RNA Therapeutics CDMO Market Report Scope & Overview:

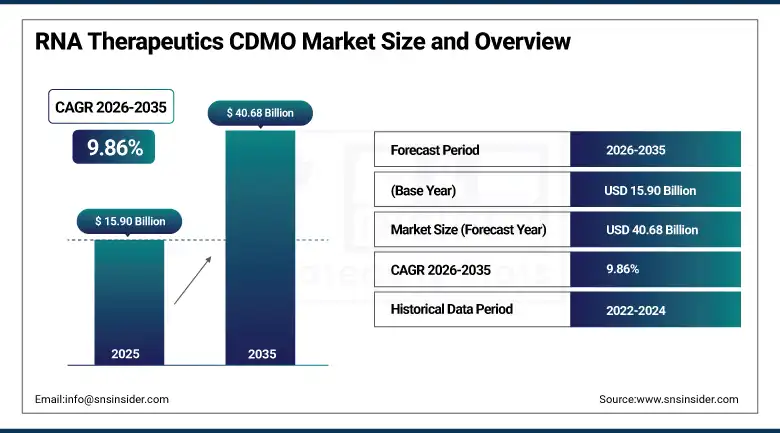

The RNA Therapeutics CDMO Market was valued at USD 15.90 Billion in 2025 and is projected to reach USD 40.68 Billion by 2035, expanding at a CAGR of 9.86% during the forecast period 2026–2035.

Globally, the RNA therapeutics contract development and manufacturing organization market is growing rapidly since pharmaceuticals and biotech organizations continue to outsource RNA development and manufacturing processes to specialized organizations. Commercializing mRNA vaccines, gene silencing medicines, antisense oligonucleotides, and other innovative RNA therapeutics is creating an increased demand for development, GMP manufacturing, characterization, and filling services for RNA products. RNA therapeutics CDMOs are making huge investments in building RNA manufacturing capabilities like infrastructure for high-throughput RNA synthesis, automation technologies for manufacturing and fill-finish process, digital quality management systems, and analytical technologies.

In 2025-2026, the RNA therapeutic industry invested significantly in building large scale RNA manufacturing facilities, lipid nanoparticle manufacturing capacities, AI-assisted platform for process optimization, and end-to-end development services to accelerate development and improve manufacturing scalability of RNA therapeutics.

Market Size and Forecast

-

Market Size 2026E: USD 17.46 Billion

-

Market Size 2035: USD 40.68 Billion

-

CAGR: 9.86% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On RNA Therapeutics CDMO Market - Request Free Sample Report

RNA Therapeutics CDMO Market Trends

-

Increasing outsourcing of RNA process development and GMP manufacturing activities.

-

Growing commercialization of mRNA, siRNA, and oligonucleotide therapeutics globally.

-

Expansion of large-scale RNA synthesis and lipid nanoparticle manufacturing facilities.

-

Rising adoption of AI-enabled manufacturing optimization and digital quality control systems.

-

Growing investments in commercial fill-finish infrastructure for RNA-based therapeutics.

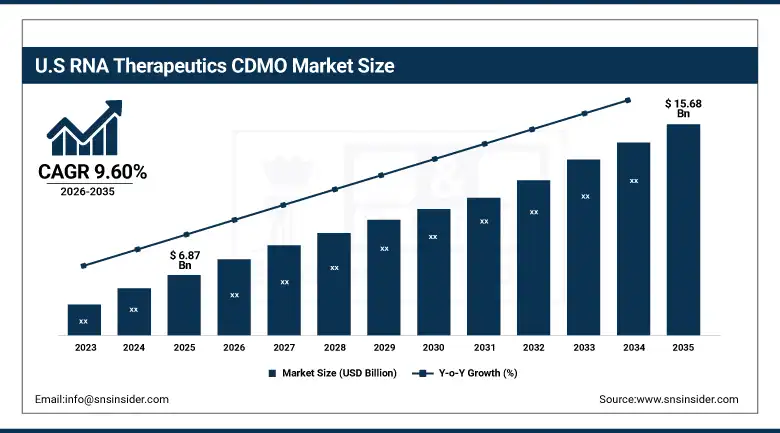

The U.S. RNA Therapeutics CDMO Market Size Outlook

The U.S. RNA Therapeutics CDMO Market was valued at USD 6.87 billion in 2025 and is expected to reach approximately USD 15.68 billion by 2035, expanding at a CAGR of 9.60% during 2026–2035.

The United States still remains at the top of the RNA therapeutics CDMO industry on account of the developed biotechnology industry, manufacturing infrastructure, clinical trial activities, and next-generation RNA technologies investment. Bophirima players are making partnerships with highly specialized CDMOs to speed up development time, utilize GMP capacities, and manufacture commercial products such as mRNA vaccines, gene silencing, and rare disease therapies. High demand from the growing number of products and RNA therapeutics' regulatory approvals ensures that the need for outsourcing will remain high. The country benefits from having innovative biotech, developed pharmaceutical manufacturers, and research organizations. Investments into advanced bio manufacturing facilities in government and private sectors are also contributing to market expansion.

In 2025-2026, some of the US CDMOs expanded their capacities for mRNA manufacturing, liposomal nanoparticles, and fill-finish of the commercial scale.

RNA Therapeutics CDMO Market Segment Analysis

-

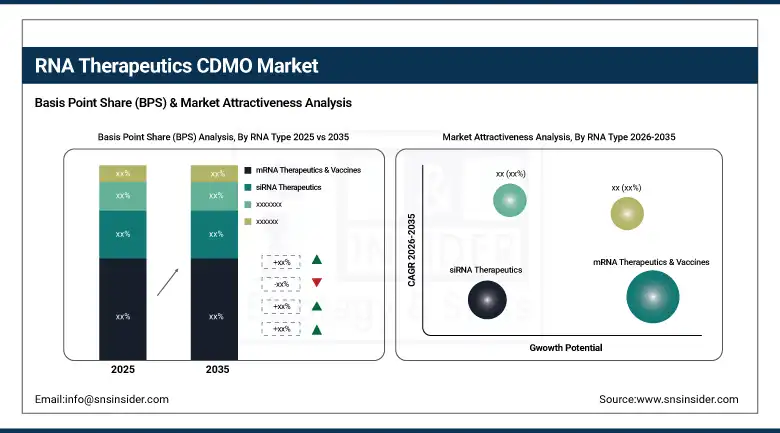

By RNA Type, mRNA therapeutics & vaccines dominated the market with 48.00% share in 2025, while ASO, circRNA & other RNA modalities are projected to witness the fastest growth with a 11.21% CAGR during the forecast period.

-

By Service Type, clinical manufacturing dominated the market with 42.00% share in 2025, while commercial manufacturing & fill-finish is projected to witness the fastest growth with a 12.43% CAGR during the forecast period.

-

By Application, infectious diseases dominated the market with 39.00% share in 2025, while oncology is projected to witness the fastest growth with a 11.62% CAGR during the forecast period.

-

By End User, biopharmaceutical companies dominated the market with 58.00% share in 2025, and are projected to witness the fastest growth with a 12.56% CAGR during the forecast period.

By RNA Type, mRNA therapeutics & vaccines dominated, while ASO, circRNA & Other RNA modalities are fastest-growing.

The share of the mRNA therapies and vaccines market was the largest in 2025 at 48.00% due to the extensive use of mRNA-based vaccines and clinical trials of therapeutic mRNA products for the treatment of cancer, infections, and rare diseases. Increasing outsourcing by biopharmaceutical companies for plasmid manufacturing, in vitro transcription, formulation, and GMP manufacturing solutions has been fueling the growth of the mRNA therapeutics & vaccines segment. Moreover, the scalability of the platform and growing global development pipeline have continued to drive outsourcing demand in this segment. Personalized cancer vaccine, self-amplifying RNA and next-generation delivery technology development investments are expected to further solidify the dominance of this segment.

The ASO, circRNA & Other RNA modalities segment was projected to exhibit the highest 11.21% CAGR in the coming years owing to increased investments in next generation RNA technologies which can enhance their stability, targeting ability and effectiveness. There are many ongoing investments being made by CDMOs in advanced RNA synthesis, purification, and analytics solutions. During the years 2025–2026, a number of RNA developers have moved forward with their unique circular RNA and oligonucleotide therapies in to clinical trials stage which adds to their demand for outsourcing.

By Service Type, clinical manufacturing dominated, while commercial manufacturing & fill-finish is fastest-growing.

Clinical manufacturing segment captured the maximum market share of 42.00% in 2025 because of an increasing number of RNA therapies being developed and moving into the Phase I, II, and III clinical studies. Biotech companies are outsourcing clinical batches production in order to have access to GMP-compliant facilities, technical know-how, and fast manufacturing process. Increasing pipeline for RNA development and the rising regulatory pressure on clinical manufacturing are supporting demand for CDMO services in this segment. Moreover, the complexity of RNA synthesis, formulation optimization, and analytical validation process requires collaboration with CDMOs for biotech companies in order to advance their RNA drug candidates in clinical trials.

Commercial manufacturing & fill-finish segment is expected to show the highest CAGR of 12.43% during 2025-2035. With the increasing number of RNA therapeutics moving into commercialization phase, the demand for large-scale manufacturing, aseptic fill-finish services, and supply chain services is increasing. During 2025-2026, many CDMOs started making announcements about investment in commercial-scale RNA manufacturing suites and high-capacity fill-finish suites to prepare for future product launches and large-scale production. Increasing regulatory approvals, rising patient need, and growing portfolio of RNA therapeutics in the global market are leading to growing capacity investments by CDMOs.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

94.00% |

|

Europe |

Germany |

28.00% |

|

Asia Pacific |

China |

19.00% |

|

Middle East & Africa |

UAE |

4.00% |

|

Latin America |

Brazil |

3.00% |

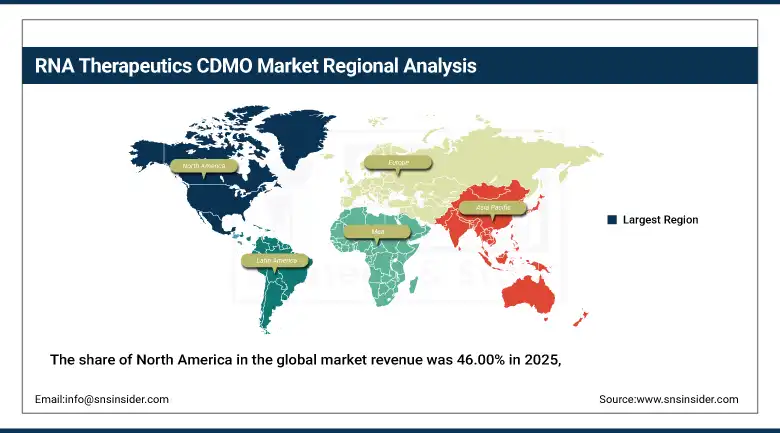

North America RNA Therapeutics CDMO Market Insights

The share of North America in the global market revenue was 46.00% in 2025, and the region retained its leading position owing to innovations in biotechnology, clinical development, and existing RNA manufacturing infrastructure. Pharmaceuticals and biotech firms keep on building new advanced RNA production facilities, analytical development facilities, and GMP manufacturing facilities. Good regulatory standards and substantial investments made by the private sector help in developing the regional market. A well-developed life sciences sector, venture capital investments, and a high number of RNA-based biotechnology companies contribute to the development of the regional market. Growing demand for RNA vaccines, gene silencing drugs, and precision medicines contributes to outsourcing and development of CDMOs in North America.

In 2025-2026, several North American CDMOs increased the capacities of their mRNA production and liposome nanoparticle manufacturing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe RNA Therapeutics CDMO Market Insights

Europe contributed about 28.00% towards the total worldwide revenue in 2025 due to the increase in the investments in RNA development programs, biopharmaceuticals, and outsourced services. Several countries such as Germany, UK, France, and Switzerland are constantly working on improving their RNA development ecosystem due to the rise in investment in bioprocessing and advanced manufacturing processes. Europe is considered one of the leading regions in the innovation of RNA therapy development and commercialization.

The market is growing due to the collaboration between academia for research, biotechnology initiatives by governments, and collaboration between pharmaceutical companies and CDMOs. The growth in the market is also attributed to an increase in clinical trials of RNA therapies in oncology, rare diseases, and infectious disease therapy.

Several CDMOs in Europe made improvements in their facilities and entered into strategic collaborations in 2025-2026 to improve their RNA process development and GMP manufacturing capabilities.

Asia Pacific RNA Therapeutics CDMO Market Insights

The Asia Pacific region is estimated to witness the highest CAGR of 13.79%. Factors such as rapid growth of biotechnology sectors, increasing healthcare investments, government policies favoring the development of the industry, and active involvement of the region in global clinical trials have driven the need for RNA manufacturing services in countries including China, Japan, South Korea, India, and Singapore. There is aggressive expansion by regional contract manufacturing organizations to serve both domestic and international customers. With the presence of competitive costs, improved technical proficiency, and increased investments in biopharmaceutical infrastructure, the region is becoming more and more favorable for outsourcing of RNA development and manufacturing services.

In 2025–2026, some of the key players in the Asia Pacific region made investments in advanced RNA synthesis technologies and development and manufacturing infrastructures that will attract global RNA therapy programs.

Middle East & Africa and Latin America RNA Therapeutics CDMO Market Insights

The Middle East & Africa region accounted for nearly 3.00% of market revenue in 2025. Government investments in biotechnologies, diversification of healthcare systems, and rising interests in advanced therapies technologies are contributing to sustainable growth in Latin American regions. In 2025-2026, there has been an increase in the number of countries implementing biotechnology infrastructure projects targeting advanced biologics and nucleic acid-based therapeutics production. Research centers, bio manufacturing facilities, and healthcare innovation hubs have been gradually built. Collaborations with multinational pharmaceutical and technology companies have been providing an opportunity to gain necessary experience and expertise.

In 2025, Latin America accounted for approximately 4.00% of global market revenue. Increased activity in manufacturing, increased investments in biotechnology and participation in clinical research are supporting a steady demand for RNA development and manufacturing services. Modernization of healthcare systems in the region has provided promising opportunities for RNA therapeutics commercialization. Brazil, Mexico, and Argentina are gaining competencies in the sphere of life sciences through investments in R&D infrastructures, regulatory modernization, and biotechnology collaborations. Although Latin American region is still in its infancy compared to North America and Europe, increased awareness of advanced therapies and participation in international clinical trials provide growth opportunities.

Market Dynamics

Growth Drivers: Growth in pipeline of RNA therapeutics and outsourcing needs.

The rapid development of RNA-based therapies in the fields of infectious diseases, oncology, rare diseases, and genetic disorders has led to an increased demand for outsourcing services. Outsourcing is necessary for pharmaceutical companies to accelerate development, gain access to more advanced technology, and manage increased complexities during manufacturing. With the growing preference for mRNA, siRNA, antisense oligonucleotides, and other types of RNA therapy, companies are constantly working on developing their processes, GMP manufacturing, and commercial manufacturing capacity across the world. With the pipeline of RNA products in various phases of preclinical and clinical development becoming increasingly large, outsourcing requirements continue to grow.

Between 2025 and 2026, CDMOs increased their use of automated manufacturing equipment, AI-based process optimization technologies, and quality control technologies.

Restraints: Complexity of manufacturing and regulatory requirements compliance burden.

The production of RNA therapeutics is associated with complicated infrastructure, analysis, quality control measures, and many regulatory issues. Complying with GMP during development and commercial production entails certain limitations. The complications involved in the logistics, availability of raw materials, and standardization of processes can result in rising production expenses and scalability challenges for some market players. Technical complexity of RNA synthesis, purification, formulation, and storage increases the burden of RNA manufacturing. Small-scale biotech companies find it harder to cope with such requirements due to resource limitations and hence become more dependent on the expertise of CDMOs.

Issues related to quality manufacturing, process validation, and product consistency were of major importance for regulatory agencies in 2025-2026.

Opportunities: Commercialization of RNA platform technologies for next-generation RNA.

RNA-based drug delivery platforms such as circular RNA, self-amplifying RNA, and oligonucleotides present many advantages to CDMOs. Advancements in success rate, expansion of therapeutic use cases, and increased spending by the pharmaceuticals are leading to the need for customized service offerings by these organizations. CDMOs that are able to provide end-to-end customized services ranging from discovery through development to manufacturing and commercialization will be well-positioned for growth in a growing market. Advancements in personalized medicine, target therapy, and genetic medications offer possibilities in terms of specialized manufacturing capabilities. In the wake of next-generation RNA technology, there will be a growing demand for better formulations, tests, and manufacturing.

In 2025-2026, the industry players invested in next generation RNA manufacturing technologies and formulations, and manufacturing platforms.

Recent Developments

-

2026: Multiple global CDMOs expanded commercial-scale mRNA and oligonucleotide manufacturing capacity to support late-stage clinical and commercial programs.

-

2026: Several RNA-focused manufacturers invested in AI-enabled process optimization platforms to improve production efficiency and batch consistency.

-

2025: Industry participants announced new lipid nanoparticle manufacturing facilities supporting next-generation RNA therapeutic development.

-

2025: Strategic partnerships between biotechnology innovators and CDMOs increased to accelerate clinical development and commercialization of RNA-based therapies.

RNA Therapeutics CDMO Market Key Players are:

-

Lonza Group

-

Catalent, Inc.

-

Thermo Fisher Scientific Inc.

-

WuXi AppTec

-

Samsung Biologics

-

AGC Biologics

-

Recipharm AB

-

CordenPharma International

-

Curia Global, Inc.

-

Evonik Industries AG

-

Aldevron LLC

-

Nitto Avecia

-

Rentschler Biopharma

-

BioNTech SE

-

eTheRNA manufacturing

-

BioSpring GmbH

-

TriLink BioTechnologies

-

GenScript ProBio

-

FUJIFILM Diosynth Biotechnologies

-

Wacker Biotech GmbH

RNA Therapeutics CDMO Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD15.90 Billion |

| Market Size by 2035 | USD 40.68 Billion |

| CAGR | CAGR of 9.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By RNA Type (mRNA Therapeutics & Vaccines, siRNA Therapeutics, Antisense Oligonucleotides (ASO), circRNA & Other RNA Modalities) • By Service Type (Process Development & Analytical Services, Clinical Manufacturing, Commercial Manufacturing & Fill-Finish) • By Application (Infectious Diseases, Oncology, Rare Diseases & Genetic Disorders) • By End User (Biopharmaceutical Companies, Academic & Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lonza Group, Catalent, Inc., Thermo Fisher Scientific Inc., WuXi AppTec, Samsung Biologics, AGC Biologics, Recipharm AB, CordenPharma International, Curia Global, Inc., Evonik Industries AG, Aldevron LLC, Nitto Avecia, Rentschler Biopharma, BioNTech SE, eTheRNA manufacturing, BioSpring GmbH, TriLink BioTechnologies, GenScript ProBio, FUJIFILM Diosynth Biotechnologies, Wacker Biotech GmbH. |

Frequently Asked Questions

The RNA Therapeutics CDMO Market was valued at USD 15.80 Billion in 2025.

The market is projected to reach USD 40.68 Billion by 2035.

The market is expected to expand at a CAGR of 9.86% during the forecast period.

North America dominated the global market with a 46.00% revenue share in 2025.

mRNA Therapeutics & Vaccines accounted for the largest revenue share of 48.00% in 2025.

Get in Touch