Osteoarthritis Therapeutics Market Report Scope & Overview:

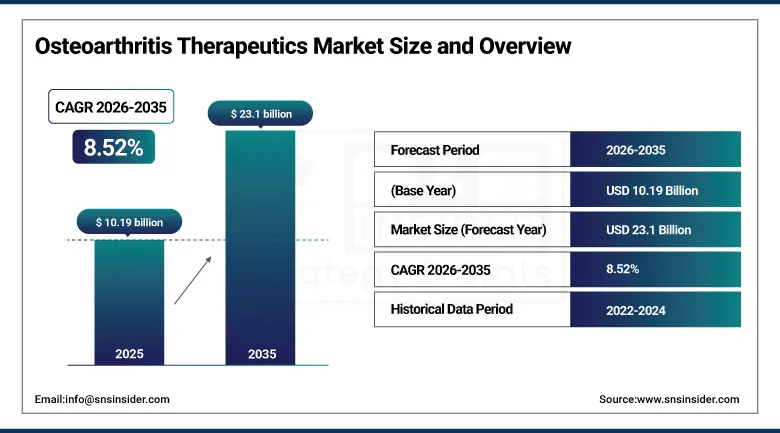

The Osteoarthritis Therapeutics Market was valued at USD 10.19 Billion in 2025 and is expected to reach USD 23.1 Billion by 2035, growing at a CAGR of 8.52% from 2026–2035.

The global osteoarthritis therapeutics market is advancing as the world’s most prevalent musculoskeletal disease affects over 528 million individuals globally and is accelerating in incidence through the intersection of the ageing population’s progressive joint cartilage degeneration and the obesity epidemic’s excessive mechanical loading of weight-bearing joints. Osteoarthritis’s pathophysiology, where the progressive degradation of articular cartilage creates pain, stiffness, joint effusion, and eventual functional disability in the knee, hip, hand, and spine joints, creates a lifelong treatment requirement spanning initial pain management with analgesics and NSAIDs through intra-articular corticosteroid and hyaluronic acid injection to eventual joint replacement surgery. Disease-modifying osteoarthritis drug research is creating pipeline therapies targeting cartilage regeneration, synovial inflammation modulation, and bone remodelling that represent the market’s most commercially transformative near-term innovation category.

In September 2024, Sun Pharmaceutical Industries and Moebius Medical received U.S. FDA Fast Track designation for MM-II, their investigational non-opioid intra-articular treatment for knee osteoarthritis pain. The Fast Track designation enables rolling NDA review and more frequent FDA interactions during the development programme, reflecting the FDA’s recognition of MM-II’s potential to address the unmet medical need for effective non-opioid osteoarthritis pain management whose current therapeutic options create inadequate pain relief or unacceptable side effect burden for a significant proportion of osteoarthritis patients.

Market Size and Forecast:

-

Market Size in 2026E: USD 11.06 Billion

-

Market Size by 2035: USD 23.1 Billion

-

CAGR: 8.52% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Osteoarthritis Therapeutics Market - Request Free Sample Report

Osteoarthritis Therapeutics Market Trends:

-

Disease-modifying osteoarthritis drug development is advancing sprifermin and lorecivivint through late-stage clinical trials targeting cartilage regeneration.

-

Intra-articular extended-release formulation development is reducing injection frequency requirements to improve patient adherence and joint exposure.

-

Platelet-rich plasma and mesenchymal stem cell injection therapies are gaining clinical adoption for knee osteoarthritis as regenerative medicine evidence accumulates.

-

Wearable biomechanical monitoring devices are integrating with pharmaceutical OA management programmes to personalise activity recommendations.

-

Topical NSAID formulation uptake is accelerating among elderly patients seeking effective joint analgesia with reduced gastrointestinal side effect burden.

The U.S. Osteoarthritis Therapeutics Market Outlook:

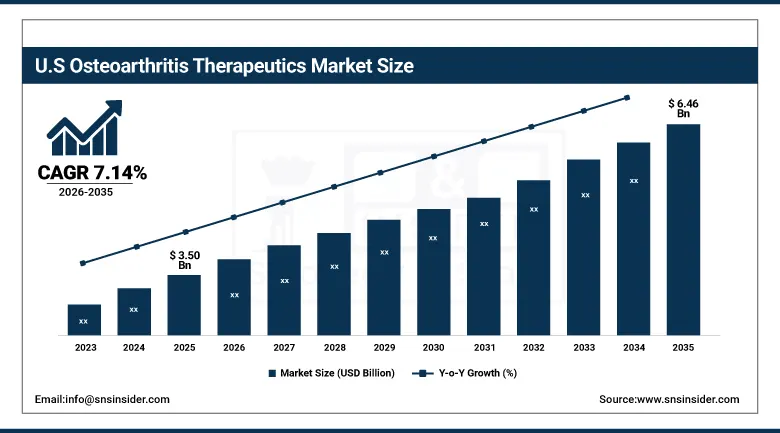

The U.S. Osteoarthritis Therapeutics Market was valued at approximately USD 3.50 Billion in 2025 and is expected to reach approximately USD 6.46 Billion by 2034, growing at a CAGR of approximately 7.14%.

The United States leads North American revenues through the world’s largest osteoarthritis patient population of approximately 32.5 million CDC-diagnosed cases, the highest per-capita healthcare expenditure creating premium therapeutic access, and the concentration of pharmaceutical R&D investment in DMOAD pipeline development. Pfizer, Eli Lilly, Sanofi, and AbbVie sustain U.S. OA therapeutics market leadership through their established NSAID, corticosteroid, and biologics portfolios, while FDA Fast Track designations for investigational DMOADs are accelerating the development of next-generation disease-modifying agents.

In June 2023, Eupraxia Pharmaceuticals received U.S. FDA Fast Track designation for EP-104IAR, a long-acting corticosteroid formulation for knee osteoarthritis providing up to six months of sustained anti-inflammatory activity from a single intra-articular injection. The designation reflected clinical urgency for improved corticosteroid delivery that extends the therapeutic window beyond the four to six-week duration of standard triamcinolone acetonide injection, reducing the injection frequency required for adequate OA pain management and the associated cumulative cartilage exposure risk from repeated corticosteroid administration.

Osteoarthritis Therapeutics Market Segment Analysis:

-

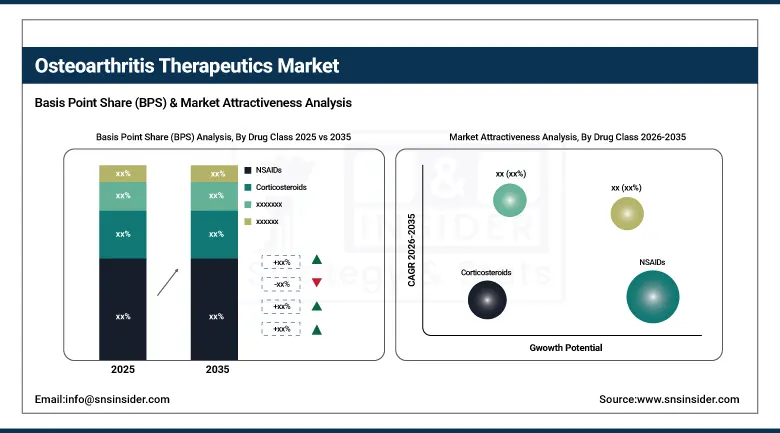

By Drug Class, NSAIDs segment dominated the osteoarthritis therapeutics market with approximately 38% market share in 2025 through widespread oral and topical analgesic prescription, while DMOADs are the fastest growing with a CAGR of approximately 12.4%.

-

By Route of Administration, oral segment dominated the osteoarthritis therapeutics market with the largest share in 2025, while the intra-articular injections segment is the fastest growing.

-

By End User, hospitals segment dominated the osteoarthritis therapeutics market with the largest share in 2025 through specialist orthopaedic and rheumatology clinical procurement, while retail pharmacies are growing through OTC NSAID and topical analgesic self-medication.

By Drug Class, NSAIDs dominate, DMOADs grow fastest

NSAIDs retained the dominant drug class position with the largest share of the osteoarthritis therapeutics market in 2025. Their commercial primacy reflects the foundational status of non-steroidal anti-inflammatory drugs as the first-line pharmacological osteoarthritis management option recommended across all major clinical practice guidelines globally, where the combination of effective prostaglandin-mediated pain and inflammation reduction, decades of clinical experience, broad prescriber familiarity, and both prescription and over-the-counter availability create the largest individual prescription and OTC sales volume among all OA therapeutic categories. Oral NSAIDs including ibuprofen, naproxen, diclofenac, and celecoxib, and topical NSAID formulations including diclofenac gel whose favorable gastrointestinal safety profile creates preferential specification for elderly patients, collectively sustain NSAIDs’ revenue leadership across the complete spectrum of OA severity from mild symptomatic management to moderate disease control.

DMOADs are growing fastest at approximately 12.4% CAGR because the biopharmaceutical pipeline’s advancing disease-modifying OA programmes represent the most commercially significant near-term OA therapeutic innovation whose successful clinical validation would create a fundamentally new treatment paradigm. Sprifermin’s fibroblast growth factor 18 mechanism stimulating cartilage matrix synthesis, lorecivivint’s CLK/DYRK kinase inhibition modulating Wnt pathway signalling, and anacaulase-bcdb’s matrix metalloproteinase inhibition represent mechanistically diverse DMOAD candidates whose late-stage clinical results are progressively defining the market’s structural growth trajectory.

By Route of Administration, oral dominates, intra-articular grows fastest

Oral administration retained the dominant route position with the largest share of the osteoarthritis therapeutics market in 2025. Oral NSAID and analgesic prescriptions create the highest volume and broadest patient access therapeutic category, whose once or twice daily dosing convenience, retail pharmacy dispensing accessibility, and established prescription reimbursement pathways sustain oral route’s commercial dominance across both early-stage symptomatic management and ongoing long-term OA pain control. Oral slow-release diclofenac, extended-release naproxen, and celecoxib’s selective COX-2 inhibition with preferential gastrointestinal safety profile each represent commercially significant oral OA therapeutics whose prescriber specification creates sustained procurement.

Intra-articular injections are growing fastest because the expanding clinical evidence for hyaluronic acid visco supplementation, corticosteroid injection, and emerging platelet-rich plasma and cellular therapy intra-articular administration creates a growing specialized injection therapy market whose per-procedure commercial value substantially exceeds oral pharmaceutical equivalent courses. Each new extended-release intra-articular formulation approved for reduced injection frequency, each PRP injection protocol validated for clinical superiority versus conventional intra-articular therapy, and each regenerative medicine injection approach accumulating positive clinical evidence creates above-market procurement growth in the injection route category.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Osteoarthritis Therapeutics Market Insights

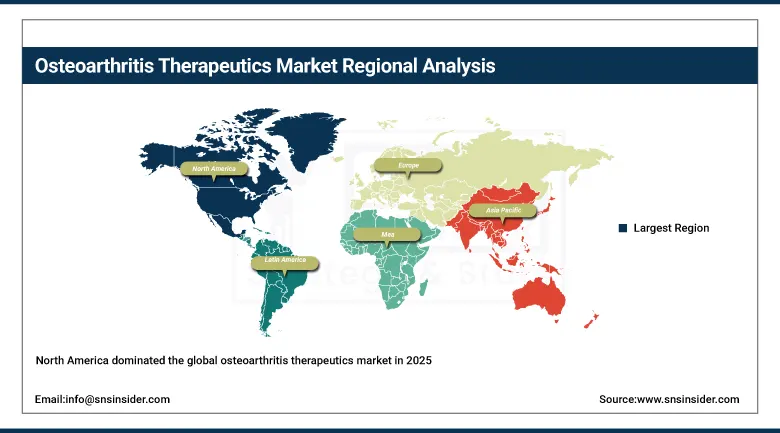

North America dominated the global osteoarthritis therapeutics market in 2025 through the world’s largest diagnosed osteoarthritis patient population, the highest per-capita healthcare expenditure creating premium therapeutic access, and the robust pharmaceutical R&D investment in DMOAD pipeline development. The United States accounts for approximately 82.5% of North American revenues through Pfizer, Eli Lilly, Sanofi, and AbbVie’s established OA product portfolios and the growing pipeline of investigational DMOADs advancing through FDA clinical development.

Canada contributes supplementary North American revenues through its universal healthcare system’s orthopaedic and rheumatology patient management, the growing geriatric population’s OA prevalence creating consistent prescription procurement, and the private supplementary insurance sector’s coverage of biologics and extended-release injection therapies not fully reimbursed under provincial formularies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Osteoarthritis Therapeutics Market Insights

Europe is a significant osteoarthritis therapeutics market where the EU’s EMA-approved NSAID, corticosteroid, and hyaluronic acid portfolio serves a large ageing population whose approximately 40 million osteoarthritis patients create structured formulary procurement across national healthcare systems. Germany accounts for approximately 22.4% of European revenues through its large pharmaceutical market, comprehensive statutory health insurance reimbursement, and established orthopaedic clinical infrastructure providing both surgical and non-surgical OA management.

France’s large visco supplementation reimbursement framework, the United Kingdom’s NHS osteoarthritis management guidelines creating standardized NSAID and physiotherapy procurement, and Spain and Italy’s large ageing populations with growing OA prevalence collectively sustain European market development. European DMOAD clinical trial activity, where sprifermin’s Phase 2 studies and emerging Wnt pathway modulator programmes have generated significant European data, creates regional pipeline investment sustaining long-term growth potential.

Asia Pacific Osteoarthritis Therapeutics Market Insights

Asia Pacific is the fastest-growing regional osteoarthritis therapeutics market, driven by the world’s largest ageing populations in China and Japan, rapidly increasing obesity prevalence creating accelerating OA incidence, expanding healthcare access through insurance coverage expansion, and growing awareness of OA as a manageable chronic condition beyond its historically accepted status as inevitable age-related joint deterioration. China accounts for approximately 44.8% of Asia Pacific revenues through its enormous and growing OA patient population and expanding prescription pharmaceutical market.

Japan’s advanced orthopaedic medicine infrastructure and high visco supplementation adoption rate, India’s rapidly growing pharmaceutical market and expanding geriatric population, and South Korea’s sophisticated healthcare system’s OA therapeutic prescription collectively sustain Asia Pacific’s fastest-growing regional trajectory. The progressive expansion of biosimilar biological OA therapeutics in Asian markets creates growing cost-effective treatment access that expands the addressable patient population.

MEA & Latin America Osteoarthritis Therapeutics Market Insights

The UAE leads MEA revenues through its advanced healthcare infrastructure, the large expatriate and local population’s OA management needs, and the progressive reimbursement expansion for specialist orthopaedic and injection therapies within its comprehensive health insurance framework. Saudi Arabia’s growing obesity-related OA burden and Vision 2030 healthcare quality investment create expanding therapeutics procurement.

Brazil leads Latin American revenues through its large ageing population’s growing OA prevalence, the SUS public health system’s NSAID and analgesic formulary procurement, and the private health insurance sector’s specialist orthopaedic care and injection therapy coverage. Mexico and Argentina contribute growing secondary demand through their expanding healthcare access and OA patient population growth.

Market Dynamics:

Growth Drivers: Ageing population and obesity epidemic creating expanding OA patient pool and DMOAD pipeline advancing disease-modification beyond symptom management

The osteoarthritis therapeutics market’s most structurally certain growth driver is the demographic and epidemiological confluence of global ageing, whose estimated 2.1 billion people aged over 60 by 2050, and obesity prevalence, whose excessive joint mechanical loading accelerates cartilage degeneration in weight-bearing joints, that collectively creates a compounding annual expansion of the global OA incidence pool. The WHO’s estimate of 528 million current OA patients growing substantially with each demographic ageing cohort creates a non-discretionary healthcare system management burden whose pharmacological treatment procurement grows proportionally with diagnosed patient population. Each new OA diagnosis creates initial NSAID and analgesic prescription, progressive injection therapy engagement, and eventual surgical management whose combined lifetime therapeutic value per patient substantially exceeds most chronic disease management analogues.

The advancing DMOAD clinical pipeline represents the most commercially transformative near-term value creation opportunity in the OA therapeutics market, where each successful Phase 3 DMOAD approval would create an entirely new treatment category addressing the unmet medical need for disease modification that current OA therapeutics addressing only symptom management cannot provide. Sprifermin’s demonstrated cartilage thickness improvement in Phase 2 trials, anacaulase-bcdb’s FDA Breakthrough Therapy designation for knee OA, and the growing number of investigational DMOADs targeting synovial inflammation, bone remodelling, and cartilage matrix synthesis collectively suggest the commercial timeline for first DMOAD approval is approaching.

Restraints: Systemic NSAID toxicity limiting long-term use and regulatory evidence requirements for DMOAD approval creating commercial development barriers

Long-term NSAID use’s gastrointestinal, cardiovascular, and renal toxicity risks create therapeutic management challenges for the chronic OA patient population whose continuous pain management requirements conflict with safety guidelines recommending minimising NSAID exposure duration. The gastrointestinal bleeding risk of non-selective NSAIDs and the cardiovascular risk signal of COX-2 selective inhibitors create prescriber caution that limits NSAID prescription duration below the chronic OA patient’s ongoing analgesic requirement, creating a therapeutic gap between available pharmacological options and long-term pain management need.

Regulatory approval requirements for DMOADs create substantial clinical development barriers, where the FDA’s dual endpoint requirements for both symptom and structural improvement evidence and the long trial durations needed to demonstrate cartilage preservation create clinical development costs exceeding USD 500 million per programme that risk aversion and portfolio economics may constrain. Each DMOAD programme that fails to demonstrate structural modification despite positive symptom improvement endpoints sets an evidence standard whose attainment adds years and hundreds of millions to development timelines.

Opportunities: Regenerative medicine injection therapy commercialization and digital therapeutics integration creating premium OA management value propositions

Regenerative medicine’s progressive clinical validation as an OA therapeutic modality, where platelet-rich plasma’s concentrated growth factor delivery to joint tissues, mesenchymal stem cell injection’s chondrogenic differentiation potential, and autologous chondrocyte implantation’s cartilage defect repair capability collectively represent a continuum of regenerative intervention whose clinical evidence is accumulating through systematic randomized controlled trial investment, creates a premium therapeutic market tier. Each positive RCT establishing statistically significant pain and structural improvement from regenerative injection over conventional corticosteroid or hyaluronic acid creates clinical guideline update momentum that expands reimbursement coverage.

Digital therapeutics integration, where AI-powered pain management applications providing real-time activity pacing guidance, biofeedback-enabled physiotherapy compliance monitoring, and personalized exercise prescription create measurable functional improvement as OA disease management adjuncts, creates a commercial ecosystem surrounding pharmaceutical OA therapeutics whose device-drug combination approaches improve overall patient outcome. Each digital therapeutic CE-marked or FDA-authorized for OA management creates a commercial product expanding the addressable OA market beyond prescription-only pharmaceutical scope.

Recent Developments:

-

2024: Sun Pharmaceutical Industries and Moebius Medical received FDA Fast Track designation for MM-II, a non-opioid intra-articular treatment for knee osteoarthritis pain, enabling rolling NDA review and more frequent FDA consultation during its clinical development programme.

-

2023: Eupraxia Pharmaceuticals received FDA Fast Track designation for EP-104IAR, a long-acting intra-articular corticosteroid formulation for knee osteoarthritis providing sustained anti-inflammatory activity from a single injection over up to six months.

-

2023: Eli Lilly and AbCellera announced a collaboration to develop bispecific antibody therapies targeting osteoarthritis disease modification through novel dual-mechanism approaches addressing both inflammatory and structural OA pathway targets simultaneously.

Osteoarthritis Therapeutics Market Key Players are:

-

Pfizer Inc.

-

Johnson & Johnson (Janssen Pharmaceuticals)

-

Sanofi S.A.

-

Eli Lilly and Company

-

AbbVie Inc.

-

Novartis AG

-

GlaxoSmithKline PLC

-

Anika Therapeutics Inc.

-

Bioventus LLC

-

Eupraxia Pharmaceuticals Inc.

-

Sun Pharmaceutical Industries Ltd.

-

Boehringer Ingelheim GmbH

-

Dr. Reddy’s Laboratories Ltd.

-

Assertio Holdings Inc.

-

Horizon Therapeutics PLC (Amgen)

-

Galapagos NV

-

Merck KGaA (Sprifermin)

-

Pacira BioSciences Inc.

-

Teva Pharmaceutical Industries Ltd.

-

Collegium Pharmaceutical Inc.

Osteoarthritis Therapeutics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.19 Billion |

| Market Size by 2035 | USD 23.1 Billion |

| CAGR | CAGR of 8.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Class (NSAIDs, Corticosteroids, Hyaluronic Acid, Disease-Modifying Osteoarthritis Drugs (DMOADs), Opioids, Others) • By Route of Administration (Oral, Topical, Intra-Articular Injections, Others) • By End User (Hospitals, Orthopaedic Clinics, Rehabilitation Centres, Retail Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Pfizer Inc., Johnson & Johnson (Janssen Pharmaceuticals), Sanofi S.A., Eli Lilly and Company, AbbVie Inc., Novartis AG, GlaxoSmithKline PLC, Anika Therapeutics Inc., Bioventus LLC, Eupraxia Pharmaceuticals Inc., Sun Pharmaceutical Industries Ltd., Boehringer Ingelheim GmbH, Dr. Reddy’s Laboratories Ltd., Assertio Holdings Inc., Horizon Therapeutics PLC (Amgen), Galapagos NV, Merck KGaA (Sprifermin), Pacira BioSciences Inc., Teva Pharmaceutical Industries Ltd., and Collegium Pharmaceutical Inc. |

Frequently Asked Questions

The Osteoarthritis Therapeutics Market is expected to grow at a CAGR of 8.52% from 2026 to 2035.

The Osteoarthritis Therapeutics Market was valued at USD 10.19 Billion in 2025.

The ageing population and obesity epidemic expanding the OA patient pool, advancing DMOAD clinical pipeline targeting disease modification beyond symptom management, and growing intra-articular injection therapy adoption for regenerative medicine applications are the primary growth factors.

NSAIDs dominated the Osteoarthritis Therapeutics Market with the largest share in 2025.

North America dominated the osteoarthritis therapeutics market.

Get in Touch