Patient Temperature Management Market Report Scope & Overview:

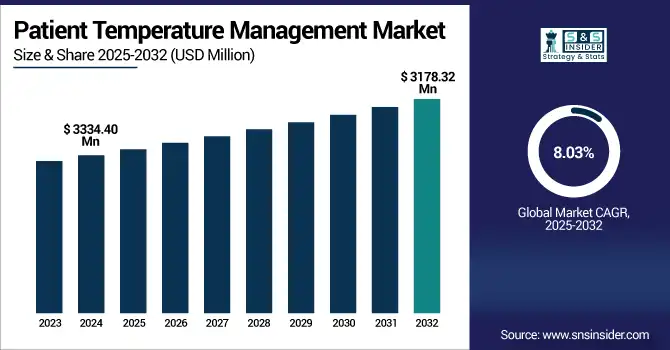

The Patient Temperature Management Market size was valued at USD 3334.40 million in 2024 and is expected to reach USD 3178.32 million by 2032, growing at a CAGR of 8.03% over the forecast period of 2025-2032.

To Get more information on Patient temperature management market - Request Free Sample Report

Technological advancements, changing clinical practices, and rising patient care requirements have led to the growth of the global patient temperature management market. IoT-enabled smart devices, real-time monitoring, and AI are changing the way temperature control is done with predictive analytics and less human error. There is a very strong trend toward non-invasive and minimally invasive solutions that are improving patient comfort and safety. Personalized medicine is also a growth driver here, including systems adapted to the respective needs of specific patients. Novel materials, such as phase change materials (PCMs) enhance thermal stability, and compact and user-friendly apparatuses are extending applications to emergency and transport settings. What’s more, green engineering and changing regulations are also driving manufacturers toward safer and more efficient systems. Combined, these forces are driving the need for accurate, patient-friendly, and scalable temperature management solutions in all healthcare environments globally.

For instance, in April 2025, Frost & Sullivan reported a 28% year-over-year increase in smart temperature management device usage, driven by rising demand for IoT-enabled, real-time monitoring in ICUs and surgical care.

The U.S. Patient Temperature Management Market was valued at USD 1082.67 million in 2024 and is expected to reach USD 1985.58 million by 2032, growing at a CAGR of 7.89% over 2025-2032.

The patient temperature management market is dominated by the U.S., which carries a high burden of cardiovascular diseases, cancer, and diabetes, and patients suffering from these types of diseases may require surgeries and critical care procedures where temperature control is necessary. The increasing number of the aging population and approximately 129-plus million Americans with co-morbidities necessitate constant surveillance and better care options. The growth of chronic disease management programs, propelled by telehealth, digital health, and remote patient monitoring, continues to drive the need for temperature management technologies. Furthermore, the developed infrastructure of the U.S. health care system will facilitate the use of smart, personal devices. With chronic disease driving 90% of the country’s health care costs, hospitals are buying into temperature management systems that cut down on complications, length of stay, and cost. This confluence of clinical necessity, infrastructure preparedness.

For instance, on 29 Feb 2024, an estimated 129 million people in the U.S. have at least 1 major chronic disease.

Patient Temperature Management Market Dynamics:

Drivers:

- Aging Population is Driving the Patient Temperature Management Market Growth

Increasing incidence with an aging population is a major factor for the patient temperature management market across the globe. As human life span becomes longer, older patients will have more surgical, ICU care, and chronic disease treatment, and all of this needs accurate temperature control to prevent complications. The elderly are more susceptible to hypothermia and hyperthermia, and thus, sophisticated temperature management is crucial during surgery. However, the growing population suffering from age-related diseases has further increased the demand for thermal management. Rising healthcare expenditure and policy changes toward care for the elderly is also fueling demand for smart and cost-effective products. Aging workforces at healthcare providers have also created labor shortages, increasing the use of automated temperature systems. In tandem, these demographic changes are driving continued demand and expansion of infrastructure for temperature management technologies within hospitals, long-term care, and home healthcare.

For instance, in January 2025, the American College of Surgeons reported that 76% of major hospital surgeries in 2024 involved patients aged 60+, highlighting increased demand for temperature management to prevent complications.

Restraints:

- Limited Accuracy of Traditional Thermometers is a Significant Restraint on the Patient Temperature Management Market

Poor accuracy of conventional thermometers restricts the patient temperature management market by affecting accurate monitoring in acute care situations. Conventional and infrared thermometers do not provide the same level of detail or accuracy in body temperature, particularly for forehead body temperature readings, which are a crucial factor in surgical, intensive care, and neonatal environments. Accuracy and consistency are further degraded by environmental factors, operator differences, and wear caused by rubbing. Additionally, these devices are dependent on manual interpretation, thus succumbing to human error, loss of data, and delayed clinical intervention. They also need to be frequently calibrated and maintained, but are generally not. Whenever access is blocked, effective patient care is compromised, pointing to the indispensable nature of integrated systems. Traditional devices still hold back the market until solutions and digital and smart answers will become affordable and widespread.

For instance, in November 2024, reported an 18% decline in global market share for traditional thermometers, as healthcare providers shifted toward smart, digital systems offering greater accuracy and integration.

Patient Temperature Management Market Segmentation Insights:

By Product

Patient Warming Systems is the dominant segment in the global Patient Temperature Management Market, with a 70.97% market share in 2024 as they are commonly applied during surgery and the perioperative period for preventing hypothermia and its related complications. These systems, which include forced-air warming blankets, surface warming pads, and conductive warming devices, are regularly employed in the pre-op room, the OR, and the PACU, particularly in general, orthopedic, and cardiac surgeries. Freedom from invasiveness, simplicity, and the ability to guarantee normothermia has seen preference even in hospital facilities and Ambulatory Surgical Centers. Furthermore, more operations being performed, increased awareness of perioperative hypothermia risk, and revised clinical guidelines advocating the use of active warming result in their use. Advanced features in smart and easily accessible warming products extend the applications of patient temperature management products, which supports the leading position of warming products in the overall patient temperature management market.

The Patient Cooling Systems is emerging as the fastest growing segment with a CAGR of 8.36%. motivated by their significant applications in the treatment of cardiac arrest, traumatic brain injury, stroke, and fever, among others. These devices, such as surface cooling pads, intravascular cooling catheters, and auto feedback system, are required to execute targeted temperature management (TTM) protocols, which have been demonstrated to enhance neurological outcomes and survival after hypoxic injury. The rising prevalence of cardiovascular and neurocritical diseases, in combination with the rising number of ICU admissions, is driving the demand. Additionally, there have been improvements in closed-loop cooling and AI-guided therapy for precision cooling and better clinical outcomes. Increasing physician awareness regarding the advantages of therapeutic hypothermia, coupled with supportive clinical guidelines and increasing penetration among emergency and trauma patients, as well as intensive care settings, is expected to fuel the segment growth in the global market.

By Site

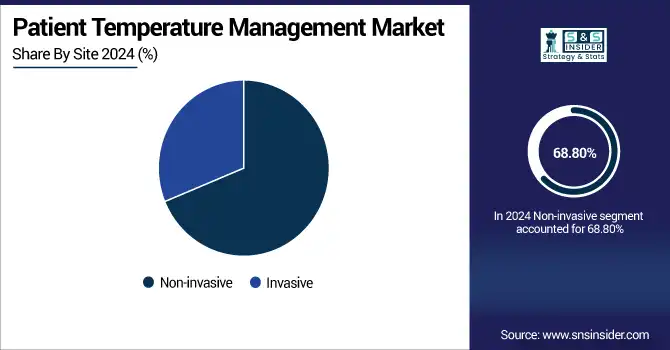

In 2024, the Non-invasive segment dominated the Patient Temperature Management Market trend with a 68.80% market share owing to its easier application, enhancement of the patient's comfort, and lower risk for complications. These systems, including forced-air warming blankets, cooling pads, and wearable sensors, are increasingly becoming the first choice rather than invasive tools, especially in perioperative, emergency department, and neonatal care. A potential pandemic and post-COVID-19 market situation led to an increasing need for minimally invasive and contactless solutions. The technological progress has generated the emergence of mobile, intelligent, and real-time monitors that can be easily implemented into clinical routine. Hence, non-invasive methods are increasingly considered, which significantly drives the patient temperature management market share.

The Invasive segment is the fastest growing aspect of the Patient Temperature Management Market Analysis, especially in emergency and critical care. These systems, which range from intravascular cooling catheters to central temperature control systems, provide accurate and timely control of core body temperature that is critical to delivering precise temperature management to patients in need of hypothermia therapy, following cardiac arrest, or for other neurocritical care conditions. Increasing prevalence of cardiovascular diseases, strokes, and cases of ICU admission are some of the factors supporting the demand for invasive devices, which are more effective as compared to their surface counterparts. In addition, improved closed-loop systems and integration with AI-assisted patient monitoring are improving accuracy and clinical outcomes. With medical bodies giving higher preference to outcome-based technologies over traditional ones, invasive systems are increasingly having an impact on the patient temperature management market share.

By Application

General Surgery has a dominant Patient Temperature Management Market share of 34.70% of the Patient Temperature Management industry in 2024 owing to the large number of patients undergoing surgery globally and the importance of preserving normothermia during surgery. Perioperative hypothermia is a common surgical risk that is associated with complications, such as infection, blood loss, and slower recovery. To avoid these risks, patient warming systems, including forced-air warmers and conductive warming devices, are used extensively in general surgery. Clinical practice guidelines support perioperative active temperature management, providing additional momentum for implementation. Driven by increased numbers of surgical procedures worldwide, and particularly in elderly patients, general surgery remains the largest segment of the patient temperature management market.

Cardiology is emerging as the fastest-growing segment in the Patient Temperature Management Market with the highest CAGR of 8.80% fueled by the increasing prevalence of cardiac arrest, heart surgeries, and cardiovascular diseases. Temperature control is essential in cardiology, in particular in or after cardiac arrest, where targeted temperature management (TTM) might increase neurological function and survival. Intravascular and surface cooling systems are becoming more popular in cardiac ICUs and emergency departments. The increasing knowledge among clinicians, the favorable clinical guidelines, and the progress in automated and closed-loop cooling technologies are contributing to the increase in this procedure. With the increasing prevalence of cardiovascular diseases worldwide, the market for the hospital cardiology segment is projected to grow at a rapid pace in the patient temperature management market.

By End-User

Operating rooms are the largest segment of end users for the Patient Temperature Management industry due to the large number of surgical procedures performed globally, and the necessary need to prevent perioperative hypothermia, which is associated with serious adverse events, including surgical site infections, blood loss, and prolonged recovery. Patient warming devices, including forced-air warming blankets or conductive warming pads, are now common adjuncts in the operating room to help maintain normothermia. Pre-, Intra-, and Post-Operative phase active temperature management is increasingly being required by clinical best practice and hospital protocol. The increasing use of these systems in the operating room environment has contributed immensely to the patient temperature management market growth.

The Neonatal Care segment is witnessing the highest growth in the Patient Temperature Management Market owing to the growing number of preterm and low birth weight neonates, extremely susceptible to thermal instability. Normothermia restoration is an essential goal in all neonatal intensive care units (NICUs) to avoid hypothermia, infections, and impairments in neurodevelopment. High-tech devices for infant warming, incubators, and skin-compatible surface warming devices are widely used to guarantee thermal protection.In addition, rising awareness, enhancement in neonatal care infrastructure, and an increase in investments in maternal and child health care by developing nations drive the demand. All these factors are together driving patient temperature management industry trends in neonatal care.

Patient Temperature Management Market Regional Analysis:

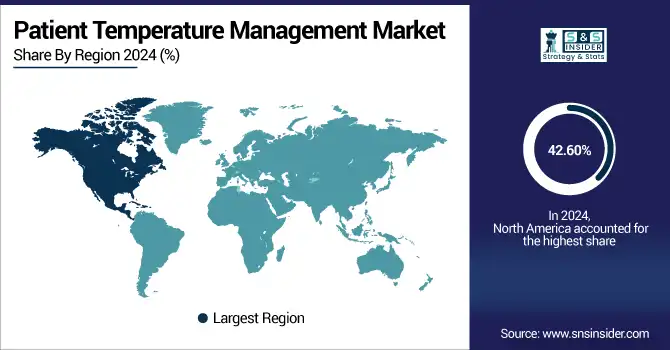

In 2024, the North American region holds the largest market share of the Patient Temperature Management Industry, which is 42.60% market share owing to its advanced healthcare infrastructure, high surgical volume, and strong adoption of innovative medical technologies. The region has a large aging population and a high prevalence of chronic diseases, such as cardiovascular disorders, cancer, and neurological conditions, which require frequent surgeries and intensive care, driving the demand for temperature management systems. Favorable reimbursement policies, strong regulatory frameworks, and the presence of leading market players including 3M, Stryker, and ZOLL further support widespread adoption. Additionally, ongoing investments in digital health, smart monitoring systems, and personalized care contribute to market growth. High awareness among clinicians, along with established clinical guidelines for perioperative normothermia and critical care protocols, positions North America as the leader in the global patient temperature management market.

Europe is the second leading market for the Patient Temperature Management industry due to the high demand for minimally invasive procedures (MIS) owing to its well-established and sophisticated health systems, high standard of clinical care, and high focus on patient safety. The region is witnessing a high number of surgical procedures, especially in countries, such as Germany, France, and the U.K., where perioperative temperature control is mandatory. The increasing number of older persons, and concomitant increased incidence of non-communicable conditions such as cardiovascular and neurological diseases, add to the demand for advanced temperature management, especially in ICUs and surgery departments. Furthermore, a favorable government healthcare scenario, growing hospital infrastructure, and the presence of leading global and regional medical device companies are expected to further boost the demand for medical devices in the country. Growing consciousness in Europe to integrate new non-invasive and green technologies contributes additional impetus to the market for patient temperature management in the region.

Asia Pacific emerges as the fastest-growing region with the highest CAGR of 8.54%. The fastest growth in the patient temperature management market is attributed to the sizeable patient population, rising geriatric population, a growing number of surgical procedures, and the strong focus of prominent players on enhancing their presence in APAC. The growing availability and intensifying demand for both public and private healthcare in countries including China, India, Japan, and South Korea are further spurring the growth of cutting-edge temperature management in hospitals and surgical hospitals. The increasing ageing population and burden of chronic diseases, such as cardiovascular disorders and cancer are increasing the demand for surgical and intensive care, which demands strict thermoregulation.

Moreover, increasing awareness about peri-operative and neonatal temperature management, the government to support patient warming and cooling systems, coupled with increasing medical tourism, would further augment the demand for patient warming and cooling systems. Availability and usage are also being turned around since the region is embracing affordable, non-invasive technologies. These are also driving the Asia-Pacific market to grow fast in the patient temperature management market. Simultaneously, the region’s growing healthcare infrastructure, advanced technology adoption, and higher healthcare demand growth promote its unmatched market growth, making it a notable catalyst for global expansion in the years to come.

The Middle East & Africa are another promising destination in the patient temperature management market, given the improving healthcare infrastructure, hefty investment slated by the hospitals for revamping, and surging awareness among the masses about ultra-modern patient care practices. Surgical volumes and demand for critical care services, including temperature management during surgery, in ICUs and in neonatal units have been increasing in countries, such as the UAE, Saudi Arabia, and South Africa. The entry of global device makers and governments’ efforts on healthcare infrastructure development are helping in the adoption of advanced temperature management techniques. Market penetration is still lower than in developed areas, but an increasingly high prevalence of lifestyle-related diseases and continued expansion of the private health sector are driving demand. Thus, the local patient temperature management market share is growing, which is leading to the region having a high market share in the above-average growth urban areas.

The Patient Temperature Management Market in Latin America has seen promising growth owing to the improved healthcare systems, an increase in surgical procedures, and awareness about perioperative and critical care practices. Countries including Brazil, Mexico, and Argentina have been spending on hospital infrastructure, which in turn drives the adoption of patient warming and cooling systems in operating rooms and ICUs. Cardiovascular diseases and cancer rates are multiplying in the region, while such conditions need temperature management as part of the treatment. In addition, they add that increasing medical tourism and public-private healthcare partnerships are increasing high-tech healthcare. Less mature but strong patient temperature management market growth has been predicted for Latin America in the next few years, as markets rise and hospitals treat more patients with care.

Get Customized Report as per Your Business Requirement - Enquiry Now

Patient Temperature Management Market Key Players:

The Patient Temperature Management companies include 3M Company, Stryker Corporation, Smiths Medical, Cincinnati Sub-Zero (CSZ) Products, LLC., ZOLL Medical Corporation, The Surgical Company Group, Medtronic plc, Becton, Dickinson and Company, Drägerwerk AG & Co. KGaA, Gentherm Medical. and other players.

Recent Developments in the Patient Temperature Management Market:

-

In April 2025, 3M expanded its Bair Hugge warming portfolio with advanced sensors for real-time patient feedback, aiming to improve surgical normothermia outcomes and reduce hypothermia-related complications.

- On 31 March 2025, Medtronic, a global leader in healthcare technology, announced a partnership with Methinks AI, a leading AI-driven radiological triage and notification system provider, to enhance stroke treatment across Central and Eastern Europe, Africa, Türkiye, and the Middle East, supporting its Neurovascular business. Financial terms of the partnership were not disclosed.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3334.40 million |

| Market Size by 2032 | USD 3178.32 billion |

| CAGR | CAGR of 8.03% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | "• By Product (Patient Warming Systems, Patient Cooling Systems) • By Site (Non-invasive, Invasive) • By Application (General Surgery, Cardiology, Pediatrics, Neurology, Orthopedic Surgery) •By End User(Operating rooms, Neonatal Care, ICUs, Emergency room)" |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | 3M Company, Stryker Corporation, Smiths Medical, Cincinnati Sub-Zero (CSZ) Products, LLC., ZOLL Medical Corporation, The Surgical Company Group, Medtronic plc, Becton, Dickinson and Company, Drägerwerk AG & Co. KGaA, Gentherm Medical. |

Frequently Asked Questions

Ans: 3M Company, Stryker Corporation, Smiths Medical, Cincinnati Sub-Zero (CSZ) Products, LLC., ZOLL Medical Corporation, are the leading players in the patient temperature management market.

Ans: The patient temperature management market is segmented as General Surgery, Cardiology, Pediatrics, Neurology, and Orthopedic Surgery by application.

Ans. North America regions dominate the patient temperature management market globally.

Ans: Aging Population is Driving the Patient Temperature Management Market Growth

Ans. The current size of the patient temperature management market is USD 3334.40 million in 2024.

Get in Touch