Precipitated Calcium Carbonate Market Report Scope & Overview:

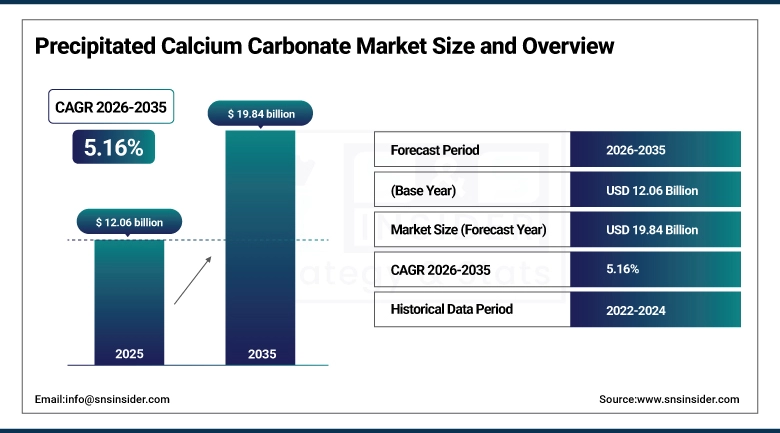

The Precipitated Calcium Carbonate Market was valued at USD 12.06 Billion in 2025 and is expected to reach USD 19.84 Billion by 2035, growing at a CAGR of 5.16% from 2026-2035.

The Precipitated Calcium Carbonate (PCC) market is witnessing substantial growth due to increased demand for fillers and additives in the paper & pulp industry, plastic industry, paint & coatings industry, and pharmaceuticals sector. The major drivers behind growth include increasing demand for light, economical, and sustainable products; improved printing quality and whiteness in paper; improved performance characteristics in the plastic industry; and the increasing application of PCC as an excipient and food additive in pharmaceuticals. Increasing development in terms of nano PCC and treated surface PCC technology is creating opportunities in the coating, packaging, and polymer market segments.

In line with this trend, the European Union Green Deal envisions an ambitious carbon-neutral agenda by 2050, promoting the use of CO₂ capture and utilization technology in manufacturing PCC. Such initiatives are fast-tracking the transition to sustainable fillers for paper, plastic, and coating applications.

The U.S. Environmental Protection Agency (EPA) has updated its guidance on sustainable industrial minerals and recommended PCC as a viable replacement for talc and kaolin.

Precipitated Calcium Carbonate Market Size and Forecast

-

Market Size in 2025: USD 12.06 Billion

-

Market Size by 2035: USD 19.84 Billion

-

CAGR: 5.16% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Precipitated Calcium Carbonate Market - Request Free Sample Report

Precipitated Calcium Carbonate Market Trends

-

Adoption of CO₂ recovery is increasing amid government pressure on industries to achieve carbon neutrality.

-

Nano PCC applications are increasing in pharmaceuticals, food additives, and coating applications.

-

The paper industry's resurgence is increasing PCC consumption in recycled and specialty papers for their opacity and printability.

-

The plastics industry's growth is fueling demand for PCC in lightweight vehicles and consumer products.

-

Eco-friendly coatings are spurring demand for surface-treated PCC in paints and coatings.

-

Applications in the pharma industry are increasing using PCC as excipients, antacids, and nutritional supplements.

-

Applications of food-grade PCC are increasing through fortification and additive applications.

-

Applications of cosmetic-grade PCC are increasing through personal care and beauty applications.

-

The carbonation process remains dominant in PCC production due to efficiency and sustainability.

-

The surface treatment of PCC is a promising niche for specialty polymers and coatings.

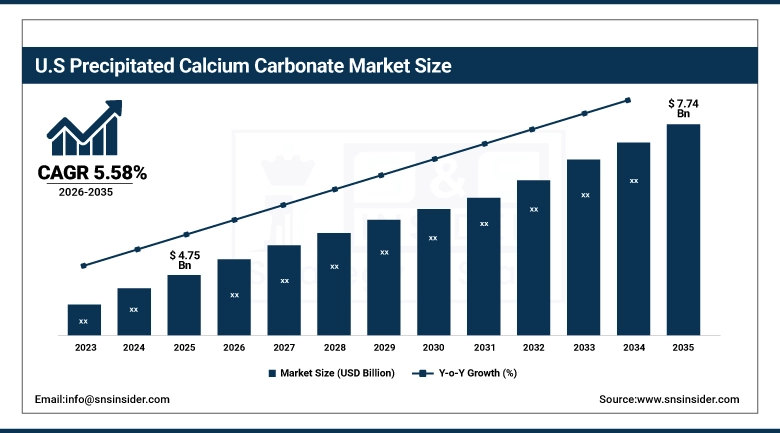

U.S. Precipitated Calcium Carbonate Market was valued at USD 4.75 billion in 2025 and is expected to reach USD 7.74 billion by 2035, growing at a CAGR of 5.58% from 2026-2035.

The United States Precipitated Calcium Carbonate (PCC) Market is considered one of the largest markets globally, based on its sophisticated industrial foundation, robust manufacturing facilities, and presence of major players like Omya, Imerys, Minerals Technologies, and Mississippi Lime. Growth of demand from the sectors of paper & pulp, plastics, paints & coatings, and pharmaceuticals has been witnessed due to the country’s focus on sustainable production processes and CO₂ recovery-based carbonation procedures.

In this regard, the United States Precipitated Calcium Carbonate (PCC) Market is boosted by demand within its industry as per the report provided by USGS, stating that the United States is among the largest producers of precipitated calcium carbonate, producing 5 million metric tons annually. This is also because of the integration of satellite PCC plants with paper mills in the region.

Moreover, EPA has issued regulations related to the production processes used to increase sustainability and promote the use of CO₂ recovery-based carbonation procedures, thus increasing the use of PCC over talc and kaolin. In addition, state-level packaging and recycling regulations will contribute towards increased demand of PCC in the segments of paper & pulp and plastics.

Precipitated Calcium Carbonate Market Segment Analysis

-

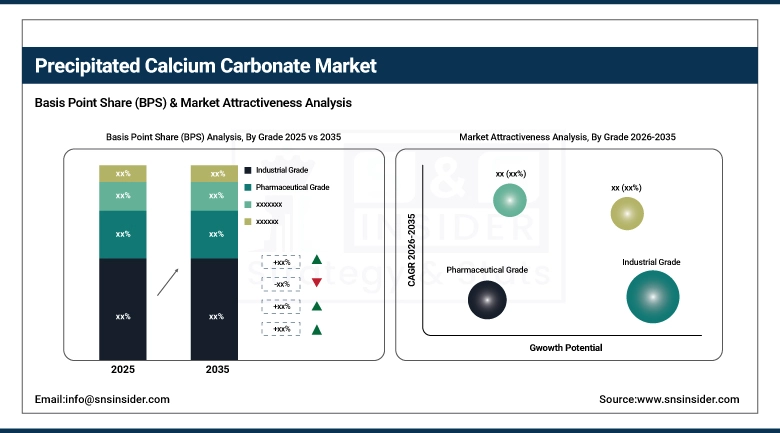

By Grade, Industrial Grade dominated the Precipitated Calcium Carbonate Market with 61.22% share in 2025; Food Grade fastest growing (CAGR).

-

By Application, Paper & Pulp dominated the Precipitated Calcium Carbonate Market with 35.44% share in 2025; Paints & Coatings fastest growing (CAGR).

-

By Form, Powder dominated the Precipitated Calcium Carbonate Market with 56.27% share in 2025; Nano PCC fastest growing (CAGR).

-

By Production Process, Carbonation Process dominated the Precipitated Calcium Carbonate Market with 70.02% share in 2025; Specialty Surface-Treated PCC fastest growing (CAGR).

By Grade, Industrial Grade dominated the Precipitated Calcium Carbonate Market with 61.22% share in 2025; Food Grade fastest growing (CAGR)

The Industrial Grade segment occupied the market leadership position in the Precipitated Calcium Carbonate industry in 2025, generating approximately 61.22% of the total market revenue. This was possible because of its widespread use in industries such as paper manufacturing, plastic, rubber, adhesives, sealants, and building materials. Here, PCC plays an important role in boosting brightness, opacity, hardness, and smoothness.

During the forecast period of 2026-2035, the Food Grade segment is anticipated to register the highest CAGR. This is because of the rising need for nutrient-enriched foods and drinks. Food-grade PCC finds growing usage in the formulation of bakery items, dairy products, confectionery, and nutraceuticals as a source of calcium content, pH adjuster, and anti-caking agent.

By Application, Paper & Pulp dominated the Precipitated Calcium Carbonate Market with 35.44% share in 2025; Paints & Coatings fastest growing (CAGR)

The Paper & Pulp segment accounted for more than 35.44% market share in terms of contribution to revenue in 2025. PCC acts as a key filler and coating pigment in the production of paper, which helps achieve improved brightness, opacity, printability, and surface finish along with lowered costs. Increasing demand for packaging materials such as corrugated boxes, labels, and specialty paper products has driven segment growth.

During the forecast period from 2026 to 2035, the Paints & Coatings segment is expected to record the highest CAGR driven by expanding infrastructure, vehicle manufacturing, and demand for decorative coatings. PCC improves the quality of coatings such as their durability, dispersibility, gloss, and weather resistance while minimizing costs. Construction activities in developing countries and growing adoption of green low-VOC coatings would further drive the segment's growth.

By Form, Powder dominated the Precipitated Calcium Carbonate Market with 56.27% share in 2025; Nano PCC fastest growing (CAGR)

In 2025, the Powder segment had a market share of 56.27%, holding a commanding position within the Precipitated Calcium Carbonate Market. Powder-based PCC is highly favored owing to its easy transportability, stable storage, good dispersability, and suitability for industrial manufacturing on a large scale. This product finds wide application in papermaking, plastics, rubber, paints, and pharmaceutical industries that require uniform particle size distribution and purity.

Between 2026 and 2035, the Nano PCC segment is expected to record the highest CAGR due to the growing application in high-performance plastics, specialty coatings, biomedical products, and advanced composite materials. Nanoscale PCC provides increased surface area, superior mechanical strength, enhanced optical properties, and improved dispersibility than regular PCCs.

By Production Process, Carbonation Process dominated the Precipitated Calcium Carbonate Market with 70.02% share in 2025; Specialty Surface-Treated PCC fastest growing (CAGR)

The Carbonation Process accounted for about 70.02% of all the market's revenue in 2025. The carbonation process continues being the most utilized manufacturing technology because of the cost effectiveness, scalability, particle morphological control, and capability to manufacture highly pure PCC for various applications. This technology ensures the manufacturing of particles of consistent sizes and brightness needed by paper, plastic, rubber, and coatings manufacturers.

Between 2026 and 2035, the Specialty Surface-Treated PCC will post the highest growth in terms of CAGR because of the need for specially tailored functional fillers with improved compatibility and properties. The specialty surface treatment of PCC enhances the hydrophobic nature, dispersibility, thermic stability, and bondability.

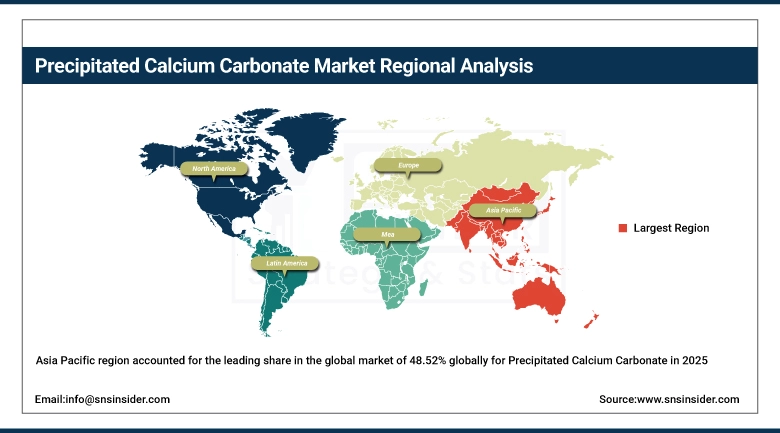

Precipitated Calcium Carbonate Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

20.37% |

|

Europe |

Germany |

18.37% |

|

Asia Pacific |

China |

48.52% |

|

Middle East & Africa |

UAE |

5.25% |

|

Latin America |

Brazil |

7.49% |

Asia Pacific Precipitated Calcium Carbonate Market Insights

The Asia Pacific region accounted for the leading share in the global market of 48.52% globally for Precipitated Calcium Carbonate in 2025 and will continue to dominate the industry in the upcoming years due to fast-paced industrialization, significant manufacturing activities, increasing demands for packaging materials, and growing consumption in paper, plastic, paint, coating, and construction industries.

Moreover, the Ministry of Economy, Trade and Industry (METI), Japan, is encouraging the development of CCUS and carbon recycling projects to facilitate decarbonization in the cement and mineral processing sectors. These efforts are also speeding up the development of new-generation Precipitated Calcium Carbonate and Synthetic Calcium Carbonate solutions in order to achieve sustainability in industry.

Additionally, several organizations, such as Sumitomo Osaka Cement, Kajima Corporation, and Idemitsu Kosan, are developing advanced technologies for manufacturing recycled calcium carbonate and CO2-based calcium carbonate solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Precipitated Calcium Carbonate Market Insights

North America is expected to witness the highest growth rate in the global Precipitated Calcium Carbonate market with CAGR of 6.58 over the forecast period due to increasing demand in high-end uses such as paints and coatings, pharmaceuticals, plastics, specialty papers, and food additives. North America possesses well-developed manufacturing facilities, superior technological know-how in specialty minerals manufacturing, and investments in sustainable packaging materials and lightweight polymers.

In addition, North America is benefiting from increasing government and institutional support for sustainable manufacturing, carbon utilization, and advanced material innovation. The U.S. Department of Energy (DOE) continues to support carbon capture, utilization, and storage (CCUS) initiatives that encourage development of CO₂-derived mineral products, including synthetic and precipitated calcium carbonate for industrial applications such as paper, plastics, construction materials, and coatings.

Europe Precipitated Calcium Carbonate Market Insights

The Europe region was seen with a second-largest revenue share of the global Precipitated Calcium Carbonate Market in 2025, considering its advanced specialty chemical sector, strict environmental norms, mature paper and coating industries, and rising need for premium fillers in various industrial applications. Germany, France, the United Kingdom, Italy, as well as the Nordic countries continue to be important regional players due to the significant contribution from paper making, coatings, automobiles, pharmaceuticals, as well as sustainable packaging industries. The leading market performance within Europe is being attributed to Germany, as it possesses a large industrial manufacturing base, as well as widespread use of PCC in paints, plastics, adhesives, and polymer-based applications.

Moreover, the EU CCUS strategy is driving innovations in carbon mineralized synthetic calcium carbonate products utilized in construction, paper, coatings, and plastic applications. Multiple European enterprises and research institutions have been investing in technologies that produce precipitated calcium carbonate using captured CO₂ emissions from industrial processes.

Middle East & Africa and Latin America Precipitated Calcium Carbonate Market Insights

The Middle East & Africa and Latin America markets have witnessed consistent market growth in terms of Precipitated Calcium Carbonate across the world due to increased industrialization, growing investments in construction industry, increased developments in infrastructure, increased demand from packaging sector, and growth in manufacturing industry such as paints & coatings, plastics, paper, and construction materials.

In addition to this, the manufacturing practices and policies in Brazil which aim to promote recycling and sustainable practices are expected to increase the usage of recycled packaging materials and mineral fillers in the plastics and paper industry. Growth in the investment in food processing industry and pharmaceuticals manufacturing is driving the market demand for food grade and pharmaceutical grade precipitated calcium carbonate in Latin America region.

Precipitated Calcium Carbonate Market Growth Drivers:

-

Rising demand for lightweight, sustainable, and high-performance filler materials across paper, plastics, coatings, and packaging industries driving global adoption of precipitated calcium carbonate

Among the major structural forces that are contributing to the expansion of the Precipitated Calcium Carbonate (PCC) market include the trend towards environmentally friendly and cost-effective lightweight materials within industries. For example, manufacturers in different sectors including paper, plastics, paints and coatings, adhesives, and packaging are increasingly turning to PCC due to its ability to increase the brightness, opacity, smoothness, mechanical strength of their products as well as making manufacturing processes easier at the same time reducing production costs through raw material savings.

Besides, there is the issue of sustainable manufacturing processes which have been highlighted by the United Nations Environment Programme (UNEP). With many industries trying to adopt more environmentally friendly practices to lower their emission levels and minimize the amount of plastic waste created, PCC becomes an important option for industries as functional mineral additives.

Precipitated Calcium Carbonate Market Restraints:

-

Volatility in raw material prices and high production costs of specialty precipitated calcium carbonate creating profitability pressures for manufacturers

Cost sensitivity is a critical limitation to the market expansion due to the high expenses incurred in the production process. The production process involves large capital outlays for calcining plants, carbonation units, energy-efficient machines, particle sizing machinery, and facilities that facilitate compliance with environmental regulations. Moreover, variations in the quality of limestone used in the process, energy prices, transportation costs, and expenses associated with managing carbon emissions affect the profitability of the process.

Precipitated Calcium Carbonate Market Opportunities:

-

Expanding adoption of nano PCC, sustainable mineral technologies, and high-performance specialty applications creating new growth opportunities across advanced industrial sectors

Opportunities for growth in the PCC market will be seen in the form of high performance, eco-friendly, and specialized calcium carbonate products that will help meet the changing needs of industries. The increasing need for nano PCC, surface treated PCC, and ultra-pure PCC will lead to huge opportunities in the application of advanced plastics, lightweight automotive parts, specialized coatings, pharmaceutical industry, food additives, and sustainable packaging products. The emphasis of manufacturers will increasingly be on the engineering of PCC materials with better dispersibility and optical properties.

Recent Developments:

-

2026: Omya AG extended its specialty range of calcium carbonate products by investing in sustainable and ultra-fine precipitated calcium carbonate products that serve high-end applications in packaging, paints, and polymers. The firm further advanced its circular economy model through innovative developments of lower carbon footprints mineral production technologies and recyclable packaging materials through additional production capacity in European and Asian plants.

-

2025: Imerys S.A. accelerated innovations of its engineered calcium carbonate products for sustainable applications in paper, coatings, and construction industries, as well as carbon reduction strategies for all its industrial mineral productions. Imerys S.A. also innovated further its specialty PCC products for plastics and low VOC coatings to meet growing demands for more environmentally friendly industrial products from Europe and North America.

-

2025: Minerals Technologies Inc. expanded further its global network of satellite plants that produce PCC products for paper and packaging industries, as well as advanced its innovations of specialty PCC products for packaging, food, and pharmaceutical industries. The firm further developed its FulFill® Eco technology aimed at increasing fiber replacement efficiencies and reducing carbon footprint in paper making.

-

2026: Schaefer Kalk GmbH & Co. KG increased their investments in processes and technology related to high purity precipitated calcium carbonate, focusing on the uses of such materials in the pharmaceutical industry, in food-related products and specialty polymers. They continued their efforts towards sustainable manufacturing by means of implementing energy efficiency and new surface treated PCCs.

Precipitated Calcium Carbonate Market Key Players

Some of the Precipitated Calcium Carbonate Market Companies

-

Omya AG

-

Imerys S.A.

-

Minerals Technologies Inc.

-

Schaefer Kalk GmbH & Co. KG

-

Shiraishi Calcium Kaisha Ltd.

-

Calcinor S.A.

-

GCCP Resources Limited

-

Graymont Limited

-

Kunal Calcium Limited

-

Gulshan Polyols Ltd.

-

Chemical & Mineral Industries Pvt. Ltd.

-

Nordkalk Corporation

-

Maruo Calcium Co. Ltd.

-

Mississippi Lime Company

-

Lhoist Group

-

Provale Holding SA

-

Okutama Kogyo Co. Ltd.

-

Fujian Sanmu Nano Calcium Carbonate Co. Ltd.

Precipitated Calcium Carbonate Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.06 Billion |

| Market Size by 2035 | USD 19.84 Billion |

| CAGR | CAGR of 5.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Industrial Grade, Pharmaceutical Grade, Food Grade, Cosmetic Grade, Reagent Grade, Others), • By Application (Paper & Pulp, Plastics, Paints & Coatings, Rubber, Pharmaceuticals, Adhesives & Sealants, Printing Inks, Others), • By Form (Powder, Slurry, Nano PCC, Colloidal PCC, Others), • By Production Process (Carbonation Process, Lime-Soda Process, Solvay-Based Process, Specialty Surface-Treated PCC, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Omya AG, Imerys S.A., Minerals Technologies Inc., Schaefer Kalk GmbH & Co. KG, Shiraishi Calcium Kaisha Ltd., SCR-Sibelco N.V., Calcinor S.A., GCCP Resources Limited, Graymont Limited, Kunal Calcium Limited, Gulshan Polyols Ltd., Chemical & Mineral Industries Pvt. Ltd., Nordkalk Corporation, Maruo Calcium Co. Ltd., Huber Engineered Materials, Mississippi Lime Company, Lhoist Group, Provale Holding SA, Okutama Kogyo Co. Ltd., Fujian Sanmu Nano Calcium Carbonate Co. Ltd. |

Frequently Asked Questions

Industrial demand for performance-enhancing fillers, sustainability pressures, and specialty PCC innovations are the primary drivers of market expansion.

Asia Pacific dominated the Precipitated Calcium Carbonate Market in 2025.

The Carbonation Process segment dominated the Precipitated Calcium Carbonate Market in 2025.

The Precipitated Calcium Carbonate Market was valued at USD 12.06 Billion in 2025.

The Precipitated Calcium Carbonate Market is expected to grow at a CAGR of 5.16% from 2026 to 2035.

Get in Touch