Medical Connectors Market Size & Trends:

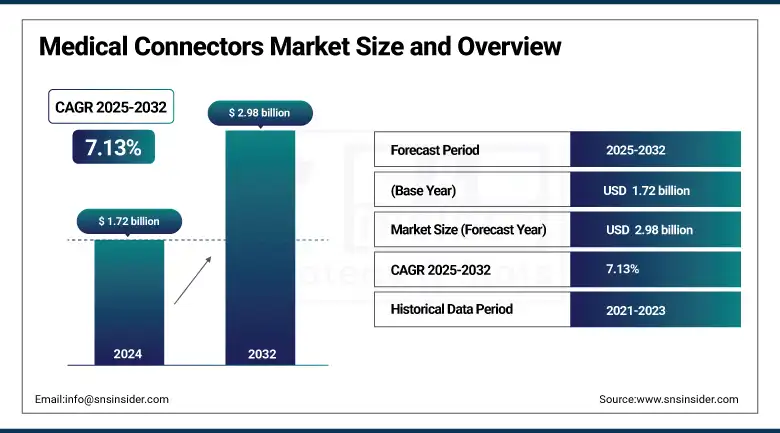

The Medical Connectors Market size was valued at USD 1.72 billion in 2024 and is expected to reach USD 2.98 billion by 2032, growing at a CAGR of 7.13% over 2025-2032.

The medical connectors market growth is being fueled by the increasing use of medical equipment and the prevalence of safe, secure, and sterile disposable connection systems in healthcare. The rapid increase in the acceptance of minimally invasive surgical devices, patient monitoring, and imaging systems is contributing to the medical connectors market growth.

To Get more information On Medical Connectors Market - Request Free Sample Report

For instance, A series of high-reliability circular medical connectors for diagnostic and therapeutic devices that require high signal integrity was introduced by Smiths Interconnect in April 2024.

More than 60% of hospitals globally have adopted modular equipment systems, which depend on precision connectors. In addition, in 2030, the global population of people aged 60 and above will reach 1.4 billion, a growing number of chronic disease patients, and long-term care medical equipment contractors will have a certain demand.

Healthcare infrastructure investments are increasing, too. India’s budget for 2024-25 included more than USD 10.6 billion for health, and the U.S. government allocated USD 1.6 billion to strengthen its Strategic National Stockpile, including components for medical devices. Over and above, medical R&D spending in the medical devices sector increased by 7.5% in 2023 in the U.S., indicating increased innovation in connector safety and miniaturization. Regulatory direction, such as the FDA’s UDI rule, also requires traceable, standardized connections, further driving the need for a compliant connector system.

For instance, Qosina launched the genderless AseptiQuik G sterile connector in March 2024 to meet biopharmaceutical processing challenges and the need for reliable sterile connections within a wide range of bioprocessing applications. These advances are consistent with current medical connectors market trends towards customizable, biocompatible, and regulations-compliant products and will continue to drive growth in the medical connectors market.

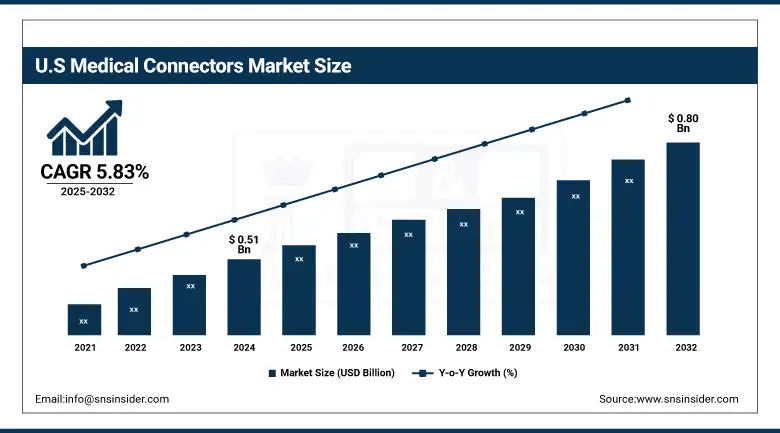

The U.S. medical connectors market size was valued at USD 0.51 billion in 2024 and is expected to reach USD 0.80 billion by 2032, growing at a CAGR of 5.83% over 2025-2032. The U.S. is the dominant player, led by the large adoption of diagnostic & monitoring applications and stringent guidelines by the FDA. USG expenditure in 2023 on medical devices R&D exceeded USD 3.3 billion, encouraging innovation in connector technology. Furthermore, the increasing adoption of wearable devices and remote patient monitoring is spurring a greater need for miniaturized and reliable connectors. Canada is growing modestly as it focuses on telehealth and ambulatory care, and Mexico is expanding as a hub for nearshore manufacturing, reinforcing regional supply chains.

| Company Name | Connector Type Developed | Application Area | Innovation Type | Launch Year |

|---|---|---|---|---|

| TE Connectivity | Hybrid Circular Connectors | Diagnostic Devices | Miniaturization | 2023 |

| LEMO S.A. | REDEL 2P High Voltage | Imaging Equipment | High-voltage handling | 2025 |

| Phillips-Medisize | TheraVolt Connectors | Wearable Devices | Integrated electronics | 2025 |

| Smiths Interconnect | High-density circular connector | Surgical Equipment | EMI shielding | 2024 |

| Fischer Connectors | UltiMate Series | Monitoring Systems | Sealed rugged designs | 2022 |

Medical Connectors Market Dynamics:

Drivers:

-

Innovations, Aging Population, and Digital Health Adoption are Propelling the Medical Connectors Market Forward

The global medical connectors market is influenced by a mixture of technological advancements, growing healthcare spending, and a rise in demand for reliable and secure connectivity solutions. The rising popularity of homecare and wearable devices, which is forecasted to exceed 1.1 billion units globally by 2026, is directly driving demand for robust connectors that are designed to facilitate uninterrupted power and data transfer. Telehealth and remote patient monitoring protocols, which experienced a 38% year-over-year growth (per the American Hospital Association) from 2021 to 2023, depend on secure, high-frequency connectors.

Growing demand for technologically advanced diagnostic imaging devices and robotic surgery tools, including da Vinci platforms of Intuitive Surgical, is also contributing to the growth of the market for medical connectors. IRL, R&D expenditure of medical technology companies increased by 6.4% in 2023 in the EU alone, thereby demonstrating a trend toward miniaturized and high-endurance connector designs. Regulatory support in the form of FDA's 510(k) clearance process and IEC 60601 standards is driving the creation of safer and high-performance interconnects. All these factors collectively support in continuous growth of the medical connectors market across hospitals, ASCs, and specialty care settings.

Restraints:

-

Complex Regulatory Compliance and Sterilization Challenges Hamper the Scalability of Medical Connectors

Despite its rising demand, the medical connectors market also faces significant constraints, such as stringent regulatory standards and a lack of customization ability of products. Medical connectors must comply with strict sterilization and safety requirements, such as ISO 10993 for biocompatibility and IEC 60601-1 for electrical safety, which in turn increases product development time and product costs. For instance, disposable device connectors need to be chemical resistant and to tolerate multiple sterilization methods, thereby imposing material cost pressures. Further complicating manufacturers is the U.S. FDA’s policing of medical device cybersecurity labeling as of October 2023, resulting in an increased burden on design and documentation.

Expensive manufacturing tools and low volume, highly customized orders mean there are no economies of scale, which in turn reduces supply chain efficiency and raises the costs of procuring for hospitals. Limited compatibility amongst the proprietary connector types has also been a barrier to supply continuity. Accordingly, despite surging demand, these supply-side challenges could hinder the further acceleration in the growth of the medical connectors market, especially for emerging-market producers looking to scale production while ensuring regulatory conformance.

Medical Connectors Market Segmentation Analysis:

By Connectors Type

Disposable plastic connectors were the leading type of medical connectors market analysis in 2024, the type held a 34.7% medical connectors market share in the overall market. They are the preferred standard owing to the growing requirement for single-use, sterile components in infusion systems, diagnostic kits, and fluid transfer applications. The global change to infection control and limiting cross-contamination in hospital settings after the COVID-19 outbreak has further boosted their application in developed and developing medical care systems.

Magnetic medical connectors are the fastest-growing segment by connector type due to easy mating, and safety interlocking feature, fail-safe connection in critical care and wearable medical equipment. Such connectors are becoming increasingly popular as they provide fast disconnects and are useful in-patient mobility solutions, particularly in home care and elderly care environments.

By Application

Monitoring devices were the applications segment leader in 2024, accounting for 41.3% of the medical connectors market share, largely due to the increasing incidence of chronic diseases and the enhanced deployment of real-time vital sign monitoring systems across inpatient and outpatient environments. Increased demand for remote patient monitoring systems and ICU expansions globally has further strengthened their preeminence.

Among them, therapeutic devices were the fastest-growing application segment. Increasing utilization of sophisticated surgical robots, infusion pumps, and neurostimulation systems needing exact electrical and fluidic connections is escalating demand for medical connectors, specifically in therapeutic applications.

By End-User

Hospitals & clinics were the leading end-user segment in 2024, with a medical connectors market share of 49.5%. This growth is attributed to the large number of patients in the region, significant healthcare infrastructure, and the increasing adoption of diagnostic and therapeutic instruments that utilize connector systems. Additionally, hospital-quality demands for equipment must meet stringent safety requirements, guaranteeing the growth in demand for certified connectors.

The ambulatory surgical centers (ASCs) are the fastest-growing end-user segment. Given the growing global trend in day-care surgeries and the demand for cost-effective care, ASCs are equipped with portable containerized and modular medical devices that necessitate a sterilizable connector system that has a small footprint, is robust, and is sterilized. Their increasing population, especially in urban areas, is also prompting a huge push in this end-use segment.

Medical Connectors Market Regional Insights:

Based on region, North America dominated the leading share of the medical connectors market analysis in 2024, primarily due to its well-established healthcare systems, which led to increased demand for medical devices, and owing to an early acceptance of new medical technologies in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second-largest growing regional medical connectors market. The growth of the European market is attributed to the rising usage of vented and non-vented connectors in diagnostic and therapeutic devices. Germany is the region’s epicenter, leveraging its strong medical equipment manufacturing base and sound regulatory systems, such as MDR (Medical Device Regulation). France and the U.K. have been experiencing steady growth of the industry, which can be attributed to the increase in outpatient treatment and digital health infrastructure investment. Only Germany will contribute almost a quarter of Europe’s combined MD export value in 2023, highlighting its strong market presence.

The Asia Pacific is the fastest-growing regional segment of the global medical connectors market, due to an increasing focus on enhancing the healthcare infrastructure, an increasing aging population, and increasing medical electronics manufacturing. China is ahead with its production capacity at scale and proliferation of high-end diagnostic systems in urban hospitals. The Chinese government in China spent USD 1.4 billion in 2023 to digitize the hospitals, thereby increasing the demand for high-end connectors. India is also ramping up, with movements including “Make in India” advocating for local production of medical devices. Japan, with its highly sophisticated electronics industry, is making a winning run in miniaturized medical connectors for wearable and robotic systems. Positive regulations and growing health insurance penetration help drive the region’s growth.

| Standard/Regulation | North America (FDA) | Europe (MDR/IVDR) | Asia (Japan, China) |

|---|---|---|---|

| Biocompatibility | ISO 10993 | ISO 10993 | GB/T 16886 (China) |

| Electrical Safety | IEC 60601-1 | IEC 60601-1 | JIS T 0601 (Japan) |

| Sterility Requirements | 21 CFR 820 | EN 556-1 | YY/T 0681 (China) |

| Labeling Requirements | UDI Rule | EUDAMED/UDI | China NMPA, Japan PM |

Key Players in the Medical Connectors Market:

Leading medical connectors companies in the market include Amphenol Corporation, TE Connectivity Ltd., Smiths Interconnect, Molex, Hirose Electric Co., Ltd., LEMO S.A., Fischer Connectors, ODU GmbH & Co. KG, Omnetics Connector Corporation, and Radiall.

Recent Developments in the Medical Connectors Market:

In June 2025, Phillips-Medisize introduced the TheraVolt medical connectors, designed to enhance connectivity, integration, and performance in next-generation medical devices, focusing on miniaturization and reliability for wearable and portable applications.

In June 2025, LEMO unveiled its new REDEL 2P High Voltage Connectors, tailored for medical imaging and diagnostic equipment, offering enhanced safety, higher voltage handling, and compact design for improved device performance.

In May 2025, A new generation of advanced connectors was highlighted by leading electronics manufacturers, engineered to meet the demanding requirements of medical technology, electric vehicles, and aerospace, emphasizing durability, data integrity, and environmental resistance.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.72 billion |

| Market Size by 2032 | USD 2.98 billion |

| CAGR | CAGR of 7.13% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Connectors Type (Flat Surgical Silicone Cables, Embedded Electronics Connectors, Radio-Frequency Connectors, Disposable Plastic Connectors, Hybrid Circular Connectors, Receptacle System, Power Cords With Retention System, Lighted Hospital-Grade Cords, Magnetic Medical Connectors, and Push-Pull Connectors) • By Application (Monitoring Devices, Therapeutic Devices, and Diagnostic Devices) • By End User (Hospital & Clinics, Ambulatory Surgical Centers, and Diagnostic Centers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Amphenol Corporation, TE Connectivity Ltd., Smiths Interconnect, Molex, Hirose Electric Co., Ltd., LEMO S.A., Fischer Connectors, ODU GmbH & Co. KG, Omnetics Connector Corporation, and Radiall |

Frequently Asked Questions

North America is expected to dominate the market by 2032 due to strong healthcare infrastructure, high R&D investment, and early adoption of advanced medical technologies.

Emerging trends include miniaturization of connectors for wearable tech, magnetic connector adoption for safety, and high-voltage and hybrid designs for next-gen diagnostic and therapeutic devices.

Major players include Amphenol Corporation, TE Connectivity Ltd., Smiths Interconnect, Molex, LEMO S.A., Hirose Electric, Fischer Connectors, Radiall, ODU GmbH & Co. KG, and Omnetics Connector Corporation.

Key growth drivers include the rising demand for home-based and wearable medical devices, increasing chronic disease prevalence, technological advancements, and stringent regulatory standards ensuring safety and reliability.

The medical connectors market was valued at USD 1.72 billion in 2024 and is projected to reach USD 2.98 billion by 2032, growing at a CAGR of 7.13% from 2025 to 2032.

Get in Touch