Machine Safety Market Report Scope & Overview:

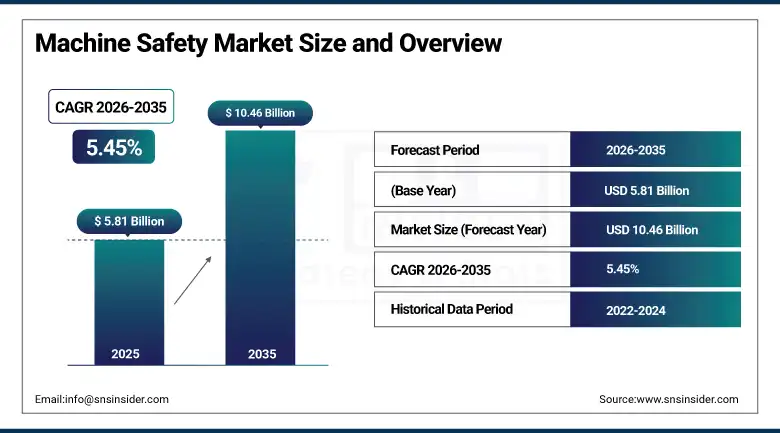

The Machine Safety Market was valued at USD 5.81 Billion in 2025 and is expected to reach USD 10.46 Billion by 2035, growing at a CAGR of 5.45% from 2026–2035.

There has been an increased rate of growth of machine safety market across the globe owing to increased focus on safety regulations at workplaces, innovations in technology, and increasing usage of automation systems in many industries. This segment comprises of different types of products such as safety sensors, controllers, interlock switches, safety light curtains, and emergency stops, among others. The key players in the industry, which includes manufacturing, oil and gas, pharmaceuticals, automotive, and food and beverages segments, have shown increasing inclination towards the use of machine safety systems that comply with international safety standards laid down by the International Electrotechnical Commission as well as other safety and health administration organizations worldwide.

In June 2025, KEYENCE Corporation introduced the GL-V series, a new small and robust safety light curtain specifically designed for industrial applications requiring compact installation in space-constrained machine guarding configurations. The GL-V series addresses the growing demand for miniaturized safety light curtain solutions in collaborative robotics and compact automated assembly cell applications where conventional safety light curtain dimensions create installation constraints that limit their deployment in modern high-density automation environments.

Market Size and Forecast

-

Market Size in 2026E: USD 6.13 Billion

-

Market Size by 2035: USD 10.46 Billion

-

CAGR: 5.45% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Machine Safety Market - Request Free Sample Report

Machine Safety Market Trends

-

Industrial IoT and AI integration enables predictive hazard detection, real-time monitoring, and automated safety responses reducing accidents and downtime.

-

Collaborative robot adoption is driving demand for dynamic safety systems like light curtains, scanners, and force-torque sensing solutions.

-

Functional safety standards such as IEC 62061 and ISO 13849 are increasing compliance-driven upgrades across automated manufacturing environments globally.

-

Wireless safety systems are gaining adoption by reducing installation complexity in mobile machinery and flexible manufacturing cell applications.

-

Cybersecurity integration is becoming essential as connected safety controllers introduce network risks affecting functional safety performance integrity.

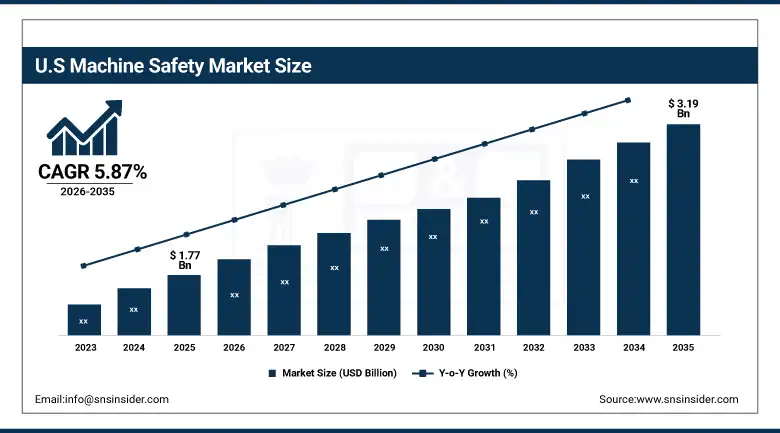

The U.S. Machine Safety Market Outlook

The U.S. Machine Safety Market was valued at approximately USD 1.77 Billion in 2025 and is expected to reach approximately USD 3.19 Billion by 2035, growing at a CAGR of approximately 5.87%.

The U.S. is the most commercially sophisticated machine safety market within North America's dominant revenue position. Rockwell Automation, Honeywell, Emerson Electric, and the U.S. operations of Siemens, ABB, and SICK AG collectively define the domestic machine safety commercial landscape. OSHA's workplace safety enforcement creates compliance-driven machine safety procurement motivation across manufacturing, construction, and process industry sectors. The U.S. automotive industry's above-average robotics adoption, the pharmaceutical sector's GMP safety standard requirements, and the food processing industry's machine guarding mandate create structured institutional demand. The extraordinary U.S. manufacturing reshoring investment programme is simultaneously creating new facility construction whose machine safety system specification creates above-average procurement growth.

In 2024, Rockwell Automation expanded its GuardShield Safety Light Curtain portfolio with new models featuring enhanced diagnostics, IP69K washdown protection, and EtherNet/IP connectivity for integration with Allen-Bradley safety PLC systems. The portfolio expansion demonstrates the commercial direction of machine safety product development toward connected; self-diagnosing safety devices whose network integration enables predictive maintenance and remote safety status monitoring that reduces the manual inspection burden that conventional safety device maintenance programmes require.

Machine Safety Market Segment Analysis

-

By Product Type, the safety sensors & switches segment dominated the machine safety market with 32.12% share in 2025, while the safety light curtains segment is the fastest growing.

-

By Implementation, the embedded components segment dominated the machine safety market with 53.08% share in 2025, while the individual components segment is the fastest growing.

-

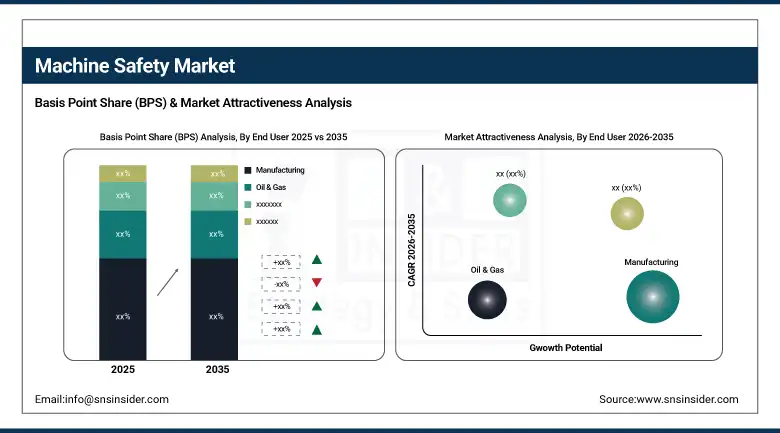

By End User, the manufacturing segment dominated the machine safety market with approximately 34% share in 2025, while the oil & gas segment is the fastest growing.

By Product Type, safety sensors & switches dominate, safety light curtains grow fastest

Safety sensors and switches retained the dominant product type position with 32.12% of the machine safety market in 2025. Their commercial primacy reflects the universal deployment requirement across production facilities where presence sensing, position detection, and hazard zone monitoring create consistent safety device procurement independent of specific industry sector or automation technology generation. Safety sensors and switches’ role in Robotic Process Automation hazard detection, their integration in machine guarding systems across the broadest range of industrial machinery types, and the regulatory mandate for presence sensing in proximity to automated equipment collectively sustain the product category’s commercial dominance.

Safety light curtains are the fastest-growing product type because collaborative robot adoption and dynamic machine guarding requirements are creating above-average demand for optoelectronic safety barriers whose programmable safety zone and muting capabilities provide flexible protection that conventional physical barriers cannot offer. Each cobot deployment that replaces a conventional industrial robot creates a safety light curtain procurement requirement whose flexible safety zone management enables productive human-robot collaboration without fixed barrier separation.

By Implementation, embedded components dominate, individual components grow fastest

Embedded components retained the dominant implementation position with 53.08% of the machine safety market in 2025. Embedding safety functionality directly into machine control systems, safety PLCs, and integrated automation architectures provides a simplified certified safety solution that eliminates the external safety device wiring, integration engineering, and certification validation that individual component approaches require separately. Each new machine designed to IEC 62061 or ISO 13849 safety function requirements specifies embedded safety architecture whose Safety Integrity Level certification is achieved through the integrated safety function design rather than external device addition.

Individual components are the fastest-growing implementation type because the extraordinary installed base of existing industrial machinery requiring safety upgrade without complete machine redesign creates retrofitting demand for standalone safety devices that can be added to existing control architectures. Each factory safety audit that identifies non-compliant machinery creates individual safety component procurement for emergency stop devices, safety interlock switches, and safety relay modules whose installation does not require control system replacement.

By End User, manufacturing dominates, oil & gas grows fastest

Manufacturing retained the dominant end-user position with approximately 34% of the machine safety market in 2025. The manufacturing sector’s commercial dominance reflects its extraordinary breadth encompassing automotive assembly, electronics manufacturing, food processing, pharmaceutical production, chemical processing, and consumer goods manufacturing whose combined facility count and automation density creates the most commercially distributed machine safety procurement of any industry vertical. Each manufacturing automation investment creates machine safety procurement whose aggregate across global manufacturing capital expenditure sustains consistent revenue growth.

Oil and gas is the fastest-growing end user because the combination of upstream production expansion in Middle Eastern, African, and Latin American oil fields, downstream refinery modernization investment, and pipeline infrastructure safety upgrade programmes are creating structured machine safety procurement at above-average per-facility commercial value. Hazardous area certification requirements for ATEX and IECEx-compliant safety devices in explosive atmospheres create premium machine safety procurement whose technical specification and certification requirements sustain above-commodity pricing. Each new LNG facility, offshore platform, and refinery upgrade creates machine safety investment whose combined commercial value substantially exceeds equivalent manufacturing facility safety procurement.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

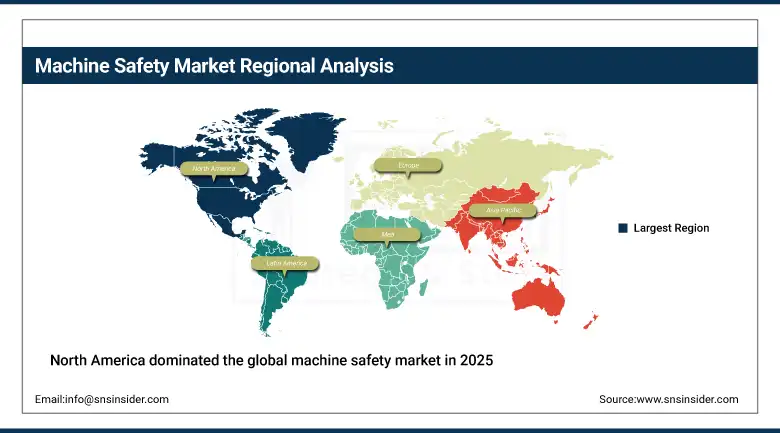

North America Machine Safety Market Insights

North America dominated the global machine safety market in 2025 driven by advanced manufacturing infrastructure, stringent OSHA workplace safety enforcement, and the strong adoption of automation across automotive, pharmaceutical, and food processing industries. The United States accounts for approximately 87.4% of North American revenues through Rockwell Automation, Honeywell, Emerson Electric, and the North American operations of Siemens, ABB, and SICK AG whose combined commercial presence defines the domestic machine safety technology standard.

Canada contributes approximately 12.6% of North American revenues through its automotive manufacturing sector’s safety investment, the natural resources industry’s hazardous equipment safety procurement, and the pharmaceutical sector’s growing machine safety compliance investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Machine Safety Market Insights

Europe is a technically sophisticated machine safety market where the EU Machinery Directive and its successor Machinery Regulation 2023/1230 create the world’s most comprehensive machine safety compliance framework whose implementation drives structured procurement across the European manufacturing base. Germany accounts for approximately 22.3% of European revenues through SICK AG’s domestic headquarters, the automotive OEM sector’s above-average robotics adoption, Pilz GmbH’s safety system expertise, and the industrial machinery sector’s machine safety standard-setting leadership.

The United Kingdom, France, and Italy are significant secondary markets where the automotive manufacturing sectors, pharmaceutical production facilities, and food and beverage processing industries create consistent machine safety procurement. SICK AG, Pilz, and Euchner’s European commercial networks sustain market supply from established regional presences.

Asia Pacific Machine Safety Market Insights

Asia Pacific is the fastest-growing regional machine safety market, driven by China’s extraordinary manufacturing automation investment, India's Industry 4.0 adoption, Japan's advanced robotics deployment, South Korea's semiconductor manufacturing, and Southeast Asia's expanding industrial base. China accounts for approximately 44.8% of Asia Pacific revenues through its automotive production scale, the electronics manufacturing sector's automation density, and the government's workplace safety enforcement improving industrial safety investment motivation across domestic manufacturing.

India represents the most commercially dynamic emerging market within Asia Pacific where the government’s workplace safety regulatory enforcement strengthening, the automotive manufacturing sector’s safety compliance investment, and the pharmaceutical industry's international GMP compliance requirement create above-average first-time machine safety system procurement growth.

MEA & Latin America Machine Safety Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through ARAMCO’s hazardous area safety investment, oil refinery automation, and Vision 2030’s industrial development creating new facility safety procurement.

Brazil leads Latin American revenues at approximately 44.2% through its automotive manufacturing sector's safety compliance, the food processing industry's machine guarding investment, and the oil and gas sector's safety system demand. Growing industrial investment across the Gulf and Latin America’s expanding manufacturing base sustain consistent regional market growth through 2035.

Market Dynamics

Growth Drivers: Automation and robotics adoption creating structured safety procurement and regulatory compliance mandates

Industrial automation and robotics adoption is the machine safety market’s most commercially certain structural growth driver. Each new robot installation creates a defined machine safety perimeter protection requirement whose safety light curtain, area scanner, or safety interlock specification compounds with the global robotics installed base growth. The International Federation of Robotics’ projection of over 700,000 new industrial robot installations annually creates proportional machine safety procurement whose aggregate across installation years compounds the global safety device installed base. Collaborative robot adoption’s human-robot shared workspace requirement creates safety architecture demand that conventional industrial robot cell guarding cannot address, creating new safety product procurement beyond conventional barrier replacement.

Regulatory compliance mandates from OSHA, the EU Machinery Regulation, IEC 62061, and ISO 13849 create non-discretionary machine safety investment across the global manufacturing base whose compliance motivation is independent of commercial ROI calculation. Each new machinery directive implementation cycle, each OSHA enforcement action against non-compliant manufacturing facilities, and each insurance requirement for machine guarding documentation creates safety procurement that sustains market growth through regulatory compliance cycles.

Restraints: High installation cost for small manufacturers and integration complexity with legacy equipment

Machine safety system installation cost creates adoption barriers for small manufacturing enterprises whose capital budget constraints require demonstrated ROI justification before safety system investment. Each safety system installation that requires control system engineering, device programming, SIL/PL validation testing, and regulatory documentation creates total implementation cost that substantially exceeds the hardware purchase price, creating budget barriers that delay compliance investment in cost-constrained small business environments.

Integration complexity with legacy equipment creates retrofit barriers whose engineering effort and production downtime requirement limit the pace of safety system upgrade across the existing installed base. Each legacy machine whose safety upgrade requires interfacing modern safety controllers with decades-old control systems creates integration engineering investment whose cost and technical complexity moderates the retrofit safety system procurement pace.

Opportunities: IIoT-enabled predictive safety and collaborative robot safety system development

IIoT-enabled predictive safety represents the most commercially premium technology direction whose real-time condition monitoring, anomaly detection, and predictive maintenance integration create safety system value substantially exceeding conventional reactive safety device capability. Each connected safety system that predicts and prevents safety incidents before they occur creates operational value whose measurement in avoided downtime, injury prevention, and insurance cost reduction sustains premium system pricing that conventional safety devices cannot command.

Collaborative robot safety system development represents the most commercially dynamic near-term product innovation opportunity whose dynamic safety zone management, force-torque sensing integration, and vision-based human presence detection create safety architectures specifically optimized for shared workspace operation. Each new cobot platform that requires application-specific safety validation creates safety system procurement from specialist safety engineering services whose expertise in cobot safety standard compliance sustains above-commodity pricing.

Recent Developments:

-

2025: Rockwell Automation advanced its integrated safety platform by strengthening GuardLogix safety controllers with cybersecurity-enabled functional safety features.

-

2025: Siemens AG expanded its machine safety portfolio by integrating advanced AI-based safety controllers and Industrial IoT connectivity, enabling real-time hazard detection and predictive safety.

-

2025: SICK AG enhanced its safety sensor solutions with next-generation LiDAR-based safety scanners and smart light curtain systems, improving dynamic zone protection.

Machine Safety Market key players are:

-

Siemens AG

-

Rockwell Automation Inc.

-

ABB Ltd.

-

Honeywell International Inc.

-

SICK AG

-

Pilz GmbH & Co. KG

-

Omron Corporation

-

Keyence Corporation

-

Eaton Corporation

-

Schneider Electric SE

-

Emerson Electric Co.

-

Euchner GmbH & Co. KG

-

Fortress Interlocks

-

Bernstein AG

-

Banner Engineering Corp.

-

Pepperl+Fuchs SE

-

Leuze Electronic GmbH

-

Wieland Electric GmbH

-

Troax Group AB

-

Schmersal Group

Machine Safety Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.81 Billion |

| Market Size by 2035 | USD 10.46 Billion |

| CAGR | CAGR of 5.45% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Safety Sensors & Switches, Safety Controllers, Safety Interlock Switches, Safety Light Curtains, Emergency Stop Devices, Safety Relays & Modules, Safety Edge & Bumpers, Others) • By Implementation (Embedded Components, Individual Components) • By End User (Manufacturing, Oil & Gas, Energy & Power, Automotive, Food & Beverages, Pharmaceutical, Chemicals, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG, Rockwell Automation Inc., ABB Ltd., Honeywell International Inc., SICK AG, Pilz GmbH & Co. KG, Omron Corporation, Keyence Corporation, Eaton Corporation, Schneider Electric SE, Emerson Electric Co., Euchner GmbH & Co. KG, Fortress Interlocks, Bernstein AG, Banner Engineering Corp., Pepperl+Fuchs SE, Leuze Electronic GmbH, Wieland Electric GmbH, Troax Group AB, Schmersal Group |

Frequently Asked Questions

The market is expected to grow at a CAGR of 5.45% from 2026 to 2035.

The market was valued at USD 5.81 Billion in 2025.

Industrial automation and robotics adoption creating systematic safety device procurement for each new robot installation, and regulatory compliance mandates from OSHA, EU Machinery Regulation, IEC 62061, and ISO 13849.

Safety Sensors & Switches dominated the market with 32.12% share in 2025.

North America dominated the market in 2025.

Get in Touch