Radiopharmaceutical CDMO Market Report Scope & Overview:

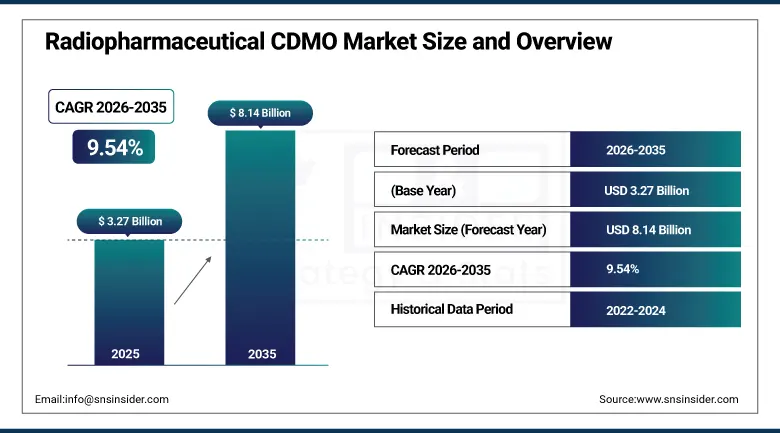

The Radiopharmaceutical CDMO Market was valued at USD 3.27 Billion in 2025 and is projected to reach USD 8.14 Billion by 2035, expanding at a CAGR of 9.54% during the forecast period 2026–2035.

The international radiopharmaceutical CDMO market is witnessing substantial growth, thanks to the increasing number of targeted radionuclide therapies entering the commercial market, increasing use of theranostics in clinics, and increased outsourcing activities on the part of pharmaceutical and biotech companies. Increasing complexity involved in radioisotopes processing, the need for GMP manufacture, short-lived isotopes, and logistics infrastructure is prompting drug makers to work with dedicated radiopharmaceutical CDMOs. Investments into the development of radio ligands, alpha radio therapeutics, and precision oncology platforms are further adding to the demand for manufacturing services in the market.

In 2025-2026, a number of radiopharmaceutical firms made substantial investments in isotope manufacturing capacities, GMP radiochemistry infrastructure, and manufacturing facilities to accommodate the fast-growing pipeline of targeted radionuclide therapies.

Market Size and Forecast

-

Market Size 2026E: USD 3.58 Billion

-

Market Size 2035: USD 8.14 Billion

-

CAGR: 9.54% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Radiopharmaceutical CDMO Market - Request Free Sample Report

-

Increasing commercialization of targeted radio ligand therapies across oncology indications.

-

Rising outsourcing of radiochemistry development and GMP manufacturing activities.

-

Growing investments in isotope production infrastructure and supply chain networks.

-

Expansion of theranostic treatment approaches combining diagnostics and therapeutics.

-

Increasing adoption of alpha-emitting and beta-emitting radioisotopes for precision medicine applications.

The U.S. Radiopharmaceutical CDMO Market Size Outlook

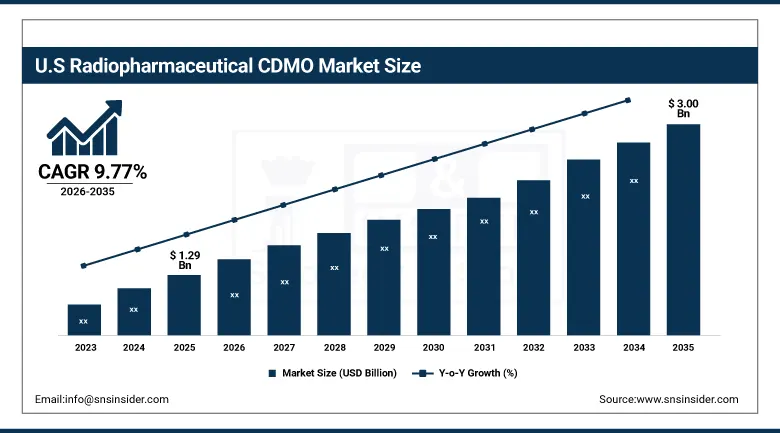

The U.S. Radiopharmaceutical CDMO Market was valued at USD 1.29 billion in 2025 and is expected to reach approximately USD 3.00 billion by 2035, expanding at a CAGR of 9.77% during 2026–2035.

The United States still dominates the radiopharmaceutical CDMO industry owing to their nuclear medicine facilities and their strong clinical research setup along with increasing usage of radio ligand therapy in oncology. Companies are now spending more on targeted radionuclides and are using services of specialized CDMOs that have the knowledge and capability to work with isotopes and manufacture them. Increasing demand for precision oncology, increasing theranostics and investments in the production of isotopes will drive the industry. Collaboration of drug developers, healthcare providers and CDMOs is further helping them dominate the industry.

In 2026, Several U.S. based radiopharmaceutical companies enhanced isotope production and radio ligand manufacturing capacity to meet the rising oncology demand.

Radiopharmaceutical CDMO Market Segment Analysis

-

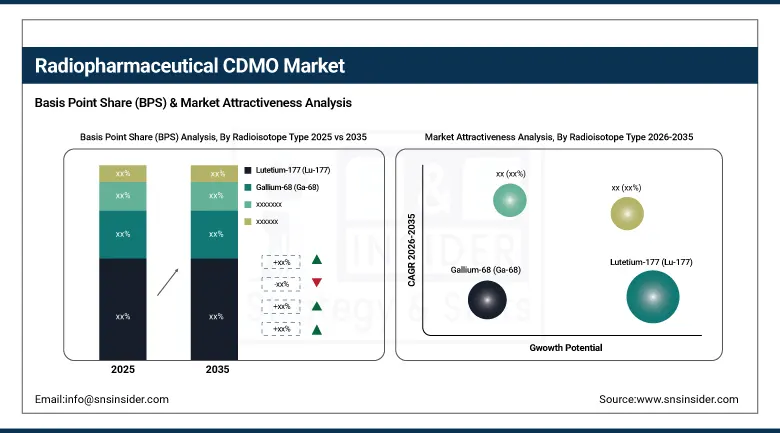

By Radioisotope Type, lutetium-177 (Lu-177) dominated the market with 29.00% share in 2025, and projected to witness the fastest growth with 14.24% CAGR during the forecast period.

-

By Service Type, clinical manufacturing dominated the market with 31.00% share in 2025, while fill-finish & packaging is projected to witness the fastest growth with 12.42% CAGR during the forecast period.

-

By Application, oncology dominated the market with 48.00% share in 2025, and is projected to witness the fastest growth with 11.44% CAGR during the forecast period.

-

By End User, pharmaceutical companies dominated the market with 32.00% share in 2025, and are projected to witness the fastest growth with 14.98% CAGR during the forecast period.

By Radioisotope Type, lutetium-177 dominated the market and the fastest-growing segment.

The segment of lutetium-177 generated the largest revenue of 29.00% in 2025 as a result of the commercialization of targeted radio ligand therapy and increasing application of theranostic approach to the oncological indications. Increasing efforts by pharma companies for development of therapeutic pipelines based on Lu-177 were driven by positive results, ability to deliver radiation dose directly and regulatory approvals. An increase in the number of late-stage clinical programs along with increased outsourcing of isotope, radiolabeling and manufacturing processes under GMP guidelines to dedicated CDMOs contributes to the further growth of this segment. Investments into the production facilities for radionuclides also boost the commercial prospects for manufacturing of Lu-177.

The lutetium-177 segment is expected to generate the highest CAGR of 14.24% in the forecast period due to increasing adoption of radio ligand therapies and investment into theranostic medicines on the global scale. Growing need for precision treatments stimulates pharma companies to develop the Lu-177-based therapeutic candidates against prostate cancer, neuroendocrine tumors and solid cancers. Recent Insight (2026): Several radiopharmaceutical companies extended Lu-177 manufacturing partnerships to cater to growing demand of targeted cancer therapies.

By Service Type, clinical manufacturing dominated the market, while fill-finish & packaging is the fastest-growing segment.

The clinical manufacturing segment occupied the largest market share of 31.00% in 2025 owing to the rising trend of clinical-stage radiopharmaceutical manufacturing outsourcing by the pharmaceuticals and biotech companies. Growing number of radio ligand therapy molecules advancing through the clinical pipeline has generated significant demand for GMP manufacturing capabilities, radionuclide expertise, and compliance of manufacturing activities. Increasingly sponsors are turning to CDMOs for faster timelines, process optimization, and quality consistency throughout development process. 2026, Many radiopharmaceutical CDMOs have made additions to their GMP production facilities and clinical manufacturing facilities to accommodate growing radio ligand therapy pipelines.

Fill-finish & packaging segment is expected to witness fastest CAGR of 12.42% during the forecast period owing to rising commercialization of radiopharmaceutical therapeutics and demand for specialized packaging needs. Radiopharmaceuticals are known for demanding handling processes, radiation-secure packaging solutions, and coordination for transportation purposes as these therapeutics are known for limited shelf life and transportation challenges. CDMOs are increasingly investing in aseptic filling systems, advanced containment solutions, and specialized distribution facilities to increase the product integrity and regulatory compliance. 2025, leading service providers have announced plans for making investments into radiopharmaceutical automated fill-finish systems.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

92.00% |

|

Europe |

Germany |

31.00% |

|

Asia Pacific |

China |

18.00% |

|

Middle East & Africa |

UAE |

4.00% |

|

Latin America |

Brazil |

4.00% |

North America Radiopharmaceutical CDMO Market Insights

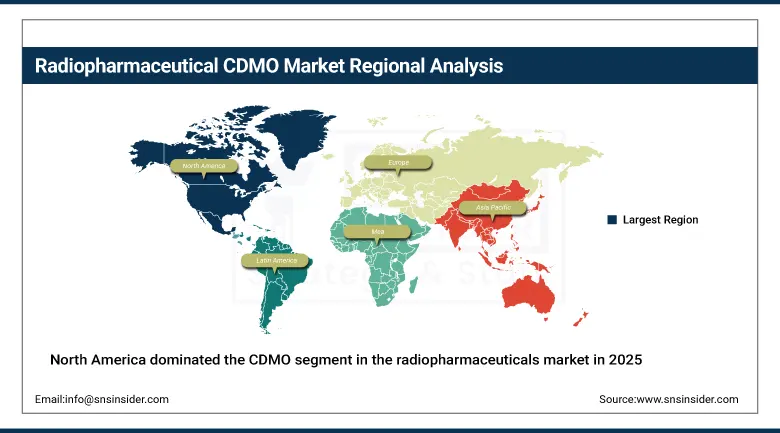

North America dominated the CDMO segment in the radiopharmaceuticals market in 2025, contributing almost 43.00% of the global revenue share. This dominance can be attributed to the advanced nuclear medicine technology available in the region, rising adoption of radio ligand therapies, as well as the active involvement of key pharmaceutical/biotech companies in the development of targeted radionuclide therapies. In addition, the CDMO firms operating in the United States and Canada continue their investments in isotopes, GMP facilities, and radiochemistry for meeting the growing demands. Regulatory compliance, high number of cancer treatments, and growing adoption of theranostics are expected to propel the regional market growth.

2026, Expansion plans of several North American radiopharmaceutical firms have been observed to enhance commercial capacities for radio ligand therapies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Radiopharmaceutical CDMO Market Insights

Europe was responsible for around 31.00% of the global radiopharmaceutical CDMO market share in 2025 due to the increased use of nuclear medicines, rising activities related to radiopharmaceuticals research and development, and growing interest in targeted cancer treatments. Nations such as Germany, France, the UK, Italy, and Switzerland still drive market growth due to well-developed healthcare systems and increasing use of precision medicine approaches. Collaborations between pharmaceutical firms and CDMOs operating in the region provide the former with isotope manufacturing experience, clinical development assistance, and production services that are compliant with regulations. Increased demand for theranostics and innovations in radionuclide therapies will lead to growth opportunities in the region.

2025, Isotope production capabilities of some European radiopharmaceuticals firms were expanded to meet the rising demand for radio ligand oncology treatments.

Asia Pacific Radiopharmaceutical CDMO Market Insights

The Asia Pacific region is forecasted to grow at the highest CAGR of 13.65% during the forecast period due to rapidly developing healthcare infrastructure, increasing population of oncology patients, and investments in nuclear medicine facilities. Regions such as China, Japan, South Korea, India, and Australia are experiencing increasing adoption of targeted radionuclides and increased development activities in the region. Pharmaceutical players in the region are increasingly making investments in R&D for radiopharmaceuticals in conjunction with CDMO partners that provide expertise in manufacturing. Increasing healthcare spending, increasing access to precision oncology treatment, and increasing government investment in nuclear medicine development will lead to significant market growth.

2026, Several Asia Pacific healthcare systems increased their investment in nuclear medicine infrastructure and radiopharmaceutical production facilities.

Middle East & Africa and Latin America Radiopharmaceutical CDMO Market Insights

There has been consistent market growth for the Middle East & Africa owing to rising modernization of healthcare in terms of increasing infrastructural developments for oncology treatment and availability of nuclear medicine. Countries like UAE, Saudi Arabia, and South Africa have been making investments in healthcare facilities and diagnostic facilities that can help in the adoption of precision medicine. Growing awareness about targeted cancer therapy and collaboration with radiopharmaceuticals developers from overseas markets continues to drive the market in the region.

Latin America was estimated to capture about 4.00% market share in 2025 due to increasing cancer treatments, improved healthcare infrastructure, and increased use of advanced nuclear medicine procedures in countries like Brazil, Mexico, Argentina, and Chile. Radiopharmaceuticals companies and healthcare organizations are adopting radiopharmaceuticals as an effective treatment option. Healthcare investments, increased access to specialized drugs, and involvement in global clinical trials are some of the factors that will continue to support market growth in the region. 2025, There have been increased investments made by healthcare organizations in both regions for the development of nuclear medicine infrastructure.

Market Dynamics

Growth Drivers: Increasing commercialization of radio ligand therapies and theranostics.

Commercialization of radio ligand therapies and an increased preference for a theranostic approach for treatment is driving the demand for radiopharmaceuticals CDMO services. Pharmaceutical and biotech companies are increasingly investing in targeted radionuclide treatments that provide the ability to administer highly concentrated radioactive agents directly into cancerous cells without damaging other tissues. Increasing focus on these therapies has led to the emergence of significant demand for services related to isotope handling, radiochemistry, GMP manufacturing, analysis, and commercial production. As the oncology pipeline continues to grow and more radiopharmaceuticals enter the commercial stage, the demand for CDMOs is likely to increase significantly in global healthcare market.

In 2026, Late-stage radio ligand therapies moved closer to commercialization, boosting demand for specialized manufacturing facilities.

Restraints: Insufficient isotope production and difficulties in building a supply chain.

While the industry enjoys good market prospects, shortage of medical radioisotopes and difficult supply chain conditions are among the key obstacles that stand in the way of the radiopharmaceutical CDMO sector's development. Most radio therapeutics need a special production facility, sophisticated transportation procedures, and proper distribution channels, owing to the short lifetime of such isotopes. There might be interruptions in isotope production caused by various factors, such as plant maintenance or other issues. Moreover, considerable investments needed to build the facilities compliant with all necessary regulations serve as a barrier for entering the market. 2025, Companies started signing more isotope production contracts in order to eliminate possible shortages.

Opportunities: Increase in the development program of alpha-emitting radiopharmaceuticals.

The development of alpha-emitting radiopharmaceuticals is one of the most important growth areas for the CDMO market players globally. The alpha-emitters including Actinium-225 have gained much attention due to the capability of providing highly potent and localized effects in a minimum amount of off-target exposure. Pharma companies are focusing on research programs for hard-to-treat cancers and rare diseases based on advanced radiopharmaceutical treatments. With further advancements in clinical trials, the demand for specific technical expertise, isotope sourcing, analytical testing services, and production capacity will grow. This new treatment paradigm is giving some long-term opportunities to the radiopharmaceutical CDMO players.

In 2026, several developers made new investments into the Actinium-225 research and manufacturing programs.

Recent Developments

-

2026: Curium announced expansion of its radiopharmaceutical manufacturing infrastructure to strengthen commercial-scale production capabilities for targeted radionuclide therapies and support increasing global demand for oncology-focused radiopharmaceutical products.

-

2026: Eckert & Ziegler expanded isotope manufacturing and radiopharmaceutical service capabilities to support growing clinical and commercial demand for precision oncology and theranostic applications.

-

2025: NorthStar Medical Radioisotopes announced investments focused on isotope production capacity expansion and supply chain optimization to improve reliability for radiopharmaceutical manufacturers and healthcare providers.

-

2025: PharmaLogic Holdings expanded radiopharmaceutical manufacturing operations and distribution capabilities to support increasing adoption of radio ligand therapies across major oncology treatment markets.

Radiopharmaceutical CDMO Market Key Players are:

-

Curium

-

Eckert & Ziegler

-

ITM Isotope Technologies Munich SE

-

NorthStar Medical Radioisotopes

-

Cardinal Health

-

SOFIE Biosciences

-

PharmaLogic Holdings Corp.

-

SpectronRx

-

Monrol

-

SHINE Technologies

-

IONETIX Corporation

-

Nucleus RadioPharma

-

Evergreen Theragnostics

-

Minerva Imaging

-

Seibersdorf Labor GmbH

-

Nihon Medi-Physics Co., Ltd.

-

Advanced Accelerator Applications

-

Jubilant Radiopharma

-

Telix Pharmaceuticals

-

Isotopia Molecular Imaging

Radiopharmaceutical CDMO Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.27 Billion |

| Market Size by 2035 | USD 8.14 Billion |

| CAGR | CAGR of 9.54% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Retail Automation Assessment, Smart Checkout Technology Trends, AI-Enabled Retail Infrastructure Analysis, DROC & SWOT Analysis, Investment Trends, Supply Chain Evaluation, Consumer Transaction Technology Assessment, and Future Market Opportunity EvaluationChain Evaluation, Industrial Packaging Demand Analysis, Sustainability Assessment, DROC & SWOT Analysis, Regulatory Framework Analysis, Innovation Benchmarking, and Future Market Opportunity Evaluation |

| Key Segments | • By Radioisotope Type (Lutetium-177 (Lu-177), Gallium-68 (Ga-68), Fluorine-18 (F-18), Actinium-225 (Ac-225), Others) • By Service Type (Process Development, Analytical & QC Testing, Clinical Manufacturing, Commercial Manufacturing, Fill-Finish & Packaging) • By Application (Oncology, Cardiology, Neurology, Theranostics, Others) • By End User (Pharmaceutical Companies, Biotechnology Companies, Academic & Research Institutes, Nuclear Medicine Centers, Hospitals & Health Systems |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Curium, Eckert & Ziegler, ITM Isotope Technologies Munich SE, NorthStar Medical Radioisotopes, Cardinal Health, SOFIE Biosciences, PharmaLogic Holdings Corp., SpectronRx, Monrol, SHINE Technologies, IONETIX Corporation, Nucleus RadioPharma, Evergreen Theragnostics, Minerva Imaging, Seibersdorf Labor GmbH, Nihon Medi-Physics Co., Ltd., Advanced Accelerator Applications, Jubilant Radiopharma, Telix Pharmaceuticals, Isotopia Molecular Imaging. |

Frequently Asked Questions

The Radiopharmaceutical CDMO Market was valued at USD 3.27 billion in 2025.

The market is projected to reach USD 8.14 billion by 2035.

The market is expected to expand at a CAGR of 9.54% during the forecast period.

Lutetium-177 (Lu-177) accounted for the largest revenue share of 29.00% in 2025 owing to increasing commercialization of targeted radio ligand therapies and theranostic treatment approaches.

North America dominated the global market owing to its advanced nuclear medicine infrastructure, increasing radio ligand therapy adoption, and strong presence of pharmaceutical and biotechnology companies.

Get in Touch