mRNA Technology Market Report Scope & Overview:

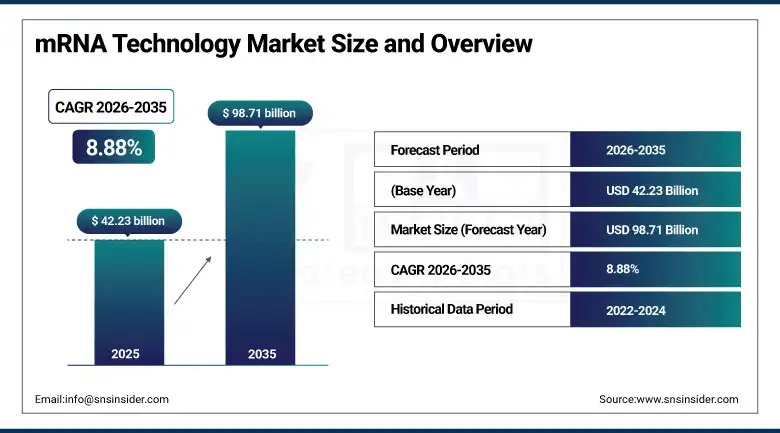

The mRNA Technology Market was valued at USD 42.23 Billion in 2025 and is expected to reach USD 98.71 Billion by 2035, growing at a CAGR of 8.88% from 2026–2035.

The global mRNA technology market has experienced a fundamental commercial transformation since the COVID-19 pandemic validated mRNA’s viability as a pharmaceutical platform at unprecedented scale. The extraordinary clinical success of Pfizer-BioNTech’s BNT162b2 and Moderna’s mRNA-1273 vaccines demonstrated manufacturing scalability, safety, and efficacy that advanced mRNA from an experimental technology into a proven pharmaceutical delivery system. The market is now diversifying beyond infectious disease vaccines into oncology, rare genetic disorders, autoimmune conditions, and cardiovascular disease applications whose clinical programmes are translating laboratory validation into commercial pipeline development.

Moderna initiated Phase 3 clinical trials for its mRNA-1345 RSV vaccine in 2023 and reported pivotal efficacy data in 2024, demonstrating 83.7% vaccine efficacy against RSV lower respiratory tract disease in adults over 60. The RSV vaccine represents Moderna’s first commercial mRNA product beyond COVID-19, demonstrating the technology platform’s generalisability to respiratory virus targets and establishing the commercial infrastructure for mRNA vaccine programme expansion beyond pandemic emergency use authorisation contexts.

Market Size and Forecast

-

Market Size in 2026E: USD 45.98 Billion

-

Market Size by 2035: USD 98.71 Billion

-

CAGR: 8.88% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On mRNA Technology Market - Request Free Sample Report

mRNA Technology Market Trends

-

mRNA cancer vaccine clinical programme development is accelerating across personalised neoantigen vaccines, shared tumour antigen vaccines, and combination approaches with checkpoint inhibitors.

-

Lipid nanoparticle engineering innovation is improving mRNA payload delivery efficiency, tissue targeting specificity, and storage stability whose cold chain requirements previously limited mRNA vaccine deployment in resource-limited settings.

-

Self-amplifying mRNA technology is enabling substantially lower mRNA dose administration that achieves equivalent immunogenicity, reducing manufacturing cost per dose and improving supply chain economics for both vaccine and therapeutic applications.

-

mRNA-based protein replacement therapy is advancing for rare genetic disorders including propionic acidaemia, methylmalonic acidaemia, and phenylketonuria.

-

CRISPR-mRNA combination approaches using mRNA to deliver Cas9 endonuclease transiently while sgRNA guides genome editing are creating precision medicine applications.

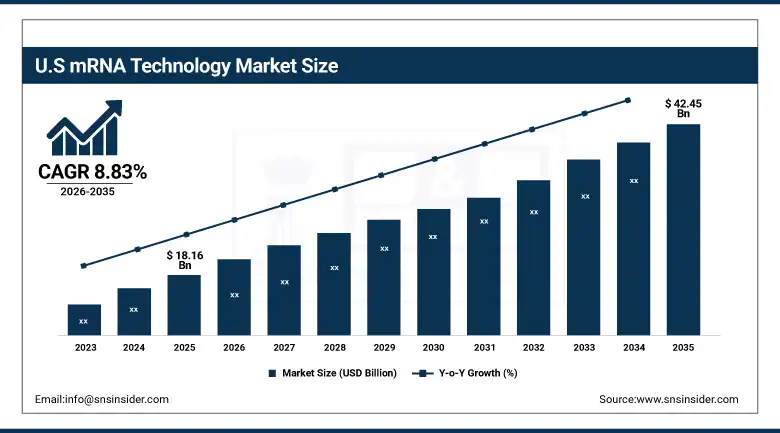

U.S. mRNA Technology Market Outlook

The U.S. mRNA Technology Market was valued at approximately USD 18.16 Billion in 2025 and is expected to reach approximately USD 42.45 Billion by 2035, growing at a CAGR of approximately 8.83%.

The U.S. is the world’s largest mRNA technology market. Moderna and Pfizer-BioNTech’s manufacturing infrastructure, BARDA’s pandemic preparedness funding for next-generation mRNA vaccines, and NIH’s substantial mRNA research investment collectively define the commercial and institutional ecosystem sustaining market leadership. FDA’s regulatory pathways for mRNA vaccines and its emerging guidance on mRNA therapeutics create the clinical development framework that sustains pipeline investment confidence.

Moderna reported positive Phase 2b/3 results for mRNA-1345 RSV vaccine in 2024, confirming 83.7% efficacy against RSV lower respiratory tract disease in older adults. The vaccine represents a landmark expansion of mRNA technology commercial application beyond COVID-19 into the large seasonal respiratory virus vaccine market whose addressable patient population encompasses hundreds of millions of older adults globally for whom RSV disease creates clinically significant hospitalisation risk.

mRNA Technology Market Segment Analysis

-

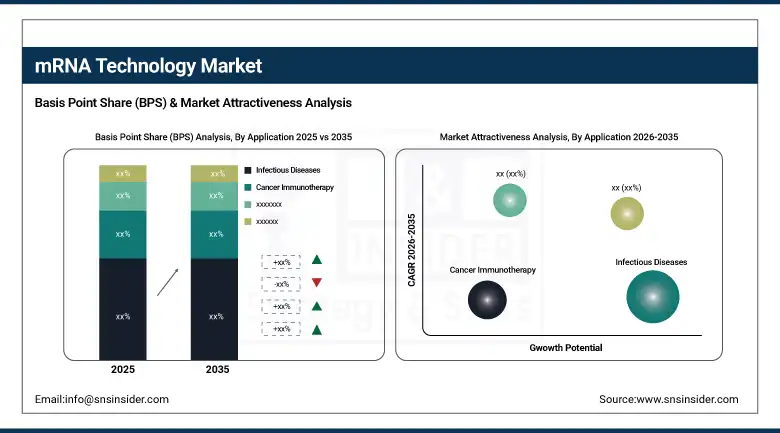

By Application, the Infectious Diseases segment dominated the mRNA Technology Market with approximately 71.00% share in 2025, while the Cancer Immunotherapy segment is the fastest growing.

-

By Delivery Method, the Lipid Nanoparticles segment dominated the mRNA Technology Market with approximately 80.00% share in 2025, while the Polymeric Carriers segment is the fastest growing.

-

By End User, the Pharmaceutical & Biotechnology Companies segment dominated the mRNA Technology Market with approximately 64.00% share in 2025, while the Contract Research Organisations segment is the fastest growing.

By Application, infectious diseases dominate, cancer immunotherapy grows fastest

Infectious diseases retained the dominant application position with over 71% of the mRNA technology market in 2025. COVID-19 vaccine revenue defines the majority of current market value, with Comirnaty and Spikevax annual sales continuing to generate multi-billion dollar revenue through variant-updated booster dose programmes. The RSV vaccine approval for Moderna’s mRNA-1345 is creating a second commercial mRNA vaccine revenue stream whose adult immunisation market addressable population of hundreds of millions of older adults creates commercial potential that approaches COVID-19 vaccine scale over a sustained annual revenue cycle.

Cancer immunotherapy is the fastest-growing application because the personalised neoantigen vaccine approach is demonstrating early clinical signals that validate mRNA’s most commercially distinctive capability: the ability to manufacture a patient-specific vaccine within weeks of tumour sequencing whose neoantigen targets are unique to each individual. Moderna’s mRNA-4157 combined with pembrolizumab reduced melanoma recurrence risk by 44% in Phase 2 data, creating the most compelling clinical evidence for personalised mRNA cancer vaccine efficacy that the field has yet generated. Each positive clinical programme readout creates investment momentum that sustains the oncology mRNA pipeline’s commercial expansion.

By Delivery Method, lipid nanoparticles dominate, polymeric carriers grow fastest

Lipid nanoparticles retained the dominant delivery method position with approximately 80% of the mRNA technology market in 2025. LNPs’ clinical validation through COVID-19 vaccine deployment at multi-billion-dose scale created an unprecedented evidence base for the delivery system’s safety, immunogenicity, and manufacturing scalability whose confidence cannot be replicated by any alternative delivery technology. Ionisable lipid formulations that are electrically neutral at physiological pH but positively charged in the low-pH endosome enable efficient mRNA release into the cytoplasm following cellular uptake, creating the delivery efficiency that makes LNP-mRNA systems commercially viable for vaccine and therapeutic applications.

Polymeric carriers are the fastest-growing delivery method because the limitations of lipid nanoparticles in therapeutic mRNA applications are creating structured development investment in alternative systems. LNPs’ primary tissue tropism for liver limits their utility for mRNA therapeutic applications targeting lung, muscle, or brain tissue where polymeric carriers with tunable surface chemistry can achieve superior cellular specificity. Polymeric systems based on poly(lactic-co-glycolic acid), polyethylenimine derivatives, and novel cationic polymers offer controlled-release kinetics that extend intracellular mRNA expression duration beyond the acute burst characteristic of LNP delivery.

By End User, pharma & biotech dominate, CROs grow fastest

Pharmaceutical and biotechnology companies retained the dominant end user position in the mRNA technology market in 2025. Moderna, Pfizer-BioNTech, CureVac, Arcturus Therapeutics, and Translate Bio collectively own the commercial mRNA manufacturing infrastructure, regulatory relationships, and intellectual property portfolios whose combined investment defines the market’s commercial scale. Each major pharma company that has established an mRNA platform creates ongoing technology investment that sustains the market’s commercial growth independently of individual product cycle variation.

Contract research organisations are the fastest-growing end user segment because the expansion of the mRNA clinical pipeline beyond the handful of companies with internal mRNA expertise is creating outsourced development demand from biotech sponsors and academic institutions whose therapeutic hypotheses require mRNA manufacturing and clinical development support that CROs with dedicated mRNA capabilities provide commercially. Lonza, Thermo Fisher’s patheon division, and specialised mRNA CROs are expanding their manufacturing and clinical support capabilities to serve the growing mRNA pipeline demand.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

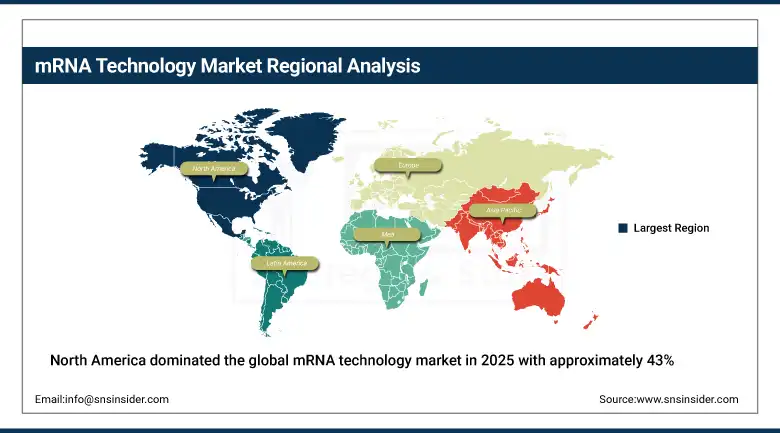

North America mRNA Technology Market Insights

North America dominated the global mRNA technology market in 2025 with approximately 43% of global revenues. The United States accounts for approximately 87.4% of North American revenues. Moderna’s Cambridge headquarters, Pfizer’s global vaccine operations, and BARDA’s multi-billion-dollar pandemic preparedness investment collectively define the U.S. market’s commercial leadership. NIH’s substantial basic mRNA research funding sustains the academic innovation pipeline that feeds commercial mRNA programme development across the most diverse oncology, rare disease, and infectious disease clinical portfolio of any national market.

Canada contributes approximately 12.6% of North American revenues through its active mRNA research institutions, government pandemic preparedness investment, and the commercial presence of mRNA manufacturing capabilities established during the COVID-19 pandemic response that are being repurposed for next-generation vaccine and therapeutic programme support.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe mRNA Technology Market Insights

Europe is a significant mRNA technology market where BioNTech’s Mainz headquarters, the EU’s HERA pandemic preparedness investment, and multiple academic mRNA research centres in Germany, the Netherlands, and the UK create a technically sophisticated mRNA ecosystem. Germany accounts for approximately 28.4% of European revenues through BioNTech’s dominant commercial position in mRNA oncology vaccine development, the German government’s mRNA technology investment, and CureVac’s next-generation vaccine programme development.

The United Kingdom and France are significant secondary markets where academic and commercial mRNA programme development, NHS vaccine deployment infrastructure, and government pandemic preparedness investment create consistent mRNA technology demand. The UK’s Vaccine Taskforce investment in mRNA manufacturing capability and France’s Sanofi mRNA partnership create national mRNA ecosystem development whose commercial output is progressively adding to European market revenue.

Asia Pacific mRNA Technology Market Insights

Asia Pacific is the fastest-growing regional mRNA technology market, driven by government pandemic preparedness investment across China, Japan, South Korea, and Australia, combined with growing domestic mRNA platform development that reduces dependence on Western technology licensing. China accounts for approximately 44.8% of Asia Pacific revenues through government investment in domestic mRNA vaccine manufacturing capability, the People’s Liberation Army Medical Research Institute’s mRNA programme development, and commercial biotech investment in mRNA oncology pipeline development.

Japan and South Korea are technically sophisticated secondary markets whose domestic pharmaceutical industries are investing in mRNA platform development. Daiichi Sankyo’s partnership with AstraZeneca on mRNA cancer vaccine development and South Korea’s Bioneer Corporation’s mRNA programme investment reflect Asia Pacific’s strategic commitment to mRNA technology capability development that creates commercial independence from Western platform licensing.

MEA & Latin America mRNA Technology Market Insights

The Middle East and Africa and Latin America are growing mRNA technology markets where government pandemic preparedness investment and the progressive expansion of mRNA manufacturing capability are creating structured market development. UAE leads MEA revenues at approximately 38.4% through the UAE’s G42 Healthcare mRNA manufacturing investment, Abu Dhabi’s life sciences cluster development, and the Gulf region’s above-average private healthcare investment that creates receptivity to novel biopharmaceutical technologies.

Brazil leads Latin American revenues at approximately 44.2% through Instituto Butantan’s mRNA technology transfer investment, FIOCRUZ’s pharmaceutical manufacturing programme, and the government’s strategic commitment to domestic mRNA vaccine manufacturing capability that reduces Latin America’s pandemic preparedness dependence on international supply chains.

Market Dynamics

Growth Drivers: COVID-19 validated platform enabling rapid programme diversification and personalised cancer vaccine demonstrating technology’s precision medicine potential

COVID-19 vaccine success has permanently altered the commercial landscape for mRNA technology by demonstrating at billion-dose scale that the platform delivers safe, efficacious products with manufacturing speed and scalability that conventional vaccine technologies cannot match. The USD 50 billion+ annual revenue generated by Comirnaty and Spikevax during peak pandemic years funded the manufacturing infrastructure, regulatory relationships, and institutional confidence that mRNA programme diversification requires. Every commercial pipeline expansion programme benefits from the technology credibility that COVID-19 vaccine success created.

Personalised cancer vaccine clinical progress is creating the most commercially transformative near-term value creation event in the mRNA technology market. Moderna’s mRNA-4157 Phase 2 data demonstrating 44% recurrence risk reduction in high-risk melanoma patients validates the neoantigen vaccine approach at a clinical evidence level that sustains FDA Breakthrough Therapy designation and justifies the substantial personalised manufacturing investment required for patient-specific vaccine production. Each positive Phase 3 readout from personalised cancer vaccine programmes will create a premium-priced commercial market whose revenue per patient substantially exceeds conventional vaccine economics.

Restraints: Cold chain storage requirements limiting developing market deployment and manufacturing cost of personalised approaches

mRNA technology’s cold chain requirements remain a meaningful deployment barrier in resource-limited settings. While COVID-19 vaccine development has improved LNP formulation stability at -20°C relative to the original -70°C requirement, room-temperature or refrigerator-stable formulations that enable developing market deployment without cold chain infrastructure are not yet universally achievable across all mRNA applications. Each degree of storage temperature improvement in LNP formulation stability expands the geographic reach of mRNA vaccine deployment.

The manufacturing cost of personalised neoantigen vaccines creates an economic challenge for mainstream clinical adoption. Each patient-specific vaccine requires individual tumour sequencing, neoantigen computational prediction, mRNA sequence design, and bespoke manufacturing whose per-patient cost is estimated at USD 100,000 to USD 200,000 prior to manufacturing scale optimisation. Achieving cost reduction to reimbursable levels requires manufacturing automation, parallel production capacity, and computational efficiency improvements whose development timeline extends the personalised vaccine’s commercial addressable market expansion.

Opportunities: RSV and influenza seasonal vaccine markets, protein replacement therapy for rare diseases, and mRNA manufacturing capacity in pandemic preparedness

RSV and influenza seasonal vaccine markets represent the most commercially certain near-term expansion opportunities beyond COVID-19 for mRNA platform companies. Both respiratory virus categories have large established vaccine markets with annual demand cycles, existing reimbursement infrastructure, and clinical precedent for efficacy-based market differentiation. mRNA’s manufacturing speed advantage enables annual strain-matched influenza vaccine production on shorter timelines than egg-based manufacturing allows, potentially capturing above-average market share in seasons where early strain selection accuracy is commercially valuable.

mRNA-based protein replacement therapy for rare genetic disorders represents a high-value therapeutic application whose orphan drug designation, premium pricing, and patent protection create commercial durability that vaccine markets cannot offer at equivalent margin. Enzyme replacement through repeated mRNA dosing avoids the immunogenicity challenges of recombinant protein therapy and the permanence risks of gene therapy whose safety profile concerns create regulatory and commercial barriers that mRNA’s transient expression profile advantageously circumvents.

Recent Developments:

-

2024: Moderna reported positive Phase 2b/3 pivotal data for its mRNA-1345 RSV vaccine demonstrating 83.7% vaccine efficacy in adults over 60, representing the first commercial mRNA vaccine programme beyond COVID-19 to achieve Phase 3 clinical validation and expanding the mRNA platform’s commercial scope into the large seasonal respiratory virus market.

-

2024: Moderna and Merck reported updated Phase 2 efficacy data for personalised cancer vaccine mRNA-4157 combined with pembrolizumab demonstrating sustained recurrence-free survival improvement in high-risk melanoma, advancing the programme toward Phase 3 trial initiation and validation of the personalised neoantigen vaccine commercial model.

-

2024: BioNTech advanced multiple mRNA oncology programmes into later-stage clinical trials in 2024, including BNT211 T-cell receptor therapy for CLDN6-positive solid tumours and BNT122 personalised neoantigen vaccine, demonstrating the systematic pipeline expansion that validates BioNTech’s commercial strategy of transitioning from pandemic vaccine provider to diversified mRNA therapeutics platform.

mRNA Technology Market Key Players

-

Moderna

-

Pfizer

-

BioNTech

-

AstraZeneca

-

CureVac

-

Arcturus Therapeutics

-

Translate Bio

-

Sanofi

-

Merck & Co.

-

Alnylam Pharmaceuticals

-

Beam Therapeutics

-

Precision BioSciences

-

Ethris GmbH

-

eTheRNA Immunotherapies

-

Entos Pharmaceuticals

mRNA Technology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 42.23 Billion |

| Market Size by 2035 | USD 98.71 Billion |

| CAGR | CAGR of 8.88% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Application (Infectious Diseases, Cancer Immunotherapy, Rare Genetic Disorders, Cardiovascular Diseases, Others) • by Delivery Method (Lipid Nanoparticles, Polymeric Carriers, Electroporation, Others) • by End User (Pharmaceutical & Biotechnology Companies, Research Institutes & Academic Centres, Contract Research Organisations, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Moderna, Pfizer, BioNTech, AstraZeneca, CureVac, Arcturus Therapeutics, Translate Bio, Sanofi, Merck & Co., Alnylam Pharmaceuticals, Beam Therapeutics, Precision BioSciences, Ethris GmbH, eTheRNA Immunotherapies, Entos Pharmaceuticals |

Frequently Asked Questions

The mRNA Technology Market is expected to grow at a CAGR of 8.88% from 2026 to 2035.

The mRNA Technology Market was valued at USD 42.23 Billion in 2025.

COVID-19 vaccine success permanently validating mRNA as a pharmaceutical platform at billion-dose scale and enabling rapid programme diversification, and personalised cancer vaccine clinical programmes demonstrating the technology’s precision medicine potential with early efficacy signals that sustain above-average R&D investment.

Infectious Diseases dominated the mRNA Technology Market with over 70% share in 2023, while Cancer Immunotherapy is the fastest growing application segment.

North America dominated the mRNA Technology Market in 2025 with approximately 43% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch