Software Composition Analysis Market Report Scope & Overview:

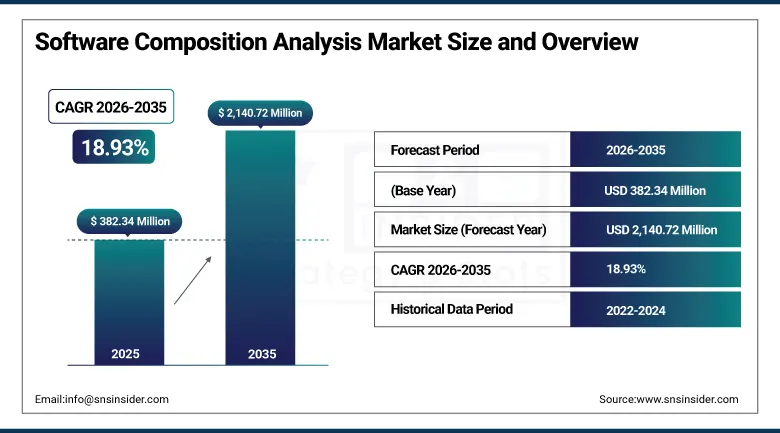

The Software Composition Analysis Market was valued at USD 382.34 Million in 2025 and is expected to reach USD 2,140.72 Million by 2035, growing at a CAGR of 18.93% from 2026 to 2035.

The global software composition analysis market is growing at a tremendous rate due to the exponential adoption of open-source software across all industry verticals, which creates software supply chain security vulnerabilities that organizations cannot manage without automated dependency analysis tools. Software composition analysis platforms scan application codebases, build manifests and binary files to detect all open source components and third-party libraries, map them against vulnerability databases, assess their licensing compliance status and generate software bills of materials that satisfy regulatory and procurement requirements.

The market is driven by increasing adoption of open-source software across industries including technology, finance, and healthcare that simultaneously increases innovation velocity and security risk exposure, rising cyber-attacks targeting open-source supply chains whose SolarWinds and Log4Shell incidents demonstrated the catastrophic potential of compromised dependency chains, and stringent regulatory compliance requirements under NIST, CISA executive orders, GDPR, and the EU Cyber Resilience Act that mandate software bill of materials generation and open-source vulnerability management.

In 2024, Synopsys enhanced its Black Duck SCA solution with AI-driven vulnerability detection that substantially strengthened risk assessment accuracy by correlating open-source component vulnerability data with application context, runtime reachability analysis, and exploitability intelligence.

Software Composition Analysis Market Size and Forecast

-

Market Size in 2026E: USD 454.78 Million

-

Market Size by 2035: USD 2,140.72 Million

-

CAGR: 18.93% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Software Composition Analysis Market - Request Free Sample Report

Software Composition Analysis Market Trends

-

SBOM generation is becoming mandatory across government and critical infrastructure sectors to improve software supply chain transparency.

-

AI-powered reachability analysis is enhancing risk prioritization by identifying exploitable vulnerabilities and reducing false positives.

-

SCA platforms are expanding to scan containers, Kubernetes environments, and infrastructure-as-code assets alongside application code.

-

Automated open-source license compliance is gaining importance for procurement, audits, and M&A due diligence activities.

-

IDE-integrated SCA tools are enabling real-time vulnerability and license checks during software development, supporting shift-left security practices.

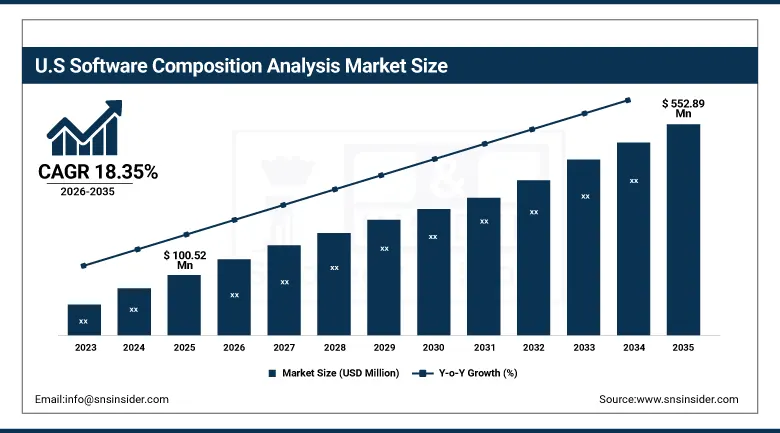

U.S. Software Composition Analysis Market Outlook

The U.S. Software Composition Analysis Market was valued at approximately USD 100.52 Million in 2025 and is expected to reach approximately USD 552.89 Million by 2035, growing at a CAGR of approximately 18.35%.

The U.S. is the world’s most commercially important SCA market, with global headquarters for Synopsys, Snyk, Sonatype, Veracode, and GitHub whose SCA platform revenues set global commercial benchmarks for open-source security investment. The White House Executive Order on Improving the Nation’s Cybersecurity, CISA’s Known Exploited Vulnerabilities catalogue and the NTIA’s Software Bill of Materials Minimum Elements guidance collectively constitute the most comprehensive government-led SCA adoption framework in the world. The sheer size of U.S. enterprise open-source software consumption, with the average enterprise application including hundreds of open-source components, creates systematic SCA procurement motivation that compounds with regulatory compliance timeline.

In 2024, GitHub expanded its Advanced Security platform with enhanced secret scanning, dependency review, and security overview capabilities that provide organization-wide visibility into open-source vulnerability exposure across all repositories within a GitHub Enterprise environment, enabling security teams to track remediation progress and measure open-source risk posture improvement without requiring separate SCA platform deployment.

Software Composition Analysis Market Segment Analysis

-

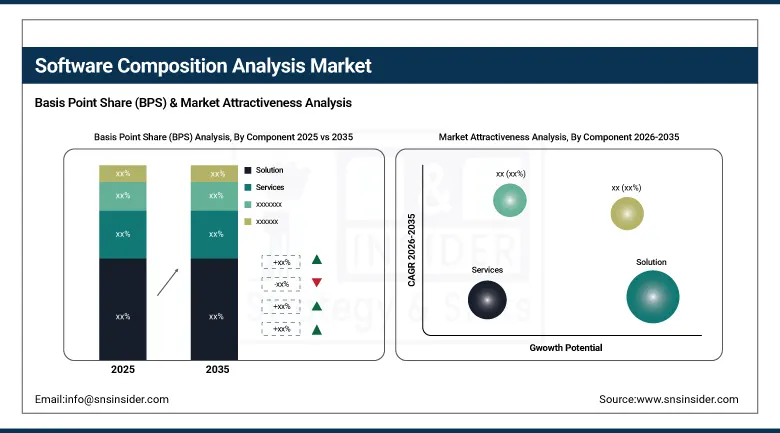

By Component, the Solution segment dominated the software composition analysis market with approximately 64% share in 2025, while the Services segment is the fastest growing at approximately 19.64% CAGR.

-

By Deployment, the Cloud segment dominated the software composition analysis market with approximately 52% share in 2025, while the On-Premise segment is the fastest growing at approximately 19.46% CAGR.

-

By Enterprise Size, the Large Enterprises segment dominated the software composition analysis market with approximately 55.24% share in 2025, while the Small and Medium Enterprises segment is the fastest growing at approximately 19.55% CAGR.

-

By End Use, the IT & Telecom segment dominated the software composition analysis market with the largest share in 2025, while the Healthcare segment is the fastest growing as electronic health record system open-source dependency management.

By Component, solutions dominate, services grow fastest

Solutions continued to be the most dominant part of the software composition analysis market in 2025, with a share of approximately 64%. The largest portion of open source security programme technology spend is on the SCA platform, which provides the automated scanning, vulnerability correlation, license classification, and SBOM generation capabilities that are the operational foundation for software supply chain security management. Every organization that does open source vulnerability management establishes SCA platform procurement whose value is proportional to the number of repositories, applications and CI/CD pipeline integrations needed for the continuous scanning coverage.

The fastest growing component is Services at approximately 19.64% CAGR. The complexity of integrating SCA tools into existing software development workflows, the cultural change that DevSecOps adoption requires, and the specialized expertise needed to configure effective vulnerability triage policies create professional services demand that scales with SCA platform adoption. Any organization that deploys a SCA platform will establish an implementation services engagement that includes CI/CD integration, policy configuration, developer training, and SBOM programme design.

By Deployment, cloud dominates, on-premise grows fastest

Cloud deployment continued to dominate the software composition analysis market with a 52% share in 2025. Automatic vulnerability database updates in cloud-based SCA platforms that synchronize in real-time with the National Vulnerability Database, GitHub Advisory Database and commercial threat intelligence sources provide current vulnerability assessment without manual update management, creating a specification preference for development teams whose continuous delivery pipelines require accurate and timely security feedback.

On-premise deployment is the fastest growing model with a CAGR of almost 19.46%. The structured demand for on-premise SCA comes from classified software development environments in government and defense, financial sector organizations with stringent data residency requirements, and critical infrastructure operators who are bound by code confidentiality obligations that prohibit cloud-hosted scanning of proprietary application source code. All of them every defense contractor with classified software development that needs on-premise security tooling, every bank whose regulatory environment prohibits the transfer of source code to cloud-hosted scanning infrastructure, and every critical infrastructure operator whose operational technology software needs air-gapped security analysis – create on-premise SCA procurement whose regulatory mandate supports above-average segment growth.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

Large enterprises held the leading enterprise size with around 55.24% of the software composition analysis market in 2025. The commercial concentration of SCA spending among large organizations is a reflection of their large open-source software portfolios, complex transitive dependency chains with thousands of indirect dependencies per application, and regulatory compliance obligations under NIST 800-218, GDPR article 32, and sector-specific frameworks that create documented software supply chain security requirements. SCA procurement is led by industry titans such as Microsoft, IBM and technology sector companies whose software development organizations produce hundreds of applications each year and whose scope of scanning and compliance documentation needs support broad enterprise SCA platform investments.

The fastest growing segment is small and medium enterprises at approximately 19.55% CAGR due to growing awareness of open-source vulnerability risk, expanding cyber insurance market requirements for software security documentation including SBOM production capability and availability of affordable cloud-based SCA tools at per-developer or per-repository subscription pricing creating first-time SCA procurement motivation. Each SME whose renewal of a cyber insurance policy creates SCA procurement creates SCA procurement whose commercial motivation is compliance-driven rather than commercially calculated.

By End Use, IT & telecom dominates, healthcare grows fastest

IT and telecom retained its top end-use spot in the software composition analysis market in 2025. The enormous usage of open-source software in the tech industry, paired with a software development culture of maximum dependency reuse, leads to applications with hundreds to thousands of direct and transitive open-source dependencies in a codebase, thus making it the industry vertical with the most intensive per-organization SCA scanning requirement. The structured adoption motivation for SCA procurement arises from each technology company with software products that contain open-source components, and the compliance of their SCA procurement with customer security requirements, software composition disclosure obligations in procurement contracts, and CISA known exploited vulnerability remediation guidance.

Healthcare is the fastest growing end-use segment The healthcare sector’s growing DevSecOps adoption, electronic health record system open-source dependency vulnerability management requirements under HIPAA’s security rule technical safeguard provisions, and the FDA’s medical device cybersecurity guidance requiring software bill of materials from medical device manufacturers create structured SCA procurement across hospital systems, health IT vendors and medical device developers simultaneously. The mandate to be compliant ensures investment irrespective of commercial calculation, with each submission for a medical device needing FDA SBOM documentation, which drives adoption of the SCA platform.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Software Composition Analysis Market Insights

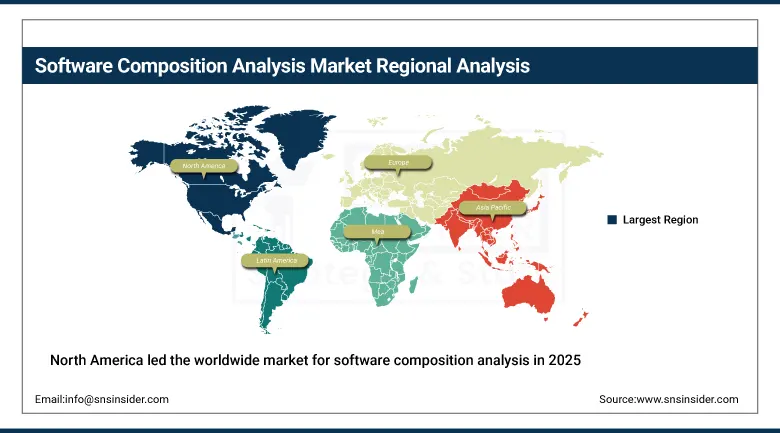

North America led the worldwide market for software composition analysis in 2025 owing to the highest level of open-source software use in the world, the most rigorous SCA regulations enforced by the government, and the commercial offices of Synopsys, Snyk, Sonatype, Veracode, and GitHub. The US makes up around 87.4% of North American revenues owing to the massive scale of enterprise software development in the country, the SBOM requirement of the White House cybersecurity executive order, and the CISA known exploited vulnerabilities requirements.

Canada makes up around 12.6% of North American revenues owing to the open source security spending in the technology sector, the government software security requirements of the federal government for government IT procurement, and the software supply chain risk management spending in the financial services sector.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Software Composition Analysis Market Insights

Europe is a SCA market that is driven by compliance, as the software security requirements of the EU Cyber Resilience Act, GDPR article 32's technical security measures for software processing personal data, and NIS2 directive's software supply chain security requirements for essential entities form a complete regulation-driven SCA adoption framework. Europe's second-largest country, Germany, contributes around 22.3% of the revenue through the country's software manufacturing industry, software-defined vehicles in the automotive industry, and software security standards developed by BSI.

The United Kingdom, France, and the Netherlands are important secondary markets, where the guidance on software security by NCSC, the software compliance investments of the financial sector, and DevSecOps adoption in the technology sector form a consistent procurement process. Veracode's presence in Europe and Checkmarx's Israeli-based European operations ensure consistent SCA market supply in the region.

Asia Pacific Software Composition Analysis Market Insights

Asia Pacific is the region with the fastest growth in the SCA market because of the adoption of open-source in the technology industry in China, the software security spending in India's rapidly growing IT services industry, the enterprise software compliance programs in Japan, and the open-source management requirement in South Korea's technology manufacturing industry. China has an estimated market share of 44.8% in the Asia Pacific region due to the size of its software development industry, the cybersecurity law's software security requirements for critical information infrastructure operators, and the technology industry's adoption of open-source.

India is the emerging market with the greatest commercial dynamism in Asia Pacific, which has been caused by the software security requirement in the IT services industry's global delivery centers, DevSecOps adoption in the software product companies, and open-source security spending in the digital public infrastructure by the government.

MEA & Latin America Software Composition Analysis Market Insights

The UAE is at the forefront of MEA revenues with about 31.2% attributed to its technology sector open-source security investment, TDRA's software security regulation on cybersecurity, and financial sector software supply chain risk management compliance. The complementing demand from Saudi Arabia is driven by its Vision 2030 technology investment. Brazil is at the lead of Latin America revenues with about 44.2% contributed by its technology sector DevSecOps adoption, LGPD software security compliance driving force, and the financial sector investment in open-source vulnerability management. Mexico and Colombia together sustain regional market growth until 2035.

Market Dynamics

Growth Drivers: Open-source software adoption creating software supply chain vulnerability exposure and regulatory SBOM mandates creating non-discretionary compliance investment

The rapid adoption rate of open source software across enterprise development organizations is the most commercially important growth driver for the SCA market. According to the Linux Foundation, 70% to 90% of today's software applications use open source components, where an enterprise-level application may include over 500 open source components. Each open source component brings an exposed vulnerability point that can be tracked only with automated SCA tools.

SBOM regulatory requirements bring non-discretionary SCA investments that reinforce commercial motivations. The minimum SBOM elements requirement by U.S. executive order 14028 for government software acquisitions, FDA cybersecurity guidance that calls for SBOMs for medical devices, and EU Cyber Resilience Act software security requirements combine to set compliance deadlines that allow SCA platform adoption beyond commercial motives alone.

Restraints: High implementation cost and integration complexity with existing development workflows

The high cost of implementation and integration of complete SCA solutions makes their use unaffordable for those organizations which have limited budgets and face challenges such as workload of development workflow process disruption, complex policies and configurations and pre-existing backlog of vulnerabilities. The cost of implementation of any SCA program involves development costs to ensure compatibility of SCA scanning within the existing CI/CD process without increasing build times.

Complexity of managing transitive dependencies of open source components leads to the issue of sustaining alert fatigue and remediation prioritization. False-positive results due to vulnerabilities which may not actually be exploitable in the specific context of a particular application make it difficult to have confidence in the accuracy of SCA tools.

Opportunities: AI-powered reachability analysis and regulatory SBOM mandate expansion

AI-based reachability analysis constitutes the most commercial impact SCA product innovation opportunity within reach. Conventional SCA products flag all vulnerabilities in dependency components irrespective of whether the vulnerable code path is actually executed by the software utilizing the component. Reachability analysis using AI flags only the vulnerabilities whose corresponding functions are indeed called in the particular application context, thereby lowering the number of flagged issues by up to 95% in some application contexts while increasing the confidence of the few remaining results that pose an actual threat.

Expanding SBOM mandates to other regulated industries and overseas jurisdictions ensures procurement of SCA in companies that do not have a procurement push due to regulation-based requirements. Every new SBOM mandate passed by a government procurement authority, a financial regulator or health regulatory authority ensures another procurement wave in the software industry whose clients have such compliance-based requirements.

Recent Developments:

-

2024: GitHub expanded its Advanced Security platform in 2024 with enhanced dependency review, secret scanning, and organization-wide security overview capabilities, providing enterprise visibility into open-source vulnerability exposure across all repositories without requiring separate SCA platform deployment.

-

2024: Snyk launched AI-powered code security enhancements in 2024 with Deep Code AI integrating static application security testing and SCA findings into unified developer feedback within CI/CD pipelines, reducing context switching between security tools during the open-source vulnerability remediation workflow.

-

2023: Synopsys enhanced its Black Duck SCA solution in 2023 with AI-driven vulnerability detection and reachability analysis that strengthened risk assessment accuracy by correlating open-source vulnerability data with application runtime context and actual code path invocation.

Software Composition Analysis Market Key Players

-

Synopsys Inc. (Black Duck)

-

Snyk Ltd.

-

Sonatype Inc.

-

Veracode Inc. (Broadcom)

-

GitHub Inc. (Microsoft)

-

FOSSA Inc.

-

WhiteSource Software Ltd. (Mend)

-

Flexera Software LLC

-

Checkmarx Ltd.

-

JFrog Ltd.

-

Anchore Inc.

-

GitLab Inc.

-

Micro Focus International plc

-

Contrast Security Inc.

-

Apiiro Security Ltd.

-

Socket Security Inc.

-

Phylum Inc.

-

Semgrep Inc.

-

Endor Labs Inc.

-

Cycode Ltd.

Software Composition Analysis Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 382.34 Million |

| Market Size by 2035 | USD 2,140.72 Million |

| CAGR | CAGR of 18.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Services) • By Deployment (Cloud, On-Premise) • By Enterprise Size (Large Enterprises, Small and Medium Enterprises) • By End Use (BFSI, IT & Telecom, Manufacturing, Government & Defense, Retail & E-Commerce, Automotive, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Synopsys Inc. (Black Duck), Snyk Ltd., Sonatype Inc., Veracode Inc. (Broadcom), GitHub Inc. (Microsoft), FOSSA Inc., WhiteSource Software Ltd. (Mend), Flexera Software LLC, Checkmarx Ltd., JFrog Ltd., Anchore Inc., GitLab Inc., Micro Focus International plc, Contrast Security Inc., Apiiro Security Ltd., Socket Security Inc., Phylum Inc., Semgrep Inc., Endor Labs Inc., and Cycode Ltd. |

Frequently Asked Questions

The Software Composition Analysis Market is expected to grow at a CAGR of 18.93% from 2026 to 2035.

The Software Composition Analysis Market was valued at USD 382.34 Million in 2025.

The extraordinary pace of open-source software adoption creating unmanaged dependency vulnerability exposure across enterprise application portfolios, and regulatory SBOM mandates under the U.S. executive order, FDA medical device guidance, and EU Cyber Resilience Act creating non-discretionary compliance-driven SCA investment.

Solution dominated the Software Composition Analysis Market with approximately 64% share in 2025, while Services is the fastest growing segment at approximately 19.64% CAGR.

North America dominated the Software Composition Analysis Market in 2025, while Asia Pacific is the fastest growing region driven by China's technology sector open-source adoption and India's IT services sector DevSecOps investment.

Get in Touch