Silicon Anode Battery Market Report Scope & Overview:

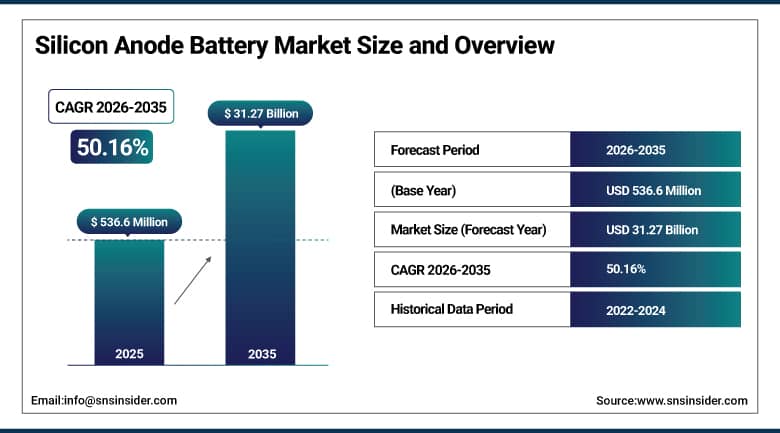

The Silicon Anode Battery Market was valued at USD 536.6 million in 2025 and is expected to reach USD 31.27 billion by 2035, growing at a CAGR of 50.16% from 2026–2035.

Global Silicon Anode Battery Market is at the most transformative inflection point in battery technology since the commercial introduction of lithium-ion batteries in the 1990s, as silicon-based anode materials that can store up to 10 times more lithium ions per unit mass than conventional graphite anodes are transitioning from laboratory curiosity to commercially deployed technology that is beginning to redefine what is achievable in energy density, charging speed, and battery size across electric vehicles, consumer electronics, and energy storage applications. Silicon anodes theoretically provide a specific capacity of 3,580 mAh/g compared to graphite's 372 mAh/g, a 10-fold advantage that translates directly into smaller batteries delivering the same energy content, or equivalently larger energy content within existing battery form factors that extend EV range, smartphone battery life, and energy storage system capacity without increasing physical size or weight.

The Silicon Anode Battery Market's extraordinary 50.16% CAGR from 2026 to 2035 reflects the compound commercial acceleration of a battery technology that simultaneously addresses the two most critical limitations of current lithium-ion batteries, energy density and charging speed, that are the primary consumer and OEM pain points in electric vehicles and consumer electronics. As silicon anode technology scales from early commercial deployment in premium wearables and smartphones into EV powertrains, the addressable market expands into one of the world's largest technology transition opportunities, creating the exceptional revenue growth trajectory that makes silicon anode batteries one of the most commercially compelling energy technology investment categories globally.

Market Size and Forecast

-

Market Size in 2025: USD 536.6 Million

-

Market Size by 2035: USD 31.27 Billion

-

CAGR: 50.16% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Silicon Anode Battery Market - Request Free Sample Report

Silicon Anode Battery Market Trends:

-

Accelerating commercial deployment of silicon-carbon composite anode materials where nano-silicon particles are dispersed within a carbon matrix that accommodates volumetric expansion during charging while maintaining electrical conductivity, enabling premium consumer electronics including Samsung Galaxy S and Apple iPhone batteries to incorporate meaningful silicon anode content that improves energy density without sacrificing cycle life.

-

Growing EV OEM investment in silicon anode battery qualification and supply chain development, with Tesla, BMW, and Porsche announcing silicon anode battery programmes targeting the 800V ultra-fast charging platforms of next-generation EV architectures where silicon anodes' superior charging kinetics deliver the 5 to 15 minute fast-charge capability that consumers demand.

-

Rapid commercial scale-up of silicon anode material suppliers including Group14 Technologies, Amprius Technologies, Nexeon, and Sila Nanotechnologies, each developing proprietary silicon carbon composite and nano-silicon manufacturing processes at increasing production scale to serve growing EV and consumer electronics customer demand.

-

Rising investment in solid-state silicon anode battery development, where solid electrolytes that do not react with silicon surfaces or form problematic solid-electrolyte interphase layers could eliminate the primary remaining cycle life limitation of liquid-electrolyte silicon anode systems, potentially enabling full silicon anode capacity utilisation without degradation.

-

Growing wearable and medical device silicon anode adoption driven by the extreme miniaturisation requirements of smartwatch, fitness tracker, continuous glucose monitor, and cardiac monitor batteries where silicon anode's energy density advantage enables smaller device form factors or meaningfully extended device runtime within existing size constraints.

U.S. Silicon Anode Battery Market Size Outlook:

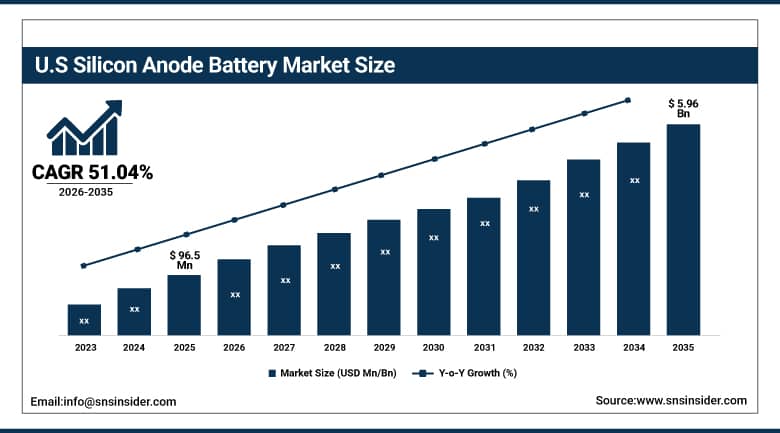

The U.S. Silicon Anode Battery Market was valued at USD 96.5 million in 2025 and is expected to reach USD 5.96 billion by 2035, growing at a CAGR of 51.04% during 2026–2035. United States represents the world's most commercially dynamic silicon anode battery market, home to the highest concentration of silicon anode technology companies including Group14 Technologies, Sila Nanotechnologies, Enovix Corporation, Amprius Technologies, and Enevate Corporation, whose continuous technology innovation is establishing U.S. commercial leadership in the most critical battery technology transition since the invention of lithium-ion. U.S. federal investment through the DOE Battery 500 Consortium, Advanced Research Projects Agency-Energy ARPA-E silicon anode development programmes, and CHIPS Act-adjacent battery manufacturing incentives is supporting the technology development and manufacturing scale-up that will establish domestic silicon anode supply chains aligned with EV battery manufacturing investment under the Inflation Reduction Act.

Group14 Technologies' SCC55 silicon carbon composite material achieving over 1,000 cycles at 80% capacity retention with 80% state of charge in under five minutes, combined with its partnership with BASF to scale commercial production, represents the most technically compelling silicon anode commercialisation milestone achieved in the United States. These validated performance metrics, demonstrating that silicon anode batteries are no longer a performance promise but a commercial reality, are the catalyst for the accelerating EV OEM qualification programmes and consumer electronics design-in activities that will drive the U.S. market's 51.04% CAGR through the 2026 to 2035 forecast period.

Silicon Anode Battery Market Segment Insights:

-

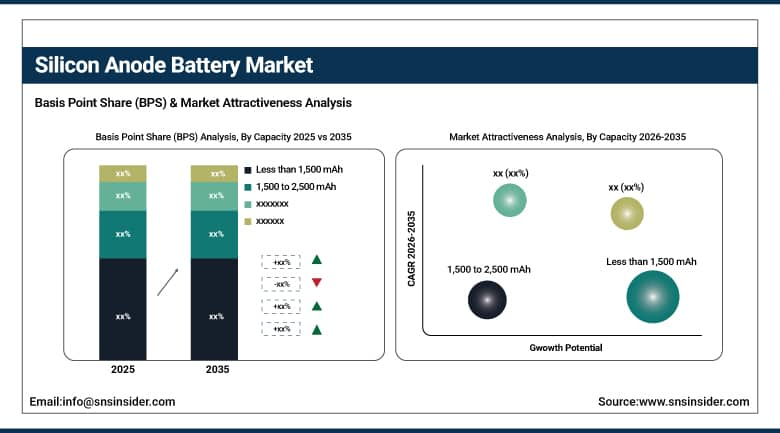

By Capacity, the Less than 1,500 mAh segment held approximately 49% of the Silicon Anode Battery Market in 2024, dominant due to wearables, medical devices, and small consumer electronics requiring compact high-density batteries; the 1,500 to 2,500 mAh segment is expected to grow fastest at a CAGR of approximately 57.92% from 2026 to 2035, driven by rapidly rising adoption in smartphones, drones, and IoT devices.

-

In terms of Anode Type, Silicon Carbon Composite dominated as the most commercially mature silicon anode material balancing high energy density with acceptable cycle life at commercial production scale; Pure Silicon is the fastest-growing anode type as advanced binder and electrolyte innovations are progressively resolving the cycle life limitations that previously prevented full silicon utilisation.

-

By Application, Consumer Electronics dominated in 2025 as the first commercial silicon anode deployment scale segment; Electric Vehicles is the fastest-growing application and will become the largest revenue segment by 2030 as automotive-scale silicon anode battery production volumes scale.

-

By End-User, Automotive is projected to be the fastest-growing and largest end-user segment through 2035 as EV manufacturers adopt silicon anode batteries to extend driving range and enable ultra-fast charging; Commercial and Industrial end-users are growing through energy storage and specialty application deployment.

By Capacity: Less than 1,500 mAh dominates, 1,500 to 2,500 mAh grows fastest

The Less than 1,500 mAh capacity segment dominated the Silicon Anode Battery Market in 2024 with approximately 49% of revenues, reflecting the fact that the first commercial applications of silicon anode technology are in small, premium consumer electronics and medical devices where the energy density improvement over graphite delivers the most immediately compelling device performance improvement. Smartwatches, fitness trackers, hearing aids, insulin pumps, continuous glucose monitors, and premium truly wireless earbuds are the primary volume applications in this capacity range, where silicon anode integration extends device battery life by 20 to 40% within existing physical form factors that cannot be enlarged without compromising consumer acceptance.

The 1,500 to 2,500 mAh segment is projected to grow at the fastest CAGR of approximately 57.92% from 2026 to 2035, driven by the rapidly increasing adoption of silicon anode technology in premium smartphones, compact drones, and IoT edge devices where this capacity range represents the operational energy requirement. Silicon anode integration in premium Android and iOS smartphones in this capacity range delivers either meaningfully thinner device designs or extended battery life within the same physical dimensions, addressing the smartphone industry's most persistent consumer demand for longer-lasting devices without the thickness and weight penalties of simply installing a larger conventional graphite battery.

By Anode Type: Silicon Carbon Composite dominates, Pure Silicon grows fastest

Silicon Carbon Composite retained the dominant anode type position in 2025, representing the most commercially proven pathway to silicon anode performance improvement that manages the fundamental challenge of silicon's 300% volumetric expansion during lithiation through dispersal of nano-silicon particles within a protective carbon matrix. The carbon matrix serves dual functions: it buffers the mechanical stress of silicon expansion and contraction during charge cycles while maintaining the electrical conductivity network that delivers electrons to and from silicon active material throughout the electrode volume. Commercial silicon carbon composite products from Group14, Sila Nanotechnologies, and BTR New Material achieve silicon loadings of 20 to 80% by weight in the composite, with higher silicon content delivering greater energy density but requiring more sophisticated carbon architecture to maintain acceptable cycle life, creating a performance-durability optimisation space that each company addresses through proprietary material science.

Pure Silicon anodes represent the technically ultimate silicon anode configuration, with theoretical capacity of 3,580 mAh/g versus silicon-carbon composite's blended effective capacity that depends on silicon loading fraction. Pure silicon anode batteries are commercially deployed by Amprius Technologies in specialty aerospace and defense applications where extreme energy density justifies the premium cost and the more demanding cycle life management required, demonstrating that pure silicon is commercially viable in high-value applications that accept shorter cycle life in exchange for maximum energy density.

By Application: Consumer Electronics dominates, Electric Vehicles grows fastest

Consumer Electronics dominated the Silicon Anode Battery Application segment in 2025, reflecting the first commercial applications of silicon anode technology in premium smartphones, wearables, laptops, and medical devices where the market development infrastructure for silicon anode qualification, supply chain, and product integration is most advanced. Consumer electronics OEMs including Samsung, Apple, and Xiaomi have driven the initial commercial scaling of silicon anode material production through their premium device programmes, establishing the supply chain, testing protocols, and manufacturing processes that are now being adapted for automotive application qualification.

Electric Vehicles represent the fastest-growing application segment with the largest long-term revenue potential, as the automotive EV market's enormous scale, combined with the urgency of solving range anxiety and enabling ultra-fast charging, creates the most compelling commercial opportunity for silicon anode batteries. Each additional 50 km of EV driving range or 5-minute reduction in charging time that silicon anode enables has direct commercial value measured in consumer purchase preference, insurance economics, and competitive positioning for automotive OEMs investing tens of billions of dollars in EV platform development.

Silicon Anode Battery Market Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

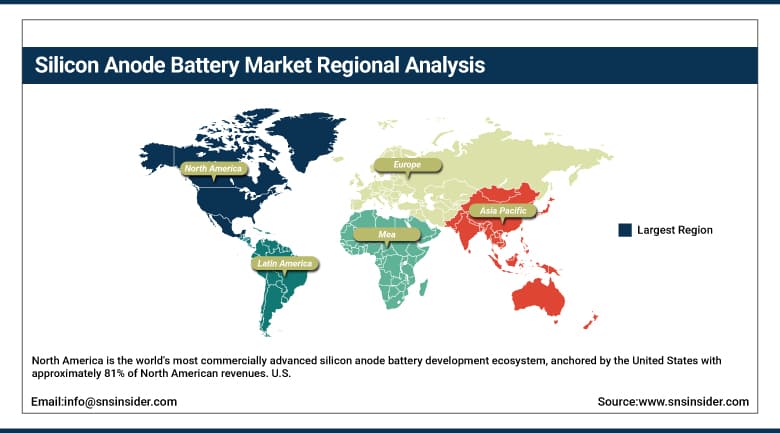

North America |

United States |

~81% |

|

Europe |

Germany |

~38% |

|

Asia Pacific |

China |

~52% |

|

Middle East & Africa |

UAE |

~27% |

|

Latin America |

Brazil |

~43% |

North America Silicon Anode Battery Market Insights

North America is the world's most commercially advanced silicon anode battery development ecosystem, anchored by the United States with approximately 81% of North American revenues. U.S. market leadership is sustained by the highest concentration of silicon anode material technology companies, the most active venture capital and strategic investment in battery technology startups, and federal R&D investment through DOE programmes that sustain the frontier research enabling next-generation silicon anode performance improvements. Domestic EV manufacturing investment including the Inflation Reduction Act provisions supporting U.S. battery manufacturing is creating growing domestic demand for silicon anode batteries from U.S. EV assembly operations that will strengthen North American market growth through the forecast period.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Silicon Anode Battery Market Insights

Europe represents a growing silicon anode battery market, shaped by the EU battery regulation's sustainability requirements that favour silicon anode batteries' improved energy density enabling smaller battery packs per vehicle and the European automotive OEM's EV electrification investments. Germany leads European silicon anode adoption through Volkswagen Group, BMW, and Mercedes-Benz EV programmes that are qualifying silicon anode battery cells from multiple suppliers. Northvolt's Sweden-based battery manufacturing programme and the EU Battery Alliance are creating European manufacturing investment that is beginning to incorporate silicon anode technology in next-generation cell designs.

Asia Pacific Silicon Anode Battery Market Insights

Asia Pacific is the fastest-growing regional Silicon Anode Battery Market, driven by China's world-leading lithium-ion battery manufacturing ecosystem that is progressively integrating silicon anode materials into next-generation cell designs for EV and consumer electronics customers, Japan's advanced battery chemistry research community contributing to silicon anode electrolyte and binder innovations, and South Korea's Samsung SDI and LG Energy Solution programmes incorporating silicon anode materials in premium EV battery cell products. China's CATL, BYD, and Ganfeng Lithium are each developing silicon anode battery capabilities, with China's government carbon neutrality targets creating policy imperative for the next-generation battery technology that will enable the longest-range and fastest-charging EVs.

Latin America and MEA Silicon Anode Battery Market Insights

Latin America and MEA represent emerging silicon anode battery markets, initially driven by consumer electronics adoption before automotive deployment begins as commercial silicon anode EV batteries reach these regions' growing electric vehicle markets in the late 2020s. Brazil leads Latin American market development through its growing EV market and domestic battery industry investment, while the UAE and Saudi Arabia are positioning their energy transition investment programmes to include advanced battery technology deployment aligned with Vision 2030 EV adoption targets.

Market Dynamics:

Growth Drivers: EV range and fast-charging imperatives combined with consumer electronics miniaturisation demand creating structural pull for silicon anode's unique performance advantages over graphite

The primary structural growth drivers for the Silicon Anode Battery Market are the simultaneous commercial imperatives from electric vehicle manufacturers requiring longer range and faster charging without larger or heavier battery packs, and consumer electronics OEMs requiring thinner, lighter devices with longer battery life, that create precisely the performance requirements that silicon anode technology uniquely addresses. Every incremental advance in silicon anode cycle life and manufacturing cost competitiveness relative to graphite directly expands the addressable commercial opportunity, and the pace of technical progress across multiple competing silicon anode approaches including silicon-carbon composites, silicon oxide, nano-silicon, and solid-state silicon is creating a progressive performance frontier expansion that accelerates commercial adoption across application segments.

Restraints: Volume expansion-driven cycle life degradation in pure silicon systems, manufacturing scalability challenges, and cost premium relative to mature graphite anode technology

A significant restraint on the Silicon Anode Battery Market is the fundamental materials science challenge of silicon's 300% volumetric expansion during lithiation that causes mechanical cracking, electrical isolation of active material, and ongoing solid electrolyte interphase formation that consumes lithium inventory and reduces cycle life relative to graphite anodes. While silicon-carbon composites have partially addressed these challenges, higher silicon loading fractions that would maximise energy density advantage still experience accelerated capacity fade that limits their deployment in automotive applications requiring 8-to-10-year battery lifetimes. The manufacturing cost of silicon anode materials remains significantly higher than graphite on a per-kilogram basis at current production volumes, requiring premium pricing that limits initial deployment to premium device segments where energy density performance justifies the cost premium before scale economies reduce silicon anode material costs toward graphite competitiveness.

Opportunities: Solid-state silicon anode integration, EV range extension and fast-charge enabling premium positioning, and aerospace and defense high-density power applications

The integration of silicon anodes with solid-state electrolytes represents the ultimate battery performance combination, as solid electrolytes that do not react with silicon surfaces eliminate the primary source of silicon anode cycle life degradation while enabling the full theoretical capacity of silicon to be utilised without electrolyte decomposition concerns. Multiple major battery and automotive companies including Toyota, QuantumScape, and Solid Power are pursuing solid-state silicon anode battery programmes targeting EV deployment in the late 2020s, with successful commercialisation creating a step-change improvement in EV battery performance that would dramatically accelerate silicon anode market growth. The EV market's range and fast-charge performance premium creates a pricing context where silicon anode batteries can command 10 to 20% premium over graphite-based EV batteries while still enabling positive OEM business cases through reduced battery pack size and manufacturing cost at scale.

Recent Developments:

-

2025: Group14 Technologies and BASF advanced commercial deployment of their SCC55 silicon carbon composite material, with the joint product demonstrating over 1,000 cycles at 80% capacity retention and 80% SOC in under five minutes, securing design-in commitments from premium EV and consumer electronics customers.

-

2025: Enovix Corporation expanded production at its Malaysia Fab2 facility for silicon anode batteries targeting IoT, wearable, and mobile device applications, advancing its manufacturing scale to serve growing commercial customer demand from consumer electronics OEMs.

Silicon Anode Battery Companies are:

-

Sila Nanotechnologies Inc.

-

Amprius Technologies Inc.

-

Enovix Corporation

-

Enevate Corporation

-

OneD Material Inc. (OneD Battery Sciences)

-

California Lithium Battery Inc. (CalBattery)

-

ENOVIX Corporation

-

XG Sciences Inc.

-

BTR New Material Group Co. Ltd.

-

Shin-Etsu Chemical Co. Ltd.

-

Umicore SA

-

Panasonic Holdings Corporation

-

Samsung SDI Co. Ltd.

-

LG Energy Solution Ltd.

-

SK On Co. Ltd.

-

CATL (Contemporary Amperex Technology Co. Ltd.)

-

QuantumScape Corporation

-

Solid Power Inc.

Silicon Anode Battery Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 536.6 Million |

| Market Size by 2035 | USD 31.27 Billion |

| CAGR | CAGR of 50.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Capacity (Less than 1,500 mAh, 1,500 to 2,500 mAh, 2,500 to 3,500 mAh, More than 3,500 mAh) •By Anode Type (Silicon Carbon Composite, Pure Silicon, Silicon Oxide) •By Application (Consumer Electronics, Electric Vehicles, Energy Storage Systems, Medical Devices, Aerospace and Defense, Others) •By End-User (Automotive, Industrial, Commercial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Group14 Technologies Inc., Sila Nanotechnologies Inc., Amprius Technologies Inc., Enovix Corporation, Enevate Corporation, Nexeon Ltd., OneD Material Inc. (OneD Battery Sciences), California Lithium Battery Inc. (CalBattery), ENOVIX Corporation, XG Sciences Inc., BTR New Material Group Co. Ltd., Shin-Etsu Chemical Co. Ltd., Umicore SA, Panasonic Holdings Corporation, Samsung SDI Co. Ltd., LG Energy Solution Ltd., SK On Co. Ltd., CATL (Contemporary Amperex Technology Co. Ltd.), QuantumScape Corporation, Solid Power Inc. |

Frequently Asked Questions

The Silicon Anode Battery Market is expected to grow at a CAGR of 50.16% from 2026 to 2035.

The Silicon Anode Battery Market was valued at USD 536.6 million in 2025.

The Less than 1,500 mAh segment dominated with approximately 49% of revenues in 2024, driven by wearables, medical devices, and small premium consumer electronics where silicon anode energy density improvements deliver the most immediately compelling device performance benefits including extended runtime within miniaturised form factors.

The 1,500 to 2,500 mAh segment is expected to grow at the fastest CAGR of approximately 57.92% from 2026 to 2035, driven by rapidly rising adoption in premium smartphones, compact drones, and IoT devices where silicon anode technology enables thinner designs or meaningfully extended battery life within the same physical form factors consumers prefer.

North America dominated the Silicon Anode Battery Market in 2025, led by the United States with the world's highest concentration of silicon anode technology companies including Group14 Technologies, Sila Nanotechnologies, Enovix, and Amprius.

Get in Touch