Power Sport Vehicle Tire Market Report Scope & Overview:

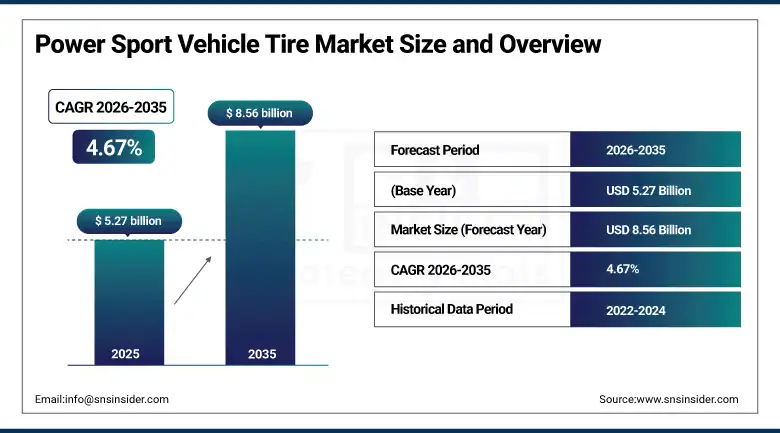

The Power Sport Vehicle Tire Market was valued at USD 5.27 Billion in 2025 and is expected to reach USD 8.56 Billion by 2035, growing at a CAGR of 4.67% from 2026–2035.

Power sport vehicle tires are purpose-engineered rubber products designed for the specific performance, terrain, and safety demands of recreational and utility vehicles operating outside conventional road environments. These vehicles include motorcycles used in competitive racing and road sport, all-terrain vehicles navigating mixed trail and track conditions, side-by-side utility terrain vehicles serving both recreation and work applications, snowmobiles traversing packed and powder snow terrain, and a growing range of electric-powered recreational vehicles whose different weight distribution and torque delivery characteristics create evolving tire specification needs. Each vehicle category imposes fundamentally different requirements on tire tread pattern, compound hardness, sidewall stiffness, and load rating that conventional passenger car and light truck tires cannot satisfy.

Global power sport vehicle registrations reached approximately 18 million units annually in 2024, with North America and Europe accounting for the majority of high-value segments including UTVs and performance motorcycles. Each registered power sport vehicle generates recurring aftermarket tire demand through wear replacement cycles that average 12 to 24 months depending on vehicle type, usage intensity, and terrain characteristics.

Market Size and Forecast

-

Market Size in 2026E: USD 5.52 Billion

-

Market Size by 2035: USD 8.56 Billion

-

CAGR: 4.67% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Power Sport Vehicle Tire Market - Request Free Sample Report

Power Sport Vehicle Tire Market Trends

-

Rising electric power sport vehicle adoption is driving demand for EV-specific tire technologies.

-

Growing consumer preference for high-performance tires is increasing adoption of advanced tread and compound technologies.

-

Radial tire adoption is accelerating due to improved ride quality, durability, and fuel efficiency benefits.

-

Expanding vehicle customization trends are boosting aftermarket replacement tire demand.

-

Online retail and direct-to-consumer sales channels are increasing accessibility to specialized power sport tires.

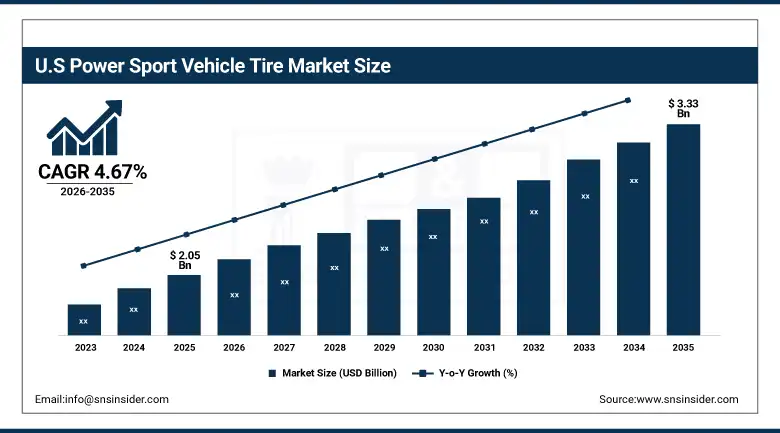

The U.S. Power Sport Vehicle Tire Market Outlook

The U.S. Power Sport Vehicle Tire Market was valued at approximately USD 2.05 Billion in 2025 and is expected to reach approximately USD 3.33 Billion by 2035, growing at a CAGR of 4.67%.

The United States is the world's largest and most commercially developed power sport vehicle tire market, reflecting the country's extraordinary recreational vehicle culture, the highest per-capita power sport vehicle ownership rate globally, and an aftermarket ecosystem of specialist retailers, online platforms, and performance tire brands that caters to the most demanding enthusiast consumer segment in any global market. American consumers are among the most active participants in ATV trail riding, UTV utility and recreation, motocross and enduro racing, snowmobile touring and competition, and street motorcycle sport and touring whose combined tire consumption is the foundation of the U.S. market's commercial scale.

U.S. public land access policy, trail network expansion through federal and state recreation programmes, and the growing popularity of adventure motorcycle touring on mixed-surface routes are all sustaining the riding activity volumes that generate aftermarket tire replacement demand. The U.S. power sport aftermarket is served by specialist retailers including Rocky Mountain ATV/MC, BikeBandit, and MotoSport whose online platforms carry thousands of tire SKUs covering every vehicle type and terrain specification. Michelin, Bridgestone, Dunlop, and Maxxis each maintain U.S.-focused product lines developed through collaboration with American motorsport programmes that validate tire performance in the terrain conditions that U.S. riders encounter most frequently.

The U.S. Consumer Product Safety Commission reported that ATV usage continued to grow across all age demographics in 2024, with side-by-side UTVs showing the fastest registration growth among all power sport vehicle categories. This ongoing fleet expansion creates the new vehicle tire demand and subsequent aftermarket replacement cycle that sustains consistent U.S. power sport tire market revenue growth.

Power Sport Vehicle Tire Market Segment Analysis

-

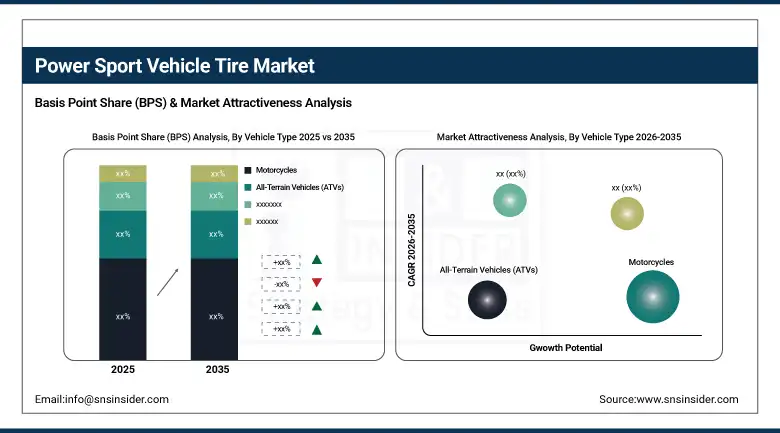

By Vehicle Type, motorcycles dominated the market with approximately 38% share in 2025. ATVs and UTVs are the fastest-growing segment with a CAGR of around 7.20% through the forecast period.

-

By Tire Construction, bias tires held the dominant market share of nearly 57% in 2025. Radial tires are projected to be the fastest-growing construction type with a CAGR of approximately 7.80%.

-

By Application, Off-Road tires accounted for the largest market share of about 42% in 2025. Dual-Purpose tires are the fastest-growing application segment with a CAGR of nearly 8.10%.

-

By End User, aftermarket dominated the market with an estimated share of around 64% in 2025. Online Retail is the fastest-growing distribution channel with a CAGR of approximately 8.60% through the forecast period.

By Vehicle Type, motorcycles dominate, ATVs and UTVs grow fastest

Motorcycles held approximately 38% of the Power Sport Vehicle Tire Market in 2025. This dominance reflects the global scale of motorcycle ownership across sport, touring, adventure, and off-road categories whose combined installed base dwarfs every other power sport vehicle segment by unit count. Street motorcycle tire demand spans a spectrum from high-performance sport tires for track day and sport riding applications through long-mileage touring compounds for loaded touring riders through adventure tires designed for mixed on-road and gravel use on the growing adventure touring motorcycle category. Off-road motorcycle tire demand from motocross, enduro, hard enduro, and trail riding communities sustains specialty tire segments requiring terrain-specific tread patterns that vary more dramatically than those of any other power sport vehicle category.

ATVs and UTVs are the fastest-growing vehicle type segment within the Power Sport Vehicle Tire Market. The side-by-side UTV category has been the power sport industry's strongest growth segment for several years, driven by their combination of recreational capability, practical utility, and family-use versatility that expands the buyer demographic beyond traditional single-rider ATV consumers. UTVs typically use larger, wider tires with higher load ratings than ATVs, creating higher per-vehicle tire revenue. The commercial and agricultural utility applications for UTVs on farms, ranches, and industrial sites create a second buyer demographic whose tire replacement decisions are driven by operational durability requirements rather than performance preference, sustaining consistent demand through economic cycles that might slow pure recreational purchasing.

By Tire Construction, bias tires dominate, radial tires grow fastest

Bias tires held the dominant position in the Power Sport Vehicle Tire Market in 2025. Bias-ply construction, in which the tyre cord layers cross each other at angles to the direction of travel, has historically dominated power sport tire categories through its inherent advantages in sidewall stiffness and impact resistance that benefit off-road applications where rock strikes, root impacts, and sharp edge encounters are routine. Bias construction provides the firm sidewall that resists deformation under the lateral loads of aggressive cornering in off-road terrain. Its lower production cost relative to radial construction makes it commercially preferred for entry-level and utility power sport vehicle categories whose buyers prioritize replacement cost over maximum performance. The large installed base of power sport vehicles specified with bias tires at OEM level sustains aftermarket demand for bias-ply replacement products throughout the vehicle service life.

Radial tires are the fastest-growing construction type in power sport applications, driven by growing rider awareness of their performance advantages and the progressive migration of premium power sport vehicle OEM specifications toward radial fitment. Radial construction, in which cord layers run perpendicular to the direction of travel, separates the sidewall flexibility from the tread stiffness, enabling a firmer, more consistent tread contact patch with the road or trail surface while maintaining sidewall compliance that absorbs terrain irregularities. This construction advantage delivers superior grip, more predictable handling, better heat dissipation at high speeds, and improved mileage relative to bias alternatives in applications where these performance dimensions are commercially valued by the rider.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.7% |

|

Europe |

Germany |

27.4% |

|

Asia Pacific |

China |

37.8% |

|

Middle East & Africa |

South Africa |

28.6% |

|

Latin America |

Brazil |

42.4% |

North America Power Sport Vehicle Tire Market Insights

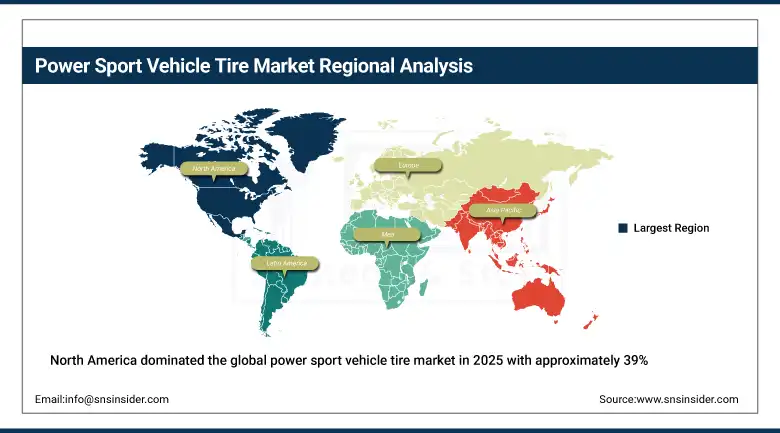

North America dominated the global power sport vehicle tire market in 2025 with approximately 39% of global revenues. The United States accounts for approximately 83.7% of North American revenues as the world's highest per-capita power sport vehicle ownership market. The combination of extensive public trail networks, vast off-road accessible public land, strong recreational vehicle culture, and high disposable income creates the most commercially significant power sport tire market globally. American consumers invest more in premium performance tire upgrades than consumers in any other market, sustaining above-average revenue per vehicle in the aftermarket replacement segment. Canada is the second most significant North American market through its snowmobile and ATV trail riding culture across its vast forested and tundra regions.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. power sport aftermarket is served by a highly developed ecosystem of specialist retailers, online platforms, and performance tire brands. Rocky Mountain ATV/MC, BikeBandit, Revzilla, and Cycle Gear collectively serve millions of American power sport consumers through their extensive product catalogues and customer service infrastructure. This retail ecosystem enables American riders to access a wider selection of performance tire options than consumers in most other markets, sustaining above-average premium tire adoption and driving overall market revenue above what installed base size alone would suggest.

Europe Power Sport Vehicle Tire Market Insights

Europe is a large and technically sophisticated power sport vehicle tire market with strong motorcycle and adventure riding cultures in Germany, France, Italy, the United Kingdom, Austria, and Switzerland. Germany accounts for approximately 27.4% of European revenues through its combination of one of the EU's largest motorcycle rider populations, an active motorsport culture, and the presence of major tire manufacturers including Continental and Metzeler whose performance-oriented product ranges drive above-average market values. European adventure motorcycle culture, driven by the popularity of BMW GS, KTM Adventure, and Ducati Multistrada platforms, sustains strong demand for dual-purpose tires combining road performance with gravel and light trail capability.

European power sport tire demand benefits from the continent's extensive motorsport competition calendar across motocross, enduro, road racing, and track day events that collectively sustain enthusiast engagement with performance tire products. EU environmental regulations on tire rolling resistance and wet grip performance are creating technical development pressure on European power sport tire manufacturers to maintain performance standards while meeting sustainability metrics that are progressively incorporated into mandatory tire labelling requirements.

Asia Pacific Power Sport Vehicle Tire Market Insights

Asia Pacific is the fastest-growing power sport vehicle tire market through rapidly rising disposable incomes, growing recreational vehicle adoption among middle-class consumers, and the expansion of motorsport participation across the region. China accounts for approximately 37.8% of Asia Pacific revenues through its large domestic motorcycle market and growing ATV and UTV sector. India is the world's largest motorcycle market by unit volume and a significant growing power sport tire market as consumer migration from basic commuter motorcycles toward higher-performance sport and adventure platforms creates above-average per-unit tire value growth. Japan, South Korea, Australia, and Southeast Asia each represent significant and growing power sport tire markets with above-average premium tire adoption rates relative to their overall vehicle fleet sizes.

MEA & Latin America Power Sport Vehicle Tire Market Insights

Middle East and Africa and Latin America are growing power sport vehicle tire markets where recreational vehicle adoption, desert and trail riding culture, and motorsport participation are creating increasing tire demand. South Africa leads MEA revenues at approximately 28.6% of the regional share through its active trail riding and adventure motorcycle community whose diverse terrain from Karoo desert to mountain tracks sustains demand for performance dual-purpose tire products. Brazil leads Latin American revenues at approximately 42.4% through its large domestic motorcycle market, growing ATV and UTV sector, and active motocross and enduro competition calendar that sustains premium performance tire demand among the competitive rider community.

Market Dynamics

Growth Drivers: Rising participation in outdoor recreational activities, growing power sport vehicle fleet size.

Outdoor recreation participation has reached record levels in North America and Europe following the pandemic period when confined consumers discovered or rediscovered trail riding, adventure touring, and off-road vehicle recreation as socially distanced outdoor activities. This participation surge translated into power sport vehicle sales records across ATV, UTV, snowmobile, and adventure motorcycle categories that have expanded the installed fleet size generating aftermarket tire replacement demand. The consumers who entered power sport activities during this period represent a cohort with above-average engagement depth whose continued participation sustains ongoing tire purchases.

Vehicle personalization and performance upgrade culture is driving premium tier tire adoption that lifts average market revenue per replacement occasion above basic functional replacement levels. Social media content from influential riders, professional racer endorsements, and online community discourse around tire performance create commercial pressure on enthusiast consumers to invest in premium aftermarket products that enhance their riding experience beyond what manufacturer-standard OEM tires deliver. This aspiration-driven purchasing pattern is most commercially significant in North America but is progressively emerging in European and Asia Pacific enthusiast communities whose engagement with power sport content has been amplified by global platform access.

Restraints: High tire cost relative to average power sport vehicle rider budgets, safety concerns limiting new participant growth in certain markets

Premium power sport tire pricing creates a commercial adoption barrier among the large segment of riders whose vehicle values and usage frequency do not justify investment in high-performance replacement products. A premium set of ATV performance tires can cost USD 400 to USD 800 or more fully mounted, a significant expenditure relative to the total value of a recreational ATV purchased used or in an entry-level configuration. Price-sensitive consumers default to the most affordable replacement options available, reducing the premium tier capture rate that limits overall market revenue growth relative to what installed fleet size alone would support.

Seasonal demand patterns create operational challenges for power sport tire retailers and distributors. Snowmobile tire demand is concentrated in autumn and early winter months. ATV and UTV peak demand follows spring trail opening and summer riding season patterns. Motorcycle tire demand is strongest in late spring through early autumn in temperate climates. These seasonal patterns create inventory forecasting challenges, working capital intensity during pre-season stocking periods, and revenue concentration risk for retailers without sufficient product category diversification to smooth annual demand curves.

Opportunities: Electric power sport vehicle tire development creating a premium new technology segment.

Electric power sport vehicles are creating a new and commercially premium tire development opportunity. EV-specific tire requirements differ from internal combustion vehicle specifications in ways that create both technical challenge and commercial differentiation opportunity for tire manufacturers who invest in EV-optimized product development. The instant torque delivery of electric motors creates higher traction demands at vehicle launch that require compound and construction adjustments beyond simply fitting conventional tires. Regenerative braking creates different wear patterns on front and rear tires. Heavier battery weight requires higher load ratings than equivalent conventional vehicles. Each of these EV-specific characteristics creates specification differentiation that supports premium pricing for purpose-developed products. Adventure tourism growth is creating sustained demand for dual-purpose and adventure touring motorcycle tires whose technical specifications balance on-road mileage with off-road traction in ways that neither purely road nor purely off-road tires achieve. The global adventure touring motorcycle market has been the motorcycle industry's fastest-growing segment for several years, driven by social media travel content, organized adventure touring events, and the commercial success of large displacement adventure platforms from BMW, KTM, Honda, and Triumph.

Recent Developments:

-

2025: Michelin launched its new Anakee Ultra adventure tire specifically designed for heavy adventure touring motorcycles, incorporating sipe patterns optimized for mixed gravel and paved road conditions that adventure riders encounter on extended touring itineraries.

-

2025: Maxxis introduced its new RAZR series UTV performance tire line targeting the growing side-by-side recreational segment with improved puncture resistance and self-cleaning tread patterns validated in desert, mud, and rock terrain testing programmes.

-

2025: Bridgestone expanded its Battlax adventure motorcycle tire range with new sizes covering the growing mid-displacement adventure segment, addressing rider demand for performance-oriented dual-purpose tires for smaller and lighter adventure platforms.

Power Sport Vehicle Tire Market Key Players are:

-

Michelin Group

-

Bridgestone Corporation

-

Continental AG

-

Pirelli & C. S.p.A.

-

Dunlop (Sumitomo Rubber Industries)

-

Metzeler (Pirelli)

-

Maxxis International

-

Kenda Rubber Industrial Co. Ltd.

-

IRC Tire (Inoue Rubber Co. Ltd.)

-

Mitas (Trelleborg Wheel Systems)

-

Shinko Tires (Zenith Rubber)

-

Cheng Shin Rubber Industry Co. Ltd.

-

Avon Tyres (Cooper Tire)

-

CST Tires (Cheng Shin)

-

Duro Tire (Duro International)

-

Kuhmo Tire

-

BKT Tires

-

Goldentyre

-

Camso (Michelin)

-

Sedona Tire & Wheel

Power Sport Vehicle Tire Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.27 Billion |

| Market Size by 2035 | USD 8.56 Billion |

| CAGR | CAGR of 4.67% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Vehicle Type (Motorcycles, All-Terrain Vehicles (ATVs), Utility Terrain Vehicles (UTVs), Snowmobiles, Others) •By Tire Construction (Radial Tires, Bias Tires) •By Application (On-Road, Off-Road, Dual-Purpose) •By End User (OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Michelin Group, Bridgestone Corporation, Continental AG, Pirelli & C. S.p.A., Dunlop (Sumitomo Rubber Industries), Metzeler (Pirelli), Maxxis International, Kenda Rubber Industrial Co. Ltd., IRC Tire (Inoue Rubber Co. Ltd.), Mitas (Trelleborg Wheel Systems), Shinko Tires (Zenith Rubber), Cheng Shin Rubber Industry Co. Ltd., Avon Tyres (Cooper Tire), CST Tires (Cheng Shin), Duro Tire (Duro International), Kuhmo Tire, BKT Tires, Goldentyre, Camso (Michelin), Sedona Tire & Wheel |

Frequently Asked Questions

North America dominated the Power Sport Vehicle Tire Market in 2025 with approximately 39% of global revenues.

Motorcycles dominated with approximately 38% of revenues in 2025.

Rising participation in outdoor recreational activities and growing power sport vehicle fleet size are the primary drivers. Premium tire upgrade demand from performance-oriented consumers is lifting average market revenue per replacement occasion above basic functional replacement levels.

The Power Sport Vehicle Tire Market was valued at USD 5.27 Billion in 2025.

The Power Sport Vehicle Tire Market is expected to grow at a CAGR of 4.67% from 2026 to 2035.

Get in Touch