Lyme Disease Testing Market Report Scope & Overview:

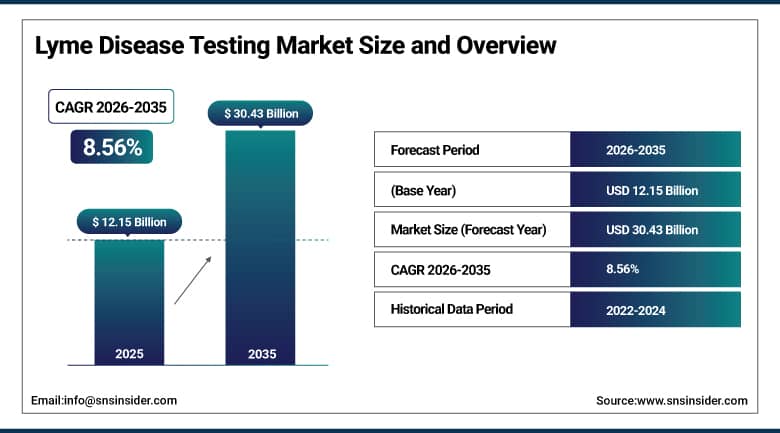

The Lyme Disease Testing Market was valued at USD 12.15 Billion in 2025 and is expected to reach USD 30.43 Billion by 2035, growing at a CAGR of 8.56% from 2026 to 2035.

The global Lyme disease diagnostic test market is currently enjoying strong and sustainable growth due to increasing prevalence of Lyme disease, increased awareness of the importance of early diagnosis, and developments in diagnostic tests that increase efficiency and accuracy of such tests. Caused by infection with spirochete bacteria Borrelia burgdorferi which is transmitted through bites from infected Ixodes ticks, Lyme disease is the leading vector-borne disease both in the United States and Europe. According to the statistics provided by the Center for Disease Control, approximately 476,000 Americans suffer from Lyme disease annually.

The market continues to grow due to an expansion of tick habitats resulting from changes in weather conditions and increasing the rate of infections in areas where such risks were initially perceived as small. Rising awareness about Lyme disease among physicians and patients exposed to Ixodes tick bites, increased financial support from governments, and replacement of traditional two-tier serological testing with more advanced and innovative approaches, such as multiplex ELISA, chemiluminescence immunoassays, and nucleic acid amplification tests, contribute greatly to this trend.

Market Size and Forecast:

-

Market Size in 2026E: USD 13.19 Billion

-

Market Size by 2035: USD 30.43 Billion

-

CAGR: 8.56% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Lyme Disease Testing Market - Request Free Sample Report

Lyme Disease Testing Market Trends:

-

Increasing adoption of modified two-tier testing (MTTT) for improved accuracy and faster results.

-

Growing development of point-of-care diagnostic tests enabling rapid, same-visit detection.

-

Rising use of multiplex panels to detect Lyme disease and other tick-borne co-infections simultaneously.

-

Integration of AI-assisted diagnostic interpretation to improve consistency and reduce errors.

-

Advancements in molecular and direct detection tests for earlier diagnosis before antibodies become detectable.

U.S. Lyme Disease Testing Market Outlook:

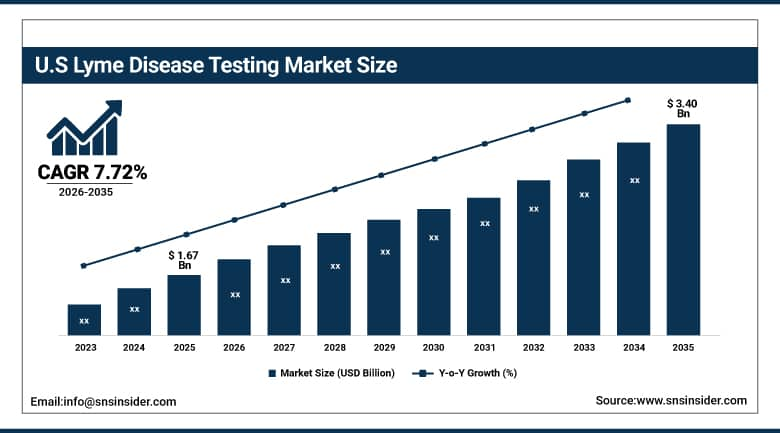

The U.S. Lyme Disease Testing Market was valued at approximately USD 1.67 Billion in 2025 and is expected to reach approximately USD 3.40 Billion by 2035, growing at a CAGR of approximately 7.72%.

The United States is without doubt the biggest market in the world for Lyme disease tests, owing to the massive burden of the disease within the country, whose roughly 476,000 cases each year account for the greatest Lyme disease testing volumes commercially. Quest Diagnostics, Laboratory Corporation of America Holdings, Mayo Clinic Laboratories, Bio-Rad Laboratories, Thermo Fisher Scientific, and Immunetics dominate the commercial arena in the Lyme disease test provision business in the country. It is worth noting that the two-tier testing strategy recommended by the CDC, Medicare/Medicaid reimbursement for the Lyme serological codes, and insurance cover for Borrelia antibody testing create organized reimbursement systems that support investment in commercial Lyme disease tests.

In August 2024, Siemens Healthineers introduced India's first AI-based multi-testing diagnostic analyser with integrated Lyme disease and other tick-borne illness detection capability, marking a significant step toward sustainable high-throughput automated infectious disease testing that improves clinical laboratory efficiency while reducing per-test operational cost across high-volume testing environments.

Lyme Disease Testing Market Segment Analysis:

-

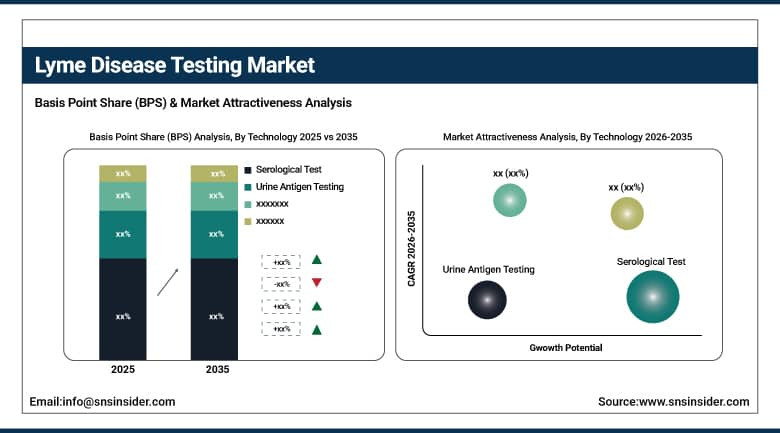

By Technology, the Serological Test segment dominated the lyme disease testing market with approximately 38.45% share in 2025, while the Nucleic Acid Test segment is the fastest growing as PCR-based and isothermal amplification methods that detect Borrelia DNA directly from clinical specimens address the critical sensitivity gap of serological testing during early infection when antibody titres remain below detectable thresholds.

-

By Sample Type, the Blood segment dominated the lyme disease testing market with approximately 61.52% share in 2025, while the CSF (Cerebrospinal Fluid) segment is the fastest growing.

-

By Patient Type, the Adult segment dominated the lyme disease testing market with approximately 58.46% share in 2025, while the Pediatric segment is the fastest growing as expanding clinical awareness of Lyme disease in children, growing paediatric Lyme disease incidence in expanding endemic regions.

-

By End Use, the Hospitals segment dominated the lyme disease testing market with the largest share in 2025, while the Diagnostic Laboratories segment is the fastest growing as expanding private laboratory networks, growing outpatient Lyme disease testing demand from primary care.

By Technology, serological test dominates, nucleic acid test grows fastest

Serology-based tests maintained their dominance among technology types with a share of around 38.45% of the Lyme disease testing market in 2025. This is due to their dominant presence in the commercial landscape, as they are supported by regulations and guidelines, such as the ones issued by the CDC, ECDC, and key infectious disease societies, making clinicians confident about their use and reimbursement possibilities. The specificity of two-tier testing algorithm is one of the main factors that makes serology-based tests preferred by the regulators and guideline committees despite their relatively lower sensitivity due to the use of ELISA screening and Western blot confirmation.

Nucleic acid tests are the fastest-growing technology type due to the clinical need that they satisfy. They are able to detect Borrelia burgdorferi DNA using PCR and thus resolve the issue of a two-week seronegative window for early infection, as serology-based tests cannot identify Lyme disease in this period because antibody response is still too low for an accurate result.

By Sample Type, blood dominates, CSF grows fastest

Blood samples remained the predominant form of testing sample, accounting for about 61.52% of the total Lyme disease testing market in 2025. The simplicity, efficiency, and convenience of venipuncture blood draws, as well as their standardization in processing for laboratory analysis, have laid the groundwork for a testing logistics strategy that centers the focus of clinical Lyme disease testing on blood serology and PCR tests. According to the Lyme disease testing recommendations provided by the CDC, serum ELISA is used in the first-tier of the two-tiered testing algorithm, followed by a second-tier western blot using either the initial or a new blood sample.

Cerebrospinal fluid remains the fastest-growing sample type due to the increasing awareness that Lyme neuroborreliosis is a significant manifestation of disseminated Borrelia infection that requires differential diagnosis through intrathecal antibody index testing in order to differentiate central nervous system infection from similar neurological symptoms. Every case of neurological Lyme disease in which there is diagnostic uncertainty regarding whether the case is Lyme neuroborreliosis or another neurological disease results in cerebrospinal fluid analysis.

By Patient Type, adults dominate, paediatric grows fastest

Adults continued to dominate the patient type category with an estimated share of 58.46% of the Lyme disease testing market in 2025. The high level of occupational and leisure outdoor activities in which adult patients engage in tick-infested areas including forestry workers, farmers, hikers, golfers, and gardeners whose likelihood of coming into contact with ticks’ results in the highest prevalence of Lyme disease is responsible for generating sufficient demand to maintain the segment’s supremacy. Adult presentations of Lyme disease's clinical presentation complexity, including the various stages such as erythema migrants, Lyme carditis, Lyme arthritis, and Lyme neuroborreliosis, maintains their above average testing value in comparison to paediatric presentations.

The rapid growth in this segment can be attributed to several factors, including the rise in Lyme disease awareness among children, increased endemic areas in suburban and peri-urban areas where tick exposure among school-age children occurs during outdoor activity, and increased parental concerns regarding tick-borne diseases among their children following media reports on Lyme disease cases in children.

By End Use, hospitals dominate, diagnostic laboratories grow fastest

Hospitals maintained their lead position as the dominant end-user in the Lyme disease testing market during 2025. Cases involving acute presentation of Lyme disease with Lyme carditis, nervous system involvement, or advanced Lyme arthritis that necessitates hospitalization contribute towards diagnostic testing which is conducted through hospital clinical microbiology laboratories. A hospitalization case of Lyme disease patient that requires extensive testing for Lyme disease that involves ELISA, Western Blot test, echocardiogram, and lumbar puncture represent diagnostic testing spending where the amount per individual far outweighs outpatient testing episode financial worth.

The fastest-growing end-user is diagnostic laboratories since much of the Lyme disease diagnosis that takes place in endemic areas entails testing done through outpatient investigation by primary care physicians, urgent care centers, and clinics specialized in infectious diseases where patients undergo testing through the facilities of major laboratories such as Quest Diagnostics, Labcorp, and other Lyme disease laboratories. An order received from a primary care physician for Lyme disease testing through the send-out testing agreement represents revenue for laboratories, and collectively, Lyme disease testing orders can amount to commercial value.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Lyme Disease Testing Market Insights

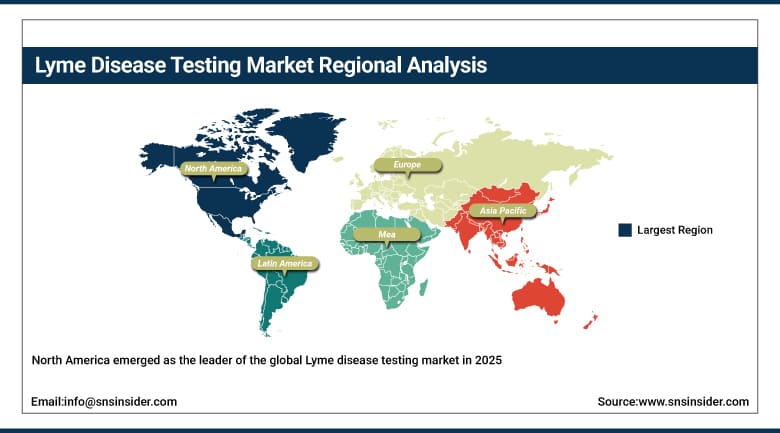

North America emerged as the leader of the global Lyme disease testing market in 2025 owing to the unprecedented domestic disease burden, where the approximate 476,000 cases reported annually in the US constitute the world's largest market for Lyme disease diagnostics. This market includes Quest Diagnostics, LabCorp, Mayo Clinic Laboratories, and Bio-Rad Laboratories' business revenue of nearly 87.4% from North America owing to the guidance provided by the CDC regarding testing and the reimbursement system in place.

Canada, on the other hand, is expected to contribute 12.6% of North American revenue owing to the increasing incidences of Lyme disease in Ontario, Quebec, and British Columbia where ticks have expanded their habitat range, just like in the northeast region of the US.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Lyme Disease Testing Market Insights

Europe represents an important testing market for Lyme disease in which Borrelia afzelii and Borrelia garinii co-inhabit with Borrelia burgdorferi among European Ixodes ricinus ticks, providing above-average diagnostic complexity when compared with the primarily B. burgdorferi infected United States market for Lyme diagnostics. Germany provides 22.3% of European revenues owing to its higher Lyme disease incidence in the states of Bavaria, Baden-Wurttemberg, and Thuringia, German Society for Infectious Diseases' Lyme testing protocols and laboratory infrastructure in the healthcare industry.

Austria, Switzerland, and the Czech Republic represent important secondary markets in Europe due to their high Ixodes ricinus tick population, outdoor recreational practices, resulting in exposure to ticks, and Lyme disease surveillance programs, respectively. The Lyme diagnostics product portfolio of both EUROIMMUN and DiaSorin serves as an example of commercial Lyme diagnostics assay suppliers in Europe.

Asia Pacific Lyme Disease Testing Market Insights

Asia Pacific is the leading regional Lyme disease testing market, fueled by increasing knowledge about infections caused by Borrelia burgdorferi sensu lato in China, Japan, South Korea, and Australia, where their ticks carry local Borrelia strains and have clinical manifestations similar to that observed in North America and Europe. China makes up around 44.8% of the revenue in Asia Pacific due to its investment in epidemiology research, serological testing capabilities in hospitals, and expansion of surveillance programs in ticks and related diseases in the region.

Commercially valuable secondary markets in Asia Pacific are Japan and South Korea, with increasing physician knowledge regarding Lyme-like borreliosis infections carried by local Ixodes ticks, public health laboratory tick-borne disease surveillance, and academic infectious disease research focused on Asian Borrelia strains.

MEA & Latin America Lyme Disease Testing Market Insights

South Africa is the leading revenue generator for MEA at an estimated 31.2% from its study on tick-borne relapsing fever and Borrelia, clinical and academic infectious disease laboratory test facilities, and physician recognition of differential diagnosis for tick-borne diseases. Brazil is the leading revenue generator for Latin America at an estimated 44.2% from its studies on Baggio-Yoshinari syndrome in cases showing characteristics of Lyme disease, academic research facilities for infectious diseases, and laboratory testing facilities.

Market Dynamics:

Growth Drivers: Rising Lyme disease incidence from climate change-driven tick habitat expansion and technological advancement improving diagnostic accuracy

Growing incidence of Lyme disease because of the expansion of tick habitats as a result of climate change is the market's leading structural factor that contributes to its growth. Warming in regions, which have experienced cold winters that restricted tick numbers, will help ticks colonize new geographical areas in the upper Midwest, Canada, and northeastern highlands in the US where Lyme disease transmission has been infrequent. Each county or region where the establishment of tick populations and the first human cases of Lyme are reported adds to an existing testing volume pool in a proportionate way.

Advances in testing accuracy will improve its clinical application and boost the value of Lyme testing in each episode. Multiplex next-generation platforms that replace the two-step testing algorithm with a highly sensitive and specific test for Lyme disease have been developed. New chemiluminescence immunoassay platforms offer automated analysis and process samples more quickly without compromising their analytical performance when compared with traditional ELISA. PCR-based tests offer a solution to the early seronegative issue.

Restraints: Diagnostic sensitivity limitations in early Lyme disease and lack of international diagnostic standardization

The lack of sensitivity of traditional two-tier serological tests in detecting early infections due to an inadequate immune response is problematic, as the most useful time window for an accurate diagnosis is precisely at this stage. Indeed, the high rates of false-negative results found by research studies (up to 50%) have contributed to a certain level of mistrust among physicians and patients regarding serological testing for Lyme disease. This mistrust is a source of further hesitation in terms of performing tests, which contributes to the progression of the infection to more serious forms.

An absence of international standardization regarding Lyme disease diagnostic tests is a significant impediment in the development of consistent procedures and standards for testing for Lyme disease around the world.

Opportunities: Point of care testing in endemic regions and next-generation molecular diagnostics

The creation of point of care Lyme disease tests presents the closest-term market growth opportunity available which allows for instant results without relying on laboratory infrastructures, meaning testing can take place in real-time while decisions are made, not after results arrive a few days later. The adoption of each physician practice, urgent care, and ED location offering point of care Lyme disease testing increases testing volume that will be generated above and beyond what existing laboratory testing workflows have produced by removing the failure rate in patient follow-up that hinders laboratory testing to initiate antibiotic therapy.

Next-generation diagnostics through molecular tests in early Lyme disease represents the greatest commercially valuable diagnostic innovation in terms of its capacity to identify Borrelia DNA directly within the seronegative window that existing Lyme testing technologies cannot accomplish. Each FDA-approved molecular Lyme disease diagnostic created will allow clinicians to use a premium-priced test that offers greater clinical utility over alternative serology tests in early Lyme disease patients that require the most urgent diagnostics possible.

Recent Developments:

-

2024: Siemens Healthineers introduced India's first AI-based multi-testing diagnostic analyser in August 2024 with integrated Lyme disease and tick-borne illness detection capability, advancing sustainable high-throughput automated infectious disease testing with AI-enhanced analytical performance.

-

2024: Roche Diagnostics expanded its Elecsys Lyme Disease testing portfolio in 2024 with enhanced second-generation chemiluminescence immunoassay reagents providing improved sensitivity for early Lyme disease serology on the cobas automated laboratory analyser platform.

-

2023: DiaSorin submitted LIAISON LymeDetect to the FDA in 2023, a next-generation chemiluminescence immunoassay designed to replace the conventional two-tier Lyme testing algorithm with a single fully automated assay on the LIAISON XL high-throughput analyser platform.

-

2023: Bio-Rad Laboratories launched enhanced BioPlex 2200 Lyme Disease profile assay updates in 2023 with improved antigen panel coverage providing simultaneous detection of multiple Borrelia burgdorferi protein antigens in a single multiplex immunoassay run, reducing turnaround time relative to sequential two-tier testing workflows.

-

2023: Immunetics launched a next-generation recombinant antigen Western blot kit in 2023 offering improved specificity and standardised result interpretation guidance for clinical laboratories seeking to reduce the subjective band pattern reading variability that characterises conventional Western blot interpretation in Lyme disease serodiagnosis.

Lyme Disease Testing Market Key Players:

-

Quest Diagnostics Incorporated

-

Laboratory Corporation of America (Labcorp)

-

Thermo Fisher Scientific Inc.

-

Bio-Rad Laboratories Inc.

-

DiaSorin SpA

-

Siemens Healthineers AG

-

Roche Diagnostics GmbH

-

Immunetics Inc.

-

EUROIMMUN AG

-

IDEXX Laboratories Inc.

-

Abbott Laboratories

-

Becton Dickinson and Company

-

Meridian Bioscience Inc.

-

Biopanda Reagents Ltd.

-

Zeus Scientific Inc.

-

Stony Brook Medicine Laboratory

-

Virotech Diagnostics GmbH

-

Binding Site Group Ltd.

-

INOVA Diagnostics Inc.

-

Qiagen NV

Lyme Disease Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.15 Billion |

| Market Size by 2035 | USD 30.43 Billion |

| CAGR | CAGR of 8.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Serological Test, Lymphocytic Transformation Test, Urine Antigen Testing, Immunofluorescent Staining, Nucleic Acid Test) • By Sample Type (Blood, Urine, CSF, Other Blood Samples) • By Patient Type (Adult, Pediatric) • By End Use (Hospitals, Diagnostic Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Quest Diagnostics Incorporated, Laboratory Corporation of America (Labcorp), Thermo Fisher Scientific Inc., Bio-Rad Laboratories Inc., DiaSorin SpA, Siemens Healthineers AG, Roche Diagnostics GmbH, Immunetics Inc., EUROIMMUN AG, IDEXX Laboratories Inc., Abbott Laboratories, Becton Dickinson and Company, Meridian Bioscience Inc., Biopanda Reagents Ltd., Zeus Scientific Inc., Stony Brook Medicine Laboratory, Virotech Diagnostics GmbH, Binding Site Group Ltd., INOVA Diagnostics Inc., and Qiagen NV. |

Frequently Asked Questions

The Lyme Disease Testing Market is expected to grow at a CAGR of 8.56% from 2026 to 2035.

The Lyme Disease Testing Market was valued at USD 12.15 Billion in 2025.

Rising Lyme disease incidence from climate change-driven tick habitat expansion into previously non-endemic regions creating new testing volume streams, and technological advancement in next-generation serological and molecular diagnostic platforms improving accuracy and expanding addressable market value per diagnostic episode.

Serological Test dominated the Lyme Disease Testing Market with approximately 38.45% share in 2025, while Nucleic Acid Test is the fastest growing segment.

North America dominated the Lyme Disease Testing Market in 2025, reflecting the extraordinary U.S. disease burden of approximately 476,000 annual diagnoses that creates the world's largest single-country Lyme disease diagnostic testing market.

Get in Touch