Polysilicon Reduction Furnace Market Report Scope and Overview:

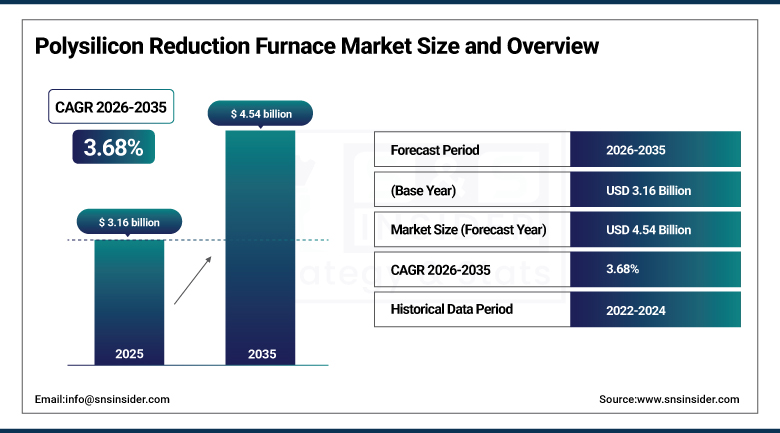

The Polysilicon Reduction Furnace Market Size was valued at USD 3.16 billion in 2025 and is expected to reach USD 4.54 billion by 2035 and grow at a CAGR of 3.68% over the forecast period 2026-2035.

The Polysilicon Reduction Furnace market is witnessing robust growth due to the demand for high-purity polysilicon required in solar photovoltaic as well as semiconductor. With the ever-growing demand for clean energy on a global scale, the application of solar energy has grown rapidly, leading to an increased requirement for efficient high volume polysilicon production. Key equipment in the conversion of metallurgical-grade silicon to solar-grade polysilicon via the Siemens process are reduction furnaces.

Advances in furnace technology are making the systems more efficient and capable of processing larger amounts of material with greater purity at costs that are more enticing for manufacturers. For larger capacity furnaces, there is also an upward shift in economies of scale. With the increasing number of solar productions, capacities in important regions and increased advances in technology will be directed towards more market share in the next few years.

The U.S. raised total tariffs on Chinese solar polysilicon, wafers, and cells to 60%, intensifying trade pressure and prompting uncertainty in solar manufacturing investments. This may boost domestic demand for polysilicon reduction furnaces as the U.S. manufacturers seek to localize production.

Polysilicon Reduction Furnace Market Size and Forecast:

-

Market Size in 2025: USD 3.16 Billion

-

Market Size by 2035: USD 4.54 Billion

-

CAGR: 3.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Polysilicon Reduction Furnace Market - Request Free Sample Report

Polysilicon Reduction Furnace Market Highlights:

-

Energy efficiency innovation in Siemens polysilicon reduction furnaces is gaining traction, with advanced AC-based heating models improving temperature uniformity, lowering power consumption, and enhancing silicon rod quality.

-

Technology-driven furnace optimization is becoming a key cost-reduction lever for polysilicon producers as electricity remains the largest operating expense in the Siemens process.

-

New polysilicon production capacity in Oman signals geographic diversification of the global polysilicon supply chain beyond China, Europe, and the U.S.

-

Middle East entry into polysilicon manufacturing leverages access to low-cost energy, port infrastructure, and export-oriented free zones, strengthening regional competitiveness.

-

Large-scale greenfield investments highlight rising long-term demand expectations from solar PV and energy transition markets.

-

Integrated furnace, hydrogen, and process equipment deployment underscores growing demand for advanced reduction furnace systems in new polysilicon facilities.

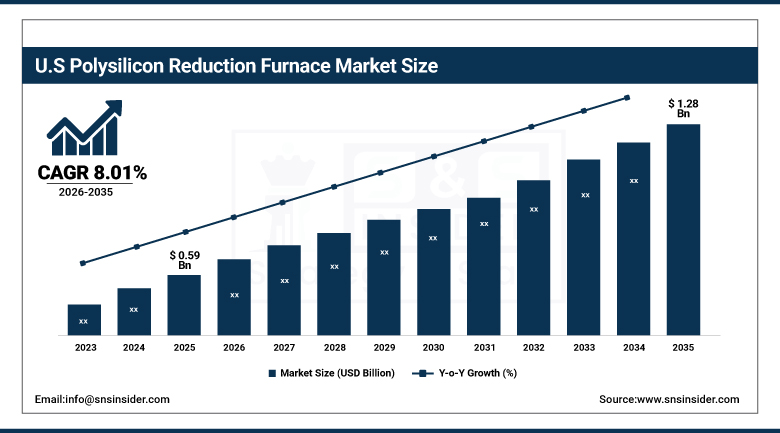

The U.S. Polysilicon Reduction Furnace Market size was USD 0.59 billion in 2025 and is expected to reach USD 1.28 billion by 2035, growing at a CAGR of 8.01 % over the forecast period of 2026–2035.on the basis of the increasing production of domestic polysilicon, increasing installation of solar and advancement in furnace technology with manufacturer focusing in the development of high-capacity, energy-efficient systems to support the growing demand for clean energy.

Polysilicon Reduction Furnace Market Drivers:

-

Growing Solar Energy Demand Drives Expansion of Polysilicon Reduction Furnace Market

The increasing global shift toward renewable energy is significantly driving the high purity polysilicon market, a key component required for the production of solar PV. With focus on securing the energy security and reducing dependence on imports the local polysilicon production in an energy efficient way is increasingly demanded. This is driving investment in advanced reduction furnace technologies, which deliver a greater throughput, lower energy intensity and product purity. Furthermore, the increasing cost effectiveness of solar power and enlargement of utility-scale solar parks are generating sustained demand for high-volume polysilicon production. Therefore, the expansion in production capacity by manufacturers is thereby propelling the market for polysilicon reduction furnace in such regions such as North America and Asia.

OCI Holdings' stock surged nearly 10% after the U.S. exempted solar-grade polysilicon from new tariffs, boosting investor confidence in its expanding U.S. solar operations.

Polysilicon Reduction Furnace Market Restraints:

-

High Capital Investment Restricts Market Entry and Slows Growth

The Polysilicon Reduction Furnace market faces significant challenges due to the high capital investment required for purchasing and installing advanced furnace systems. These costs, combined with substantial operational and maintenance expenses, create financial barriers, especially for small and medium-sized manufacturers. As a result, many potential entrants may hesitate to invest, limiting competition and innovation within the market. Furthermore, the high costs can slow the adoption of newer, more efficient technologies, impacting overall industry growth. This financial burden can also lead existing players to prioritize cost-cutting over technological upgrades, potentially affecting product quality and efficiency. Therefore, the heavy investment demand acts as a key restraint, slowing market expansion and limiting the widespread deployment of polysilicon reduction furnace technologies.

Polysilicon Reduction Furnace Market Opportunities:

-

Technological Advancements Increase Efficiency and Drive Market Growth

The Polysilicon Reduction Furnace market is poised for significant growth due to active development of new generation treatment technologies for semiconductors, especially SiC power ones. Productivity-improving solutions such as improved batch processing and parallel wafer handling will help streamline manufacturing and lower costs of operation. These enhancements will help to meet the growing need for high-purity polysilicon in solar photovoltaic and semiconductor applications. Moreover, Electric vehicles and renewable energy solutions adoption, which is still in progress, would provide growth opportunity to the market. As the focus on sustainability and energy-efficient systems continues to intensify, there is a significant opportunity for manufacturers to develop advanced systems that are more advanced and geared to satisfy new industry requirements and regulations, driving strong Polysilicon Reduction Furnace market growth.

JTEKT Thermo Systems developed new heat treatment equipment for SiC power semiconductors, boosting productivity by 25% with advanced batch processing and parallel wafer handling

Polysilicon Reduction Furnace Market Segment Analysis:

By Type

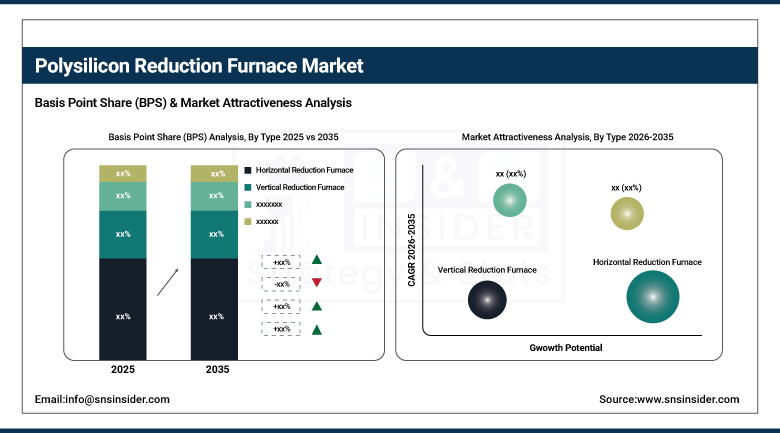

The Horizontal Reduction Furnace segment held a dominant Polysilicon Reduction Furnace Market share of around 66% in 2025, and expected to be the fastest growing over the forecast period of 2026-2035 with CAGR 7.44%, Continuous technology innovation, and growing requirement of high purity polysilicon in solar and semiconductor industry, this Polysilicon Reduction Furnace Industry will remain in leading position in market development as well as in meeting future industry demand.

By Capacity

The Large segment held a dominant Polysilicon Reduction Furnace Market share of around 41% in 2025, and expected to be the fastest growing over the forecast period of 2026-2035 with CAGR 8.34%. This growth is attributed to the demand for high-capacity and high-efficiency furnaces in the solar and semiconductor industry. Furthermore, technological innovations in furnaces and the requirement for high volume production in response to growing demand for polysilicon, are offering substantial growth to this segment during the forecast period.

By Application

The Solar Photovoltaic segment held a dominant Polysilicon Reduction Furnace Market share of around 71% in 2025, and expected to be the fastest growing over the forecast period 2026-2035 with CAGR 8.08%. This market’s expansion is propelled by the growing worldwide use of the renewable energy, surge in solar panels installations, and governments' initiatives for clean power. Rising requirement for ultra-pure polysilicon to improve solar cell efficiency is another factor driving the segment growth.

By End User

The Solar Industry segment held a dominant Polysilicon Reduction Furnace Market share of around 76% in 2025, and expected to be the fastest growing over the forecast period 2026-2035 with CAGR 8.03%. This expansion is largely fueled by the international surge in clean energy activity, solar power installations, and investment in solar infrastructure. High-efficiency solar panels are driving the demand for such high purity polysilicon, and underpinning the indefinite growth of the market.

Polysilicon Reduction Furnace Market Regional Analysis:

Asia-Pacific Polysilicon Reduction Furnace Market Trends:

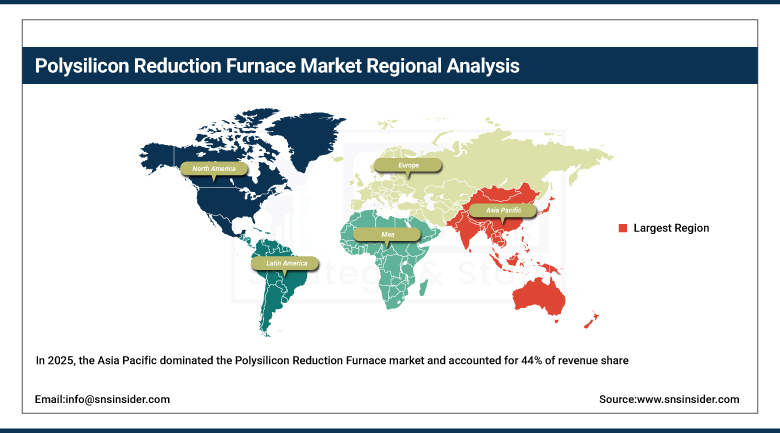

In 2025, the Asia Pacific dominated the Polysilicon Reduction Furnace market and accounted for 44% of revenue share, due to its rapid industrialization, presence of solar equipment manufacturers, growing renewable energy investments and government support. However, China and other countries including Japan and South Korea, are continuing to be the main driver in demand for high-purity polysilicon for use in solar and semiconductor applications.

China’s dominance in the Asia Pacific Polysilicon Reduction Furnace market, driven by its vast manufacturing capacity, strong solar industry growth, and government support for renewable energy expansion.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Polysilicon Reduction Furnace Market Trends:

North America is projected to register the significant growth for CAGR of 9.06% during 2026-2035, owing to increasing investments toward domestic solar manufacturing, favorable government initiatives, and attempts to limit reliance on overseas made solar products. Proliferating need for clean energy and developments in the technology of furnace systems further boost the market growth.

The U.S. leads the Polysilicon Reduction Furnace market, due to strong solar manufacturing initiatives, favorable federal policies, and increased demand for high-purity polysilicon in renewable energy and semiconductor applications.

Europe Polysilicon Reduction Furnace Market Trends:

In 2025, Europe emerged as a promising region in the Polysilicon Reduction Furnace, owing to strong adherence to clean energy transitions, increasing demand for the photovoltaic technologies along with strict regulations associated with the environment. With government subsidies and policies on low-carbon economy, polysilicon production of high purity and local polysilicon will command a growing market demand.

Latin America and Middle East & Africa Polysilicon Reduction Furnace Market Trends:

LATAM and MEA is experiencing steady growth in the Polysilicon Reduction Furnace market, due to rising demand for solar energy, favorable climatic conditions for solar power and strengthening government support for deployment of renewable energy projects. Growing infrastructure and foreign investments in clean energy and Polysilicon manufacturing equipment are further propelling the demand for polysilicon production technologies in the regions.

Polysilicon Reduction Furnace Market Competitive Landscape:

Hemlock Semiconductor Corporation (established in 1961) is a leading U.S.-based producer of high-purity polysilicon for semiconductor and solar applications. The company specializes in advanced Siemens reduction furnace technology, delivering ultra-clean, energy-efficient polysilicon with strong focus on process innovation, quality control, and sustainable manufacturing practices.

- In October 2024, Hemlock Semiconductor received USD325 million from the Biden administration to build a new Michigan factory, creating 180 manufacturing jobs. This investment supports U.S. semiconductor production under the CHIPS Act and strengthens the domestic supply chain.

Tokuyama Corporation (established in 1918) is a Japan-based chemical manufacturer and a key producer of high-purity polysilicon for semiconductor and solar applications. The company leverages advanced Siemens reduction furnace processes, focusing on product purity, energy-efficient operations, and continuous technological innovation to support global electronics and photovoltaic supply chains.

- In August 2024, Tokuyama plans to build a USD30 million polysilicon factory in Vietnam's Ba Ria-Vung Tau province to produce semiconductor-grade polysilicon. The move supports its expanding production capacity alongside its Malaysia partnership with OCI.

Polysilicon Reduction Furnace Market Key Players:

-

GCL-Poly Energy Holdings Ltd.

-

Wacker Chemie AG

-

OCI Company Ltd.

-

Hemlock Semiconductor Corporation

-

REC Silicon ASA

-

Tokuyama Corporation

-

Daqo New Energy Corp.

-

Mitsubishi Materials Corporation

-

LDK Solar Co., Ltd.

-

SunEdison, Inc.

-

Sichuan Yongxiang Co., Ltd.

-

TBEA Co., Ltd.

-

Asia Silicon (Qinghai) Co., Ltd.

-

Zhonghuan Semiconductor Co., Ltd.

-

KCC Corporation

-

Hanwha Solutions Corporation

-

Jiangsu Zhongneng Polysilicon Technology Development Co., Ltd.

-

Huanghe Hydropower Development Co., Ltd.

-

Xinjiang East Hope Nonferrous Metals Co., Ltd.

-

Xinte Energy Co., Ltd.

| Report Attributes | Details |

| Market Size in 2025 | USD 3.16 Billion |

| Market Size by 2035 | USD 4.54 Billion |

| CAGR | CAGR of 3.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Horizontal Reduction Furnace, Vertical Reduction Furnace) • By Capacity (Small, Medium, Large) • By Application (Solar Photovoltaic, Electronics, Others) • By End-User (Solar Industry, Semiconductor Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GCL-Poly Energy Holdings Ltd., Wacker Chemie AG, OCI Company Ltd., Hemlock Semiconductor Corporation, REC Silicon ASA, Tokuyama Corporation, Daqo New Energy Corp., Mitsubishi Materials Corporation, LDK Solar Co., Ltd., SunEdison, Inc., Sichuan Yongxiang Co., Ltd., TBEA Co., Ltd., Asia Silicon (Qinghai) Co., Ltd., Zhonghuan Semiconductor Co., Ltd., KCC Corporation, Hanwha Solutions Corporation, Jiangsu Zhongneng Polysilicon Technology Development Co., Ltd., Huanghe Hydropower Development Co., Ltd., Xinjiang East Hope Nonferrous Metals Co., Ltd., and Xinte Energy Co., Ltd. |

Frequently Asked Questions

Asia-Pacific dominated the Polysilicon Reduction Furnace Market in 2025.

The “Horizontal Reduction Furnace” segment dominated the Polysilicon Reduction Furnace Market.

Key drivers of the Polysilicon Reduction Furnace Market include rising demand for solar energy, increasing semiconductor manufacturing, and advancements in furnace technology.

The Polysilicon Reduction Furnace Market Size was valued at USD 3.16 billion in 2025 and is expected to reach USD 4.54 billion by 2035

The Polysilicon Reduction Furnace Market is expected to grow at a CAGR of 7.38% during 2026-2035.

Get in Touch