Neurology Device Market Report Scope & Overview:

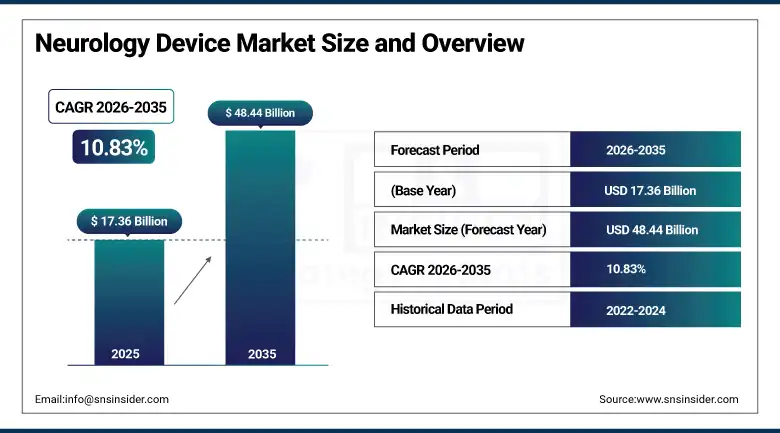

The Neurology Device Market was valued at USD 17.36 billion in 2025 and is expected to reach USD 48.44 billion by 2035, growing at a CAGR of 10.83% from 2026–2035.

The neurology device market is witnessing strong growth in the global market owing to the increasing prevalence of neurological disorders and rising demand for advanced diagnostic and therapeutic solutions. The growing burden of epilepsy, Parkinson’s disease, stroke, and Alzheimer’s disease is driving adoption of neurostimulation and neuroimaging devices in healthcare settings. Increasing investments in hospital infrastructure and neurology care centers are supporting market expansion. Technological advancements in deep brain stimulation, transcranial magnetic stimulation, and EEG systems are enhancing treatment outcomes. Rising geriatric population and increasing focus on minimally invasive neuro therapies are further fueling demand for neurology devices.

According to World Health Organization neurological disorder, more than 1 in 3 people globally are affected by neurological conditions, with over 1 billion individuals living with such disorders worldwide. Stroke accounts for approximately 12 million new cases annually and epilepsy affects around 50 million people. These measurable disease burdens are increasing demand for neuroimaging, electroencephalography, and neurostimulation devices across global healthcare systems.

Market Size and Forecast

-

Market Size 2026E: USD 19.20 billion

-

Market Size 2035: USD 48.44 billion

-

CAGR (2026 - 2035): 10.83%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Neurology Device Market - Request Free Sample Report

Neurology Device Market Trends

-

Increasing adoption of neurostimulation and neuromodulation devices for treating Parkinson’s disease, epilepsy, depression, and chronic neurological disorders globally.

-

Growing integration of artificial intelligence in neuroimaging systems improving diagnostic accuracy, early detection, and real time clinical decision support.

-

Rising investments in brain mapping research and neuroscience studies driving innovation in advanced neurotechnology and precision neurological treatments.

-

Expanding use of minimally invasive neurological procedures reducing patient recovery time and increasing adoption of advanced neurology devices.

-

Increasing development of brain computer interface technologies enabling communication between brain signals and external medical and assistive systems.

-

Growing demand for personalized neurological treatments supported by precision medicine approaches and advanced patient specific diagnostic technologies worldwide.

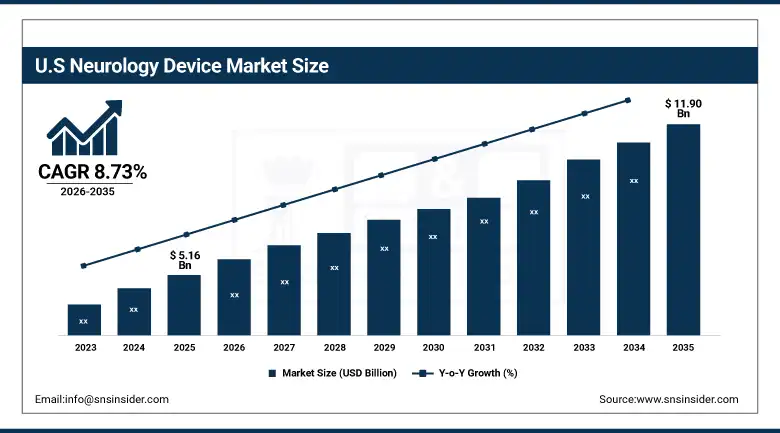

U.S. Neurology Device Market Size Outlook.

The U.S. Neurology Device Market was valued at USD 5.16 billion in 2025 and is expected to reach around USD 11.90 billion by 2035, growing at a CAGR of 8.73% from 2026–2035.

The U.S. neurology device market is growing consistently owing to increased demand for advanced neuroimaging systems, neurostimulation devices, and neurological care infrastructure. The usage of neurology devices in hospitals, neurology clinics, and research institutions has contributed to market growth in a consistent manner. Increased spending in neurological disorder treatment and digital healthcare adoption has generated an increase in demand for high-precision neuro diagnostic devices. Development of deep brain stimulation, transcranial magnetic stimulation, and EEG based monitoring systems is further driving the demand for this product.

According to the U.S. National Institute of Neurological Disorders and Stroke and Centers for Disease Control and Prevention, neurological disorders such as Parkinson’s disease affect nearly 1 million people in the United States, with approximately 90,000 new cases diagnosed annually, while essential tremor impacts millions of adults requiring clinical intervention.

As per the U.S. Census Bureau projections, the population aged 65 and older will continue rising, with over 58 million older adults recorded in recent estimates, increasing demand for neurostimulation and diagnostic neurology devices, including DBS and EEG systems used in clinical neurological care pathways.

Neurology Device Market Segment Analysis

-

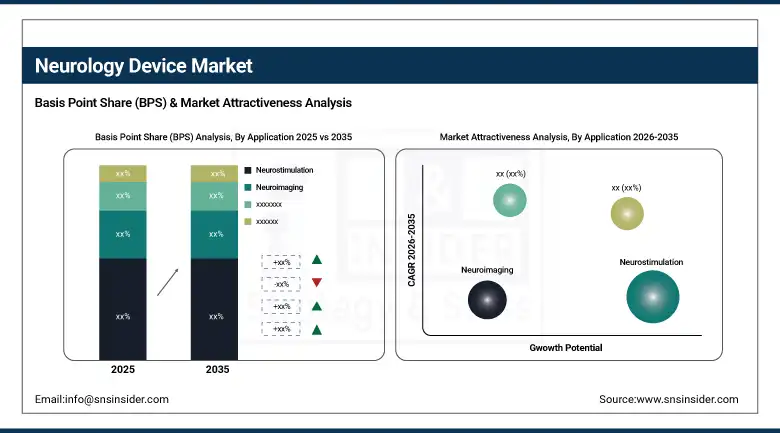

By Application, Neurostimulation dominated the market with 34.85% share in 2025; while Neurorehabilitation is the fastest growing segment with CAGR of 18.17% during 2026 to 2035.

-

By Device Type, Magnetic Resonance Imaging Devices dominated the market with 33.25% share in 2025; while Deep Brain Stimulation Devices are the fastest growing segment with CAGR of 16.15% during 2026 to 2035.

-

By End User, Hospitals dominated the market with 45.60% share in 2025; while Home Care Settings are the fastest growing segment with CAGR of 18.29% during 2026 to 2035.

By Application, neurostimulation dominated the neurology device market, while neurorehabilitation is the fastest growing segment.

Neurostimulation is the leading segment in the neurology device market owing to the maximum revenue share held by it in 2025. The main reason behind this is the increased incidence of Parkinson’s disease, epilepsy, and chronic pain disorders all over the world. Growing application of the deep brain stimulation system and the spinal cord stimulation devices is driving the demand. Positive clinical results, better patient acceptance, and constant technological development of implantable neurostimulation system are contributing to its market leadership position.

Neurorehabilitation segment is anticipated to have the fastest CAGR during the forecast period from 2026 to 2035. The growing number of stroke patients, traumatic brain injury patients, and age-related neurological disorders are expected to fuel the demand. High need for post-treatment rehabilitation programs and robotic rehabilitation devices is boosting the growth rate. Home care neurology services are also adding to the growth.

By Device Type, magnetic resonance imaging devices dominated the neurology device market, while deep brain stimulation devices are the fastest growing segment.

The Magnetic Resonance Imaging Devices segment accounted for the dominated revenue share in the neurology device market in 2025. It is primarily attributed to the significance of the MRI devices in making brain disorders diagnosis accurate. Furthermore, it is due to non-invasive abilities of these devices. Growing prevalence of neurological diseases and increasing adoption in hospitals are additional drivers boosting the segment growth. Advanced medical imaging technologies enable timely disease identification and efficient treatment planning.

The Deep Brain Stimulation Devices segment would witness fastest CAGR between 2026 and 2035. Rising numbers of Parkinson’s disease cases, epilepsy, and other movement disorders across the world fuel the growth. High adoption rate due to an increase in minimally invasive surgeries is a key driver pushing the segment growth. Advances in implantable neurostimulators enhance efficiency of treatment. Additionally, expanding neurological research and increasing awareness about neurostimulation treatment foster growth in the deep brain stimulation devices market.

By End User, hospitals dominated the neurology device market, while home care settings are the fastest growing segment.

The Hospital Segment was seen dominating the Neurology Device Market with the maximum revenue share in 2025. The reason for such domination is due to the presence of advanced neurological facilities and healthcare professionals in hospitals. The number of patients dealing with neurological diseases in hospitals is very high. The growing acceptance of neuro imaging, neuro stimulation, and surgical devices helps the market segment to dominate. Government investment and regular investments in neurology hospitals play a significant role in the same.

The Home Care Settings Segment is expected to be the fastest-growing CAGR between 2026 and 2035. The reason for the growth is the growing need for remote patient care facilities. Due to aging patients and the growing prevalence of chronic neurological conditions, there is an increasing demand for home care facilities. The introduction of portable neuro devices has helped the market to grow.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.65% |

|

Europe |

Germany |

28.50% |

|

Asia Pacific |

China |

42.00% |

|

Middle East & Africa |

UAE |

18.50% |

|

Latin America |

Brazil |

46.00% |

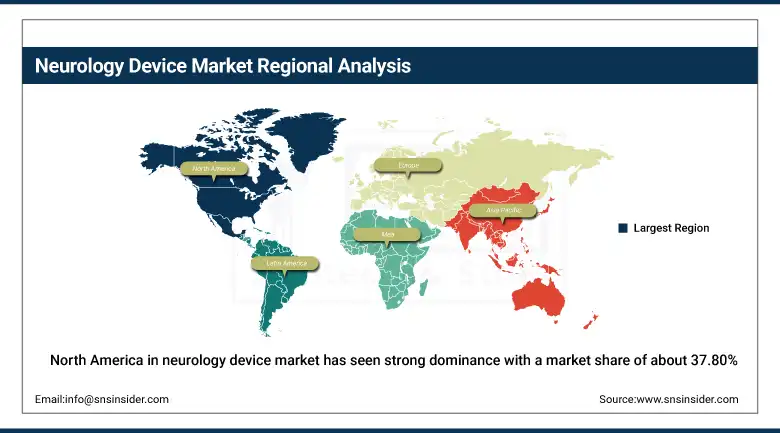

North America Neurology Device Market Insights.

North America in neurology device market has seen strong dominance with a market share of about 37.80% in 2025 due to advanced neurology infrastructure and high medical technology adoption. The region benefits from strong demand in neuroimaging systems, neurostimulation devices, and brain monitoring solutions. Increasing demand for early neurological disorder detection, chronic disease management, and advanced treatment solutions is driving market expansion across the United States and Canada. Rising adoption of digital neurology and homecare monitoring is further supporting market leadership. Strong R&D investments are strengthening neuro innovation capabilities.

According to the U.S. National Institute of Neurological Disorders and Stroke and the FDA regulatory clearance reports, neurological disorders impact more than 1 in 6 adults in the United States, with an annual incidence of about 795,000 strokes.

As per CMS reimbursement and FDA device approval tracking, deep brain stimulation, spinal cord stimulation, and vagus nerve stimulation devices are classified as Class III implantable devices, with over 500,000 DBS evaluations conducted annually in the U.S. The growing neurological disease burden and expanding clinical adoption of neurostimulation technologies continue to drive measurable uptake of neurology devices across North America in 2025.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Neurology Device Market Insights.

The Europe neurology device market shows strong presence in 2025 due to strict healthcare regulations and growing demand for advanced neurological treatment solutions. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on aging population care, stroke management, and neurodegenerative disease treatment is supporting steady market growth across the region. Increasing adoption in neuroimaging, EEG systems, and brain stimulation devices is further strengthening consumption. Expanding digital health frameworks are driving advanced neurology device adoption.

According to the European Brain Council and Eurostat, neurological disorders affect over 179 million people across Europe, representing more than one-third of the population when including mental and neurological conditions. As per Eurostat demographic indicators for 2025, over 21% of the EU population is aged 65 years or older, increasing demand for neurology devices used in stroke, Parkinson’s disease, and dementia management. WHO Europe reports stroke remains among the leading causes of long-term disability, with rising incidence linked to aging populations, while adoption of neurostimulation and monitoring devices exceeds 35% of tertiary neurological care centers in advanced European healthcare systems.

Asia Pacific Neurology Device Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the market during the forecast period with a market share of about 12.60% in 2025. Rapid healthcare infrastructure expansion and increasing neurological device manufacturing are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Expanding hospital networks, rising neurological disorder burden, and growing medical tourism are significantly boosting adoption. Rising demand for affordable and advanced neuro diagnostic solutions is further accelerating market growth across the region. Large scale healthcare investments support strong regional demand outlook.

According to the World Health Organization and Asia Pacific neurology devices market data reported under regional healthcare technology indicators, neurological disorders account for approximately 6.3% of the global disease burden, driving increased adoption of diagnostic and therapeutic neurodevices.

As per regional Asia Pacific neurology device, the region accounted for about 21.9% of global neurology device market share in 2025, with neurostimulation representing over 54% of product utilization in major hospital settings. Japan leads regional adoption with a 35.4% share in interventional neurology device usage, reflecting rapid expansion of advanced neurological care infrastructure and procedure-based device deployment across hospitals.

Middle East & Africa and Latin America Neurology Device Market Insights.

The Middle East & Africa and Latin America neurology device market is witnessing steady growth due to rising healthcare infrastructure development and neurological care modernization. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are emerging as key demand centers. Increasing investments in hospitals, neurology clinics, and diagnostic centers are supporting market expansion. Growing need for advanced neuroimaging and neurostimulation devices is further boosting product adoption. Rising healthcare access and government initiatives strengthen long term demand outlook across both regions.

As per WHO neurological workforce indicators, low-income countries only 0.1 neurologists per 100,000 population compared to a global median of 3.1, while over 24% of countries have stand-alone neurological policies. These measurable gaps in workforce and policy adoption directly influence demand for diagnostic and neurology devices across MEA and Latin America.

Market Dynamics

Growth Drivers: Rising prevalence of neurological disorders and growing demand for advanced diagnostic and therapeutic neurology devices

Rising prevalence rates for neurological ailments, such as strokes, epilepsy, Parkinson’s, and Alzheimer’s, have greatly increased demand for neurology devices. The aging demographics of both developed and developing nations will contribute to higher incidences of diseases. The need for early diagnosis and regular monitoring will result in greater uptake of neuroimaging and neuro stimulation technologies. Advanced technologies in brain analysis and minimally invasive procedures are improving results. Governmental activities aimed at raising awareness about neurological ailments will promote usage of neurology devices. Constant innovations related to neuro-diagnoses using artificial intelligence will positively impact global market growth.

According to the World Health Organization & Global Health Estimates, neurological disorders affect more than 3 billion people globally, accounting for over 43% of the world population experiencing some neurological condition burden during their lifetime.

As per WHO neurological disorder burden indicators, stroke contributes around 11% of total global deaths, while Alzheimer’s disease and other dementias account for approximately 7% of global mortality among older adults.

Restraints: Shortage of skilled professionals and complex regulatory approval processes for neurology devices

Lack of sufficient neurologists and technical skills hinders the optimal usage of technologically sophisticated neurology devices in numerous areas. Neurology devices are complex equipment that needs skilled people to operate them. Lack of training programs in emerging nations leads to low levels of adoption rates of neurology devices. There is stringent certification process needed before any neurology device can be launched into the market due to the need for compliance with safety requirements among others. Companies find it difficult to adhere to the varied regulatory requirements of different nations.

Opportunities: Rising investments in neuroscience research and development of advanced brain mapping and neurostimulation technologies

The rise of research investment in the field of neuroscience is providing new prospects for the creation of more sophisticated neurology equipment. There are many areas that can be used for innovative developments including brain mapping, cognition function analysis, and the study of neuroplasticity. The development of next generation neurostimulation and brain computer interface is creating new opportunities. Research facilities along with medical devices manufactures are actively working together to make breakthroughs. The government funding for neurological research is becoming higher around the world. The need for precision medicine in neurology encourages the development of individualized treatment options.

According to the U.S. National Institutes of Health & Brain Research through Advancing Innovative Neurotechnologies Initiative 2025, federally supported neuroscience research spans over 1,000 active projects focused on brain mapping, neural circuit decoding, and neurostimulation technologies.

As stated by OECD health innovation indicators, over 54% of neurology device utilization in advanced healthcare systems is concentrated in neurostimulation and interventional applications. WHO neurological disorder burden data shows that neurological conditions affect more than 1 in 3 people globally, reinforcing demand for advanced brain mapping and next-generation neurotherapeutic devices.

Recent Developments

-

2026: Penumbra received FDA clearance for next-generation Thunderbolt thrombectomy system enabling advanced neurovascular clot removal in acute ischemic stroke treatment.

-

2025: Medtronic expanded BrainSense adaptive deep brain stimulation system integration across Parkinson’s treatment workflows and digital neuromodulation platforms.

-

2025: Boston Scientific expanded neuromodulation portfolio through acquisition of Nalu Medical, enhancing peripheral nerve stimulation and chronic pain treatment capabilities globally.

-

2024: Abbott strengthened neuromodulation portfolio focusing on spinal cord stimulation and neurostimulation device advancements for chronic pain treatment applications.

Neurology Device Market Key Players are:

-

Medtronic

-

Boston Scientific Corporation

-

Abbott Laboratories

-

Johnson & Johnson

-

Siemens Healthineers

-

GE HealthCare

-

Koninklijke Philips N.V.

-

Stryker Corporation

-

Penumbra, Inc.

-

LivaNova PLC

-

Nihon Kohden Corporation

-

Natus Medical Incorporated

-

Integra LifeSciences Holdings Corporation

-

Elekta AB

-

Terumo Corporation

-

Olympus Corporation

-

Canon Medical Systems Corporation

-

MicroPort Scientific Corporation

-

Cadwell Industries

-

B. Braun Melsungen AG

Neurology Device Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.36 Billion |

| Market Size by 2035 | USD 48.44 Billion |

| CAGR | CAGR of 10.83% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Neurostimulation, Neuroimaging, Cerebrospinal Fluid Management, Neuromodulation, Neurorehabilitation) • By Device Type (Electroencephalography Devices, Magnetic Resonance Imaging Devices, Computed Tomography Devices, Deep Brain Stimulation Devices, Transcranial Magnetic Stimulation Devices) • By End User (Hospitals, Neurology Clinics, Research Institutions, Home Care Settings, Rehabilitation Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic, Boston Scientific Corporation, Abbott Laboratories, Johnson & Johnson, Siemens Healthineers, GE HealthCare, Koninklijke Philips N.V., Stryker Corporation, Penumbra, Inc., LivaNova PLC, Nihon Kohden Corporation, Natus Medical Incorporated, Integra LifeSciences Holdings Corporation, Elekta AB, Terumo Corporation, Olympus Corporation, Canon Medical Systems Corporation, MicroPort Scientific Corporation, Cadwell Industries, B. Braun Melsungen AG |

Frequently Asked Questions

The neurology device market is expected to grow at a CAGR of 10.83% from 2026 to 2035.

The neurology device market was valued at USD 17.36 billion in 2025.

Rising prevalence of neurological disorders such as stroke, epilepsy, Parkinson’s disease, and Alzheimer’s disease is driving global neurology device market growth.

North America dominated the neurology device market due to advanced infrastructure, high adoption of devices, and strong research investments.

Get in Touch