Semiconductor Front-end Equipment Market Size:

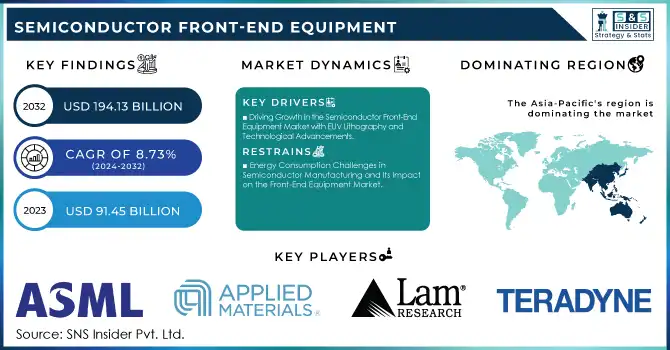

The Semiconductor Front-End Equipment Market Size was valued at USD 91.45 Billion in 2023, and is expected to reach USD 194.13 Billion by 2032, and grow at a CAGR of 8.73% over the forecast period 2024-2032.

The Semiconductor Front-End Equipment Market is on a strong growth trajectory, fueled by the surging demand for advanced semiconductor nodes, essential for the development of cutting-edge technologies such as AI, 5G, IoT, and automotive applications. With industries focusing on improving efficiency and miniaturizing chips (such as 5nm, 3nm, and smaller), this trend has driven the adoption of critical technologies like EUV lithography and plasma etching systems, which are necessary for the precision required in modern semiconductor manufacturing. Asia-Pacific continues to dominate the semiconductor-manufacturing sector, with heavy investments from major players like TSMC, Samsung, and SMIC. Concurrently, efforts such as the U.S. CHIPS Act and funding initiatives in Europe are enhancing semiconductor production capabilities in North America and Europe, helping to reduce reliance on imports. The rapid expansion of electric vehicles (EVs), autonomous driving technologies, and the increasing demand for high-performance computing further stimulate the market for semiconductor equipment. The global trend toward digitalization is intensifying, pushing the need for smart devices and consequently driving the demand for advanced manufacturing equipment. Additionally, the complexity of 3D semiconductor architectures and the ongoing shift toward heterogeneous integration present both challenges and opportunities, fostering continuous innovation in equipment design. Companies are investing significantly in R&D, as seen with advancements like ACM Research's ultra-precision cleaning tools that enhance production yields for advanced nodes. Over 70% of global semiconductor foundry capacity for older technologies (28nm and beyond) is concentrated in China and Taiwan, while Taiwan also accounts for nearly 70% of the world's advanced semiconductor manufacturing capacity (16/14nm and more). The top 30 technology equipment companies, including leaders like NVIDIA, TSMC, Samsung, Broadcom, and ASML, represent around 85% of the total market capitalization of the top 100 technology equipment firms as of April 2024. This concentration further highlights the dominance of key players driving the growth of the semiconductor equipment market.

To get more information on ASemiconductor Front-End Equipment Market - Request Free Sample Report

Semiconductor Front-End Equipment Market Dynamics

Drivers

-

Driving Growth in the Semiconductor Front-End Equipment Market with EUV Lithography and Technological Advancements

The semiconductor front-end equipment market is witnessing significant growth, primarily driven by advancements in extreme ultraviolet (EUV) lithography. EUV is revolutionizing semiconductor production by enabling the fabrication of chips with smaller nodes, which are essential for creating high-performance and energy-efficient devices used across various industries, including automotive, artificial intelligence (AI), telecommunications, and data centers. This technology, which utilizes shorter wavelengths of light, allows the manufacture of smaller transistors, accelerating the miniaturization of chips crucial for applications like 5G networks and AI-driven technologies. As demand increases for smaller, faster, and more efficient semiconductors, the need for advanced front-end equipment, particularly EUV machines, has surged. Industry leaders like ASML, which specialize in EUV technology, are playing a critical role in advancing semiconductor manufacturing by improving yield and reducing production costs. Notably, the wafer processing equipment sector, which includes EUV tools, saw a 15% increase in demand, with test equipment growing by 20%. In 2023, South Korea emerged as the largest market for semiconductor equipment, surpassing Taiwan, with China, Japan, and North America also experiencing notable growth. The continued evolution of the semiconductor industry, spurred by applications in 5G, AI, IoT, and data centers, is expected to further fuel the demand for cutting-edge semiconductor front-end equipment, ensuring sustained market growth.

Restraints

-

Energy Consumption Challenges in Semiconductor Manufacturing and Its Impact on the Front-End Equipment Market

Energy consumption in semiconductor manufacturing, particularly with the use of advanced technologies such as extreme ultraviolet (EUV) lithography, presents significant challenges. EUV machines, which are essential for producing smaller, high-performance chips, require enormous amounts of energy due to the complex process of generating light for etching patterns onto semiconductor wafers. Semiconductor fabrication facilities (fabs) are among the most energy-intensive in the world. For example, the semiconductor industry consumed a staggering 149 billion kWh in 2021, enough to power a city of 25 million people for an entire year. The trend toward smaller chips with node sizes shrinking to 3 nm exacerbates this issue, as more energy is consumed per unit of output. This increase in energy demand raises concerns about the environmental impact of semiconductor manufacturing, especially as global production continues to scale. As the industry grows, particularly with the introduction of more advanced front-end equipment like EUV machines, energy use could increase significantly, potentially up to eight times, making it one of the most energy-intensive sectors. Despite efforts to move towards renewable energy, 95.8% of the semiconductor industry's energy still comes from grid electricity and fossil fuels, with renewable sources contributing a mere 2.7%. Additionally, the use of hazardous chemicals and gases in the manufacturing process poses environmental risks, which are now being restricted by regulations like the EU’s F-gas and PFAS bans. As semiconductor production scales up to meet demand, addressing the growing energy consumption and its environmental footprint will be crucial. Failure to prioritize energy efficiency and sustainability could result in higher operational costs and hinder the long-term growth of the semiconductor front-end equipment market, creating a conflict between economic expansion and sustainability goals.

Semiconductor Front-End Equipment Market Segment Analysis

by Type

In 2023, the lithography equipment segment dominated the semiconductor front-end equipment market, capturing around 60% of the share. Lithography, a critical process in semiconductor manufacturing, involves transferring patterns onto silicon wafers to create integrated circuits. The demand for smaller nodes, such as 7nm, 5nm, and 3nm, which require extreme ultraviolet (EUV) lithography, has fueled the growth of this segment. EUV technology enables the production of advanced chips for applications like 5G, AI, and high-performance computing. As the need for faster, smaller, and more efficient semiconductors continues to rise, the lithography equipment segment is expected to remain dominant, driven by market leaders like ASML and continued investments in next-generation lithography tools.

by End-User Industry

In 2023, the semiconductor fabrication plants (fabs) segment led the semiconductor front-end equipment market, capturing around 69% of the share. Fabs are essential to semiconductor manufacturing, where advanced processes like photolithography, etching, and deposition occur to produce integrated circuits. Growing demand for high-performance chips in sectors such as 5G, AI, and automotive has driven substantial investments in new fabs and equipment. The shift towards smaller process nodes, such as 7nm and 5nm, and the adoption of EUV lithography have further increased the need for advanced front-end equipment. The expansion of fabs in regions like Asia-Pacific, North America, and Europe solidifies the segment’s dominance, with high-performance computing and IoT continuing to fuel industry growth.

Semiconductor Front-End Equipment Market Regional Outlook

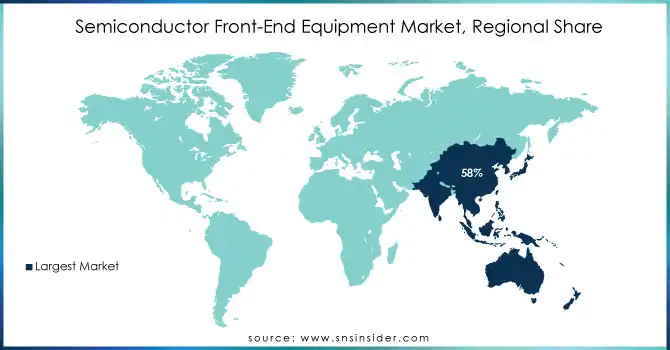

Asia-Pacific's dominance in the semiconductor front-end equipment market, accounting for 58% of global revenue in 2023, is driven by key countries like Taiwan, South Korea, Japan, and China. Taiwan, with TSMC leading the market, holds over 50% of the global semiconductor-manufacturing share, particularly excelling in advanced 3nm and 5nm technologies, integrated with EUV lithography. South Korea, with Samsung at the forefront, contributes significantly to APAC's share, with investments in next-generation semiconductor manufacturing. China, focusing on domestic production through its "Made in China 2025" initiative, aims to reduce reliance on imports and ramp up semiconductor capabilities with substantial government backing. Japan also plays a vital role, advancing semiconductor materials and precision manufacturing. This dominance is supported by a thriving electronics market, robust supply chains, and rising demand for technologies like AI, 5G, and IoT, ensuring APAC’s continued leadership in the semiconductor front-end equipment market.

North America is the fastest-growing region in the semiconductor front-end equipment market in 2023, fueled by both public and private sector investments, technological advancements, and expanding fabrication capacity. The United States plays a key role, with companies like Intel, Micron, and Global Foundries increasing their investments in next-generation technologies, including 5nm and 3nm chips. The passing of the CHIPS Act in 2022 has significantly boosted the region’s growth by providing substantial funding for domestic semiconductor manufacturing. This policy aims to reduce reliance on foreign chip production, particularly from Asia, while strengthening the supply chain and national security. In addition to federal support, states such as Arizona, Texas, and Ohio are attracting semiconductor fabs through state-level incentives. These local efforts, combined with a rapidly expanding demand for chips in sectors such as AI, electric vehicles, and telecommunications, have accelerated North America's market position.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

Some of the Major players in Semiconductor Front-End Equipment Market with their product:

-

ASML (EUV Lithography Machines)

-

Applied Materials (Etching Systems, Deposition Equipment)

-

Lam Research (Etch and Deposition Systems)

-

Tokyo Electron Limited (TEL) (Wafer Cleaning, Etching, Deposition Equipment)

-

KLA Corporation (Metrology & Inspection Systems)

-

Teradyne (Test Equipment)

-

Advantest Corporation (Semiconductor Testing Equipment)

-

Screen Semiconductor Solutions (Coating Systems, Lithography Equipment)

-

Nikon Corporation (Lithography Equipment)

-

Hitachi High-Tech Corporation (Inspection Systems, Metrology Equipment)

-

Rudolph Technologies (now part of Onto Innovation) (Process Control Systems, Metrology Equipment)

-

Chugai Technos Corporation (Wafer Bonding Equipment)

-

Semes Co., Ltd. (Etching, Coating, and Cleaning Equipment)

-

Zeiss (Optical Metrology and Lithography Systems)

-

Meyer Burger Technology AG (Deposition Equipment)

-

SUSS MicroTec (Wafer Bonding, Lithography, and Coating Systems)

-

Carl Zeiss SMT GmbH (Microscopes for Metrology)

-

Entegris (Materials Handling, Filtration, and Chemical Delivery Systems)

-

Nikon Precision Inc. (Photolithography Equipment)

-

Amkor Technology (Packaging and Testing Services)

List of raw material and equipment suppliers in the semiconductor front-end equipment market:

Raw Material Suppliers:

-

Shin-Etsu Chemical (Silicon Wafers, Photoresists)

-

SUMCO Corporation (Silicon Wafers)

-

GlobalWafers Co., Ltd. (Silicon Wafers)

-

Dow Inc. (Photoresists, Chemicals)

-

Merck Group (Specialty Chemicals for Lithography, Photoresists)

-

BASF (Chemicals for Semiconductor Processing)

-

JNC Corporation (Photoresists, Etching Materials)

-

Albemarle Corporation (Lithography Materials)

-

SK Materials Co., Ltd. (High-Purity Gases, Specialty Chemicals)

-

Air Products and Chemicals, Inc. (Industrial Gases)

Equipment Suppliers:

-

ASML (EUV Lithography Systems)

-

Applied Materials (Deposition, Etch, and CMP Equipment)

-

Lam Research (Etching and Deposition Equipment)

-

Tokyo Electron Limited (TEL) (Wafer Processing Equipment)

-

KLA Corporation (Metrology and Inspection Equipment)

-

Teradyne (Test Equipment)

-

Advantest Corporation (Test Equipment)

-

Nikon Corporation (Photolithography Equipment)

-

Hitachi High-Tech Corporation (Metrology and Inspection Equipment)

-

Zeiss (Optical Metrology Equipment)

Recent Development

-

September 12, 2024 Tata Electronics and Tokyo Electron Limited (TEL) have signed a memorandum of understanding to accelerate semiconductor equipment development in India, supporting Tata's semiconductor fab in Dholera, Gujarat, and its assembly and test facility in Jagiroad, Assam. This partnership also focuses on workforce training and R&D collaboration.

-

October 07, 2024 Amkor Technology and TSMC have signed a memorandum of understanding to expand their partnership, focusing on advanced packaging and test services in Peoria, Arizona. This collaboration aims to support high-performance computing and communications markets, leveraging TSMC’s wafer fabrication in Phoenix and Amkor’s packaging expertise.

-

September 4, 2024, Shin-Etsu Chemical has strengthened its market position by developing new interposer-less equipment for semiconductor manufacturing. This innovation is aimed at addressing evolving competition in the semiconductor materials market, where the company holds leading positions with its silicon wafers and other materials.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 91.45 Billion |

| Market Size by 2032 | USD 194.13 Billion |

| CAGR | CAGR of 8.73% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Lithography Equipment, Etching Equipment) • By End-User Industry (Semiconductor Fabrication Plant, Semiconductor Electronics Manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Key players in the semiconductor front-end equipment market include ASML, Applied Materials, Lam Research, Tokyo Electron Limited (TEL), KLA Corporation, Teradyne, Advantest Corporation, Screen Semiconductor Solutions, Nikon Corporation, Hitachi High-Tech Corporation, Rudolph Technologies (now part of Onto Innovation), Chugai Technos Corporation, Semes Co., Ltd., Zeiss, Meyer Burger Technology AG, SUSS MicroTec, Carl Zeiss SMT GmbH, Entegris, Nikon Precision Inc., and Amkor Technology. |

| Key Drivers | • Driving Growth in the Semiconductor Front-End Equipment Market with EUV Lithography and Technological Advancements. |

| Restraints | • Energy Consumption Challenges in Semiconductor Manufacturing and Its Impact on the Front-End Equipment Market. |

Frequently Asked Questions

Ans: Lithography Equipment is the dominating segment in Semiconductor Front-End Equipment market.

Ans: The Semiconductor Front-End Equipment Market Size is expected to reach USD 194.13 Billion by 2032.

Ans: Asia-Pacific is dominating in Semiconductor Front-End Equipment Market in 2023.

Ans: The primary market driver for the Semiconductor Front-End Equipment Market is the increasing demand for advanced semiconductor nodes and technologies fueled by AI, 5G, IoT, and automotive.

Ans: Semiconductor Front-End Equipment Market is anticipated to expand by 8.73% from 2024 to 2032.

Get in Touch