Process Automation and Instrumentation Market Size:

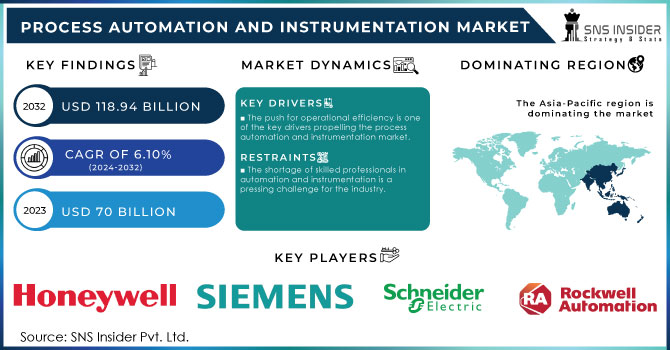

The Process Automation and Instrumentation Market Size was valued at USD 70 Billion in 2023 and is expected to reach USD 118.94 Billion by 2032, growing at a CAGR of 6.10% over the forecast period 2024-2032.

The process automation and instrumentation market has gained significant traction in recent years, driven by the increasing need for operational efficiency, safety, and regulatory compliance across various industries. Sectors such as oil and gas, chemicals, pharmaceuticals, and food and beverage are increasingly adopting automation solutions to streamline operations and reduce human error. In 2023, 60% of all occupations could automate at least 30% of their tasks, contributing to an anticipated 1.5% annual boost in global productivity. This surge in automation is expected to create between 3.3 to 6 million jobs by 2030, countering fears of job displacement. These technologies help companies achieve higher output rates, improved product quality, and more efficient resource utilization. Furthermore, the integration of the Internet of Things (IoT) and artificial intelligence (AI) into automation systems has revolutionized the industry. These advancements enable real-time data collection and analysis, allowing businesses to make informed decisions, optimize processes, and anticipate equipment failures before they occur.

Process Automation and Instrumentation Market Size and Forecast

-

Market Size in 2023: USD 70 Billion

-

Market Size by 2032: USD 118.94 Billion

-

CAGR: 6.10% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

Get more information on Process Automation and Instrumentation Market - Request Sample Report

Process Automation and Instrumentation Market Trends

-

Increasing adoption of industrial automation across manufacturing and energy sectors is driving market growth, with over 65% of large enterprises implementing automation solutions to enhance efficiency and reduce operational costs.

-

Rising integration of IIoT (Industrial Internet of Things) and smart sensors is enabling real-time monitoring and control, with connected devices in industrial environments growing at over 18% annually.

-

Strong demand for process optimization and predictive maintenance is boosting advanced instrumentation adoption, reducing downtime by 20–30% and improving asset utilization.

-

Expansion of oil & gas, chemicals, and power industries is accelerating deployment of automation systems, contributing to over 40% of total market demand.

-

Increasing focus on energy efficiency and regulatory compliance is driving adoption of advanced control systems, helping industries achieve 10–20% reduction in energy consumption.

In the context of industry applications, the oil and gas sector stands out as a significant contributor to the process automation and instrumentation market. With operations spanning exploration, production, refining, and distribution, the oil and gas industry requires highly automated systems to efficiently manage complex processes. Automation solutions in this sector include distributed control systems (DCS), supervisory control and data acquisition (SCADA) systems, and advanced process control (APC) technologies. These systems enable operators to monitor and control processes remotely, ensuring optimal performance while minimizing the risks associated with human intervention in hazardous environments.

Process Automation and Instrumentation Market Dynamics

Drivers

-

The push for operational efficiency is one of the key drivers propelling the process automation and instrumentation market.

Businesses are always looking for ways to improve productivity and lower costs, with process automation acting as a key strategy. by automating repetitive tasks, companies can reduce mistakes made by humans, maintain a consistent level of product quality, and make the most of their resources. In industries like manufacturing, oil and gas, and pharmaceuticals, improving operational efficiency results in substantial cost reductions. Automated procedures enhance manufacturing timelines, minimize operational interruptions, and enhance logistics coordination. In the manufacturing sector, automated production lines with advanced instruments can monitor quality in real-time, resulting in decreased waste and quicker turnaround times. With the escalation of global competition, the demand for operational efficiency will keep prompting investments in process automation and instrumentation technologies. Businesses that do not implement these solutions are at risk of lagging behind rivals that use automation to boost productivity.

-

The increasing emphasis on regulatory compliance in various industries is another significant driver for the process automation and instrumentation market.

Industries such as pharmaceuticals, food and beverage, and oil and gas are subject to stringent regulations aimed at ensuring safety, quality, and environmental sustainability. Automation solutions can help organizations comply with these regulations by providing precise control and monitoring capabilities. For example, in the United States, ISA/IEC 61511 is a key regulatory compliance standard for process automation and instrumentation, focusing on the safety lifecycle of safety instrumented systems. It emphasizes risk assessment, functional safety, comprehensive documentation, and management of change, ensuring effective design, implementation, and maintenance to enhance safety and minimize operational risks in the process industry. The rising costs associated with non-compliance, including fines, legal fees, and damage to reputation, further incentivize organizations to invest in process automation and instrumentation. As regulatory frameworks become more complex, businesses will increasingly turn to automation solutions to navigate these challenges effectively.

Restraints

-

The shortage of skilled professionals in automation and instrumentation is a pressing challenge for the industry.

With the rising utilization of automation technologies in organizations, there is a growing need for skilled personnel to develop, install, and upkeep these systems. A lot of schools and universities have fallen behind in adapting to the fast developments in automation technologies, resulting in a lack of necessary skills in the labor market. The lack of workers with the necessary skills may lead to increased labor expenses, causing competition among organizations and possibly causing delays in projects and obstacles in adopting automation solutions. Moreover, the intricacy of contemporary automation systems frequently necessitates expertise in fields like robotics, data analysis, and cybersecurity. Companies might find it challenging to locate individuals who possess the necessary abilities to effectively manage these intricacies. The lack of skills can also result in more dependence on outside consultants or contractors, causing costs to rise and making project management more complex. It will be crucial to address the skills gap as the industry evolves to successfully implement process automation and instrumentation technologies.

Process Automation and Instrumentation Market Segmentation

by Instruments

Field instruments dominated the process automation and instrumentation market in 2023 with a 57% market share, because of their widespread use across different industries. These devices, such as pressure transmitters, temperature sensors, flow meters, and level sensors, play a vital role in obtaining real-time data, allowing for process control and optimization. Siemens' SITRANS line of flow and temperature measurement instruments are commonly utilized in industrial settings, guaranteeing accurate supervision and regulation.

Process analyzers are projected to become the fastest-growing segment during 2024-2032. This growth is fueled by a rising need for quality assurance and regulatory compliance in various sectors such as food and beverage, pharmaceuticals, and water treatment. For instance, ABB's Process Automation Analyzer assists in the constant monitoring and regulation of essential process factors, guaranteeing superior product quality and waste reduction. As businesses prioritize automation and data-driven decision-making, the use of process analyzers is increasing at a fast pace.

by Solution

The PLC segment led the market in 2023 with a 29% market share. Their main purpose is to manage machinery and procedures using programmable instructions that can be easily adjusted to meet evolving operational requirements. Siemens and Rockwell Automation have created sophisticated PLC solutions that seamlessly integrate with other automation systems, improving efficiency and productivity. For example, Siemens' S7 series is extensively utilized in factories to oversee operations like controlling assembly lines, ensuring they run smoothly and in sync.

SCADA is expected to experience the fastest CAGR during 2024-2032. This centralized control system gathers information from distant sites, enabling data analysis and operational effectiveness. The expansion of SCADA systems is fueled by the emergence of Industry 4.0 and the growing demand for unified and automated solutions. Schneider Electric and Honeywell provide strong SCADA solutions, including Schneider's EcoStruxure, which combines IoT features for improved monitoring and control functions.

Process Automation and Instrumentation Market Regional Analysis

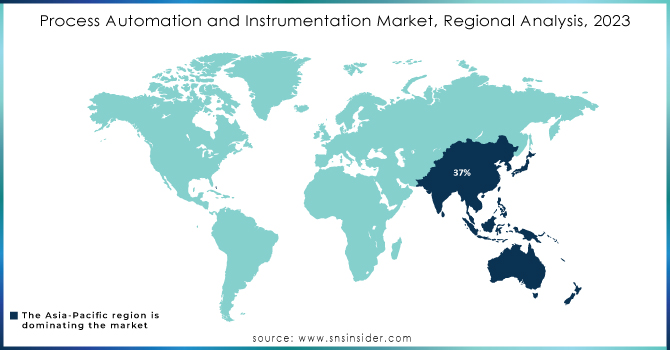

Asia-Pacific dominated in 2023 with a 37% market share and is anticipated to become the fastest-growing region during 2024-2032. The rapid growth in countries like China, India, and Japan is driven by fast industrialization, urbanization, and a growing need for efficiency in manufacturing processes. Key companies like Siemens, Mitsubishi Electric, and Yokogawa Electric are increasingly growing their presence in the area by providing creative solutions that cater to the specific demands of the local market. These companies are prioritizing smart manufacturing technologies like robotics and artificial intelligence to boost efficiency in diverse sectors like automotive, electronics, and food and beverage. The focus on sustainable practices and digital transformation in the APAC region boosts its growth, positioning it as a key investment area for process automation solutions.

Get a Customized Report as per your Business Requirement - Request For Customized Report

Key Players

The major key players in the Process Automation and Instrumentation Market are:

-

Siemens (SIMATIC S7-1200, SITRANS P320)

-

Honeywell (Experion PKS, SmartLine Pressure Transmitters)

-

Emerson (DeltaV Control System, Micro Motion Coriolis Flow Meters)

-

Schneider Electric (EcoStruxure Control Expert, Modicon M580)

-

ABB (ABB Ability System 800xA, 2600T Pressure Transmitters)

-

Rockwell Automation (PlantPAx Process Automation System, Allen-Bradley ControlLogix)

-

Yokogawa (CENTUM VP, EJX Series Pressure Transmitters)

-

Endress+Hauser (Proline Series Flow Meters, Liquiphant FTL31)

-

Mettler-Toledo (Ind560 Weighing Terminal, Thornton 770Max Conductivity Monitor)

-

KROHNE (OPTIFLEX 2200 C, OPTISENS Series)

-

Panasonic (FP-X Automation Controllers, ELCB Series Circuit Breakers)

-

Keysight Technologies (B1505A Power Device Analyzer, U1640B Handheld Multimeter)

-

Rohde & Schwarz (FSPN Power Meter, FPH Spectrum Analyzer)

-

Baker Hughes (Myscan PAX, 3D Scan)

-

GE Digital (Predix Platform, Proficy Smart Factory)

-

FLSmidth (MVP Technologies, Hot Kiln Alignment)

-

Azbil Corporation (Yamatake Series Control Valves, ZR Series Controllers)

-

Flowserve (Valtek Control Valves, Limitorque Actuators)

-

National Instruments (LabVIEW, PXI Systems)

-

Delta Electronics (DeltaVFD-B, PLC Automation Systems)

Suppliers of Raw Materials/Components for the key players:

-

Duke

-

WIKA

-

Texas Instruments

-

Texas Instruments

-

Omron

-

Toshiba

-

Murata Manufacturing

-

STMicroelectronics

-

Microchip Technology

-

Infineon Technologies

Recent Development

-

May 2024: ABB launched Symphony Plus SDe Series, a new range of hardware designed to upgrade existing process control systems while limiting any operational interference. The series serves power, water, oil & gas, and pharmaceutical industries to ensure smooth upgrades based on existing infrastructures.

-

April 2024: Siemens presented Simatic S7-1200 G2 – a next-generation controller intended for an enhanced motion control system, machine safety features, and overall performance. The solution is integrated with Siemens Xcelerator to attain industrial automation that is not only productive but cost-efficient.

-

February 2024: GE presented an innovative cloud-reliant solution called Autonomous Inspection, leveraging AI to automate inspections for industrial assets. The solution is integrated with the APM suite, offering unprecedented efficiency for the inspection process and valuable insights based on which the condition of industrial assets can be managed.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 70 Billion |

| Market Size by 2032 | USD 118.94 Billion |

| CAGR | CAGR of 6.10% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Instrument (Field Instruments, Process Analyzers) By Solution (PLC, DCS, SCADA, HMI, Functional Safety, MES) By Industry (Oil & Gas, Chemicals, Pulp & Paper, Pharmaceuticals, Metals & Mining, Energy & Power, Food & Beverages, Water & Wastewater Treatment, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Siemens, Honeywell, Emerson, Schneider Electric, ABB, Rockwell Automation, Yokogawa, Endress+Hauser, Mettler-Toledo, KROHNE, Panasonic, Keysight Technologies, Rohde & Schwarz, Baker Hughes, GE Digital, FLSmidth, Azbil Corporation, Flowserve, National Instruments, Delta Electronics. |

| Key Drivers | • The push for operational efficiency is one of the key drivers propelling the process automation and instrumentation market. • The increasing emphasis on regulatory compliance in various industries is another significant driver for the process automation and instrumentation market. |

| RESTRAINTS | • The shortage of skilled professionals in automation and instrumentation is a pressing challenge for the industry. |

Frequently Asked Questions

Ans: The Process Automation and Instrumentation Market is expected to grow at a CAGR of 6.10% during 2024-2032.

Ans: The PLC segment dominated the Process Automation and Instrumentation Market.

Ans: Asia-Pacific dominated the Process Automation and Instrumentation Market in 2023.

Ans: The increasing emphasis on regulatory compliance in various industries is another significant driver for the process automation and instrumentation market.

Ans: The Process Automation and Instrumentation Market was USD 70 Billion in 2023 and is expected to Reach USD 118.94 Billion by 2032.

Get in Touch