions reporting frameworks.

-

2024: Eastman introduced its EastaPure high-purity electronic-grade IPA product as an expansion of its specialty electronic solvent portfolio, targeting semiconductor and advanced electronics manufacturing customers requiring certified ultra-high-purity IPA with comprehensive trace metallic and particle count certification.

-

2024: Cepsa commenced construction of an 80,000-tonne capacity IPA production facility in Spain, targeting European disinfectant, pharmaceutical, and personal care markets and positioning the company to serve growing regional IPA demand driven by pharmaceutical manufacturing expansion and sustained healthcare hygiene product consumption.

Isopropyl Alcohol Market Key Players are:

-

Exxon Mobil Corporation

-

The Dow Chemical Company

-

Royal Dutch Shell plc

-

INEOS Group Holdings S.A.

-

LG Chem Ltd.

-

Mitsui Chemicals, Inc.

-

Tokuyama Corporation

-

BASF SE

-

Sasol Limited

-

LCY Chemical Corp.

-

Eastman Chemical Company

-

ISU Chemical Co., Ltd.

-

Deepak Nitrite Limited

-

Zhejiang Xinhua Chemical Co., Ltd.

-

Sinopec Corp.

-

Suzhou Upline Chemicals Co., Ltd.

-

Jiangsu Denoir Technology Co., Ltd.

-

Kellin Chemical

Isopropyl Alcohol Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.97 Billion |

| Market Size by 2035 | USD 4.70 Billion |

| CAGR | CAGR of 4.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Industrial Grade, Pharmaceutical Grade, Electronic Grade) • By Production Process (Indirect Hydration, Direct Hydration) • By Application (Solvent, Disinfectant, Cleaning Agent, Coating & Paints, Chemical Intermediate, Others) • By End Use Industry (Pharmaceuticals, Chemicals, Cosmetics & Personal Care, Food & Beverages, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Exxon Mobil Corporation, The Dow Chemical Company, Royal Dutch Shell plc, LyondellBasell Industries N.V., INEOS Group Holdings S.A., LG Chem Ltd., Mitsui Chemicals, Inc., Tokuyama Corporation, BASF SE, Sasol Limited, LCY Chemical Corp., Eastman Chemical Company, Ecolab Inc., ISU Chemical Co., Ltd., Deepak Nitrite Limited, Zhejiang Xinhua Chemical Co., Ltd., Sinopec Corp., Suzhou Upline Chemicals Co., Ltd., Jiangsu Denoir Technology Co., Ltd., Kellin Chemical. |

Frequently Asked Questions

Asia Pacific dominated the Isopropyl Alcohol Market in 2025, holding approximately 43.20% of global revenues, with China accounting for approximately 46.28% of Asia Pacific revenues.

The industrial grade segment dominated the Isopropyl Alcohol Market with 47.36% share in 2025.

Expanding pharma and electronics manufacturing, hygiene awareness, and semiconductor growth driving strong isopropyl alcohol market demand globally.

The Isopropyl Alcohol Market was valued at USD 2.97 Billion in 2025.

The Isopropyl Alcohol Market is expected to grow at a CAGR of 4.70% from 2026 to 2035.

Get in Touch