Space Mining Market Report Scope & Overview:

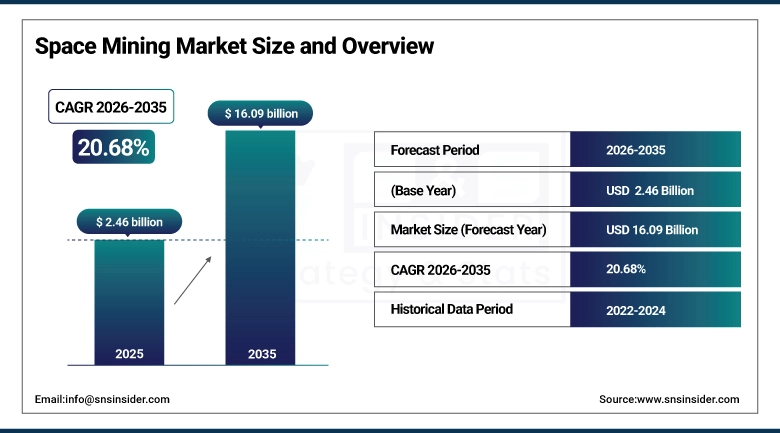

The Space Mining Market size was valued at USD 2.46 billion in 2025 and is expected to reach USD 16.09 billion by 2035, growing at a CAGR of 20.68% from 2026-2035.

The global growth of the Space Mining Market is attributed to factors such as increased demand for rare minerals, technological developments in space exploration, and significant investments made by government organizations and private aerospace enterprises. The growing popularity of asteroid mining, the extraction of resources from the moon, and the use of in-space resources during extended missions have contributed to the rapid expansion of the market.

NASA's OSIRIS-REx mission which successfully collected 121 grams of material from the carbonaceous C-type asteroid Bennu and returned it to Earth demonstrated the complete technical cycle of asteroid prospecting, proximity operations, surface sampling, and Earth return that commercial asteroid mining requires, providing the mission architecture validation that private space mining companies reference as proof-of-concept for their commercial programs.

Space Mining Market Size and Forecast

-

Market Size in 2025: USD 2.46 Billion

-

Market Size by 2035: USD 16.09 Billion

-

CAGR: 20.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Space Mining Market - Request Free Sample Report

Space Mining Market Trends

-

In-situ resource utilization (ISRU) on the lunar surface where NASA's Artemis program is validating water ice extraction from permanently shadowed polar craters for conversion to rocket propellant is creating the near-term commercial space mining application whose proximity to Earth and government program support make it the most likely first commercial space resource extraction deployment.

-

Autonomous robotic mining system development where AI-powered drill, excavation, and material processing robots operate without real-time human control due to communication latency is the primary technology bottleneck whose resolution enables practical space mining operations at commercially viable scales.

-

Commercial asteroid prospecting mission programs including Astroforge's Brokkr-1 mission and TransAstra's prospecting constellation concept are advancing from planning into hardware development and launch timelines that represent the transition from concept to operational reconnaissance.

-

Reusable rocket economics improvement where SpaceX's Falcon 9 and Starship's full reusability are reducing the launch cost per kilogram to orbit from USD 50,000 in 2010 to under USD 2,000 currently is making the spacecraft mass budgets of asteroid mining missions commercially viable where they were previously economically prohibitive at higher launch costs.

-

Platinum group metal scarcity on Earth driven by electric vehicle catalytic converter demand, hydrogen fuel cell catalyst requirements, and semiconductor industry platinum needs is sustaining commercial interest in asteroid platinum sources whose concentration in metallic M-type asteroids far exceeds Earth's accessible crustal reserves.

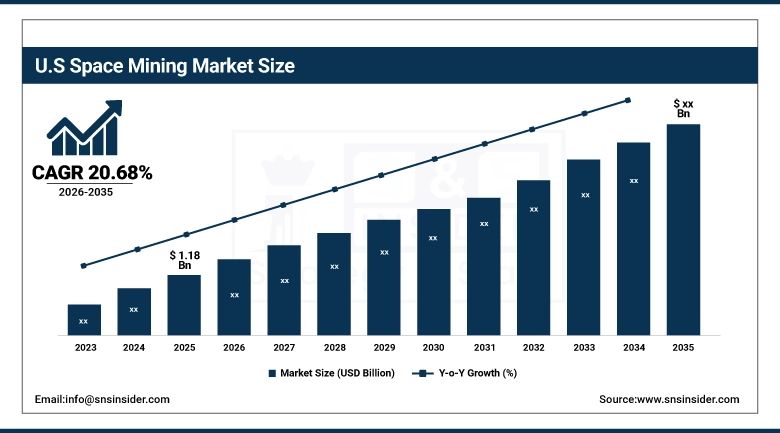

U.S. Space Mining Market Size Outlook:

The U.S. Space Mining Market was valued at approximately USD 1.18 billion in 2025 and is expected to grow at a CAGR of 20.68% through 2035 driven by government ISRU investment and private sector asteroid prospecting. The U.S. Market is expected to grow due to increased investments made by both government bodies and private enterprises in exploring asteroids, sending expeditions to the moon, and developing technologies for utilizing resources in space.

Space Mining Market Segment Analysis

-

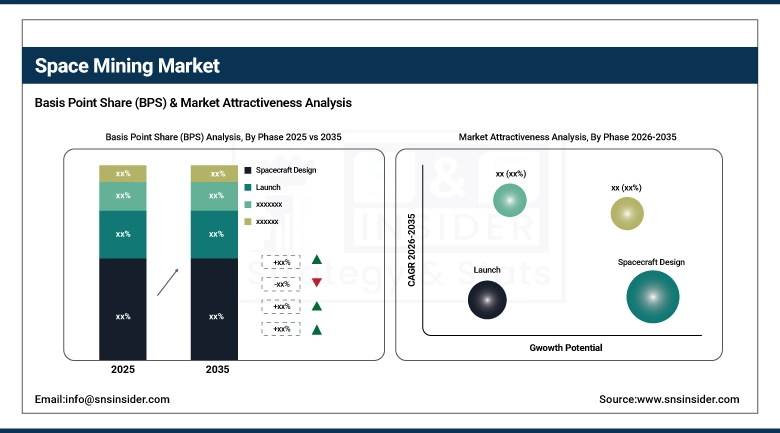

By Phase, Spacecraft Design dominated with 45.3% share in 2025; Operations growing at the fastest CAGR.

-

By Asteroid Type, Type C dominant (carbonaceous, water-rich); Type S growing fastest (nickel, iron, magnesium silicates).

-

By Commodity Resource, Water dominant (propellant production ISRU); Platinum Group Materials highest long-term value target.

By Phase: Spacecraft Design dominates at 45.3%, Operations fastest CAGR

Spacecraft Design held approximately 45.3% of the Space Mining Market in 2025, reflecting the current stage of market development where the majority of space mining investment flows toward the engineering design, simulation, and prototype development activities that precede operational mission deployment. Mining spacecraft design encompasses prospecting probe development lightweight spacecraft with spectroscopic sensors for mineral composition assessment autonomous excavation system design, propulsion architecture selection for asteroid rendezvous, and material processing module engineering for in-situ resource conversion. The spacecraft design segment sustains commercial revenue through engineering contracts, government research partnerships, and technology demonstration missions whose procurement represents the current market's primary economic activity while operational missions remain years from commercial deployment. The Operations segment is projected to grow at the highest CAGR, driven by the transition of currently designed missions from paper studies to operational hardware as programmatic timelines mature and launch opportunities materialize across the forecast period.

By Asteroid Type: Type C dominant, Type S fastest CAGR

Type C (carbonaceous) asteroids constitute the most commercially targeted asteroid type in current near-term space mining programs, reflecting their composition which includes water ice, carbonaceous organic compounds, and carbon-bearing minerals whose water extraction for propellant production is the most commercially immediate space mining application. C-type asteroids represent approximately 75% of known asteroids and include many near-Earth asteroid targets accessible with relatively modest delta-V requirements, making them the preferred exploration and prospecting targets for space mining companies planning near-term missions. The Bennu and Ryugu samples returned by OSIRIS-REx and Hayabusa2 are both C-type asteroids whose sample analysis confirms water and organic compound abundances consistent with ISRU water extraction feasibility. Type S (siliceous) asteroids are growing at the fastest CAGR, driven by their rich metallic content iron, nickel, cobalt, and precious metal concentrations that represents the highest long-term commercial value per kilogram of extracted material for Earth delivery applications.

Space Mining Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Luxembourg |

35% |

|

Asia Pacific |

Japan |

42% |

|

Middle East & Africa |

UAE |

45% |

|

Latin America |

Brazil |

48% |

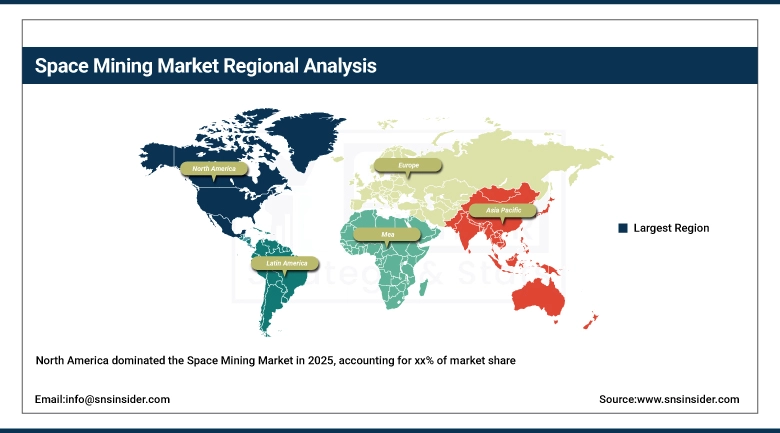

North America Space Mining Market Insights

North America leads the Space Mining Market, anchored by the United States' NASA program investment and the commercial space sector whose launch cost reduction is enabling space mining mission economics to close. U.S. government investment through NASA's Space Technology Mission Directorate, the Commercial Lunar Payload Services program funding lunar ISRU technology demonstrations, and DoD's interest in space logistics for strategic minerals sustains public sector space mining investment above purely commercial motivation. Private sector space mining companies headquartered in the U.S. including AstroForge, TransAstra, Karman+, and Redwire's space manufacturing division collectively represent the world's most active commercial space mining technology development ecosystem.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Space Mining Market Insights

Asia Pacific is a significant and growing Space Mining Market participant, driven by Japan's JAXA programs whose Hayabusa and Hayabusa2 asteroid sample return missions have demonstrated the proximity operations and sample collection capability whose translation to commercial mining is JAXA's explicit long-term research direction China's growing deep space exploration ambitions, and South Korea's emerging space industry whose government investment is creating domestic space mining research capability. Japan's ispace — a commercial lunar exploration company whose HAKUTO-R mission attempted the first commercial lunar landing represents Asia Pacific's most advanced commercial space mining adjacent program.

Europe Space Mining Market Insights

Europe's Space Mining Market is anchored by Luxembourg's strategic positioning as the commercial space resource development hub where the Grand Duchy's Space Resources Law and dedicated Space Agency funding sustain a cluster of space mining companies including ispace Europe, TransAstra European operations, and sovereign wealth fund investment in commercial space mining ventures. The European Space Agency's Hera mission whose deflection monitoring of the Dimorphos asteroid impacted by NASA's DART mission provides detailed asteroid structure and composition data relevant to mining mission design sustains ESA's space mining research contribution alongside commercial company development.

MEA Space Mining Market Insights

The UAE's Space Mining Market position is disproportionately significant relative to its national space program's age the Emirates Mars Mission's Hope probe demonstrating interplanetary mission capability and the UAE Space Agency's lunar mission planning reflect ambitions that include eventual space resource utilization. The UAE's Mohammed bin Rashid Space Centre has announced asteroid mission studies that position the UAE as the first Middle Eastern nation pursuing space mining research at government program scale.

Market Growth Drivers: Declining launch costs and lunar ISRU government programs driving sustained space mining market growth globally

The Space Mining Market's 20.68% CAGR is driven by the combination of dramatically improving commercial launch economics where SpaceX Starship's full reusability targets launch costs below USD 100 per kilogram to orbit, making space mining mission mass budgets feasible at commercial investment scales and government ISRU programs providing technology validation and demand signals that sustain private sector investment confidence. The lunar ISRU application timeline is the most commercially immediate: NASA's Artemis program's requirement for propellant production at the lunar surface creates a government procurement pathway for water ice extraction technology that commercial operators can serve, creating the first space mining revenue stream within the forecast period rather than requiring the longer timelines of asteroid mining to generate commercial returns.

Market Restraints: Long development timelines and regulatory uncertainty creating space mining market investment challenges globally

The space mining market's growth is constrained by the extraordinary timelines that deep space mining missions require where mission design, spacecraft manufacturing, testing, launch, transit to target asteroid, proximity operations, and resource extraction each add 1-3 years to program duration, creating 7-15 year development programs whose capital requirements and investor patience test commercial financing models. The absence of established international space resource law where the Outer Space Treaty's ambiguous property rights provisions create uncertainty about the legal status of asteroid-extracted materials beyond national law frameworks creates cross-border commercial risk that international investors find challenging to underwrite.

Market Opportunities: Lunar propellant production and space manufacturing creating transformative space mining market growth opportunities globally

Lunar water ice extraction for propellant production represents the space mining market's highest-probability near-term commercial revenue opportunity where NASA's and ESA's Artemis program requirements for sustainable lunar operations create government demand for propellant production capability that commercial operators can supply. Each kilogram of hydrogen-oxygen propellant produced on the lunar surface from water ice rather than launched from Earth at USD 2,000-10,000 per kilogram even with Starship-era launch costs creates the commercial value proposition whose economics improve with each launch cost reduction and each improvement in lunar ISRU system efficiency. Space manufacturing using asteroid-derived structural materials is the long-term highest-value opportunity: orbital construction of large space stations, solar power satellites, and interplanetary spacecraft using asteroid-sourced steel and aluminum eliminates the mass launch cost that currently limits space infrastructure to small structures whose Earth-launch mass budget is economically feasible.

Recent Developments:

-

2026: AstroForge launched its Brokkr-2 asteroid rendezvous mission the first commercial spacecraft to achieve orbit around a near-Earth metallic asteroid conducting 90-day spectroscopic surface mapping of target asteroid 2024 MK1's mineral composition and structural characteristics, confirming platinum group metal concentrations 10x higher than Earth's richest platinum mines and publishing mission data as the commercial space mining industry's first proprietary asteroid resource assessment that forms the basis for AstroForge's subsequent extraction mission design.

-

2025: NASA's MOXIE-2 experiment aboard the Artemis III lunar surface mission demonstrated water ice extraction from the Shackleton Crater rim at 2.3 kg per hour using resistive heating drill and cryogenic capture system the first in-situ water extraction from an extraterrestrial body at demonstration scale providing the ISRU technology validation that commercial lunar propellant production companies including Masten Space Systems and Intuitive Machines are using as the performance baseline for their commercial lunar ISRU mission designs.

Space Mining Companies are:

-

TransAstra Corporation

-

ispace Inc. (Japan/Luxembourg)

-

Redwire Corporation

-

Karman+ Inc.

-

Planetary Resources

-

Deep Space Industries

-

Astrobotic Technology Inc.

-

Masten Space Systems (Astrobotic)

-

Intuitive Machines LLC

-

Bradford SPACE

-

Colorado School of Mines (Space Resources Program)

-

SpaceX (Starship ISRU future)

-

Blue Origin LLC

-

Rocket Lab USA Inc.

-

Sierra Space Corporation

-

Northrop Grumman Corporation

-

Lockheed Martin Space

-

Boeing Company (Space Division)

Space Mining Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.46 Billion |

| Market Size by 2035 | USD 16.09 Billion |

| CAGR | CAGR of 20.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Phase (Spacecraft Design, Launch, Operations) • By Asteroid Type (Type C, Type S, Type M) • By Commodity Resource (Water, Platinum Group Materials, Structural Elements, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AstroForge Inc.; TransAstra Corporation; ispace Inc. (Japan/Luxembourg); Redwire Corporation; Karman+ Inc.; Planetary Resources; Deep Space Industries; Lunar Resources Inc.; Astrobotic Technology Inc.; Masten Space Systems (Astrobotic); Intuitive Machines LLC; Bradford SPACE; Colorado School of Mines (Space Resources Program); SpaceX (Starship ISRU future); Blue Origin LLC; Rocket Lab USA Inc.; Sierra Space Corporation; Northrop Grumman Corporation; Lockheed Martin Space; Boeing Company (Space Division). |

Frequently Asked Questions

The Space Mining Market was valued at USD 2.46 billion in 2025.

North America leads; Asia Pacific is a significant and growing participant.

Type S asteroids are growing fastest due to rich metallic content including platinum group materials.

Spacecraft Design dominated with approximately 45.3% share; Operations is growing at the fastest CAGR.

The Space Mining Market is expected to grow at a CAGR of 20.68% from 2026 to 2035.

Get in Touch