Selective Laser Sintering Equipment Market Report Scope & Overview:

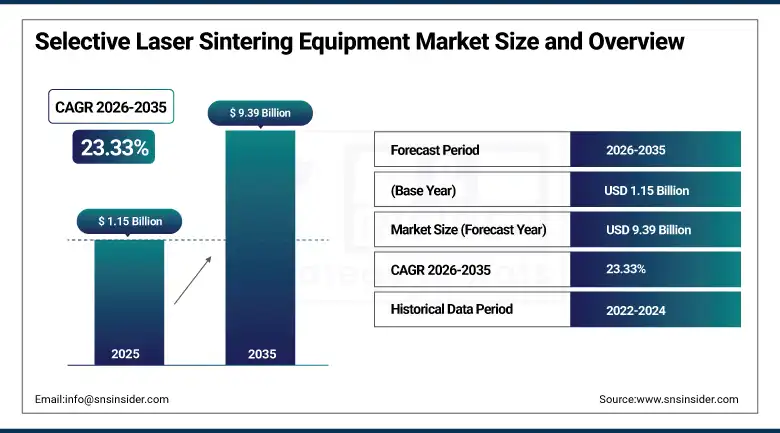

The Selective Laser Sintering Equipment Market Size was valued at USD 1.15 Billion in 2025 and is expected to reach USD 9.39 Billion by 2035, growing at a CAGR of 23.33% from 2026–2035.

The global market for selective laser sintering machines is developing quickly owing to stiff competition amongst major players in terms of innovative capabilities and advanced solutions in manufacturing. Companies are implementing digital manufacturing technology and smart manufacturing technology to improve their manufacturing processes. Examples of improved capabilities are AI-assisted process optimization and process monitoring through the use of IoT. The advancements made in manufacturing processes include improvement in material compatibility, enhanced speed of printing, and increased precision. There has been an emphasis on sustainability in form of green materials and reduced energy consumption and waste generation. Due to changes in environmental standards, companies are now under pressure to develop recycling or biodegradable powder materials.

In November 2024, 3D Systems introduced advanced printers, post-processing solutions, and new materials at Formnext 2024, enhancing efficiency and innovation across its additive manufacturing portfolio. The launch reflected 3D Systems’ strategy of expanding its end-to-end SLS ecosystem, combining hardware, software, and materials innovation to address growing enterprise demand for production-grade additive manufacturing capability across aerospace, healthcare, and automotive applications requiring complex, high-precision component geometries.

Market Size and Forecast

-

Market Size in 2026E: USD 1425.5 Million

-

Market Size by 2035: USD 9398.6 Million

-

CAGR: 23.33% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Selective Laser Sintering Equipment Market - Request Free Sample Report

Selective Laser Sintering Equipment Market Trends

-

AI-driven process optimization and IoT-enabled monitoring are advancing production efficiency across industrial SLS equipment.

-

Recyclable and biodegradable powder material development is accelerating amid tightening environmental sustainability requirements.

-

Desktop SLS printer pricing reductions are expanding adoption among small businesses and research institutions.

-

Biocompatible material innovation is enabling growing SLS adoption for personalised implants and dental prosthetics.

-

Fiber and diode laser technology improvements are increasing solid-state laser adoption for precision applications.

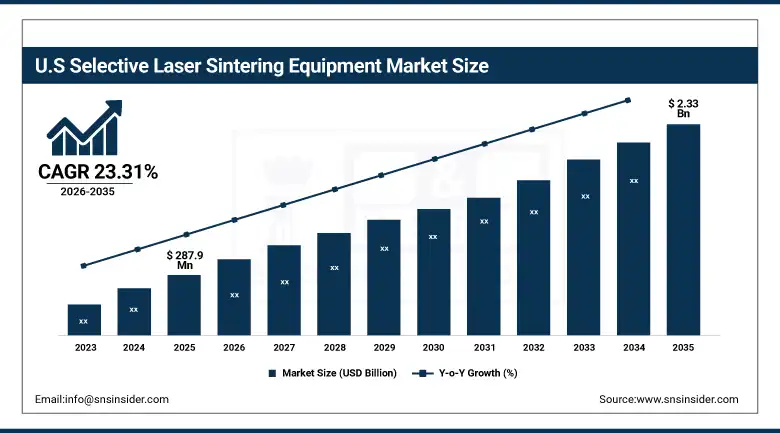

The U.S. Selective Laser Sintering Equipment Market Outlook

The U.S. Selective Laser Sintering Equipment Market was valued at approximately USD 287.9 Million in 2025 and is expected to reach approximately USD 2.33 Billion by 2035, growing at a CAGR of approximately 23.31%.

Demand for advanced additive manufacturing, especially in industries such as aerospace, automotive, healthcare, and consumer goods, is propelling growth of the SLS equipment market in the United States. This is leading to rapid adoption enabled by advances in digital manufacturing, materials innovation, and low-cost production. General Motors and Boeing utilize SLS technology to manufacture lightweight, high-performance components for vehicles and aircraft, sustaining strong domestic procurement across the country’s mature manufacturing ecosystem.

The Mayo Clinic uses 3D printed surgical guides produced through SLS technology to increase the efficiency of medical procedures, with many other U.S. hospitals producing customized implants and prosthetics using equivalent equipment. This growing healthcare adoption reflects the broader American medical industry’s shift toward personalized, patient-specific surgical planning tools that SLS-printed anatomical models and guides enable at a precision level conventional manufacturing methods cannot economically achieve.

Selective Laser Sintering Equipment Market Segment Analysis

-

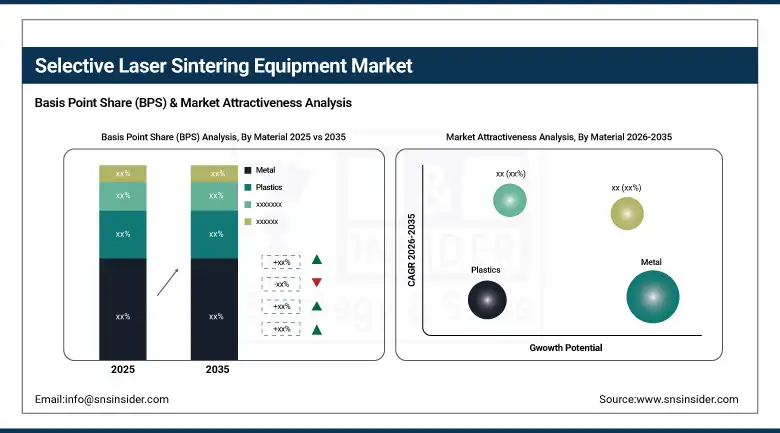

By Material, metal segment dominated the selective laser sintering equipment market with approximately 43.6% share in 2025, while the plastics segment is the fastest growing.

-

By Laser Type, the gas laser segment dominated the selective laser sintering equipment market with approximately 62.2% share in 2025, while the solid laser segment is the fastest growing.

-

By Technology, the industrial printer segment dominated the selective laser sintering equipment market, while the desktop printer segment is the fastest growing driven by declining pricing and SME adoption.

-

By End-Use, the automotive segment dominated the selective laser sintering equipment market with approximately 24.6% share in 2025, while the healthcare segment is the fastest growing end use.

By Material, metal dominates, plastics grow fastest

Metal accounted for approximately 43.6% share of the selective laser sintering equipment market in 2025, owing to its widespread use across aerospace, automotive, and healthcare applications. Metal SLS is often the go-to technology for high-strength, lightweight, and durable components, making it essential in industries that demand precision and performance. High demand for metal 3D printing in tooling, spare parts, and structural components has further reinforced its dominant market position. Aerospace manufacturers’ growing reliance on metal SLS for producing complex, weight-optimized structural components and automotive OEMs’ increasing adoption for tooling and prototyping collectively sustain metal’s commercial leadership across the broadest range of high-value industrial applications within the SLS equipment landscape.

Plastics is expected to experience the fastest CAGR from 2026 to 2035, due to expanding volume in prototyping, consumer goods, and medical applications. Demand is currently driven by the development of new polymer materials that are increasingly affordable and easier to process. The growing application of biocompatible plastics in dental prosthetics and medical implants presents a major growth opportunity for the plastic SLS segment, as healthcare providers seek patient-specific devices manufactured at lower cost and faster turnaround than traditional metal alternatives, expanding the addressable market for plastic-based additive manufacturing equipment.

By Technology, industrial printers dominate, desktop printers grow fastest

Industrial printers accounted for the largest technology share of the SLS equipment market in 2025, with approximately 73.2% share, largely owing to the high precision and scalability offered by industrial SLS printers along with adoption of SLS technology in large-scale manufacturing. Commonly used across automotive, aerospace, and healthcare industries, these printers are capable of producing highly complex thermal-process components with superior mechanical properties. They have established themselves as market leaders through their capability to handle a wide spectrum of materials, from metals to high-performance polymers, with manufacturers including 3D Systems, EOS, and Farsoon Technologies sustaining industrial printer leadership through continuous large-format machine innovation targeting enterprise-scale production volumes.

Desktop SLS printers are projected to register the highest CAGR from 2026 to 2035, due to growing requirements for economical and smaller-sized 3D printers. Adoption is accelerating among small businesses, research institutions, and prototyping applications, with increasing material compatibility and improved user interfaces making desktop SLS printers more accessible across a wider range of applications including education, medical modelling, and customised manufacturing tools. Formlabs’ Fuse 1 and Sinterit’s Lisa Pro exemplify the growing desktop printer category whose declining price point is expanding the addressable customer base beyond traditional industrial manufacturers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

46.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Selective Laser Sintering Equipment Market Insights

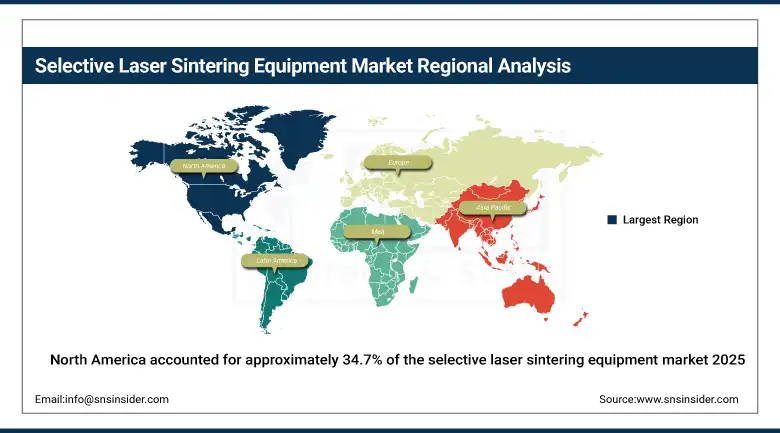

North America accounted for approximately 34.7% of the selective laser sintering equipment market in 2025, owing to adoption across various industrial sectors, mature manufacturing environment, and high research and development investment. Large players including 3D Systems, Stratasys, and Formlabs are contributing substantially to regional leadership through innovation in aerospace, healthcare, and automotive applications.

The United States accounts for approximately 82.5% of North American revenues, with General Motors and Boeing using SLS technology to manufacture lightweight, high-performance parts for cars and airplanes. North America is making strides to adopt SLS in healthcare, with the Mayo Clinic using 3D printed surgical guides and many other hospitals producing customized implants and prosthetics using SLS equipment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Selective Laser Sintering Equipment Market Insights

Europe is a significant SLS equipment market where EOS GmbH’s industrial printer leadership and strong aerospace and automotive manufacturing base sustain consistent demand. Germany accounts for approximately 24.6% of European revenues through its world-leading industrial manufacturing sector and advanced materials research infrastructure.

The United Kingdom’s aerospace manufacturing sector, France’s growing healthcare 3D printing adoption, and Switzerland’s Sintratec-driven desktop printer innovation collectively sustain European market development. European environmental sustainability regulation is accelerating manufacturer investment in recyclable and biodegradable powder material development across the region.

Asia Pacific Selective Laser Sintering Equipment Market Insights

Asia Pacific is projected to grow at the highest CAGR from 2026 to 2035, driven by increasing industrialization, growing demand for additive manufacturing, and government support for 3D printing technologies. Advanced manufacturing is attracting significant investment in China, Japan, South Korea, and elsewhere, with Chinese automotive firms including NIO and BYD already utilizing SLS for electric vehicle part production.

China accounts for approximately 46.8% of Asia Pacific revenues through Farsoon Technologies’ industrial-grade SLS solutions and growing domestic automotive sector adoption. India’s wide-scale adoption of 3D-printed medical implants amid an emerging healthcare sector and increasing affordability of SLS systems within small and medium enterprises further sustain the region’s rapid growth trajectory.

MEA & Latin America Selective Laser Sintering Equipment Market Insights

The UAE leads MEA revenues through its growing advanced manufacturing initiatives and government-backed industrial diversification programmes promoting additive manufacturing adoption. Saudi Arabia’s Vision 2030 industrial development strategy creates growing institutional SLS equipment demand.

Brazil leads Latin American revenues through its growing automotive and aerospace manufacturing sectors’ additive manufacturing adoption. Mexico’s expanding automotive manufacturing sector serving the North American market and Argentina’s growing industrial technology sector create additional regional SLS equipment procurement growth.

Market Dynamics

Growth Drivers: Revolutionizing manufacturing with SLS technology across automotive, aerospace, and healthcare applications

The growth of the selective laser sintering systems market is being driven by the increasing need for manufacturing technologies in the automotive, aerospace & defense, healthcare, and electronics industry. The increasing acceptance of the SLS technique due to the unique features like manufacturing of precise and complex geometries of components without any wastage of material and higher mechanical properties will be an important factor driving the market growth. The increasing trend of lightweight materials especially in automotive and aerospace where designers want to use components that have lighter weight but the same strength will further drive the market.

Industry 4.0 and smart manufacturing will contribute to the growth of the market through their increasing importance since manufacturers are concerned with incorporating the manufacturing process through additive manufacturing for greater efficiency and cost optimization. Using artificial intelligence-based process optimization and process monitoring based on the Internet of Things are allowing manufacturers to ensure consistency in the manufacture of components and minimizing material wastage and energy expenditure.

Restraints: Limited material options and complex post-processing challenges impacting SLS adoption in high-speed industries

A key challenge among the users of SLS machines is the restricted number of available materials. Even though there have been several improvements in this aspect, the scope of materials available in SLS technology still lags behind other AM techniques. In addition, the slow pace at which new materials can be discovered for certain applications is an obstacle for the growing industries which need specific materials to satisfy their needs. Another significant problem with SLS technology is the post-processing of printed parts, which necessitates cleaning, sintering, and surface treatment.

The need for this step adds more time and labor to the production process, which may affect efficiency in industries where the production pace is rather fast. Regulations and the necessity for extensive testing in some industries such as healthcare and aviation, where performance and safety should meet particular criteria, can also serve as a barrier to implementation. The lack of specialized workers to run SLS machines and other types of AM technologies becomes an increasing problem for organizations.

Opportunities: Expanding SLS opportunities in healthcare and electronics through biocompatible materials and affordable desktop printers

The lucrative opportunities that exist due to growth in the healthcare sector can be attributed to the rapid changes in the use of SLS in terms of customized implants, prosthetics, and dental products. With the development of more biocompatible materials coupled with increasing approvals from regulations bodies, SLS is expected to continue gaining momentum in application within the healthcare sector. There is also great potential in the application of SLS technology in the electronics sector where manufacturers seek to obtain highly precise parts, such as heat sinks and housings, which are difficult to make using conventional manufacturing techniques.

In addition to being used by large companies due to their investment in material development, SLS technology is expected to see more applications among small-scale firms and research institutions due to the falling prices of desktop SLS printers.

Recent Developments:

-

2024: 3D Systems introduced advanced printers, post-processing solutions, and new materials at Formnext 2024, enhancing efficiency and innovation across its additive manufacturing portfolio for industrial-scale production applications.

-

2024: EOS launched the P3 NEXT, enhancing productivity and reducing costs for industrial-scale polymer 3D printing, strengthening its position in the high-volume industrial printer segment.

-

2023: Farsoon Technologies expanded its FS271M industrial SLS printer production capacity to meet growing demand from Chinese automotive manufacturers adopting additive manufacturing for electric vehicle component production.

Selective Laser Sintering Equipment Market Key Players are:

-

3D Systems Inc.

-

EOS GmbH

-

Farsoon Technologies

-

Prodways Group

-

Formlabs Inc.

-

Ricoh Company Ltd.

-

Sinterit Sp. z o.o.

-

Sintratec AG

-

Sharebot SRL

-

Red Rock SLS

-

Natural Robotics

-

Z Rapid Tech

-

Aerosint

-

Aspect Inc.

-

Jenoptik AG

-

Stratasys Ltd.

-

Renishaw plc

-

TRUMPF SE + Co. KG

-

DMG MORI Co. Ltd.

-

SLM Solutions Group AG

Selective Laser Sintering Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.15 Billion |

| Market Size by 2035 | USD 9.39 Billion |

| CAGR | CAGR of 23.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Metal, Plastics, Nylon) • By Laser Type (Solid Laser, Gas Laser) • By Technology (Desktop Printer, Industrial Printer) • By End-Use (Automotive, Aerospace & Defense, Healthcare, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3D Systems Inc., EOS GmbH, Farsoon Technologies, Prodways Group, Formlabs Inc., Ricoh Company Ltd., Sinterit Sp. z o.o., Sintratec AG, Sharebot SRL, Red Rock SLS, Natural Robotics, Z Rapid Tech, Aerosint, Aspect Inc., Jenoptik AG, Stratasys Ltd., Renishaw plc, TRUMPF SE + Co. KG, DMG MORI Co. Ltd., and SLM Solutions Group AG |

Frequently Asked Questions

The Selective Laser Sintering Equipment Market is expected to grow at a CAGR of 23.33% from 2026 to 2035.

The Selective Laser Sintering Equipment Market was valued at USD 1.15 Billion in 2025.

Rising demand for advanced manufacturing technologies in automotive, aerospace, and healthcare, growing adoption of Industry 4.0 smart manufacturing, and expanding biocompatible material innovation are the primary growth factors.

The Metal segment dominated the Selective Laser Sintering Equipment Market with approximately 43.6% share in 2025.

North America dominated the Selective Laser Sintering Equipment Market with approximately 34.7% revenue share in 2025.

Get in Touch