Satellite Broadband Market Report Scope & Overview:

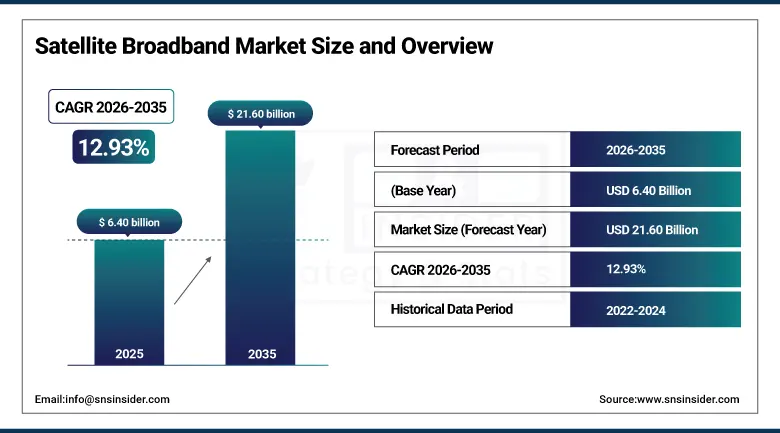

The Satellite Broadband Market was valued at USD 6.40 billion in 2025 and is expected to reach USD 21.60 billion by 2035, growing at a CAGR of 12.93% from 2026-2035.

Satellite Broadband Market growth is due to high demand for connectivity with high-speed internet from remote and underserved areas that lack proper terrestrial infrastructure. Growth in the adoption of digital services, cloud computing, and remote working applications is driving the demand even more. The growth in low Earth orbit satellite networks is providing better coverage and less latency, which is improving services. The increased use in telecommunications, maritime, aviation, and defense industries is also contributing towards market growth. Furthermore, technological innovation and increased government investment is driving the market globally.

According to the International Telecommunication Union (ITU), about 2.6 billion people remained offline in 2024, underscoring a persistent global digital divide and increasing demand for satellite-based broadband to expand connectivity coverage in underserved regions worldwide globally today.

According to the Federal Communications Commission (FCC), billions of dollars have been allocated through the Rural Digital Opportunity Fund (RDOF) to expand broadband deployment in underserved areas, including satellite-based connectivity where fiber infrastructure is not feasible or cost-effective.

In addition, the European Space Agency (ESA) has accelerated investment in next-generation satellite communications, including the IRIS² secure connectivity program, aimed at building a sovereign multi-orbit network to improve broadband availability, resilience, and security across Europe region wide.

Market Size and Forecast

-

Market Size in 2025: USD 6.40 Billion

-

Market Size by 2035: USD 21.60 Billion

-

CAGR: 12.93% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Satellite Broadband Market - Request Free Sample Report

Satellite Broadband Market Trends

-

Rising demand for high-speed internet in remote and underserved regions is driving the satellite broadband market.

-

Growing adoption across residential, maritime, aviation, and defense sectors is boosting market growth.

-

Expansion of low Earth orbit (LEO) satellite constellations is fueling global coverage and low-latency connectivity.

-

Increasing focus on bridging the digital divide and enabling global internet accessibility is shaping adoption trends.

-

Advancements in satellite miniaturization, phased-array antennas, and ground station technologies are enhancing performance and scalability.

-

Rising investments from private space companies and government-backed connectivity programs are supporting market expansion.

-

Collaborations between satellite operators, telecom providers, and technology firms are accelerating innovation and global adoption.

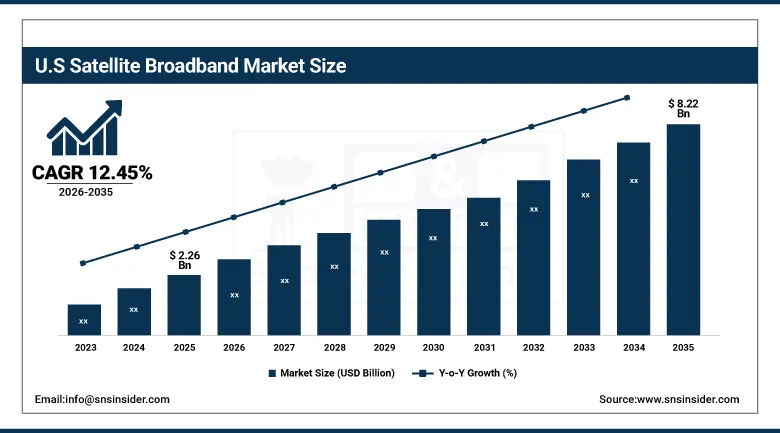

U.S. Satellite Broadband Market was valued at USD 2.26 billion in 2025 and is expected to reach USD 8.22 billion by 2035, growing at a CAGR of 12.45% from 2026-2035.

Growth in U.S. Satellite Broadband Market is being supported by increasing demand for faster Internet in rural places, increasing use of digital services, and rapid growth in LEO satellite constellations. Increasing applications in military, aviation, and rural Internet broadband access have contributed to growth in the market.

Satellite Broadband Market Segment Highlights

-

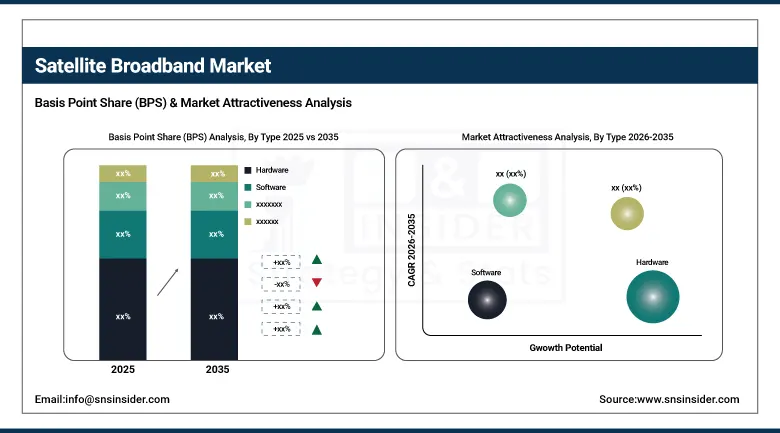

By Type, Hardware segment dominated the Satellite Broadband Market in 2025 with approximately 48% share; Services segment fastest growing (CAGR).

-

By Application, Residential segment dominated the Satellite Broadband Market in 2025 with approximately 41% share; Government & Defense segment fastest growing (CAGR).

-

By Frequency Band, Ku Band segment dominated the Satellite Broadband Market in 2025 with approximately 44% share; Ka Band segment fastest growing (CAGR).

-

By End-User, Telecommunications segment dominated the Satellite Broadband Market in 2025 with approximately 38% share; Aviation segment fastest growing (CAGR).

Satellite Broadband Market Segment Analysis

By Type, Hardware segment dominates the Satellite Broadband Market, Services segment expected to grow fastest.

The Hardware segment had a largest market share in the Satellite Broadband Market in 2025 owing to growing demand for various components such as satellite terminals, antennas, modems, and user equipment. Hardware plays a crucial role in facilitating satellite communications and is therefore integral in establishing satellite connectivity infrastructure both in residential and corporate settings. The increasing deployment of satellite constellations, the development of connectivity solutions in rural regions, and the need for high-speed internet in remote places has fueled demand for hardware installations. Advances in user equipment have helped boost the prominence of hardware even more.

The Services segment is expected to experience the fastest growth owing to growing demand for various services including managed connectivity services, optimization, installation services, and subscription services. Service providers are increasingly providing services that cover a wide range of solutions such as monitoring and maintenance as well as network management using the cloud platform. The increasing adoption of satellite internet solutions in remote areas, maritime sector, and enterprises is further stimulating demand for services in this category.

By Application, Residential segment dominates the Satellite Broadband Market, Government & Defense segment expected to grow fastest

The residential segment was the dominant segment in the Satellite Broadband Market in 2025, owing to increasing need for high-speed internet access in rural, remote, and poorly connected places. Satellite broadband has emerged as an effective tool to bridge the digital divide when there is not enough terrestrial infrastructure. With the increased demand for remote working, e-learning, and entertainment services, the adoption by residents has increased considerably. Availability of low-earth orbit satellites and low-cost subscriptions has enabled the dominance of residential segment in the global market.

Government & Defense segment is the fastest-growing, owing to increasing requirement of secure and robust satellite communications solutions for critical operations. There is increased deployment of satellite broadband technology in defense missions, surveillance of borders, disaster management, and emergency communications. Large-scale investments made by governments in developing advanced infrastructure and networks has helped boost the adoption by this segment in the coming years. Increasing geopolitical concerns, modernization of defense systems, and security of national communications have boosted the growth of this segment globally.

By Frequency Band, Ku Band segment dominates the Satellite Broadband Market, Ka Band segment expected to grow fastest

Ku Band Segment led the Satellite Broadband Market in 2025 owing to its extensive usage in Satellite TV, broadband services, and communications systems. The segment provides a well-balanced combination of coverage, efficient bandwidth utilization, and affordability that makes it feasible for both residential and commercial purposes. Availability of the segment in already established infrastructure and compatible with existing satellites further added value to its growth. Significant deployment in maritime, aviation, and broadcasting services strengthened the domination of Ku Band segment in global market.

Ka Band Segment is fastest growing because of its high bandwidth capabilities, fast data transmission capability, and capacity to provide high throughput satellite services. The segment finds application in future broadband constellations as well as in high performance communication networks. Increasing demand for high-speed Internet and cloud computing services is fuelling its fast adoption in the global market. Technological advancements in satellite technologies and increasing low earth orbit constellations are further driving the growth of Ka Band segment.

By End-User, Telecommunications segment dominates the Satellite Broadband Market, Aviation segment expected to grow fastest

The Telecommunication Segment accounted for the dominant share in Satellite Broadband Market in 2025 because of its importance in enabling connection services to remote locations and underdeveloped areas. For telecommunication companies, satellite broadband technology helps in expanding their network connectivity, improves backhaul network connectivity, and supports mobile and internet connectivity. Factors such as increasing demands for uninterrupted connectivity, data usage, and integration with the terrestrial network increased the prominence of the telecommunication segment.

The Aviation Segment has been witnessing the highest growth rate driven by rising demand for on-board connectivity solutions, entertainment systems, and real-time communication facilities in aircrafts. With an increase in the demand for flights and the expansion of commercial flights, satellite broadband technology has become more popular among airlines to provide efficient services. Improvements in satellite communications technology and collaborations among airlines and satellite companies have resulted in fast-paced growth in this segment.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

93.6% |

|

Europe |

United Kingdom |

24.9% |

|

Asia Pacific |

Australia |

9.4% |

|

Middle East & Africa |

UAE |

15.7% |

|

Latin America |

Brazil |

52.1% |

North America Satellite Broadband Market Insights

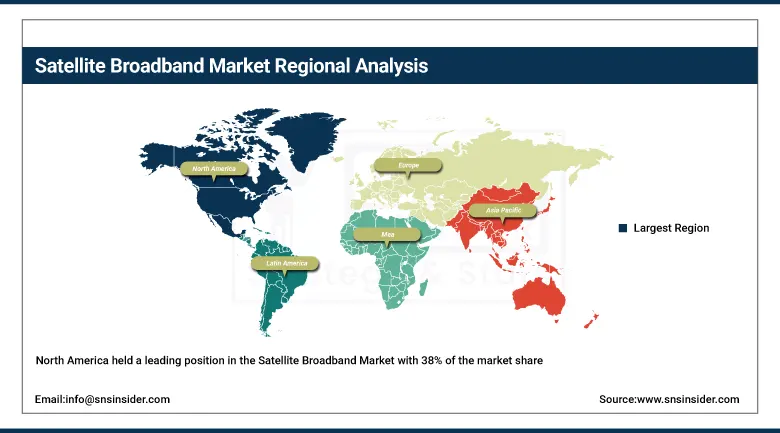

North America held a leading position in the Satellite Broadband Market with 38% of the market share owing to high demand for high-speed internet connections. Adoption by the residential, commercial, governmental, and military segments is also boosting the dominance of North America. This regional dominance can be attributed to the presence of large satellite broadband players, technological innovations, and investments in LEO satellites. Rising demand for connectivity solutions in remote areas, along with an increase in demand for the use of satellite broadband in air and sea mobility, has been boosting the dominance of North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Satellite Broadband Market Insights

The Asia Pacific Satellite Broadband Market is witnessing significant growth owing to the rising demand for reliable and faster internet connectivity among rural and remote areas. The increased focus on digital transformation, rising smartphone adoption rate, and increasing use of cloud services have been fueling the growth of the market. Investments in satellite communication network by government to provide better broadband connectivity have been fueling market growth. Apart from this, increasing applications in telecommunication, marine, aircraft, and defense segments are also fueling demand.

Europe Satellite Broadband Market Insights

The Europe Satellite Broadband Market is showing consistent growth as a result of growing demand for high-speed connectivity services among the population living in rural and remote locations. Consistent government initiatives in favor of digital inclusion and development of broadband networks are expected to accelerate adoption. The growing utilization of broadband services in aviation, maritime, and defense applications is another key factor driving growth in the market. Growing implementation of state-of-the-art satellite systems as well as partnerships between governments and private sector is boosting coverage area in the market.

Middle East & Africa and Latin America Satellite Broadband Market Insights

Market for Middle East & Africa and Latin America Satellite Broadband is experiencing fast-paced growth owing to the insufficient terrestrial infrastructure in far-off geographical locations. The demand for dependable connectivity services in the rural population, offshore industries, and underdeveloped sectors is contributing to the increased adoption rate. Growing government efforts in digital transformation and smart infrastructure development are also favoring market growth. Increasing adoption of satellite broadband solutions in the oil & gas, maritime, and disaster management industry verticals is also increasing the growth potential for the market.

Market Growth Drivers:

Expanding Demand for High-Speed Internet Connectivity in Remote and Underserved Regions Driving Global Satellite Broadband Adoption Rapidly: Increasing demand for reliable internet connectivity in distant and rural areas is playing an important role in growing demand for the satellite broadband market worldwide. Unavailability of terrestrial network infrastructure in geographic areas that are hard to cover is boosting the utilization of satellite technology to meet connectivity needs. Increasing adoption of digitization in various sectors including education, healthcare, agriculture, and governmental services is contributing towards the growth in demand for satellite broadband systems. Increasing use of Internet-based services, cloud computing, and remote solutions for working purposes is contributing towards the growth of satellite broadband market.

Market Restraints:

High Initial Investment Costs and Complex Satellite Deployment Infrastructure Limiting Widespread Adoption Across Cost-Sensitive Markets: The need for high levels of capital for satellite fabrication, launching operations, and ground station creation constitutes another important factor that acts as a barrier to growth within the global satellite broadband market. Satellite network installation involves several technical operations and heavy investments that may limit participation by small players within the industry. Besides, satellite broadband installation requires huge operational and maintenance budgets compared to regular broadband network installation. Affordability in developing nations also becomes difficult as another challenge limiting adoption of the technology. The complexities in spectrum allocation and reliance on advanced satellite launch technologies also constitute key barriers to market penetration.

Market Opportunities:

Increasing Demand for Maritime, Aviation, and Defense Connectivity Solutions Creating Strong Growth Potential for Satellite Broadband Services Worldwide: The rising need for high-speed and uninterrupted broadband connections in various industries such as maritime, aviation, and defense can lead to substantial growth opportunities for satellite broadband market. Communication systems that offer uninterrupted connection are required by ships, planes, and military forces that function in offshore locations where terrestrial systems cannot be set up. The growing use of systems that involve navigation and surveillance systems can drive market demand. Market growth will also be driven by the expansion in trade routes and flights on an international level. The increasing investments made in setting up satellite broadband communication facilities will drive market demand.

Recent Developments:

-

2026: Hughes expanded its JUPITER satellite broadband platform supporting enterprise and rural connectivity. The company enhanced multi-orbit managed services combining GEO satellites and LEO partnerships to improve global broadband reliability and low-latency internet access.

-

2026: SpaceX expanded Starlink Gen2 satellite deployments to increase global broadband capacity for enterprise, aviation, and maritime users. The company focused on higher throughput satellites and improved spectrum utilization, strengthening low-latency satellite internet coverage worldwide for consumer and government applications.

-

2025: Viasat expanded its next-generation ViaSat-3 satellite system to deliver high-capacity broadband connectivity for aviation and mobility markets. The company focused on improving global internet coverage, especially for in-flight and remote enterprise communication services.

Satellite Broadband Market Key Players

-

SpaceX

-

Hughes Network Systems

-

Viasat Inc.

-

Eutelsat Communications

-

SES S.A.

-

OneWeb

-

Inmarsat Global Limited

-

Telesat Canada

-

Iridium Communications Inc.

-

Thuraya Telecommunications Company

-

Intelsat S.A.

-

Globalstar Inc.

-

Hispasat S.A.

-

Singtel Satellite

-

Gilat Satellite Networks Ltd.

-

Skycasters LLC

-

Yahsat

-

Kacific Broadband Satellites Group

-

Speedcast International Limited

-

Swarm Technologies Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.40 Billion |

| Market Size by 2035 | USD 21.60 Billion |

| CAGR | CAGR of 12.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hardware, Software and Services) • By Application (Residential, Commercial, Government & Defense and Others) • By Frequency Band (C Band, Ku Band, Ka Band, L Band and Others) • By End-User (Telecommunications, Maritime, Aviation, Energy and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX, Hughes Network Systems, Viasat Inc., Eutelsat Communications, SES S.A., OneWeb, Inmarsat Global Limited, Telesat Canada, Iridium Communications Inc., Thuraya Telecommunications Company, Intelsat S.A., Globalstar Inc., Hispasat S.A., Singtel Satellite, Gilat Satellite Networks Ltd., Skycasters LLC, Yahsat, Kacific Broadband Satellites Group, Speedcast International Limited and Swarm Technologies Inc. |

Frequently Asked Questions

North America dominated the Satellite Broadband Market in 2025.

The Residential segment dominated the Satellite Broadband Market in 2025.

Expanding Demand for High-Speed Internet Connectivity in Remote and Underserved Regions Driving Global Satellite Broadband Adoption Rapidly.

The Satellite Broadband Market was valued at USD 6.40 billion in 2025.

The Satellite Broadband Market is expected to grow at a CAGR of 12.93% from 2026 to 2035.

Get in Touch