Inspection Analysis Device Market Key Insights:

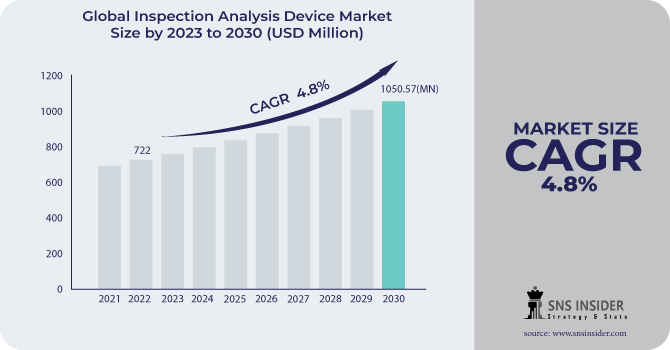

The Inspection Analysis Device Market size was valued at USD 15.44 Billion in 2023 and is expected to grow to USD 26.78 Billion by 2032 and grow at a CAGR of 6.31% over the forecast period of 2024-2032.

The Inspection Analysis Device Market is witnessing significant growth, driven by the rising demand for precision and accuracy across industries such as automotive, electronics, aerospace, and healthcare. As manufacturing becomes more complex, the need for sophisticated inspection solutions to maintain quality control, detect defects, and ensure optimal performance is crucial. Technological innovations like 3D imaging, non-contact sensors, and AI-powered metrology systems are revolutionizing inspection processes, making them faster and more accurate. In industries like semiconductor manufacturing, where defect-free components are essential, sub-nanometer precision is increasingly required, pushing the adoption of advanced inspection tools. For example, the accuracy in PCB inspection has improved defect detection by over 30%, and X-ray metrology for wafer inspection now enables detection at sub-nanometer levels, fueling market growth.

Get More Information on Gaming Hardware Market - Request Sample Report

Furthermore, the integration of Industry 4.0 and automation technologies is accelerating the demand for robotic inspection systems and machine vision, which offer faster speeds and greater precision while reducing operational costs. AI-powered inspection devices, for instance, now provide inspection speeds that are up to 40% faster compared to traditional methods, boosting productivity. The market's expansion is also supported by the growing industrialization in emerging economies such as India and China, where the demand for high-performance, affordable inspection systems is on the rise. As these technologies advance and become more embedded in smart factories, the inspection analysis device market is poised for continued growth. This evolution ensures that quality control and inspection processes remain at the forefront of industrial progress, meeting the increasing demand for precision, efficiency, and reliability in manufacturing operations.

Inspection Analysis Device Market Dynamics

Drivers

-

Expansion of the Automotive Sector Driving Demand for Advanced Inspection Devices

The expansion of the automotive sector, particularly through the growth of electric vehicles (EVs) and autonomous vehicles (AVs), is significantly driving the demand for advanced inspection devices. These vehicles require highly sophisticated inspection systems to ensure the reliability, safety, and performance of critical components such as batteries, sensors, and electronic control units. In electric vehicles, precision in battery cell inspection is paramount to avoid risks such as thermal runaway and to ensure efficiency and longevity. Inspection systems capable of evaluating battery performance under various conditions are essential, with technologies like X-ray inspection and 3D imaging becoming increasingly vital in evaluating cell integrity and detecting defects. Additionally, autonomous vehicles rely heavily on sensors such as LiDAR, radar, and camera systems, which require advanced inspection devices to verify the accuracy and functionality of these components. These sensors must be tested for real-time response and reliability in a range of environmental conditions, driving the adoption of AI-powered inspection systems for speed and precision. Furthermore, the automotive manufacturing process itself, with a rising focus on welding and surface finishing applications, demands high-quality inspection systems to ensure components meet stringent safety standards. Machine vision and robotic inspection systems are used to inspect welded joints, check for surface imperfections, and verify the Class A surface quality in vehicle exteriors. This surge in demand for advanced inspection devices is largely attributed to the automotive industry's shift toward more complex manufacturing and stricter regulatory requirements, with technologies that improve speed and accuracy of inspections becoming indispensable. As these innovations continue to shape the automotive landscape, the need for high-performance inspection solutions will only continue to grow.

Restraints

-

Impact of Maintenance and Calibration Costs on the Growth of the Inspection Analysis Device Market

Inspection devices requiring high precision, such as microscopes, coordinate measuring machines (CMMs), and machine vision systems, necessitate regular maintenance and calibration to ensure optimal performance. These devices are sensitive to environmental conditions and wear, which can impact their accuracy and reliability over time. Consequently, periodic maintenance is crucial to ensure continued precision in measurements and defect detection, especially in industries like aerospace, automotive, and electronics. The associated maintenance costs can be significant, particularly for high-end equipment that requires specialized technicians and advanced calibration tools. Some devices may need costly replacement parts or involve complex procedures for calibration, further driving up expenses. Additionally, companies may need to hire third-party service providers or invest in training internal staff, adding to operational costs. Over time, these ongoing expenses increase the total cost of ownership for businesses relying on these devices. For industries with tight profit margins, such as semiconductors and automotive manufacturing, these costs can discourage smaller companies from upgrading to more advanced systems or adopting newer technologies. This restraint is particularly challenging in emerging markets, where budgetary constraints limit businesses’ ability to invest in sophisticated inspection tools. Despite the clear benefits of high-precision inspection devices, maintenance and calibration costs remain a significant barrier to market growth. Overcoming these challenges is crucial for promoting the adoption of advanced inspection technologies, especially in cost-sensitive industries.

Inspection Analysis Device Market Segment Analysis

By Type

The Machine Vision segment is the dominant segment in the Inspection Analysis Device market, accounting for approximately 26% of the market share in 2023. This segment’s prominence is attributed to its ability to automate the inspection process, enhancing speed, accuracy, and consistency in defect detection, which is essential in industries like automotive, electronics, and pharmaceuticals. Machine vision systems utilize advanced imaging technologies, such as cameras, sensors, and software, to perform high-precision inspections, making them indispensable in quality control and process monitoring. Their capabilities in identifying microscopic defects, measuring components, and verifying product conformity have made them a preferred choice for manufacturers. The increasing demand for automation and the need for real-time, high-quality inspections in modern manufacturing processes further boost the market growth of machine vision systems. As industries continue to prioritize efficiency and precision, the Machine Vision segment is expected to maintain its leading position in the coming years.

By Industry Vertical

The Automotive segment is a key driver in the Inspection Analysis Device market, holding around 30% of the market share in 2023. This dominance is primarily due to the increasing complexity of automotive manufacturing processes and the need for precise quality control. Inspection devices, such as machine vision systems, coordinate measuring machines (CMMs), and 3D scanners, are critical in ensuring the reliability and safety of automotive components like sensors, batteries, and structural parts. With the rise of electric vehicles (EVs) and autonomous vehicles, advanced inspection systems are increasingly required to meet stringent safety and performance standards. Additionally, the automotive sector’s growing emphasis on automation and Industry 4.0 technologies further accelerates the adoption of inspection devices, driving the segment’s strong growth. This trend is expected to continue as the demand for high-quality, defect-free automotive parts rises.

Inspection Analysis Device Market Regional Analysis

North America holds the largest share of around 35% in the Inspection Analysis Device market in 2023, driven by strong industrialization, technological advancements, and robust manufacturing sectors. The region's dominance is primarily due to the high demand for precision-driven inspection devices across industries like automotive, aerospace, healthcare, and electronics. The United States, in particular, is a major contributor to this growth, with its advanced manufacturing landscape and focus on automation and smart manufacturing solutions. The presence of key players such as Cognex Corporation, Keyence Corporation, and Hexagon AB in the region further strengthens its market position. Additionally, Canada’s increasing investment in industries like energy, mining, and automotive manufacturing enhances the demand for advanced inspection systems. The region’s focus on maintaining strict quality control standards, particularly in aerospace and automotive industries, drives the adoption of inspection devices. The combination of technological innovation, strong industrial infrastructure, and regulatory support for high-quality production makes North America a dominant force in the Inspection Analysis Device market.

Asia-Pacific is the fastest-growing region in the Inspection Analysis Device market from 2024 to 2032, driven by rapid industrialization, technological advancements, and increased manufacturing capabilities. Countries like China, Japan, South Korea, and India are leading this growth, with strong investments in sectors such as automotive, electronics, aerospace, and semiconductors. China’s manufacturing boom, in particular, has spurred a significant demand for advanced inspection devices to maintain quality standards in production lines. India’s growing automotive and electronics industries are also contributing to market expansion, with a focus on automation and precision-driven processes. Furthermore, the region’s adoption of Industry 4.0 technologies, such as robotics, AI, and machine vision, is accelerating the demand for sophisticated inspection systems. With increasing infrastructure development and a push towards higher-quality manufacturing standards, Asia-Pacific is poised for significant growth in the inspection analysis device market over the forecast period.

Key Players

Some of the Major Players in Inspection Analysis Device Market with product:

-

Carl Zeiss AG (Industrial CT Scanners, Microscopes)

-

Hitachi High-Technologies Corporation (Scanning Electron Microscopes, TEMs)

-

Nikon Metrology NV (3D Scanners, Coordinate Measuring Machines)

-

Hexagon AB (Coordinate Measuring Machines, Metrology Software)

-

Omron Corporation (Machine Vision Systems, Inspection Sensors)

-

Bruker Corporation (X-Ray Diffraction Instruments, Atomic Force Microscopes)

-

Cognex Corporation (Machine Vision Cameras, Barcode Readers)

-

Keyence Corporation (Laser Scanners, Machine Vision Sensors)

-

Perceptron Inc. (3D Scanning and Measurement Systems)

-

Olympus Corporation (Industrial Microscopes, Non-Destructive Testing Equipment)

-

Shimadzu Corporation (X-Ray Inspection Systems, Spectroscopy Instruments)

-

Thermo Fisher Scientific Inc. (Transmission Electron Microscopes, SEMs)

-

Zetec Inc. (Non-Destructive Testing Systems, Eddy Current Testing Devices)

-

Ametek Inc. (Spectrometers, Thickness Gauges)

-

Hamamatsu Photonics K.K. (Optical Sensors, Photomultiplier Tubes)

-

FARO Technologies Inc. (3D Measurement Devices, Laser Scanners)

-

Mitutoyo Corporation (Coordinate Measuring Machines, Micrometers)

-

Leica Microsystems (Optical Microscopes, Digital Microscopes)

-

Rohde & Schwarz (Network Analyzers, Signal Testing Instruments)

-

Eddyfi Technologies (Non-Destructive Testing Equipment, Ultrasound Inspection Devices)

List of suppliers in the inspection analysis device market, highlighting their contributions to raw materials and components used in manufacturing these devices. These suppliers play crucial roles in the supply chain by providing essential parts and materials to inspection device manufacturers.

1. Optical Components and Lenses Suppliers

-

Schott AG: Supplies optical glass for lenses and imaging components.

-

Edmund Optics: Provides precision optics for cameras and microscopes.

-

Thorlabs Inc.: Specializes in optical components, including lenses and filters.

-

Excelitas Technologies Corp.: Supplies high-performance optical sensors and photonics.

2. Electronic Components Suppliers

-

Analog Devices, Inc.: Supplies sensors, amplifiers, and signal processing ICs.

-

Texas Instruments: Provides microcontrollers, digital signal processors (DSPs), and integrated circuits.

-

STMicroelectronics: Offers imaging sensors and semiconductor solutions.

-

Hamamatsu Photonics K.K.: Supplies photodiodes and light detection modules for inspection systems.

3. Imaging Sensors and Modules Suppliers

-

Sony Semiconductor Solutions Corporation: Produces CMOS and CCD imaging sensors.

-

ON Semiconductor: Provides imaging modules for machine vision and scanning systems.

-

OmniVision Technologies: Specializes in advanced imaging sensors for 3D and vision systems.

4. Non-Destructive Testing (NDT) Equipment Components Suppliers

-

Olympus NDT: Supplies probes, ultrasonic transducers, and other NDT components.

-

Phoenix Inspection Systems: Provides transducers and wedges for ultrasonic testing devices.

5. X-Ray and Radiation Detection Components Suppliers

-

Varian Medical Systems: Supplies X-ray tubes and high-energy imaging components.

-

GE Healthcare: Produces flat-panel detectors and X-ray imaging systems.

-

Teledyne DALSA: Specializes in X-ray imaging sensors for industrial applications.

6. Software and Computing Systems Suppliers

-

NVIDIA Corporation: Supplies GPUs for machine vision and AI-based analysis systems.

-

Intel Corporation: Provides processors and FPGAs for image processing and computational tasks.

-

MathWorks (MATLAB): Supplies software for data analysis and modeling in inspection devices.

7. Mechanical Components and Housing Suppliers

-

igus GmbH: Supplies motion plastics, cable carriers, and bearings for inspection systems.

-

Bosch Rexroth: Provides actuators and precision motion components for machines.

-

THK Co., Ltd.: Supplies linear motion guides and actuators for high-precision inspection devices.

8. Material Suppliers for Device Housings

-

Alcoa Corporation: Supplies lightweight aluminum materials for machine structures.

-

BASF SE: Provides advanced plastics and coatings for durable housing.

-

Covestro AG: Supplies polycarbonate materials for optical device enclosures.

9. Display and Touch Screen Suppliers

-

BOE Technology Group: Supplies LCD and OLED displays for inspection devices.

-

Corning Incorporated: Provides Gorilla Glass for touchscreens used in portable inspection tools.

10. Specialized Components Suppliers

-

Coherent, Inc.: Provides laser systems and components for 3D scanning and inspection.

-

IPG Photonics Corporation: Supplies fiber lasers for material processing and inspection devices.

-

Rohde & Schwarz: Provides signal analyzers and testing equipment for electronic devices.

Recent Development

-

November 2024, Hitachi High-Tech and the University of Tokyo are advancing high-resolution Laser-PEEM technology for semiconductor manufacturing, enhancing wafer defect inspections and chemical information visualization to improve throughput.

-

June 2024, Thermo Fisher Scientific announces that the Applied Biosystems CytoScan Dx Assay and ChAS Dx software now comply with EU In Vitro Diagnostic Regulations (IVDR), enhancing cytogenetics testing capabilities and ensuring high patient safety standards.

| Report Attributes | Details |

| Market Size in 2023 | USD 15.44 Billion |

| Market Size by 2032 | USD 26.78 Billion |

| CAGR | CAGR of 6.31% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Industrial CT, 3D Scanner, CMM, Machine Vision, SEM, TEM) • By Industry Vertical (Automotive & Transportation, Semiconductor & Electronics, Metal & Materials, Machinery & Equipment, Aerospace & Defense, Medical & Pharmaceutical, Energy & Power, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Carl Zeiss AG, Hitachi High-Technologies Corporation, Nikon Metrology NV, Hexagon AB, Omron Corporation, Bruker Corporation, Cognex Corporation, Keyence Corporation, Perceptron Inc., Olympus Corporation, Shimadzu Corporation, Thermo Fisher Scientific Inc., Zetec Inc., Ametek Inc., Hamamatsu Photonics K.K., FARO Technologies Inc., Mitutoyo Corporation, Leica Microsystems, Rohde & Schwarz, Eddyfi Technologies. |

| Key Drivers | • Expansion of the Automotive Sector Driving Demand for Advanced Inspection Devices. |

| Restraints | • Impact of Maintenance and Calibration Costs on the Growth of the Inspection Analysis Device Market. |

Frequently Asked Questions

Ans:Technological Advancement and Pre-owned inspection analysis instruments are available

Ans: North America is dominating the Inspection Analysis Device market.

Ans: Inspection Analysis Device Market size was valued at USD 15.44 Billion in 2023

Ans: USD 26.78 Billion is expected to grow by 2032.

Ans: Inspection Analysis Device Market is anticipated to expand by 6.31% from 2024 to 2032.

Get in Touch