K-12 Testing and Assessment Market Report Scope & Overview:

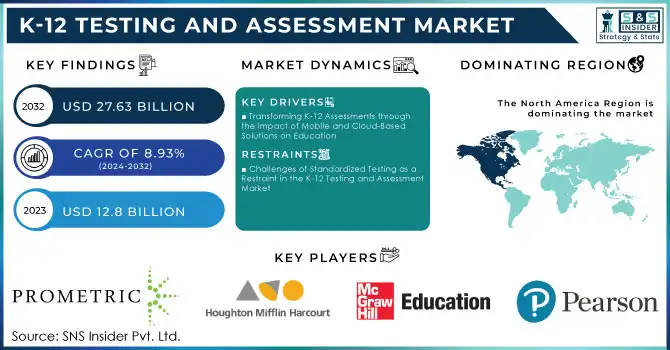

The K-12 Testing and Assessment Market Size was valued at USD 12.7 Billion in 2023. It is expected to grow to USD 26.9 Billion by 2032 and grow at a CAGR of 8.7% over the forecast period of 2024-2032. The rise of gamification in the K -12 testing and assessment market is revolutionizing traditional evaluation methods by incorporating game-based elements to enhance student engagement and motivation. Gamified assessments leverage interactive elements like gifts, missions, leaderboards, and avatars to make the assessment process enjoyable and immersive. Not only does this help alleviate the exam stress that many students may feel, it also inspires student engagement, particularly with younger primary students. Gamification plays an important role and helps in keeping the students focused, by converting the assessments into an entertaining task that also facilitates retention of knowledge. Additionally, gamified testing is also in line with the current trend of providing more experience-based learning, which will help make the assessment process much more activity-based and responsive to individual learning requirements.

Get more information on K-12 Testing and Assessment Market - Request Free Sample Report

A key government initiative supporting this trend is the U.S. Department of Education’s National Education Technology Plan (NETP), which emphasizes integrating technology-driven and engaging pedagogical practices to transition students from passive to active learning.

New government initiatives have played an increasing role in developing educational scaffolding through digital learning tools that bring about a positive change in student performance. This movement has often been led by the U.S. Department of Education, emphasizing personalized and technology-driven education models through policies like the National Education Technology Plan (NETP). It supports the use of digital tools to build equitable learning environments for diverse student needs and learning styles.

Additionally, federal funding programs like Every Student Succeeds Act (ESSA) incentivize states to embrace new and innovative learning technologies as part of educational curricula so schools can provide the best high-quality, individualized education. ESSA, for example, includes a grant program to design adaptive learning systems that assess how each student is performing and modify the content available to that student to maximize educational progress. These initiatives reflect the government's determination to leverage technology to reduce disparities in mustering success by students in learning.

K-12 Testing and Assessment Market Dynamics

Drivers

-

The demand for assessment solutions that provide actionable insights and analytics is driven by the need for data-driven decision-making.

-

There is an emerging trend toward a greater reliance on interactive learning technologies that drive the market growth.

One of the major factors driving the growth of the K-12 Testing and Assessment Market is the increased dependence on interactive learning technologies. Interactive technologies (AI-based adaptive assessments, gamified testing platforms, and online tools) are changing the conventional classroom ecosystem to ensure learning and teaching experiences never cease being interesting and customized. This technology allows teachers to evaluate students in real-time, immediately providing customized feedback to help students learn better.

This trend is further amplified by government initiatives promoting digital transformation in education. Programs that have encouraged the use of digital tools in schools have fast-tracked the use of interactive technologies around the world. In the increasingly rigorous environment where schools and other educational institutions search for means to both ensure optimum student performance and keep in line with the drastic changes being integrated into pedagogy practices, such interactive technologies would be amongst the most powerful tools for their arsenal. They cater to different learning needs, support remote and hybrid learning, and allow for broad-scale assessment through scalability. Not only does this tech transition facilitate more interactive assessments, but also urges market impetus towards offering innovative assessment and testing solutions in the K-12 space.

Restraint

The lack of immersive learning environments and engagement programs hamper the market growth.

The absence of immersive learning environments and engagement programs is hampering the growth of the K-12 testing and assessment market. Virtual Reality Simulations: Virtual reality (VR) simulations or interactive platforms that act as immersive learning environments are critical to touch or develop a deeper level of student engagement and understanding. Nonetheless, lots of schools especially in underfunded or resource-poor areas are not equipped with the facilities, funding help, and technical expertise to apply this advanced equipment effectively. The lack of relevant engagement programs that go hand-in-hand with the assessment and testing tools further minimizes their impact as students lose interest, and educators cannot capitalize on the potential of technology. This gap not only constrains effective assessment of innovative solutions but also restricts their potential market slowing down the large-scale adoption process.

Opportunities

-

There are abundant opportunities in emerging sectors such as healthcare, edge computing, automotive electronics, and industrial IoT.

-

The emergence of new applications, such as autonomous vehicles, smart grids, and medical implants, has revolutionized various industries.

-

Advancements in processor technology have played a crucial role in driving these technological developments.

K-12 Testing and Assessment Market Segmentation

By Types

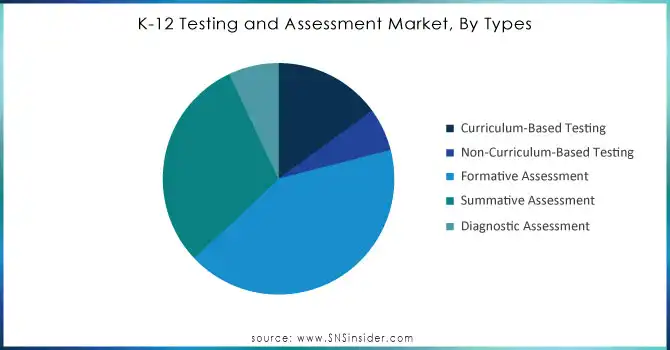

Curriculum-based testing held the largest market share around 32% in 2023. The reason for this is mostly that it directly fits with the educational standards and learning targets. The key aspect of curriculum-based tests is that these tests are intended to measure a student's understanding and progress against the prescribed or suggested curriculum, thereby making it the most basic contribution towards the education process. Additionally, both formative and summative assessments primarily rely on curriculum-based testing, which plays a significant role in maintaining its market share. Curriculum-based testing still holds the biggest market share due to its integral position in standardized testing systems and its insertion into the majority of normalized curricula worldwide.

By Component

The software held the largest market share around 48% in 2023. Its dominance is fuelled by the growing application of digital assessment tools and platforms offering scalable, effective and interactive solutions for teachers as well as learners. Using software to solve this problem, Tech Grader: AI assessment, LMS, and digital test help to automate grading, track real-time performance, and provide personalized feedback, which dramatically improves the assessment process. They are great for offering flexibility, seamless with curriculum-based content, and meeting diverse learning requirements, making them indispensable to modern educational systems. Consequently, software still rules the roost, beating hardware, content, and even services as the share-gainer of choice.

By End-User

The schools held the largest market share around 30% in 2023. Standardized tests, formative assessments, and summative subjects are primarily administered in schools, especially at the primary and secondary levels. Because they are responsible for student outcomes and academic progress, these stakeholders are among the earliest adopters of tools for testing and assessment. While schools have long been the primary consumers of assessment tools due to their reliance on digital learning platforms, their increased usage and what some experts claim is an undue emphasis comes as nations around the world make it mandatory to use standardized testing. It is schools again that play a major option in implementing syllabus-focused assessment in the country harnessed by the national curriculum integrated syllabus. Moreover, government funding initiatives and educational grants promoting improved student performance are often routed through school systems leading to increased demand for advanced testing solutions.

K-12 Testing and Assessment Market Regional Overview

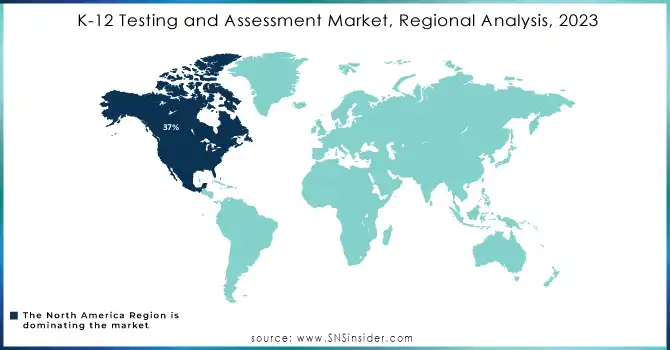

The North America region held the largest revenue share. During the projected period, it is predicted that North America will contribute 46% to the growth of the worldwide market. In North America, an e-learning model with online testing and assessment options for grades K–12 is widely used since it is regarded as a learning process and a platform through which students may make use of new technology and receive immediate feedback on their academic performances. Students mostly employ technological resources in the US, Canada, and Mexico to learn in and explore a virtual learning environment. The major growth factor for North America that dominated the global K-12 testing and assessment is the increasing number of government initiatives to improve the quality of education and the overall development of students. These have encouraged many schools to incorporate testing and assessment tools into the curriculum. As a result, many school districts are entering into a collaboration with testing and assessment tool vendors to opt for efficient testing and assessments. ETS has entered into a collaboration with the district of California to develop and administer an array of state-wide assessments for public schools in the district.

In the Asia-Pacific region mostly East Asia like China, Japan, and South Korea these nations have strict examination systems, which is fueling the demand for assessment materials and test preparation resources. These nations in Southeast Asia, Singapore, Malaysia, Thailand, and Indonesia have standardized tests in place to monitor student progress and university admissions. Assessment tools, online resources, and tutoring services are all part of the industry. South Asia, India, Pakistan, and Bangladesh These nations have various educational systems with local, national, and international exams. The market provides resources for preparation, digital platforms, coaching services, and evaluation materials.

Need any customization research on K-12 Testing and Assessment Market - Enquiry Now

Key Players in K-12 Testing and Assessment Market

-

Anthology Inc. (Blackboard Learn, Ally)

-

Batia Infotech (EduExam, EduAssessment)

-

CogniFit Inc. (Cognifit Assessments, MindBoost)

-

Coursera Inc. (Coursera for Campus, Coursera for Educators)

-

D2L Corp. (Brightspace, ePortfolio)

-

Edutech (Edutech Assessment Suite, EduPlatform)

-

ExamSoft Worldwide LLC (ExamSoft, Examplify)

-

FairTest (FairTest Resources, Test-Optional Advocacy)

-

Houghton Mifflin Harcourt Co. (Houghton Mifflin Harcourt Assessments, i-Ready)

-

Instructure Holdings Inc. (Canvas LMS, Canvas for K-12)

-

Pearson Education (Pearson eAssessment, SuccessMaker)

-

McGraw-Hill Education (ALEKS, Wonders)

-

ACT, Inc. (ACT Test, ACT Aspire)

-

College Board (SAT, Advanced Placement (AP) Program)

-

Riverside Insights (Voyager Sopris, i-Ready Diagnostic)

-

Kahoot! (Kahoot! Academy, Kahoot! for Schools)

-

Turnitin (Turnitin Feedback Studio, Turnitin Originality)

-

Google for Education (Google Classroom, Google Forms)

-

IBM (IBM Watson Education, IBM Cognitive Tutor)

-

McKinsey & Company (McKinsey Education Insights, McKinsey Learning Solutions)

Recent Development:

-

In 2024, Anthology Inc. launched Ally for Schools, a platform designed to enhance accessibility and inclusivity in learning. It integrates with existing Learning Management Systems (LMS) and provides teachers with tools to support diverse student needs, improving assessment processes.

-

In 2023, Batia Infotech released an upgraded version of its Edu Assessment platform in 2023, which now includes AI-driven analytics to offer deeper insights into student performance, helping educators better tailor their assessments to meet individual learning requirements.

-

In 2023, Coursera expanded its Coursera for Campus program in 2023 by adding more K-12 resources, enabling schools to access a broader range of interactive assessments and learning tools to enhance their curriculum.

| Report Attributes | Details |

|---|---|

|

Market Size in 2023 |

USD 12.7 Billion |

|

Market Size by 2032 |

USD 26.9 Billion |

|

CAGR |

CAGR of 8.7% From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Types (Curriculum-Based Testing, Non-Curriculum-Based Testing, Formative Assessment, Summative Assessment, Diagnostic Assessment) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Pearson Education, McGraw-Hill Education, Houghton Mifflin Harcourt, Prometric, ACT, Inc., College Board, NCS Pearson, Edmentum, Pearson Clinical Assessment, Cambridge Assessment, Scantron Inc., CTB/McGraw-Hill, MeritTrac Services Pvt Ltd., Knewton, CogniFit Ltd., Cognia, Riverside Insights, Learning A-Z, Edulastic, ETS Global BV, and Instructure are key players in the K-12 Testing and Assessment Market. |

|

Key Drivers |

• Transforming K-12 Assessments through the Impact of Mobile and Cloud-Based Solutions on Education |

|

Restraints |

• Challenges of Standardized Testing as a Restraint in the K-12 Testing and Assessment Market |

Frequently Asked Questions

Use of Formative assessments to track students' progress and give continuing feedback to teachers is the major steps taken by the companies, so they may improve education.

By Application, By Types, By End-User, and By Component are the major segments in the K-12 Testing and Assessment Market.

The use of advanced learning analytics, competency-based assessments, and the growing adoption of digital assessments are the key trends in the K-12 Testing and Assessment market.

The K-12 Testing and Assessment Market size was valued at USD 12.7 Billion in 2023.

The K-12 Testing and Assessment Market is growing at a CAGR of 7.8% Over the Forecast Period 2024-2032.

Get in Touch