Solar Silicon Wafer Market Report Scope & Overview:

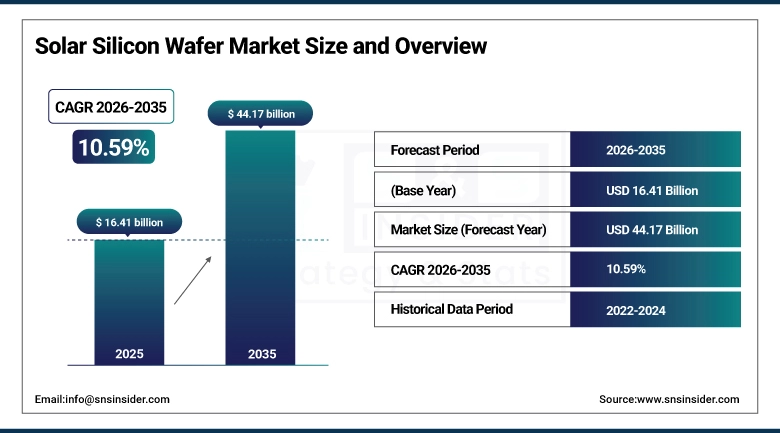

The Solar Silicon Wafer Market was valued at USD 16.41 billion in 2025 and is expected to reach USD 44.17 billion by 2035, growing at a CAGR of 10.59% from 2026-2035.

The Solar Silicon Wafer Industry can be regarded as an important segment within the global photovoltaics market and plays a vital role in the creation of efficient solar cells and modules. The definition of solar silicon wafers can be seen as the thin semiconductor discs which are manufactured mainly using monocrystalline and polycrystalline silicon. Solar silicon wafers serve as the base materials and is used in photovoltaic cells to determine the performance, durability, and power-generating capabilities of solar cells. The growing trend towards renewable energy sources, carbon neutrality, and energy security is increasing increased the demand for advanced solar wafer technologies.

Solar Silicon Wafer Market revolves around the processes of refining and purifying silicon, silicon casting, wafer slicing process of silicon wafers, pull technology of crystals, and post-integration processes for photovoltaic modules and their applications such as solar batteries, solar inverters, and mounting systems. The emergence of innovative designs of n-type wafers, TOPCon, heterojunction HJT cells, M10 wafers, and G12 wafers has resulted in improved efficiency levels with reduced manufacturing costs.

Longi Green Energy Technology is one of the main companies in the industry and would increase its ability to produce high efficiency mono-crystalline wafers. The company would be focused on utilizing wafer technology innovations, vertical integration in the production of solar panels, and capacity increase to improve international solar supply chains. All of that would be done during the period from 2026 until 2035 to meet increased demand for PV products.

Market Size and Forecast

-

Market Size in 2025: USD 16.41 Billion

-

Market Size by 2035: USD 44.17 Billion

-

CAGR: 10.59% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Solar Silicon Wafer Market - Request Free Sample Report

Solar Silicon Wafer Market Trends

-

The fast uptake of the N-type silicon wafers has brought about change in the solar industry since these wafers are more efficient than the traditional P-type silicon wafers and have less degradability besides offering higher energy yields. There is a growing trend where manufacturers are adopting new technologies like TOPCon and heterojunction for producing N-type wafers.

-

There is an increasing demand for bigger wafer designs like M10 and G12 in the utility scale solar project industry. Larger wafer design makes modules more powerful while at the same time reduces system cost in large-scale solar projects.

-

The manufacturing of ultra-thin wafers is currently one of the important trends in the industry. Wafer thinning helps manufacturers save on silicon usage and material costs.

-

The application of automation and smart technologies in manufacturing is increasingly becoming popular in wafer production facilities. The manufacturers have been adopting inspection techniques, robotics, and digital monitoring systems based on AI in order to enhance efficiency and avoid downtimes.

-

The process of localization is taking place all around the world as countries strive to decrease dependency on foreign solar products and establish manufacturing facilities for renewables within their territories. Government incentives are being offered in order to facilitate the production of silicon wafers and other components.

-

The demand for premium photovoltaic modules continues to grow, due to the significant increase in investments in rooftop installations, large-scale solar farms, and mixed renewable energy ventures. This has led to increased support for the premium silicon wafers technology.

-

Sustainability is becoming an increasingly relevant issue in today’s world as companies work toward meeting the growing number of environmental laws and regulations worldwide. Companies are actively developing methods of producing green silicon.

U.S. Solar Silicon Wafer Market Size Outlook:

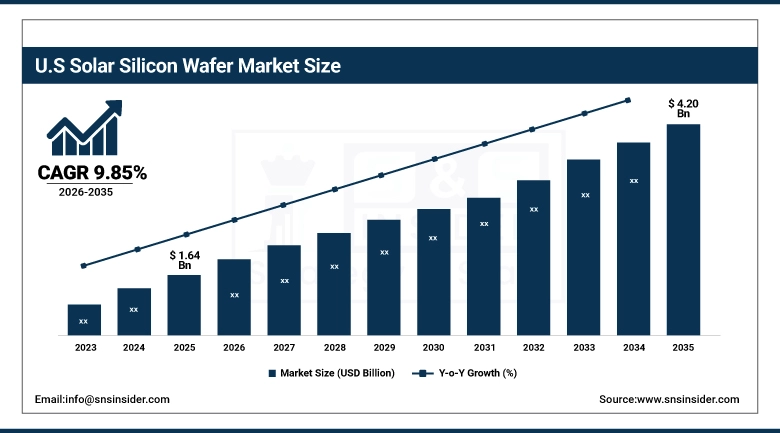

The U.S. Solar Silicon Wafer Market was valued at USD 1.64 billion in 2025 and is expected to reach USD 4.20 billion by 2035, growing at a CAGR of 9.85%. Strategically, the United States market is very significant for the Solar Silicon Wafer Market due to the presence of increasing investments in domestic manufacturing of solar, deployment of renewable energy, and clean energy policies in the country. With growing investment and development of solar farms at a utility scale, solar installation on commercial rooftops, and residential solar, many firms and individuals have started moving towards energy sources that are more environmentally friendly. Clean energy independence policies in the country have attracted huge investments into solar wafer and photovoltaic manufacturing. The Inflation Reduction Act (IRA) has played an important role in accelerating investment in U.S. solar manufacturing facilities owing to the availability of tax credits and production incentives on solar components. These policies are not only improving manufacturing facilities within the nation but also attracting both national and foreign investment into photovoltaic manufacturing technology. With growing demand for electricity in data centers, electric vehicles, and industries, the demand for energy-efficient solar power systems has increased considerably.

There has been an observed uptick in the number of uses made by the U.S. market of high-efficiency monocrystalline wafers. This is especially true for solar projects where the need for higher energy efficiency is paramount. Innovations made within the industry for the manufacture of efficient TOPCon and heterojunction solar cells have also increased demand for high-efficiency silicon wafers. Additionally, the emphasis being placed on supply chain robustness and energy security in recent times is also leading to more such investments. LONGi Green Energy Technology has made a name for itself in the American solar market, mainly because of its involvement in the manufacture of high-efficiency photovoltaics.

Solar Silicon Wafer Market Segment Analysis

-

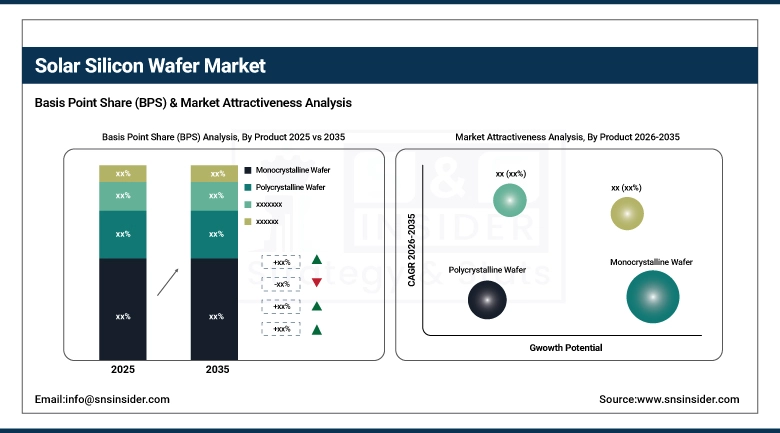

By Product, Monocrystalline dominated in 2025 with largest share; Polycrystalline growing at the fastest CAGR.

-

By Application, PV modules dominated the market in 2025; solar cell segment is expected to grow rapidly.

By Product: Monocrystalline dominant, Polycrystalline fastest CAGR

Monocrystalline silicon wafers have continued to maintain dominance in the Solar Silicon Wafers market with a large share of total revenue predicted for 2025 on account of their higher efficiencies, longer life, and better performance at low light and high temperatures. Monocrystalline silicon wafers have seen wide use in both residential and utility-scale applications as they allow more electricity to be produced from available installation space. Ongoing innovation in N-type silicon wafers, TOPCon, heterojunction cells, as well as M10 and G12 wafers is expected to bolster segment growth further. Lower costs of production, wafer automation, and investment in efficient photovoltaic technologies are also contributing to global adoption.

The forecast period is likely to see consistent growth for polycrystalline wafers, driven by the benefit of low cost and rising adoption of these wafers in affordable solar installations, especially in emerging countries. Even if the efficiency of polycrystalline wafers is relatively less when compared to monocrystalline wafers, the former continue to enjoy significant popularity in large installations because of cost-effectiveness. Improvement in wafer quality and efficiency, alongside sustainability in manufacturing, is being sought by manufacturers to stay competitive. Increasing solar capacity installations and favorable renewable energy regulations are likely to support demand throughout the forecast period.

Solar Silicon Wafer Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

84% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

68% |

|

Middle East & Africa |

Saudi Arabia |

34% |

|

Latin America |

Brazil |

46% |

Asia Pacific Solar Silicon Wafer Market Insights

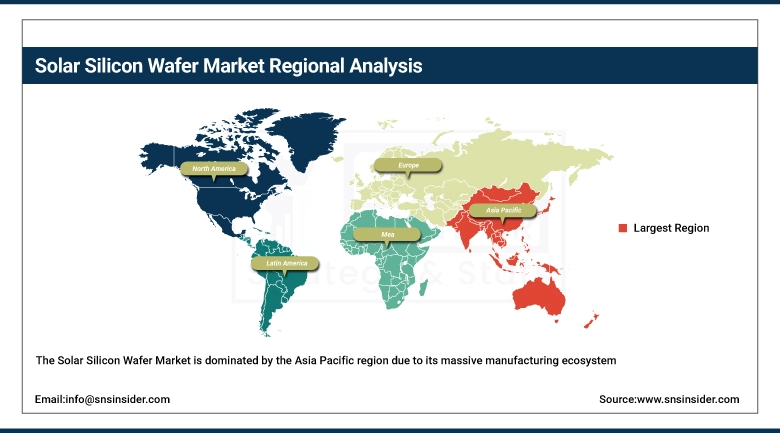

The Solar Silicon Wafer Market is dominated by the Asia Pacific region due to its massive manufacturing ecosystem, efficient photovoltaic supply chain, and quick implementation of renewable energy sources. The reason for that is that China is still the main manufacturer of silicon wafers, solar cells, and photovoltaic modules due to significant manufacturing capacity, affordable production, and constant investments in innovative solar power technology. Other countries, including India, Japan, South Korea, and Vietnam, are developing their solar power infrastructure in order to cope with increased demands in electricity and to reach their carbon neutral status. Growing interest in renewable energy generation, utility-scale solar farms, and solar panel manufacturing in the region stimulates further growth of the market. There is a constantly growing demand for highly effective monocrystalline silicon wafers and bigger-sized wafers due to improved energy efficiency and decreased costs per unit of produced energy.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Solar Silicon Wafer Market Insights

North America presents itself as an important market for the use of solar silicon wafers owing to growing investments in local solar manufacturing, large-scale renewable energy development projects, and clean energy transition programs. In the United States, there is a rising demand for solar silicon wafers because of increased solar farm, commercial roof top, and residential PV installation projects. Local wafer, solar cell, and module manufacturing facilities are getting funded rapidly with help from government incentives, manufacturing subsidies, and renewable energy programs. Demand for high-efficiency monocrystalline wafers is growing quickly with growing adoption of state-of-the-art solar technology, including TOPCon, and heterojunction cells. There is also a growing emphasis on self-reliance within the region with respect to solar component manufacturing, and hence a vertical integration of solar manufacturing ecosystems. The need for more power to meet the growing requirement of electric vehicles, data centers, and industrial decarbonization efforts is also playing an important role in boosting the adoption of solar energy.

Europe Solar Silicon Wafer Market Insights

The demand for Solar Silicon Wafers in Europe is continuously growing owing to increased goals for renewable energy, carbon emissions reduction, and substantial investments in sustainable energy infrastructure. Countries such as Germany, France, Italy, Spain, and the Netherlands are increasingly installing solar energy systems in order to minimize their dependency on non-renewable sources of energy and increase energy security. There is an emphasis on energy transition initiatives and localization of solar wafer production in Europe owing to supply chain risks. High performance wafers for use in residential, commercial, and industrial solar energy projects are experiencing growing demand due to stringent energy efficiency requirements and space constraints in cities. Funding of photovoltaic technologies is being provided by European governments through various initiatives that provide financial incentives for green energy production and decarbonization of industries. The market is experiencing an uptick in terms of demand for advanced solar solutions such as the use of TOPCon, heterojunction cells, and bifacial modules.

MEA and Latin America Solar Silicon Wafer Market Insights

The expansion of the Middle East & Africa Solar Silicon Wafer Market is being driven by growing investments in utility-scale solar power plants, energy diversification efforts, and supportive government policies for adoption of renewable energy sources. Many countries in the Middle East & Africa regions, including Saudi Arabia, UAE, South Africa, and Egypt are making substantial investments in utility-scale solar farms to minimize reliance on traditional coal-powered power generation systems.

The Latin American region can be considered an attractive solar silicon wafer market because of rising investments in renewable energy generation capacity, enhanced solar power infrastructure, and growing demands for electricity generation across developing nations. Countries like Brazil, Mexico, Chile, and Argentina are taking a lead in solar deployment through growing adoption of utility-scale and rooftop solar power systems. There is also a growing trend toward advanced mono-crystalline wafers, which provide better energy output and efficiency.

Market Growth Drivers: Rising Global Investments in Renewable Energy Infrastructure

The rise in focus worldwide on renewable energy sources is one of the key drivers of the Solar Silicon Wafer Market. Governments around the world have set themselves goals for achieving carbon neutrality and have been implementing various policies and programs that include financial incentives to promote solar power. Utility-scale solar projects, rooftop photovoltaics, and industrial applications of renewable energy are creating huge demand for efficient silicon wafers. The falling price levels of energy generated through solar power along with better conversion efficiency of solar power is further driving the adoption of solar energy. Furthermore, high demand for electricity due to increased applications in electric cars, smart cities, data centers, and industrial electrification projects is also contributing towards the steady growth of the market. The industry is witnessing considerable spending on the research and development of next-generation technologies, including N-type wafer, TOPCon, and heterojunction cells. Increased concerns about energy security along with the establishment of local solar ecosystem is expected to drive demand for solar silicon wafers globally between 2026 and 2035.

Market Restraints: High Manufacturing Costs and Supply Chain Volatility

Higher cost of manufacturing and higher variability of raw materials will continue to pose significant barriers to the growth of Solar Silicon Wafers Market. Polysilicon refinement, crystal growth, silicon ingot preparation, and slicing of wafers require high energy input, making the process expensive. Any changes in the prices of polysilicon, electricity, and transport will directly affect production costs and may have a significant influence on the stability of the market. Moreover, polysilicon, which is used by solar panel manufacturers, has a centralized production base around the world, thus making the sector prone to risks associated with geopolitics, trade embargoes, and export controls. Small companies operating in the industry can find it difficult to compete with large companies that integrate production facilities, thereby offering them the advantage of economies of scale and better automation. Besides, the need to develop thinner and more efficient wafers will also pose new challenges for the growth of the industry.

Market Opportunities: Expansion of Advanced Photovoltaic Technologies

The rapid advancements of innovative photovoltaic solutions are providing ample opportunities for growth in the Solar Silicon Wafer Market. There is an ever-growing requirement for efficient photovoltaics, which in turn is driving innovations in the wafer manufacturing sector, as well as leading to increased usage of advanced technology solutions like N-Type Monocrystalline, TOPCon Cells, heterojunction, and bifacial photovoltaics. Such products ensure superior performance, enhanced efficiency, reduced rate of degradation, and better tolerance to various conditions. Increased investment in large-scale energy projects and initiatives of Smart Grid Energy is generating a need for superior quality silicon wafers that can generate greater amounts of power. Moreover, innovations in wafer manufacturing include the creation of ultra-thin wafers, manufacturing larger wafers such as M10 and G12, and use of artificial intelligence in wafer manufacturing processes. Governments of various nations are also offering incentives in terms of subsidies and renewable energy initiatives to promote domestic production of solar panels and other equipment.

Recent Developments:

-

2026: LONGi Green Energy broke a world record in efficiency with its HIBC silicon-based solar cell with 28.13%, and in module efficiency certification with 26.4%. The innovation further helped solidify the company’s position as a leader in developing new monocrystalline wafers and PV technologies.

-

2026: Hongyuan Green Energy showcased ultra-thin 40 μm mono-silicon wafers that can be used in conventional solar panel production at its intelligent manufacturing factory in China. The engineering-grade wafers are compatible with all standard configurations for solar modules and were manufactured by the company through its in-house wafer slicing technology.

-

2026: Approval for Tata Power Renewable Energy to invest INR 6,500 crore in the setting up of 10 GW solar PV ingot and wafer manufacturing capacity in India was made to improve the domestic manufacturing industry, create supply chain robustness, and reduce dependence on upstream PV component imports.

Solar Silicon Wafer Companies are:

-

LONGi Green Energy Technology Co., Ltd.

-

TCL Zhonghuan Renewable Energy Technology Co., Ltd.

-

GCL-Poly Energy Holdings Limited

-

Trina Solar Limited

-

JinkoSolar Holding Co., Ltd.

-

Canadian Solar Inc.

-

SUMCO Corporation

-

NexWafe GmbH

-

Daqo New Energy Corp.

-

OCI Company Ltd.

-

Wacker Chemie AG

-

REC Silicon ASA

-

Tongwei Co., Ltd.

-

Risen Energy Co., Ltd.

-

Meyer Burger Technology AG

-

Green Energy Technology Inc.

-

Targray Technology International

-

First Solar, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.41 Billion |

| Market Size by 2035 | USD 44.17 Billion |

| CAGR | CAGR of 10.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Monocrystalline Wafer, Polycrystalline Wafer) • By Application (PV Modules, Inverter, Solar Cell, Solar Racking System, Solar Battery) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | LONGi Green Energy Technology Co., Ltd., TCL Zhonghuan Renewable Energy Technology Co., Ltd., GCL-Poly Energy Holdings Limited, JA Solar Technology Co., Ltd., Trina Solar Limited, JinkoSolar Holding Co., Ltd., Canadian Solar Inc., SUMCO Corporation, Wafer Works Corporation, NexWafe GmbH, Daqo New Energy Corp., OCI Company Ltd., Wacker Chemie AG, REC Silicon ASA, Tongwei Co., Ltd., Risen Energy Co., Ltd., Meyer Burger Technology AG, Green Energy Technology Inc., Targray Technology International, First Solar, Inc. |

Frequently Asked Questions

The Solar Silicon Wafer Market is expected to grow at a CAGR of 10.59% during 2026-2035.

Solar Silicon Wafer Market size was USD 16.41 Billion in 2025 and is expected to Reach USD 44.17 Billion by 2035.

The major growth factor of the Solar Silicon Wafer market is the increasing global adoption of solar energy, driven by technological advancements, and supportive government policies.

The Monocrystalline Wafer segment dominated the Solar Silicon Wafer market in 2025.

Asia Pacific dominated the Solar Silicon Wafer Market in 2025.

Get in Touch