Vessel Sealing Devices Market Report Scope and Overview:

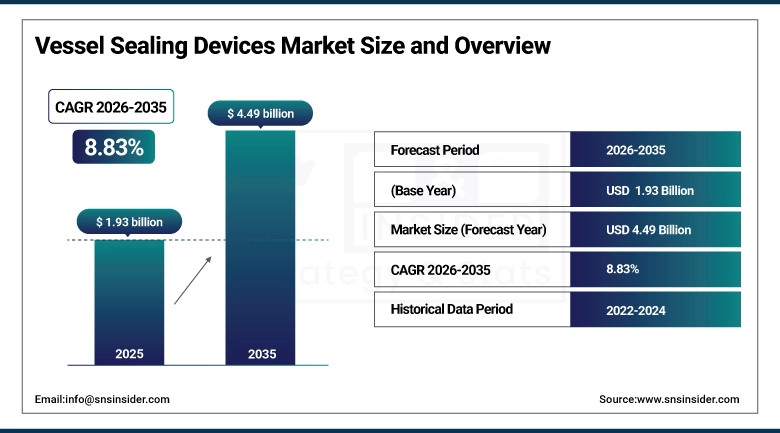

The Vessel Sealing Devices Market was estimated at USD 1.93 billion in 2025 and is expected to reach USD 4.49 billion by 2035 and grow at a CAGR of 8.83% over the forecast period of 2026-2035.

Over the last couple of decades, there has been a paradigm shift in the management of hemorrhage associated with surgery, and the key to this change has been the advent of vessel sealing devices. While the previous generation of surgeons depended on sutures, staples, and rudimentary electrosurgical instruments to control hemorrhage, modern day operating theatres feature complex energy-based devices that can seal vessels as large as 7 mm in diameter using a single device application without requiring any further suture or ligature placement. These features not only make such devices clinically handy; they represent a true step forward in the realm of surgery. Decreased operative times, decreased intraoperative blood loss, decreased complication rates, and enhanced recovery periods are some of the benefits that have been attributed to the use of advanced vessel sealing devices across general, gynecological, oncological, and urological surgeries.

Global demand for vessel sealing devices is being driven by forces that show no signs of abating. Surgical procedure volumes are rising in virtually every major market, fueled by aging populations, growing rates of chronic conditions requiring surgical intervention, and improving access to healthcare in emerging economies. At the same time, the shift toward minimally invasive and robotic surgical techniques is accelerating the adoption of advanced energy instruments, since laparoscopic and robotic platforms specifically benefit from the compact, multifunctional design of modern vessel sealing systems. The global market is also receiving a push from the supply side, as leading manufacturers continue to introduce next generation platforms with enhanced jaw configurations, improved tissue feedback algorithms, and extended sealing capabilities.

Regulatory approvals have been an important catalyst in recent years. The FDA's clearance of several new generation vessel sealing platforms in 2024 and 2025 has strengthened the competitive product landscape and signaled continued agency support for innovation in energy based surgical instruments, further bolstering institutional and investor confidence in the category.

Market Size and Forecast

-

Market Size in 2025: USD 1.93 Billion

-

Market Size by 2035: USD 4.49 Billion

-

CAGR: 8.83% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get more information on Vessel Sealing Devices Market - Request Free Sample Report

Vessel Sealing Devices Market Trends

-

The incorporation of vessel sealing devices within the robotic surgical systems, especially the da Vinci robotic platform by Intuitive Surgical, which expands the use of advanced vessel sealing devices to the robotic-assisted laparoscopy.

-

The development of multi-purpose devices incorporating vessel sealing capabilities, along with dissection, cutting, and specimen extraction in one device, hence increasing the efficiency of procedures.

-

The increased use of ultrasonic vessel sealing devices in tissue-sparing procedures where surgeons need both dissection and sealing during surgery.

-

Increasing shift of surgical volumes from hospital inpatient settings to ambulatory surgical centers, driven by cost containment pressures, patient preference for outpatient procedures, and advances in technique that enable same day surgery for a growing range of indications.

-

Growing investments by leading medical device companies in next generation tissue feedback and impedance monitoring technology that enables real time vessel sealing quality assessment during procedures.

-

Expansion of vessel sealing device adoption in emerging markets across Asia Pacific and Latin America as surgical volumes grow, healthcare infrastructure modernizes, and access to advanced surgical technologies improves.

-

Rising focus on disposable and single use vessel sealing instruments driven by infection control concerns, reprocessing cost considerations, and the clinical risk management priorities of large hospital systems.

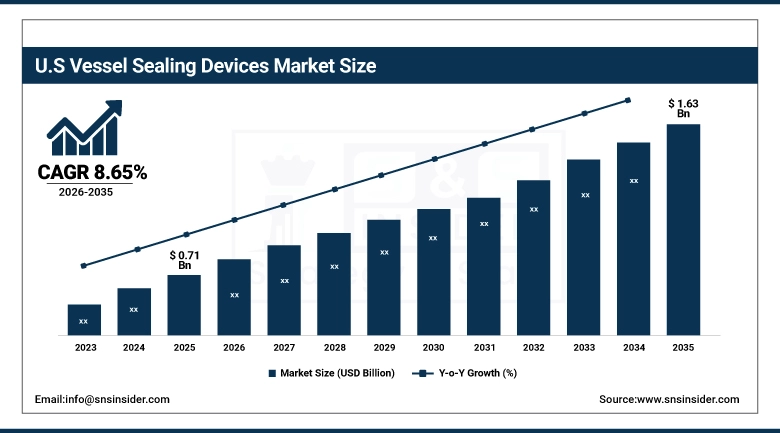

The U.S. Vessel Sealing Devices Market was valued at USD 0.71 billion in 2025 and is expected to reach USD 1.63 billion by 2035, registering a CAGR of 8.65% during 2026 to 2035.

The USA ranks as the world's biggest market for vessel sealing systems as well as one of the countries with the highest levels of technological sophistication. The reasons why the USA is the biggest single market can be traced back to the fact that the country conducts millions of inpatient and outpatient operations each year. The USA has a health care delivery system that is highly innovative when it comes to introducing advancements in surgery technologies. The introduction of novel energy instrument platforms in US hospitals and ambulatory surgical facilities is attributed to clinical leadership, surgeon preference, and an environment where positive changes in the results achieved matter most. In terms of the technology used, the most popular vessel sealing systems in the US include Medtronic's LigaSure and Johnson & Johnson's Enseal.

The ongoing shift from inpatient to outpatient surgery in the U.S. is one of the most consequential structural trends affecting the vessel sealing devices market. Procedures that were once performed exclusively in hospital operating rooms — including cholecystectomies, hysterectomies, thyroidectomies, and certain oncological resections — are increasingly being performed in ambulatory surgical centers where operative time and equipment efficiency are at a premium. This migration directly benefits vessel sealing device utilization rates and is expected to be a sustained driver of market growth through 2035.

Vessel Sealing Devices Market Segment Analysis

-

Based on Product Type, Bipolar Vessel Sealing Devices accounted for the largest market share in 2025, driven by their broad clinical applicability and established market penetration. Ultrasonic Vessel Sealing Devices are expected to register the fastest CAGR through 2035.

-

Based on Application, General Surgery accounted for the largest market share in 2025, reflecting the high volume of laparoscopic and open procedures performed globally. Oncological Surgery is expected to be the fastest growing application segment.

-

Based on End User, Hospitals accounted for the largest market share in 2025. Ambulatory Surgical Centers are expected to register the fastest CAGR of 9.38%, driven by the global shift toward outpatient surgical care.

By Product Type, Bipolar Vessel Sealing Devices segment dominates the Vessel Sealing Devices Market, Ultrasonic Vessel Sealing Devices segment expected to grow fastest

The bipolar vessel sealing segment dominated the market in 2025. There were multiple factors responsible for its large market share, including technological advancements and high clinical utility. In bipolar vessel sealing technology, surgical instruments apply controlled electrical energy between two jaws of the device to denature the collagen of the vessel wall and create a seal that is strong enough to withstand several times higher burst pressures compared to the average blood pressure level. High control accuracy made possible due to the current technology advances enables a surgeon to produce high-quality seals, even when there is a limited working space. Medtronic's LigaSure series and Ethicon's Enseal are leading brands in this segment, and their adoption on a wide scale for various surgeries, including general, gynecological, and colorectal procedures, has set the bipolar vessel sealing technology as the gold standard among laparoscopic surgeries.

Ultrasonic vessel sealing devices are positioned to record the fastest CAGR from 2026 through 2035. The clinical rationale for this growth is compelling. Ultrasonic systems generate mechanical energy through high frequency vibration of the active blade, creating heat through tissue friction rather than direct electrical current delivery to the patient. This mechanism offers two important clinical advantages in certain settings: minimal lateral thermal spread, which is particularly valuable near sensitive structures such as nerves and ducts, and simultaneous cutting and coagulation with a single instrument. These characteristics make ultrasonic devices the preferred choice for thyroid and parathyroid surgery, certain cancer resections near critical neural structures, and fine dissection in anatomically complex fields. As surgical oncology and head and neck surgery volumes grow globally, demand for ultrasonic vessel sealing platforms is expected to scale correspondingly.

By Application, General Surgery segment dominates the Vessel Sealing Devices Market, Oncological Surgery segment expected to grow fastest

General surgery accounted for the largest application segment of the vessel sealing devices market in 2025. The category encompasses the highest volume surgical procedures in which vessel sealing devices are routinely deployed: laparoscopic cholecystectomy, appendectomy, colorectal resection, hernia repair with tissue dissection, and bariatric surgery. In the United States alone, millions of these procedures are performed annually across hospital systems and ambulatory surgical centers. The laparoscopic approach has become the default surgical strategy for a broad range of abdominal conditions, and advanced vessel sealing instruments are integral to enabling efficient dissection, hemostasis, and tissue management through the narrow working channels of laparoscopic trocars. As surgical volumes in this category continue to grow and laparoscopic adoption expands in emerging markets, general surgery will remain the largest demand source for vessel sealing device manufacturers.

Among all application areas, oncological surgery is projected to witness the highest CAGR between 2026 and 2035. According to data released by the World Health Organization, global cancer diagnoses have steadily increased, and the trend is set to continue, reaching up to 35 million cases each year by 2050. In addition, surgeries serve an essential purpose in oncology treatment as a primary therapy or as a complementary technique for reducing tumor mass, which is performed in the case of various tumors, such as colorectal, hepatic, gynecological, urological, thyroid, and breast cancers. For more complex oncological surgeries, where lymph node dissection or resection of vessels occurs, the importance of advanced vessel sealing technology becomes especially relevant because of its capability to precisely and quickly handle a wide range of vessels. An increasing number of surgical oncology departments in emerging countries and cancer incidence growth contribute to this development driver in the market under review.

By End User, Hospitals hold the largest share, Ambulatory Surgical Centers expected to grow at the fastest CAGR of 9.38%

Hospitals accounted for the largest end user segment in 2025, reflecting the reality that the highest complexity and highest volume surgical procedures are still performed in hospital inpatient and outpatient operating rooms. Large academic medical centers, regional hospital systems, and specialized surgical centers within hospitals represent the core institutional customer base for vessel sealing device manufacturers. Hospital group purchasing organizations play a significant role in procurement, and the major device manufacturers maintain substantial contract and clinical support infrastructure dedicated to winning and retaining GPO positioning. For high acuity procedures including major oncological resections, complex pelvic surgery, and robotic assisted operations, the hospital operating room remains the dominant and appropriate setting.

Ambulatory surgical centers are expected to grow at the fastest CAGR of 9.38% from 2026 to 2035, making them the most dynamic end user segment in the market. The global shift toward outpatient surgical care is one of the defining structural trends reshaping surgical medicine. Payers are actively incentivizing the migration of appropriate procedures to ASC settings because the cost of delivering surgical care in a freestanding ambulatory center is substantially lower than in a hospital outpatient department. Surgeons are increasingly willing to perform laparoscopic procedures — including cholecystectomies, hysterectomies, and urological interventions — in the ASC environment as anesthesia and recovery protocols have advanced to make same day discharge safe and routine for a broader patient population. Vessel sealing devices, by enabling faster and more efficient hemostasis and tissue management, are a key enabler of the abbreviated surgical timelines that make outpatient surgery economically and clinically feasible.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~85% |

|

Europe |

Germany |

~29% |

|

Asia Pacific |

China |

~43% |

|

Middle East and Africa |

UAE |

~31% |

|

Latin America |

Brazil |

~50% |

North America Vessel Sealing Devices Market Insights

North America led the Vessel Sealing Devices market in 2025 with a market share of approximately 42.85%, the largest of any global region. The United States accounts for the vast majority of North American demand. Its healthcare system is characterized by high surgical procedure volumes, early and enthusiastic adoption of advanced surgical technology, and well-established reimbursement frameworks for energy based surgical instruments. American surgeons were among the earliest adopters of advanced vessel sealing platforms and continue to drive significant clinical demand for next generation iterations. The U.S. ambulatory surgery market is one of the most developed in the world, creating a structural tailwind for vessel sealing device utilization as outpatient procedure volumes grow. Canada contributes meaningful market demand through its publicly funded provincial healthcare systems, which have been progressively increasing access to minimally invasive surgical options.

Asia Pacific Vessel Sealing Devices Market Insights

Asia Pacific is the fastest growing regional market for vessel sealing devices, with an expected CAGR of 9.67% from 2026 through 2035. Several overlapping forces are driving this trajectory. Rapidly aging populations across China, Japan, and South Korea are generating rising surgical procedure volumes across general, gynecological, and oncological specialties. Healthcare infrastructure investment is expanding access to advanced surgical facilities in tier two and tier three cities in China, India, and across Southeast Asia, opening entirely new patient populations to minimally invasive surgery. Medical tourism flows in countries like Thailand, India, and Malaysia are also contributing to surgical volume growth. China's domestic medical device manufacturing sector has produced increasingly competitive vessel sealing systems at lower price points, which is accelerating adoption in cost sensitive hospital settings while also intensifying competitive dynamics for multinational manufacturers.

Europe Vessel Sealing Devices Market Insights

The region of Europe accounted for a considerable market share for Vessel Sealing Devices in 2025, with Germany, the United Kingdom, France, and Italy being the leading country-level markets within the segment. The operating conditions for surgical devices in Europe are known to be highly advanced, requiring CE markings and MDR regulation. The presence of a surgical innovation culture that relies strongly on evidence-based methods adds value to the European region as well. There are several hospitals and academic medical centers in Germany that make good use of advanced vessel sealing technology due to Germany's surgical culture and large number of surgeries performed every year.

Middle East and Africa and Latin America Vessel Sealing Devices Market Insights

The Middle East and Africa and Latin America markets represent important emerging growth frontiers for the vessel sealing devices industry. The Gulf Cooperation Council countries, particularly the UAE and Saudi Arabia, are investing heavily in world class hospital infrastructure and have demonstrated strong willingness to adopt advanced surgical technology in line with their national healthcare modernization programs. Brazil leads the Latin American market, supported by a high volume surgical care sector and growing private hospital network that is actively investing in minimally invasive surgical capability. Argentina, Colombia, and Mexico are also expanding their surgical infrastructure. Both regions are expected to record above average market growth through 2035 as healthcare access improves, surgical volumes increase, and advanced energy instrument adoption reaches a broader share of the surgical facility base.

Vessel Sealing Devices Market Growth Drivers:

Rising global adoption of minimally invasive surgery and growing surgical procedure volumes driving sustained market expansion

The primary and most durable growth driver of the vessel sealing devices market is the sustained global rise in minimally invasive surgical procedure volumes. Laparoscopic and robotic surgery platforms have become the standard of care for a growing range of indications across general, gynecological, urological, and thoracic surgery, and advanced vessel sealing instruments are a necessary enabling technology for these approaches. Every new laparoscopic surgical program established in an emerging market hospital, every robotic surgery system installed at a regional medical center, and every procedure migrated from open to minimally invasive technique represents incremental demand for vessel sealing devices. The global aging population is a structural multiplier: older patients undergo significantly higher rates of surgical intervention for conditions ranging from colorectal disease to gallbladder conditions to cancer, all of which are among the highest volume indications for vessel sealing instrument use. The result is a demand base that grows organically with demographic trends, independent of any additional market development activity by manufacturers.

Surgical outcome data consistently confirms that the use of advanced vessel sealing technology is associated with reduced intraoperative blood loss, shorter operative times, fewer complications related to hemorrhage, and faster patient recovery compared to conventional techniques. These outcomes improvements translate directly into cost savings for hospital systems and healthcare payers, creating an economic rationale for procurement that complements the clinical rationale.

Vessel Sealing Devices Market Restraints

High device cost and reprocessing complexity creating adoption barriers in resource constrained healthcare settings

A meaningful constraint on the vessel sealing devices market is the relatively high acquisition cost of advanced energy based sealing systems, particularly next generation platforms from leading multinational manufacturers. For hospitals in developing markets with limited capital equipment budgets, the upfront cost of adopting advanced vessel sealing technology can be a genuine barrier, particularly when lower technology alternatives are available at significantly lower price points. The ongoing debate between disposable and reusable instrument models also creates complexity in procurement decisions: reusable systems have lower per procedure consumable costs but carry reprocessing expenses and the risk of performance degradation across sterilization cycles, while single use systems offer consistent performance but generate ongoing supply costs. In markets where healthcare reimbursement for advanced energy instruments is limited or absent, hospital administrators may resist adoption despite strong clinical advocacy from surgical teams.

Vessel Sealing Devices Market Opportunities

Robotic surgery integration, emerging market expansion, and next generation sealing platforms creating significant growth opportunities

The integration of vessel sealing technology into next generation robotic surgical platforms is one of the most strategically significant market opportunities for the vessel sealing devices industry through 2035. The global robotic surgery installed base is growing at a remarkable pace, with Intuitive Surgical's da Vinci system expanding its presence and new competitive platforms from Medtronic, Johnson and Johnson, CMR Surgical, and Chinese manufacturers entering clinical use. Each new robotic surgical platform creates fresh demand for purpose built vessel sealing instruments engineered to operate within the specific kinematic and energy delivery constraints of that platform. Manufacturers that establish preferred instrument status on high volume robotic platforms position themselves for sustained recurring revenue from a rapidly growing installed base. In emerging markets, the combination of growing surgical volumes, improving economic conditions, and increasing government investment in hospital modernization is creating an addressable market for vessel sealing devices that simply did not exist a decade ago and that represents genuine greenfield opportunity for both multinational and local manufacturers.

Recent Developments:

-

Feb 2025: Medtronic was awarded FDA clearance for its LigaSure XP device, which incorporated an innovative jaw design for efficient dissection and vessel sealing in anatomically restricted areas. FDA clearance strengthened Medtronic's position in the energy surgical instruments market segment and increased the ability of LigaSure to address the needs of surgeons operating in difficult anatomical sites.

-

Aug 2024: Olympus Corporation received FDA clearance for its POWERSEAL Sealer and Divider, which included novel features related to energy delivery and vessel sealing within the bipolar vessel sealing category. FDA clearance represented an important competitor entry into the bipolar vessel sealing market space.

Vessel Sealing Devices Market Key Players

-

Medtronic plc

-

Johnson and Johnson (Ethicon)

-

Olympus Corporation

-

B. Braun Melsungen AG

-

Stryker Corporation

-

Becton, Dickinson and Company

-

Intuitive Surgical Inc.

-

KLS Martin Group

-

Erbe Elektromedizin GmbH

-

Integra LifeSciences Holdings Corporation

-

CONMED Corporation

-

Teleflex Incorporated

-

Applied Medical Resources Corporation

-

LiNA Medical

-

Bowa Electronic GmbH and Co. KG

-

Richard Wolf GmbH

-

Aesculap AG

-

Karl Storz GmbH and Co. KG

-

Microline Surgical Inc.

-

AtriCure Inc.

Vessel Sealing Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.93 Billion |

| Market Size by 2035 | USD 4.49 Billion |

| CAGR | CAGR of 8.83% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Bipolar Vessel Sealing Devices, Ultrasonic Vessel Sealing Devices, Others) • By Application (General Surgery, Gynecology, Oncological Surgery, Urological Surgery, Others) • By End User (Hospitals, Ambulatory Surgical Centers, Clinics and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic plc, Johnson and Johnson (Ethicon), Olympus Corporation, B. Braun Melsungen AG, Stryker Corporation, Becton, Dickinson and Company, Intuitive Surgical Inc., KLS Martin Group, Erbe Elektromedizin GmbH, Integra LifeSciences , Holdings Corporation, CONMED Corporation, Teleflex Incorporated, Applied, Medical Resources Corporation, LiNA Medical, Bowa Electronic GmbH and Co. KG, Richard Wolf GmbH, Aesculap AG, Karl Storz GmbH and Co. KG, Microline Surgical Inc., AtriCure Inc. |

Frequently Asked Questions

The Vessel Sealing Devices Market is expected to grow at a CAGR of 8.83% from 2026 to 2035.

The Vessel Sealing Devices Market was valued at USD 1.93 billion in 2025.

The rising global adoption of minimally invasive and robotic surgical techniques, increasing surgical procedure volumes driven by aging populations and growing chronic disease prevalence, and ongoing technological advancement in energy based vessel sealing platforms are the primary growth drivers.

Bipolar Vessel Sealing Devices dominated the Vessel Sealing Devices Market in 2025, driven by their broad clinical applicability, established market penetration across laparoscopic and open surgical procedures, and the strong installed base of leading platforms from Medtronic and Johnson and Johnson.

Ambulatory Surgical Centers are expected to register the fastest CAGR of 9.38% from 2026 to 2035, driven by the global structural shift of appropriate surgical procedures from hospital inpatient and outpatient settings to freestanding ambulatory centers where cost efficiency and operational throughput are priorities.

Get in Touch