Oil Water Separator Market Report Scope & Overview:

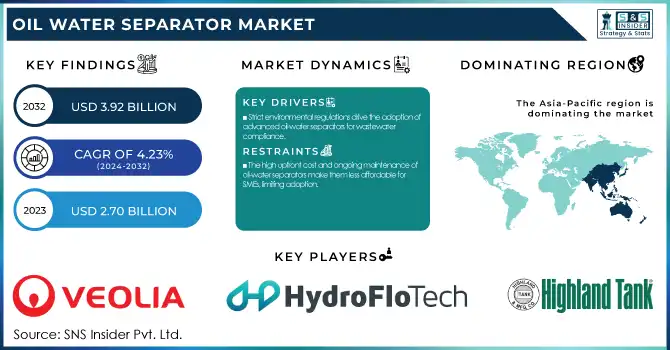

The Oil Water Separator Market Size was estimated at USD 2.70 billion in 2023 and is expected to arrive at USD 3.92 billion by 2032 with a growing CAGR of 4.23% over the forecast period 2024-2032.

The Oil Water Separator Market report offers unique insights by analyzing production capacity trends across key regions, highlighting supply-side dynamics. It explores adoption rates by industry, revealing sector-wise demand shifts, while assessing installation & maintenance costs by region, addressing operational expenditures. The study also examines regulatory compliance rates, mapping evolving environmental mandates, and provides export/import data to track global trade flow. Additionally, the report covers technological advancements in automated separation systems and the impact of stricter discharge regulations, shaping future industry standards.

Market Size and Forecast:

-

Market Size in 2023: USD 2.70 Billion

-

Market Size by 2032: USD 3.92 Billion

-

CAGR: 4.23% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

To Get more information on Oil Water Separator Market - Request Free Sample Report

Oil Water Separator Market Trends:

-

Increasing environmental regulations regarding wastewater discharge in industrial and marine sectors are driving market growth.

-

Rising demand from oil & gas, marine, manufacturing, and power generation industries is boosting installation of advanced separation systems.

-

Growing awareness about water conservation and environmental sustainability is accelerating adoption globally.

-

Expansion of offshore exploration activities and refinery operations is increasing the need for efficient oil-water separation technologies.

-

Technological advancements such as coalescing plate separators, hydrocyclones, and automated monitoring systems are improving efficiency and compliance.

-

Government initiatives supporting industrial wastewater treatment infrastructure are strengthening long-term market expansion.

Oil Water Separator Market Drivers

-

Stringent environmental regulations are driving the adoption of advanced oil-water separators across industries to ensure compliance with wastewater treatment and oil discharge standards.

Stringent environmental regulations are a key driver in the oil-water separator market, as governments worldwide enforce stricter wastewater treatment and oil discharge standards. Regulatory authorities like U.S. Environmental Protection Agency (EPA) and European Environment Agency (EEA) and International Maritime Organization (IMO) require industries to deploy oil-water separators in their facilities to forbid environmental pollution. These regulations affect industries such as marine, automotive and manufacturing, where oil-laden wastewater is a primary challenge. As new standards for sustainability are being established, industries are integrating improved separation technologies in the form of coalescence and membrane space systems to keep up with them. Currently the trend in the market is moving towards simply built, energy efficient designs that offer high oil removal efficiency while keeping maintenance to a minimum. Moreover, the increasing adoption of zero-liquid discharge (ZLD) policies and green manufacturing practices is further propelling market growth. As a result, this regulatory-driven growth pattern will not be reversed and will remain in place even as innovation and technology advances in oil-water separation solutions.

Oil Water Separator Market Restraint

-

The high upfront cost and ongoing maintenance of oil-water separators make them less affordable for SMEs, limiting adoption.

The high initial investment and maintenance costs associated with oil-water separators pose a significant challenge, particularly for small and medium-sized enterprises (SMEs). These initial costs involve acquiring superior separation technology, deploying, and embedding the plant within established wastewater treatment frameworks. Moreover, typical maintenance (filter replacements, cleaning, and system inspection, etc.) is also a recurring cost of operations. The cost also increases for advanced separation technologies (e.g. coalescing plate separators and membrane-based systems) due to the complex design and specialized components. These costs can be a barrier for SMEs with limited budgets, dissuading them from adopting oil-water separation solutions. Additionally, maintenance and adherence to environmental standards require money which disables small enterprises to operate on a long term basis. This causes several SMEs to resort to inefficient alternatives which then can lead to non-compliance with environmental regulations and a higher risk of oil contamination in water bodies.

Oil Water Separator Market Opportunities

-

The growing adoption of oil-water separators in food processing, mining, and power generation is driven by environmental regulations, wastewater management needs, and technological advancements.

The adoption of oil-water separators is expanding into new end-use industries, including food processing, mining, and power generation, driving significant market growth. They are widely used in the food processing industry for the treatment of wastewater containing oils, fats, and grease, allowing the facility to achieve compliance with environmental standards. The mining sector, which uses heavy machinery and consumes the most oil in its operations, depends on oil-water separators to treat wastewater and prevent natural water sources from getting contaminated. Likewise, power generation facilities and especially one with turbines and transformers generate wastewater heavily laden with oil necessitating effective separation solutions for optimal production performance and stringent discharge standards. With many industries now focusing more on environmental sustainability and regulatory compliance, the need for advanced oil-water separation technologies continues to grow. Beside membrane-based and coalescing separators they have different examples of new improving techniques for such process to increase efficiency and make them more attractive for wide range of applications. The spread of the trend opened profitable avenues for the manufacturing process to evolve and be brought on multiple sectors.

Oil Water Separator Market Challenges

-

Oil-water separators struggle with high oil concentrations and emulsified oils, requiring advanced technologies for effective separation and increased maintenance.

Oil-water separators often face technical limitations when handling high concentrations of oil and emulsified oils. Conventional gravity separators typically struggle to separate small, dispersed droplets of oil, reducing separation efficiency. So-called emulsified oils, which are made into stable mixtures with water by using surfactants or mechanical agitation, are very difficult to eliminate and their removal generally needs advanced process like coalescing or membrane filtrations. Moreover, the non-recovered high oil content causes obstacles, less working efficiency, and greater maintenance moment, thus elevating operational expenses. In industrial applications like marine, manufacturing, and wastewater treatment, failure to achieve separation can lead to environmental pollution or non-compliance with regulations. This includes separation technologies like centrifugal separators, electrocoagulation and ultrafiltration membranes. Nonetheless, such solutions tend to range on the expensive and operationally complex side, causing challenges with implementation, particularly along the small and medium enterprises (SME) segment.

Oil Water Separator Market Segmentation Analysis

By Technology

Gravity segment dominated with a market share of over 42% in 2023, due to their cost-effectiveness, ease of operation, and minimal maintenance requirements. These separators use oil-water density difference for the separation process and are the most commonly used separators in different industries. They are extensively adopted in the marine, industrial wastewater treatment, and oil & gas sectors due to regulatory compliance and environmental protection. Also, their ability to consume high amounts of polluted water without needing complex mechanical structures or high-power consumption gives them a further edge in becoming a market leader. However, industries are using gravity-based systems like gravity separators for cost-effective oil and water separation.

By End-User

The Industrial segment dominated with a market share of over 32% in 2023as the technology is widely used in a variety of diverse industries, including manufacturing, chemical processing, food & beverage, and wastewater treatment. These industries produce large volumes of oil-contaminated water, which requires effective separation solutions to meet environmental regulatory standards. Furthermore, the implementation of strict wastewater disposal regulations by governments and regulatory authorities to avoid pollution along with maintain operational efficiency is expected to drive industries towards the oil water separator market. Moreover, increasing emphasis on sustainability and water recycling also drive the market growth. Due to such automation as well as cost-effective and regulatory-compliant solutions for wastewater treatment, the Industrial segment retains its place in this market by far, which is attributed to rising growth opportunities for high-performance separators with improved efficiency.

Oil Water Separator Market Regional Outlook

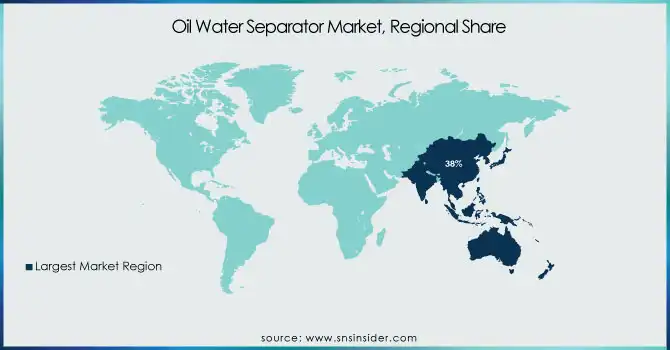

The Asia-Pacific region dominated with a market share of over 38% in 2023, owing to rapid industrialization, strict environmental rules and regulations, and the presence of manufacturing and oil & gas industries. The demand for oil and water separators in these countries is increasing due to an increase in industrial wastewater treatment needs along with government initiatives for pollution control. Moreover, the market is further propelled by the growing petrochemical, marine, and power generation segments. Stringent discharge regulations by environmental agencies coupled with the region's emphasis on sustainability, are propelling demand for effective separation technologies across the region. Asia-Pacific will continue to be a prominent market for oil-water separators owing to the increased investment in infrastructure and industrial installation, contributing to adherence with environmental regulations while facilitating industrial growth.

Europe is the fastest-growing region in the oil water separator market, driven by stringent environmental regulations aimed at reducing water pollution and ensuring compliance with wastewater discharge standards. In addition, increasing demand for wastewater treatment solutions across various industries, such as oil & gas, chemicals, and manufacturing, is expected to drive the market growth. Furthermore, with industries focusing towards sustainability, advanced oil water separators are getting more popular to avoid the environmental impact. Government policies like European Green Deal promotes investment in sustainability technologies as the market develops faster accelerates expansion. The increasing emphasis on industrial automation and also smart water management solutions is further driving the demand for efficient oil water separation systems in the region, making Europe a prominent region for future market developments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Some of the Major Key Players in the Oil Water Separator Market

-

Veolia (France) – (Hydrex Oil-Water Separators)

-

HydroFloTech (U.S.) – (Coalescing Oil-Water Separators)

-

Highland Tank (U.S.) – (Oil/Water Separators - UL-SERIES)

-

Wärtsilä (Finland) – (Wärtsilä OWS-15 Series)

-

Victor Marine Ltd. (U.K.) – (OWS-25GT Oil Water Separator)

-

Ultraspin (Australia) – (Ultraspin Oil Water Separator)

-

Mercer International Inc. (U.S.) – (Mercer CPI-Tilt Oil Water Separator)

-

Parkson Corporation (U.S.) – (Hydrocarbon Removal Systems)

-

Schlumberger (SLB) (U.S.) – (Cameron Oil-Water Separation Systems)

-

EnekaUAB (Lithuania) – (Eneka Oil-Water Separators)

-

Llalco Fluid Technology, S.L. (Spain) – (Bilge Water Separators)

-

Ellis Corporation (U.S.) – (Ellis Oil Water Separators)

-

Sulzer (Switzerland) – (Sulzer Oil/Water Separation Systems)

-

Alfa Laval (Sweden) – (PureBilge Bilge Water Separator)

-

GEA Group (Germany) – (GEA BilgePure Oil Water Separator)

-

H2O Surplus Ltd. (Canada) – (Industrial Oil Water Separators)

-

Containment Solutions (U.S.) – (Underground Oil-Water Separators)

-

Jowa AB (Sweden) – (JOWA 3SEP Oily Water Separator)

-

Freylit (Austria) – (Oil Separator Systems)

-

Filtramax (Italy) – (Centrifugal Oil Water Separators)

Suppliers for (Coalescing plate oil-water separators) on oil water separator market

-

Flottweg SE

-

Alfa Laval AB

-

GEA Westfalia Separator Group GmbH

-

Mohr Separations Research, Inc. (MSR)

-

Bhagyashree Accessories Pvt. Ltd.

-

H2K Technologies, Inc.

-

Parker Hannifin Corporation

-

HydroFlo Tech

-

Mercer International Inc.

-

Highland Tank

Recent Development

In May 2024: Veolia's subsidiary, SIDEM, won a $320 million contract to provide engineering and key technologies for Dubai's Hassyan seawater desalination plant. Commissioned by DEWA and ACWA Power, it will be the world's second-largest reverse osmosis facility and the largest powered entirely by solar energy.

In February 2024: Wärtsilä Water & Waste reintroduced its STC0-23 sewage treatment plant, the most compact model in its Super Trident series. Designed for both gravity and vacuum waste systems, it uses an activated sludge system to enhance biological treatment.

| Report Attributes | Details |

| Market Size in 2023 | USD 2.70 Billion |

| Market Size by 2032 | USD 3.92 Billion |

| CAGR | CAGR of 4.23% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Gravity, Sponge, Coalescing, Centrifuge, Other) • By End-User (Industrial, Marine, Aerospace, Power Generation, Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Veolia, HydroFloTech, Highland Tank, Wärtsilä, Victor Marine Ltd., Ultraspin, Mercer International Inc., Parkson Corporation, Schlumberger (SLB), EnekaUAB, Llalco Fluid Technology, S.L., Ellis Corporation, Sulzer, Alfa Laval, GEA Group, H2O Surplus Ltd., Containment Solutions, Jowa AB, Freylit, Filtramax |

Frequently Asked Questions

Asia-Pacific dominated the Oil Water Separator Market in 2023

The “Gravity” segment dominated the Oil Water Separator Market.

Stringent environmental regulations are driving the adoption of advanced oil-water separators across industries to ensure compliance with wastewater treatment and oil discharge standards.

The Oil Water Separator Market was USD 2.70 billion in 2023 and is expected to reach USD 3.92 billion by 2032.

The Oil Water Separator Market is expected to grow at a CAGR of 4.23% during 2024-2032.

Get in Touch