Laser Cleaning Market Report Scope & Overview:

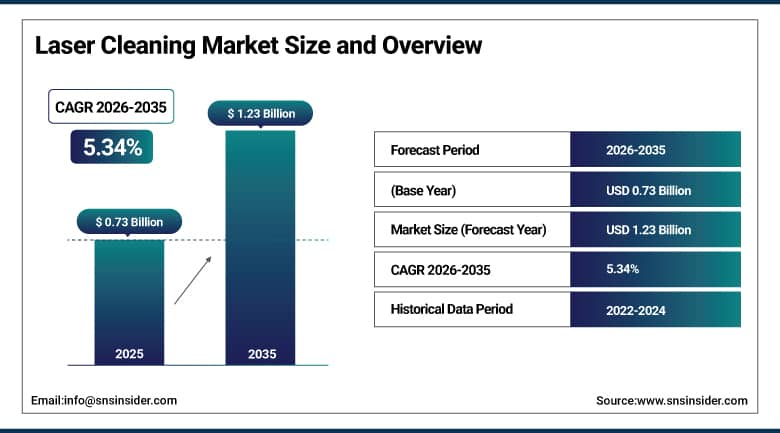

Laser Cleaning Market was valued at USD 0.73 billion in 2025 and is expected to reach USD 1.23 billion by 2035, growing at a CAGR of 5.34% from 2026-2035.

Laser cleaning is the surface treatment process that directs high-intensity laser pulses at substrate surfaces to selectively remove contaminants rust, oxides, paint, oil, coatings, and particulate deposits through the photothermal and photomechanical interactions that ablate contaminant material without damaging the underlying substrate. The commercial case for laser cleaning over conventional cleaning methods abrasive blasting, chemical stripping, ultrasonic cleaning rests on three mutually reinforcing advantages precision, because laser spot size and pulse energy can be calibrated to remove contaminant layers of specific thickness without touching underlying material, environmental cleanliness, because laser cleaning generates no chemical waste, no abrasive media disposal, and no contaminated wastewater requiring treatment; and operator safety, because workers are not exposed to the silica dust, chemical solvents, and heavy metal particles that conventional cleaning generates. These advantages are commercially decisive in applications where substrate surface integrity is critical aerospace component depainting before non-destructive inspection, electronics PCB preparation, and art conservation and increasingly competitive in volume industrial applications including automotive component rust removal, marine hull cleaning, and railway infrastructure maintenance. Adoption expansion as laser cleaning system costs declines with fiber laser technology maturation and as environmental regulations tighten the compliance cost of chemical cleaning alternatives.

The U.S. Environmental Protection Agency's National Emission Standards for Hazardous Air Pollutants for surface coating operations create air quality compliance costs for solvent-based cleaning whose regulatory burden sustains laser cleaning adoption in the aerospace and automotive manufacturing industries whose cleaning volumes make compliance investment economically significant. The International Council of Museums' conservation standards increasingly favor laser cleaning for historical artifact and architectural stone restoration where the technology's non-contact, controllable nature preserves original surface material at precision levels that mechanical and chemical cleaning cannot achieve.

Laser Cleaning Market Size and Forecast

- Market Size in 2025: USD 0.73 Billion

- Market Size by 2035: USD 1.23 Billion

- CAGR: 5.34% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026-2035

- Historical Data: 2022-2024

To Get More Information On Laser Cleaning Market - Request Free Sample Report

Laser Cleaning Market Trends

- Fiber laser system cost reduction where 1-10 kW fiber laser sources have declined 60% in price since the category's commercial introduction is making laser cleaning economically competitive with abrasive blasting in high-volume industrial applications that previously justified only premium precision cleaning scenarios.

- Robotic laser cleaning integration where laser cleaning heads are mounted on collaborative or industrial robotic arms programmed for autonomous surface treatment is enabling consistent, high-throughput laser cleaning without operator fatigue variation.

- Portable hand-held laser cleaning systems compact units under 20 kg enabling field cleaning of in-situ infrastructure including pipelines, bridges, and offshore equipment are expanding the addressable market beyond controlled manufacturing environments.

- AI-powered laser parameter optimization where machine learning models adjust pulse frequency, power, and scan speed in real time based on surface condition sensing is improving cleaning efficiency and reducing substrate damage risk in variable-condition industrial environments.

- Cultural heritage preservation adoption where laser cleaning is becoming the standard method for stone cleaning at UNESCO World Heritage sites, monument restoration, and museum artifact conservation is growing with international cultural preservation program funding.

- Additive manufacturing surface preparation using laser cleaning before and after 3D metal printing removing oxidation and residual powder from printed surfaces is creating a new aerospace and medical device manufacturing application segment.

- Green shipping regulations driving hull coating removal adoption where IMO sulfur regulations are accelerating ship recoating that requires complete existing coating removal are creating maritime laser cleaning demand from shipyards seeking chemical stripping alternatives.

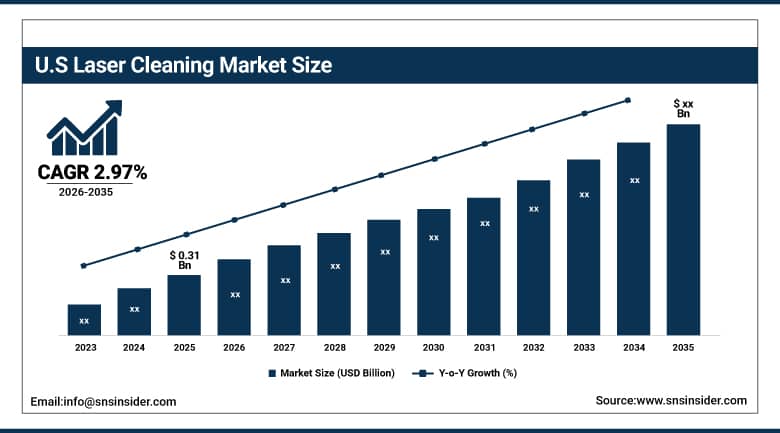

U.S. Laser Cleaning Market was valued at approximately USD 0.31 billion in 2025 and is expected to grow at a CAGR of 2.97% from 2026-2035.

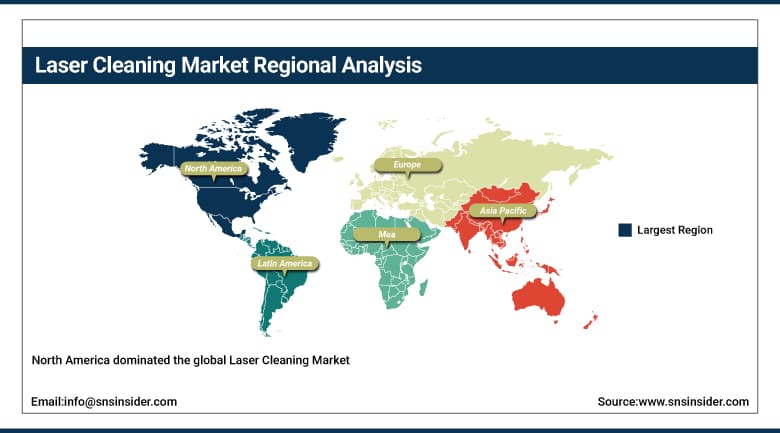

North America dominated the global Laser Cleaning Market in 2025, driven by the United States' combination of the world's most active aerospace manufacturing sector whose strict surface preparation standards before bonding, coating, and non-destructive inspection create systematic laser cleaning demand and the large defense contractor community whose security-sensitive manufacturing environments prefer laser cleaning's zero-chemical-waste approach. The U.S. aerospace sector's laser cleaning adoption reflects Boeing's, Lockheed Martin's, and Northrop Grumman's documented use of laser cleaning for aircraft skin depainting before non-destructive testing where the precision of laser material removal enables inspection of areas whose paint thickness previously compromised ultrasonic testing sensitivity. The automotive sector's adoption of laser cleaning for pre-weld surface preparation, battery housing cleaning in EV manufacturing, and aluminum casting cleaning is creating a growing industrial laser cleaning market adjacent to the precision aerospace segment.

The U.S. Air Force's SBIR program has funded laser cleaning system development specifically for aircraft depot maintenance targeting the replacement of chemical stripping at depots where chemical waste generation and disposal creates operational cost and environmental compliance burden. The Department of Defense's directive to reduce hazardous material use at military facilities which identifies chemical paint strippers as priority reduction targets sustains defense contractor investment in laser cleaning alternatives at manufacturing and maintenance facilities.

Laser Cleaning Market Segment Analysis

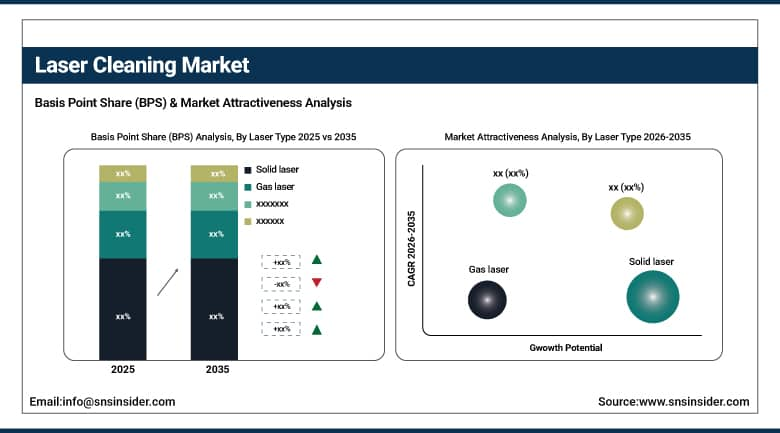

- By Laser Type, Solid Laser dominated with the largest share in 2025; Gas Laser growing at the fastest CAGR.

- By Power Range, Medium Power Laser dominated with the largest share in 2025; High Power Laser growing at the fastest CAGR.

- By Application, Cleaning Process dominated with the largest share in 2025; Conservation and Restoration growing at the fastest CAGR.

- By End-user Industry, Industrial dominated with the largest share in 2025; Aerospace and Aircraft growing at the fastest CAGR.

By Laser Type: Solid Laser dominates, Fiber Laser growing fastest

Solid Laser systems accounted for the dominant type of laser in the Laser Cleaning Market in 2025, and these are commonly employed in various industrial cleaning, rust removal, paint stripping and surface preparation applications where high beam stability, effective cleaning and minimal damage to substrate is needed. Ideal for automotive, aerospace, electronics and manufacturing whether for efficient contaminant removal across metals, composites or sensitive surfaces while maintaining operational reliability and energy-efficiency are the main drivers of these laser systems. The compatibility of these systems with automated manufacturing technologies and their ability to provide precisely controlled cleaning processes further reinforced its market dominance in large-scale industrial uses.

The fastest growing segment is Gas Laser systems which are witnessing explosive demand for multi-area surface treatment at high speeds and significantly larger areas through light-encoding via fiber laser that offers consistent, continuous and high power laser delivery in heavy industry applications. Rising efficiency of gas lasers, increased operational lifespan and growing usage in cleaning of industrial equipment, infrastructure restoration & aerospace maintenance are supplementing rapid market growth. This is in addition to the rising adoption of gas laser systems across the globe, which is further fuelled by growing investments in green and non-contact cleaning technologies.

By Power Range: Medium Power Laser dominant, High Power Laser fastest CAGR

Medium Power Laser systems emerged as the dominant technology across power range in 2025. These systems are commonly utilized for rust removal, coating stripping, surface preparation and maintenance operations requiring a moderate level of power output that will provide good cleaning performance but not damage heat sensitive substrates. Easy suitability in automated manufacturing environments and wide applicability across automotive, machinery and metal processing industry further strengthened segment growth.

Based on power type, high Power Laser systems are estimated to register the highest CAGR due to increasing demand for high-speed cleaning, large area surface conditioning and heavy industrial applications such as deeper material removal and higher operational throughput.

By Application: Cleaning Process dominant, Conservation and Restoration fastest CAGR

Based on application, this market has been segmented into cleaning process (which is expected to retain its dominant position in the Laser Cleaning Market during the forecast period), paint removal, rust removal, and others; laser cleaning systems have extensive applications across industries due to their non-hazardous nature as they help in replacing chemical, abrasive, and manual cleaning methods with eco-friendly laser-based technologies that enhance precision of processing and automation capability while also improving workplace safety. The laser cleaning systems are also widely used in the industrial maintenance, manufacturing, and surface treatment markets due to their efficient and non-contact cleaning process with considerably less waste produced.

Conservation and Restoration applications are anticipated to have the highest due its rapidly increasing uptake across laser cleaning systems in historical monuments, cultural heritage structures, artworks and other sensitive surfaces where fine contaminant removal without substrate damage is critical.

By End-user Industry: Industrial dominant, Aerospace and Aircraft fastest CAGR

The Industrial segment was the largest end-user industry in the Laser Cleaning Market in 2025 due to increasing demand for laser cleaning systems, especially in manufacturing plants and facilities, machinery maintenance, metal fabrication and automated production lines involving precise cleaning where operational efficiency is paramount. Since the maintenance cost is lower with lasers, they have been rapidly adopted by industrial users.

By Industry Aerospace & Aircraft is the fastest-growing segment, attributed to the rising needs for precision surface treatments, coating removals, corrosion clearings and maintenance of high-cost aircraft components where damage-free and highly controlled cleaning technologies have been essential to comply with strict safety as well as performance standards.

Laser Cleaning Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

48% |

North America Laser Cleaning Market Insights

North America dominated the global Laser Cleaning Market, driven by U.S. aerospace and defense sector adoption and the growing industrial manufacturing segment. U.S. laser cleaning system vendors including Clean Laser Systems and Laser Power Technologies compete with European and Asian suppliers in the domestic aerospace and manufacturing markets.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Laser Cleaning Market Insights

Europe's Laser Cleaning Market is growing with Germany's automotive manufacturing sector adoption where laser cleaning for pre-weld surface preparation and aluminum component cleaning is growing in BMW, Mercedes-Benz, and Audi manufacturing programs and the EU's exceptional cultural heritage inventory whose preservation programs sustain consistent laser cleaning procurement across historical monument, church, and museum stone conservation projects. The European Cultural Heritage Strategy's funding programs and EU Horizon grants for conservation technology specifically sustain laser cleaning adoption in Europe's unmatched cultural heritage preservation market.

Asia Pacific Laser Cleaning Market Insights

Asia Pacific is the fastest-growing regional Laser Cleaning Market, driven by China's rapidly growing manufacturing base whose electronics, automotive, and semiconductor industries create laser cleaning demand for precision surface preparation applications. China's domestic laser technology industry including IPG Photonics' China operations, Raycus Fiber Laser, and JPT Opto-electronics is developing competitive laser cleaning systems at pricing that accelerates domestic industrial adoption beyond what imported systems could achieve at equivalent market penetration.

MEA and Latin America Laser Cleaning Market Insights

The Middle East's Laser Cleaning Market is growing with oil and gas infrastructure maintenance where pipeline and process equipment corrosion removal using laser cleaning avoids the chemical waste challenges of conventional cleaning in environmentally sensitive desert and marine environments and cultural heritage restoration across the region's significant archaeological sites. Latin America's market concentrates in Brazil's aerospace maintenance sector and manufacturing industry.

Laser Cleaning Market Growth Drivers:

- Environmental regulations and precision manufacturing demand driving sustained laser cleaning market growth globally

The Laser is driven by the dual pressure of tightening environmental regulations on chemical cleaning processes and the growing precision requirements of advanced manufacturing whose surface preparation standards conventional cleaning methods cannot consistently meet. The elimination of hazardous chemical cleaning solvents from manufacturing processes driven by REACH regulations in Europe, EPA NESHAP in the U.S., and national industrial chemical regulations globally creates conversion motivation that strengthens as regulatory enforcement tightens. Additive manufacturing's growing role in aerospace and medical device production creates new surface cleaning requirements between print layers, after support removal, and before coating that laser cleaning's precision and cleanliness advantages address more effectively than conventional alternatives.

Laser Cleaning Market Restraints:

- High initial system costs and operator safety requirements creating laser cleaning market adoption challenges globally

The primary adoption barrier for laser cleaning is initial system capital cost where a complete industrial laser cleaning installation including laser source, beam delivery, safety enclosure, exhaust system, and robotic integration costs USD 100,000-500,000 that creates payback period calculations whose justification requires either high cleaning volume or premium cleaning quality requirements that alternatives cannot match. Operator safety requirements for Class 4 laser systems interlocked enclosures, laser safety officer designations, annual training, and PPE compliance create ongoing operational overhead that smaller manufacturers find burdensome relative to the chemical cleaning status quo.

Laser Cleaning Market Opportunities:

- Maritime hull cleaning and EV battery manufacturing applications creating significant laser cleaning market growth opportunities globally

Maritime hull cleaning represents the laser cleaning market's largest near-term volume growth opportunity where the global commercial fleet's requirement for periodic hull paint removal before recoating creates a cleaning market whose scale is measured in millions of square meters annually. IMO's strict regulations on dry-dock biocide-containing paint waste disposal and the global shipbuilding industry's sustainability commitments are creating investment in laser cleaning as the zero-waste, zero-chemical alternative to abrasive blasting whose scale economics improve with each fiber laser system cost reduction. Electric vehicle battery manufacturing creates a growing laser cleaning demand for cell electrode cleaning, current collector surface preparation, and battery module assembly surface treatment.

Recent Developments:

- 2026: Coherent Corp. launched its CleanBurst Ultra pulsed fiber laser cleaning system — achieving 500W average power in a portable 35 kg industrial cabinet format with AI-assisted parameter auto-calibration demonstrating rust removal from structural steel at 12 m²/hour throughput while maintaining base metal surface integrity, qualifying for AWS D1.1 structural welding code pre-weld surface preparation specifications that establish the system's suitability for civil infrastructure applications including bridge rehabilitation and offshore platform maintenance.

- 2025: Laserax received Airbus Qualified Product List approval for its LXQ 1000 laser cleaning system for aluminum aircraft fuselage panel depainting the first laser cleaning system approved for use on Airbus A320 family fuselage skin surfaces enabling airline maintenance facilities to replace chemical stripping with laser depainting in airframe heavy maintenance visits, with Airbus documenting 60% reduction in hangar chemical waste generation at two early-adopter MRO facilities using the Laserax system for panel preparation.

- 2025: Trumpf GmbH launched the TruLaser Clean 1000 integrating a 1 kW single-mode fiber laser with robotic scan head and real-time surface monitoring camera enabling automated adaptive laser cleaning that adjusts power density in real time based on surface condition imaging, achieving consistent rust removal from automotive stamping dies at die repair facilities in Germany and Japan while preventing the substrate steel damage that manual laser cleaning parameter selection creates in variable corrosion thickness applications.

Laser Cleaning Market Key Players

Some of the Laser Cleaning Market Companies

- Coherent Corp. (formerly II-VI)

- Trumpf GmbH + Co. KG

- Han's Laser Technology Industry Group Co. Ltd.

- IPG Photonics Corporation

- Laserax Inc.

- Laser Power Technologies (LPT)

- Adapt Laser Systems LLC

- P-Laser NV

- Clean Laser Systems GmbH

- HGTECH Laser

- Bystronic AG

- Laser Photonics

- DIHORSE Technology Co. Ltd.

- Senfeng Laser

- Raycus Fiber Laser Technologies Co. Ltd.

- JPT Opto-Electronics Co. Ltd.

- 4JET Technologies GmbH

- Powerlase Ltd.

- Quanta System SpA

- National Laser Company LLC

Laser Cleaning Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.73 Billion |

| Market Size by 2035 | USD 1.23 Billion |

| CAGR | CAGR of 5.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Laser Type (Gas laser, Solid laser) • By Power Range (High, Medium, Low) • By Application(Conservation and Restoration, Cleaning Process, Industrial Usage) • By End-User Industry(Infrastructure, Automotive, Aerospace and Aircraft, Industrial, Other End-user Industries) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Coherent Corp., Trumpf GmbH + Co. KG, Han's Laser Technology Industry Group Co. Ltd., IPG Photonics Corporation, Laserax Inc., Laser Power Technologies, Adapt Laser Systems LLC, P-Laser NV, Clean Laser Systems GmbH, HGTECH Laser, Bystronic AG, Laser Photonics, DIHORSE Technology Co. Ltd., Senfeng Laser, Raycus Fiber Laser Technologies Co. Ltd., JPT Opto-Electronics Co. Ltd., 4JET Technologies GmbH, Powerlase Ltd., Quanta System SpA, and National Laser Company LLC |

Frequently Asked Questions

Aerospace & Defense, Manufacturing, Automotive, and Cultural Heritage Preservation are the primary applications.

The Laser Cleaning Market was valued at USD 0.73 billion in 2025.

North America dominated; Asia Pacific is the fastest growing.

Solid Laser dominated Gas Laser is growing at the fastest CAGR.

The Laser Cleaning Market is expected to grow at a CAGR of 5.34% from 2026 to 2035.

Get in Touch