Snack Food Packaging Market Key Insights:

Get More Information on Snack Food Packaging Market - Request Sample Report

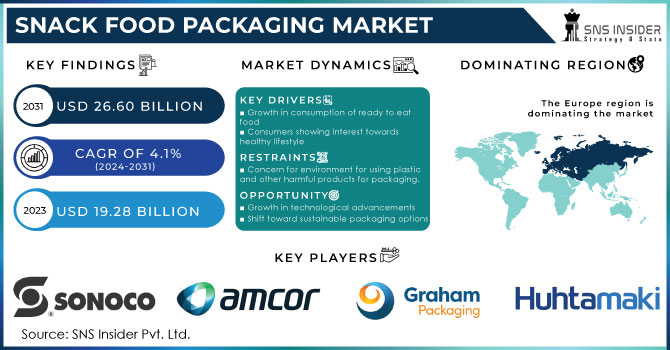

The Snack Food Packaging Market size was USD 19.28 billion in 2023 and is expected to Reach USD 26.60 billion by 2031 and grow at a CAGR of 4.1% over the forecast period of 2024-2031.

The design, manufacture, and distribution of packaging products and services especially suited for snack food products is referred to as the "snack food packaging market." It includes a broad range of packaging types and materials used to safeguard, preserve, and improve the visual appeal of different snack food items, such as chips, cookies, candies, nuts, popcorn, and other such goods.

The market for snack food packaging attempts to offer practical and appealing packaging options that satisfy the particular needs of snack foods. Freshness of the product, defense against physical harm, moisture control, barrier qualities, practical features, and appealing visual presentation are a few examples of these factors.

Snack food packaging has many benefits, such as prolonging product shelf life, guaranteeing product integrity and safety, facilitating transportation and distribution, offering branding and marketing opportunities, and improving the entire shopping experience. The market includes many different packaging types, such as bags, pouches, boxes, cans, and wraps, as well as a large variety of packaging materials, such as plastics, paperboard, metals, and glass.

The snack food packaging market is continually evolving to satisfy shifting industry demands due to shifting customer preferences, technology improvements, and sustainability concerns. To meet the changing needs of both snack food manufacturers and customers, this includes the creation of green packaging solutions, intelligent packaging technology, and creative designs.

MARKET DYNAMICS

KEY DRIVERS:

-

Growth in consumption of ready to eat food

There has been substantia growth in consumption of ready to eat food which has directly led to the growth of snack food packaging market. The study has shown that consumers are consuming snacks in between their meals which has shown growth in snack food packaging market. Consumers are choosing for healthier snack options but at the same time are not ready to compromise the taste and quality of the snacks they are consuming. This trend in today’s snack food market has shown growth in recent years and is also gaining momentum in our forecast period of 2024 – 2031.

• Consumers showing interest towards healthy lifestyle

• Increasing demand for the franchise food organization

• Preference towards sustainable plastic packaging

RESTRAIN:

-

Concern for environment for using plastic and other harmful products for packaging.

The concern regarding environment for using harmful products and plastic for the purpose of packaging is major problem for global snack food packaging industry. Use of plastic for snack food packaging has created pollution, and their disposal is also the major problem faced in today’s society.

OPPORTUNITY:

• Growth in technological advancements

Various new technological advancements and developments have been seen in snack food packaging market. This technological advancement has brought with them the growth of the snack food packaging market. Development in the packaging methods, easy to use products which will be easy for consumers to use is surely a great opportunity for snack food packaging industry. Materials such as BOPP, CPP in making packaging look more creative and attractive which is attracting customers.

• Shift toward sustainable packaging options

CHALLENGES:

• Environmental Concerns

The use of plastic and other such products and harming the environment so it is a challenge for manufacturers to research and develop eco friendly solutions for snack food packaging.

IMPACT OF RUSSIAN UKRAINE WAR

Russia Ukraine war resulted in the disruption of supply chain, this will reduce the flow the raw materials, which will further lead to delay in production of packaging material hence resulting in increase in cost. Since rise in downfall of raw materials will lead to price volatility. Manufactures will face problem is maintaining pricing for their product. Due to disruption of supply chain market size will be affected.

IMPACT OF ONGOING RECESSION

Consumer spending usually decreases during a recession as people become more frugal with their money. This may lead to a decline in the demand for snack foods as a whole, which may have an impact on the demand for snack food packaging. Reduced orders and sales volumes may affect snack food packaging businesses, which would result in lower revenue.

Consumers frequently modify their tastes and purchase behaviours during a recession. They might choose to forgo snacks completely or choose more reasonably priced options. This may have an effect on the types of snack food items sold and, subsequently, the packaging specifications. Companies that make packaging may need to adjust to shifting consumer preferences and create packaging options that meet changing market demands.

Consumers and businesses frequently place a higher priority on efficiency and value for money during a recession. This could lead to a greater focus on packaging options that provide benefits for sustainability, increased product protection, longer shelf lives, or cost savings. Packaging businesses that can provide affordable and effective solutions may be better prepared to withstand the current economic climate.

IMPACT OF COVID-19

Covid-19 brought with him the problems to manufacturers, dealers as well as for the retailers on the growing market of snack food packaging. Lockdown was imposed by all the governments across the world, due to which supply chain was completely under restrictions. International market trade was stopped which affected the snack food packaging market at a huge scale.

Unavailability of raw materials, labor also became the reason for reduced growth of the snack food packaging market.

KEY MARKET SEGMENTS

By Raw Material

-

Plastic

-

Metal

-

Paper

-

Others

By Packaging

-

Rigid

-

Flexible

By Application

-

Bakery Snacks

-

Candy & Confections

-

Nuts & Dried Fruits

-

Others

REGIONAL ANALYSIS

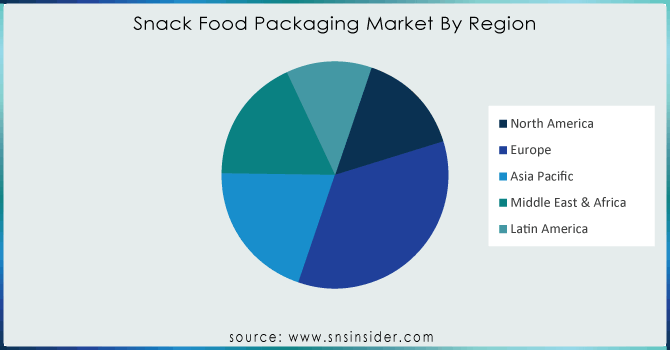

US market is likely to grow for bakery and snack foods.

Europe is second largest growing market of snack food packaging.

Asia-Pacific region is largely contributed by China, India and Japan in snack food packaging.

Middle East and Africa & Latin America will show a little growth over forecast period of 2024 – 2031. They will create opportunities for growth of snack food packaging market.

Get Customised Report as per Your Business Requirement - Enquiry Now

REGIONAL COVERAGE:

North America

-

USA

-

Canada

-

Mexico

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

Asia-Pacific

-

Japan

-

South Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of the Middle East & Africa

Latin America

-

Brazil

-

Argentina

-

Rest of Latin American

RECENT DEVELOPMENTS

-

Research & Development is going on the use of plant-based materials, recyclable compostable packaging.

-

Innovation in packaging such as use of BOPP, CPP for making packaging more attractive.

-

For the purpose of consumer safety the retailers are shifting towards personalized packaging option for consumers.

Key Players:

The major key players in the snack food packaging are Sonoco Products (US), Modern-Pak Pte Ltd (US), Graham Packaging Holdings, ProAmpac (US), Huhtamaki Global, Bemis Company (US), Amcor (Australia), Clondalkin Group, Swiss pack private limited, Bryce Corporation (US), Sealed Air Corporation (US) and Others players.

| Report Attributes | Details |

| Market Size in 2023 | US$ 19.28 Bn |

| Market Size by 2031 | US$ 26.60 Bn |

| CAGR | CAGR of 4.1% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Raw material (Plastic, Metal, Paper, Others) • By Packaging (Rigid, Flexible) • By Application (Bakery snacks, Candy & confections, Savory snacks, Nuts & dried fruits, Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Sonoco Products (US), Modern-Pak Pte Ltd (US), Graham Packaging Holdings, ProAmpac (US), Huhtamaki Global, Bemis Company (US), Amcor (Australia), Clondalkin Group, Swiss pack private limited, Bryce Corporation (US), Sealed Air Corporation (US) and Others players |

| Key Drivers | • Growth in consumption of ready to eat food |

| Market Opportunities | • Growth in technological advancements |

Get in Touch