Rare Disease Genetic Testing Market Report Scope & Overview:

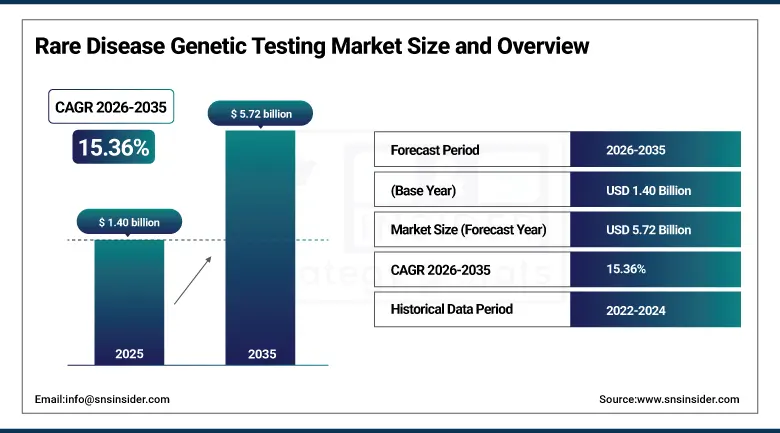

The Rare Disease Genetic Testing Market was valued at USD 1.40 Billion in 2025 and is expected to reach USD 5.72 Billion by 2035, growing at a CAGR of 15.36% from 2026–2035.

The Rare Disease Genetic Testing Market is witnessing tremendous growth due to the rising requirement for early and precise genetic testing among the estimated 300+ million individuals affected by rare diseases around the world, of which an estimated 80% of cases are believed to have a genetic component. The development of next-generation sequencing techniques, the decreasing costs of genome and exome sequencing, the increasing scope of newborn screening initiatives, and the incorporation of artificial intelligence for analysis of genetic data are significantly enhancing diagnostic precision, minimizing the duration of the diagnostic journey, and facilitating timely treatment with specific drugs. Increased governmental allocation of funds for rare disease research, expanded national newborn screening panels, and the rising interest of pharmaceutical companies in the development of orphan drugs are driving market demand.

Clinical data consistently demonstrates that accurate rare disease genetic diagnosis – enabled by next-generation sequencing technologies – reduces the average diagnostic odyssey from 4–6 years to under 12 months for many genetic disorders, delivering both clinical and economic value through earlier treatment initiation, reduced unnecessary diagnostic workup costs, and improved patient quality of life outcomes.

Market Size and Forecast:

-

Market Size in 2025: USD 1.40 Billion

-

Market Size by 2035: USD 5.72 Billion

-

CAGR: 15.36% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Rare Disease Genetic Testing Market - Request Free Sample Report

Rare Disease Genetic Testing Market Trends:

-

Fast reduction in costs of whole-genome sequencing driving adoption of sequencing in rare disease diagnostic applications at academic medical centers and reference labs.

-

Development of artificial intelligence and machine learning technologies to aid genomics data interpretation platforms in enhancing diagnosis and variant classification.

-

Broadening of national newborn screening programs to include NGS panels for diagnosis of rare genetic conditions treatable through early intervention.

-

Pharmaceutical companies increasing investment in companion diagnostics and patient identification services in rare disease clinical trial research and orphan drugs.

-

Use of multiomic testing in diagnosis of rare diseases as part of genomics, transcriptomics, and proteomics testing to increase diagnostic sensitivity.

-

More provision of genetic counseling services in relation to rare disease genetic testing to provide information about risks of heredity.

-

Growth of consumer- and patient-driven rare disease genetic testing services in the form of direct-to-consumer genetic testing platforms.

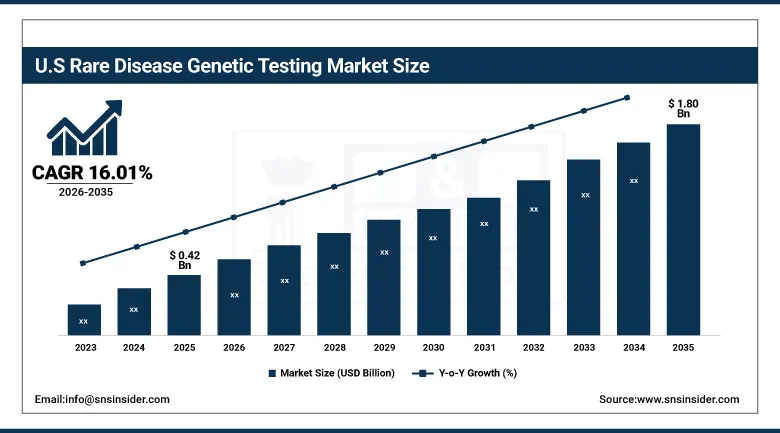

U.S. Rare Disease Genetic Testing Market was valued at USD 0.42 billion in 2025 and is expected to reach USD 1.80 billion by 2035, registering a CAGR of 16.01% during 2026–2035.

The U.S. Rare Disease Genetic Testing Market enjoys the strong impetus provided by federal programs such as the National Institutes of Health’s Undiagnosed Diseases Program, FDA’s financial incentives to treat rare pediatric diseases, and the overall framework provided by the Orphan Drug Act. These efforts are supported by the country’s highly developed genomics medicine ecosystem, comprising cutting-edge genetic testing laboratories, bioinformatics centers, and academic medical facilities offering programs focused on rare diseases. Increased coverage by health insurance providers for genetic testing and physician knowledge about the value of genetic testing in diagnosing rare conditions are major growth factors for the market.

The U.S. Department of Defense's Congressionally Directed Medical Research Programs (CDMRP) and NIH's All of Us Research Program are generating large-scale genomic datasets that are advancing rare disease gene discovery, creating a compounding positive feedback loop between research investment and clinical genetic testing demand that is expected to sustain above-average U.S. market growth through 2035.

Rare Disease Genetic Testing Market Segment Insights:

-

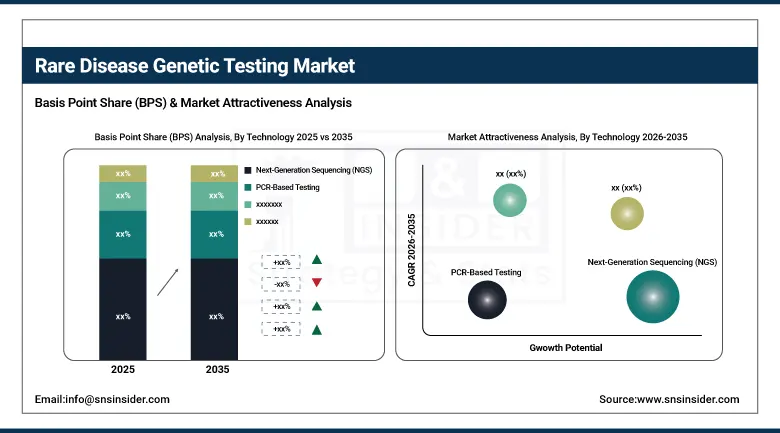

Based on Technology, Next-Generation Sequencing (NGS) accounted for the largest market share (~33.9%) in 2025; Whole Genome Sequencing (WGS) expected to be the fastest-growing segment (CAGR).

-

Based on Specialty, Molecular Genetic Tests accounted for the largest market share in 2025; Biochemical Genetic Tests expected to grow steadily (CAGR).

-

Based on Disease Type, Immunological Disorders accounted for the largest market share (~10.5%) in 2025; Endocrine & Metabolism Diseases expected to be the fastest-growing segment (CAGR).

-

Based on End-Use, Research Laboratories & CROs accounted for the largest market share in 2025; Diagnostic Laboratories expected to be the fastest-growing segment (CAGR: 17.36%).

Rare Disease Genetic Testing Market Segment Analysis:

By Technology, NGS dominates, WGS expected to grow fastest

Next Generation Sequencing (NGS) was the largest contributor to the technology market share, contributing about 33.9% of the market in 2025 due to the capability of conducting multi-genetic variant analysis in large genomic regions at significantly lower costs than before. NGS based panels covering sets of genes associated with different rare diseases can be considered highly economical first-tier genetic tests for patients having symptoms indicating certain rare diseases.

Whole Genome Sequencing (WGS) is projected to generate the highest growth rate through 2035 due to the low cost of genome sequencing which has decreased significantly and will soon become between $200-$500 per sample, making it possible to use as a first line test for undiagnosed rare diseases in academic hospitals. Whole Genome Sequencing is the only technique that can detect all types of genetic variations such as single nucleotide variants, structural variants, and repeat expansions that may remain undetected by targeted panels and WES. The whole genome sequencing approach has been used to develop national diagnostic programs based on WGS in the UK, Australia, and several European countries.

By Disease Type, Immunological Disorders dominate, Endocrine & Metabolism Diseases expected to grow fastest

The Immunological Disorders accounted for the largest disease type market share, estimated at around 10.5%, in 2025. The high prevalence rate of primary immunodeficiency diseases, autoimmune diseases, and complement system disorders with clear genetic origins amenable to genetic testing underlies the large disease type market share. Increasing availability of gene-based and immunotherapy treatments, specific for certain genotypes, will continue to drive significant clinical interest in the need for genetic testing in immunocompromised individuals.

The Endocrine & Metabolism Diseases are forecasted to have the highest CAGR during 2026–2035. Increasing recognition and awareness about inherited metabolic diseases, coupled with rising enzyme replacement therapy (ERT), substrate reduction therapy, and gene therapy, specific for treating such diseases, have been increasing the demand for genetic testing of metabolic diseases. The growing number of newborn screening programs with expanded panels for metabolic diseases is identifying infants affected with metabolic diseases even before the onset of any symptoms, making them eligible for early treatment.

By End-Use, Research Laboratories & CROs dominate, Diagnostic Laboratories expected to grow fastest

The Research Laboratories and CROs segment was dominant in terms of end use during the forecast period, 2025, due to extensive research conducted on rare diseases to understand the physiology of these diseases and their biomarkers. There is a surge in demand for genetic testing among clinical trial studies that require patient stratification based on genetics, development of companion diagnostics, and tracking the response to the treatment using biomarkers.

The Diagnostic Laboratories segment will witness the highest CAGR of around 17.36% throughout the forecast period, 2035. A growing number of patients being referred for rare disease genetic testing through hospital-based genetic laboratories, rare disease clinics, and general practitioners' genetic counseling services have resulted in an increase in demand for genetic tests among diagnostic laboratories. Strategic collaborations between diagnostic laboratory providers and genetic testing platforms will enhance the test menu and expand geographical coverage.

Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

United Kingdom |

30% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

UAE |

34% |

|

Latin America |

Brazil |

50% |

North America Rare Disease Genetic Testing Market Insights

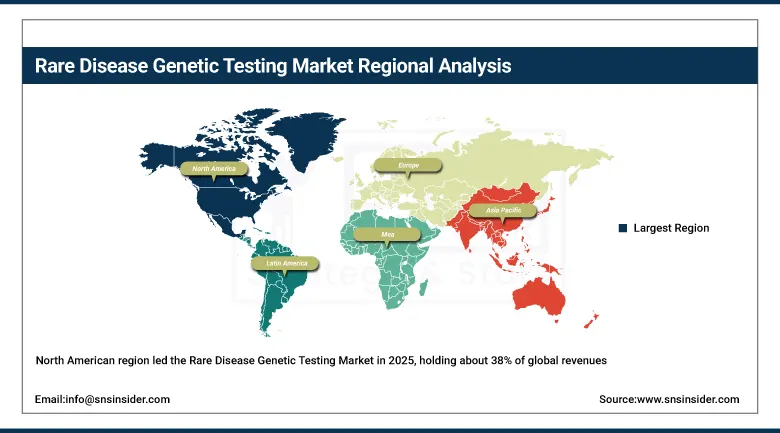

The North American region led the Rare Disease Genetic Testing Market in 2025, holding about 38% of global revenues. The U.S. boasts the most advanced regulatory structure for rare diseases globally, having FDA Orphan Drug Designation and Breakthrough Therapy options to promote companion diagnostic development. The cluster of rare disease speciality care centers, superior genetic testing reference laboratories, and genomics-focused biotechnology companies keeps the U.S. at the forefront of the market. National Institutes of Health (NIH), Congressionally Directed Medical Research Programs (CDMRP), and Undiagnosed Diseases Program investments drive consistent research support.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Rare Disease Genetic Testing Market Insights

Europe held around 30% of the global share of Rare Diseases Genetic Testing Market in 2025. The existence of European Reference Networks for rare diseases, EU's framework for orphan medicinal products, and rare diseases diagnostics programs in countries like the UK, France, Germany, and the Netherlands is an organized drive towards using genetic testing. The 100,000 Genomes Project by the UK and the NHS Genomic Medicine Service being conducted by Genomics England mark important national initiatives in genomic medicine leading to the adoption of WGS in diagnosing rare diseases.

Asia Pacific Rare Disease Genetic Testing Market Insights

Asia Pacific is expected to register the fastest CAGR during the forecast period, driven by rapidly expanding government-funded rare disease genomics programs in China, Japan, and South Korea, growing healthcare infrastructure investment in emerging Asian economies, and increasing awareness of genetic testing among rare disease patient communities. China's national genomics initiatives and India's expanding genetic counseling infrastructure are creating significant new market opportunities. The large and still-largely-undiagnosed rare disease patient population across Asia represents a substantial untapped diagnostic market.

Middle East & Africa and Latin America Rare Disease Genetic Testing Market Insights

The Middle East & Africa and Latin America Rare Disease Genetic Testing Markets are emerging segments with growth driven by increasing government recognition of rare disease healthcare needs, growing patient advocacy organization activity, and expanding international genomic laboratory partnerships extending testing access. Gulf Cooperation Council nations are investing in national precision medicine programs incorporating genetic testing capabilities. Brazil's growing rare disease patient registry infrastructure and public health system genetic testing provisions are creating a foundation for sustained market growth.

Rare Disease Genetic Testing Market Growth Drivers:

-

Growing prevalence of rare disease diagnosis and advancing genomic sequencing technologies enabling scalable genetic testing

The key growth factor in the Rare Disease Genetic Testing Market is the synergistic effect of increasing awareness about rare diseases' prevalence – where over 300 million individuals globally are impacted by rare diseases – alongside the swift development of next-generation sequencing platforms that make whole-genome sequencing financially and technologically viable for routine use in clinics. This confluence of decreasing cost barriers, enhanced genomic data analysis capabilities driven by artificial intelligence, and growing proof of concept regarding the efficacy of genetic testing in rare disease care is generating multiple layers of demand for genetic testing services for clinical, research, and pharmaceutical purposes.

In addition, the US FDA's approval of more than 100 gene therapy products and innovative genomic drugs during 2020-2025, several of which require genetic testing for patient eligibility, will open up an entirely new revenue stream for rare disease genetic testing companies outside of their existing diagnostic business model, making genetic testing a mandatory precursor step before administering any form of treatment.

Rare Disease Genetic Testing Market Restraints:

-

High testing costs and limited reimbursement coverage restricting patient access in many markets

One of the major restraints in the development of the Rare Disease Genetic Testing Market includes the expensive nature of comprehensive genome testing, specifically Whole Genome Sequencing and Whole Exome Sequencing, coupled with irregular and insufficient insurance coverage for genetic tests in many countries' healthcare setups. For individuals living in regions without an existing setup for reimbursement for rare diseases genetic tests, the expenses involved in conducting the test are prohibitively high, thus hindering patient accessibility to diagnosis. Another aspect of the use of genetic tests, which poses challenges for utilization, includes their complicated results.

Rare Disease Genetic Testing Market Opportunities:

-

Whole genome sequencing as first-line diagnostic tool and AI-powered variant interpretation enabling precision diagnosis

The maturation of whole genome sequencing as a first-line diagnostic tool for rare diseases represents a transformative growth opportunity, replacing the traditional lengthy sequential testing approach with a single comprehensive test that can simultaneously detect all classes of genetic variation. AI-powered variant interpretation platforms that can classify variants of uncertain significance, integrate phenotypic data with genomic findings, and leverage population-scale genomic databases are dramatically improving diagnostic yield and reducing the proportion of inconclusive results. The establishment of national WGS-based rare disease diagnostic programs by governments in the UK, Australia, and European nations is creating large-scale institutional procurement demand that is expected to accelerate global adoption of WGS as a clinical diagnostic standard.

Recent Developments:

-

2026: Multiple leading rare disease genetic testing laboratories announced expansions of their AI-powered variant interpretation capabilities, incorporating phenotype-genotype correlation algorithms trained on large rare disease patient cohorts to improve diagnostic yield. Several national healthcare systems in Europe formalized reimbursement frameworks for whole-genome sequencing as a first-line diagnostic tool for undiagnosed rare disease patients, substantially expanding clinical testing volumes.

-

2025 (April): GeneDx launched an enhanced version of its whole-exome sequencing platform incorporating improved structural variant detection and AI-powered phenotype integration, enabling higher diagnostic yield for patients with previously undiagnosed rare diseases. The platform demonstrated a 35% improvement in diagnosis rate for ultra-rare neurodevelopmental conditions in clinical validation studies.

-

2024 (August): Ambry Genetics launched ExomeReveal, a multiomic exome sequencing test integrating RNA analysis to enhance rare disease detection. Unlike conventional DNA-based sequencing, ExomeReveal performs functional RNA studies, resolving variants of uncertain significance and improving diagnostic accuracy, with initial trials showing clinically meaningful results across rare disease patient cohorts.

Rare Disease Genetic Testing Market Key Players:

-

Blueprint Genetics (Quest Diagnostics)

-

Ambry Genetics

-

Centogene N.V.

-

3billion, Inc.

-

Eurofins Scientific

-

BGI Group

-

Revvity (PerkinElmer)

-

Agilent Technologies, Inc.

-

Illumina, Inc.

-

Pacific Biosciences (PacBio)

-

Oxford Nanopore Technologies

-

Thermo Fisher Scientific

Rare Disease Genetic Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.40 Billion |

| Market Size by 2035 | USD 5.72 Billion |

| CAGR | CAGR of 15.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Next-Generation Sequencing (NGS), Whole Exome Sequencing (WES), Whole Genome Sequencing (WGS), PCR-Based Testing, Chromosomal Microarray Analysis, Sanger Sequencing, Karyotyping, Others) • By Specialty (Molecular Genetic Tests, Chromosomal Genetic Tests, Biochemical Genetic Tests) • By Disease Type (Immunological Disorders, Endocrine & Metabolism Diseases, Cardiovascular Disorders, Neurological Disorders, Hematology & Oncology, Musculoskeletal Disorders, Others) • By End-Use (Research Laboratories & CROs, Hospitals & Clinics, Diagnostic Laboratories |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GeneDx, LLC, Blueprint Genetics (Quest Diagnostics), Invitae Corporation, Ambry Genetics, Baylor Genetics, Centogene N.V., 3billion, Inc., Eurofins Scientific, BGI Group, Revvity (PerkinElmer), Agilent Technologies, Inc., Illumina, Inc., Pacific Biosciences (PacBio), Oxford Nanopore Technologies, Thermo Fisher Scientific |

Frequently Asked Questions

North America dominated the Rare Disease Genetic Testing Market in 2025, accounting for approximately 38% of global market revenue.

The Next-Generation Sequencing (NGS) segment dominated the Rare Disease Genetic Testing Market in 2025, accounting for approximately 33.9% of technology segment revenue.

Growing global prevalence of rare disease recognition and rapidly advancing next-generation sequencing technologies enabling scalable, cost-effective genetic testing that is improving rare disease diagnosis rates and supporting treatment access.

The Rare Disease Genetic Testing Market was valued at USD 1.40 billion in 2025.

The Rare Disease Genetic Testing Market is expected to grow at a CAGR of 15.36% from 2026 to 2035.

Get in Touch