Spray Adhesives Market Report Scope & Overview:

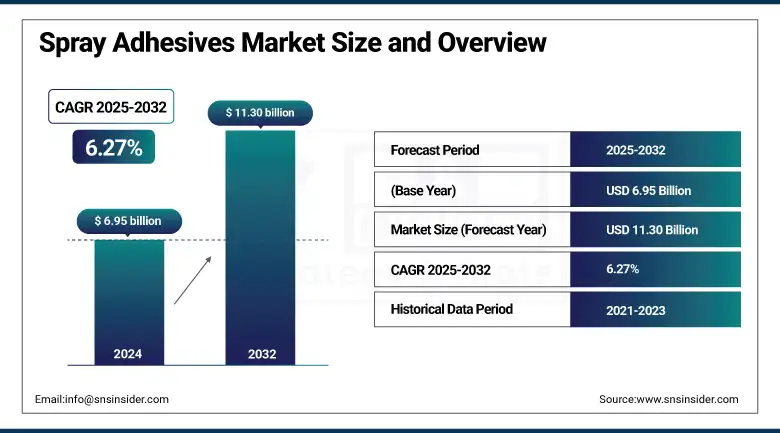

The Spray Adhesives Market Size was valued at USD 6.95 billion in 2024 and is expected to reach USD 11.30 billion by 2032 and grow at a CAGR of 6.27% over the forecast period 2025-2032.

Global Spray Adhesives Market Analysis reveals an increase in the usage due to the automotive and transportation sectors. As more and more vehicle makers use lightweight materials to meet the pressure of fuel efficiency and emission requirements, more and more makers and OEMs are adding dry inside and outside the car interior, especially the insulation walls, headliners, seats, and door panels, and more and more spray adhesives are becoming an integral part. Their ability to be applied with relative ease, quick molecular function at room temperature, and compatibility with different substrates are well-suited for high-speed production lines. Moreover, increasing adoption of spray adhesives in automotive production is attributed to the increasing interest in electric vehicles (EVs), which require noise-dampening and thermal insulation materials. This is likely to shift further as automotive manufacturers adopt new manufacturing processes and sustainable adhesive solutions, which drive the spray adhesives market growth.

To Get more information On Spray Adhesives Market - Request Free Sample Report

By the end of 2023, a U.S. government program, known as the National Electric Vehicle Infrastructure (NEVI) program, aims to invest around USD 2.5 billion in the development of US-wide EV charging stations along key highway corridors. These investments enable the adoption of EVs and, indirectly, increase demand for interior adhesive technology as automakers ramp up manufacturing.

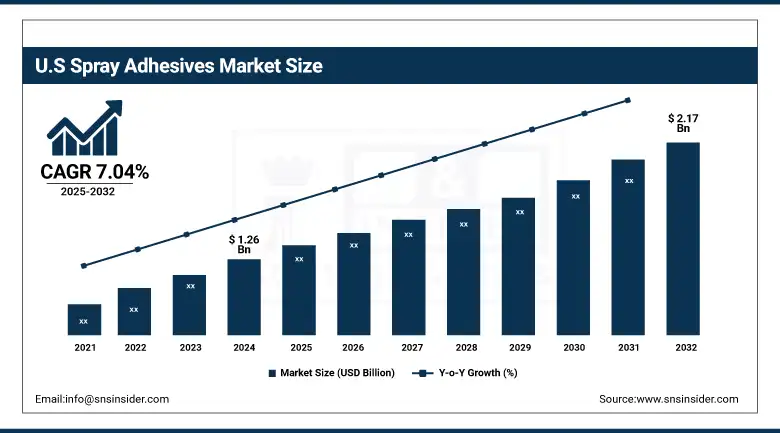

The U.S Spray Adhesives market size was USD 1.26 billion in 2024 and is expected to reach USD 2.17 billion by 2032 and grow at a CAGR of 7.04% over the forecast period of 2025-2032. It due to a strong do-it-yourself (DIY) culture, large-scale residential and commercial renovation trends, and a steady demand from the automotive upholstery and construction sectors. Government policies promoting energy-efficient construction practices have indirectly fueled the use of high-quality adhesive solutions in roofing, insulation, and HVAC installations.

Market Dynamics

Key Drivers:

-

Rising Adoption in Construction and Furniture Industries Drives the Market Growth

In construction, spray adhesives are used for flooring, panels, drywall, and insulation, offering fast curing and clean application. In furniture, they bond foams, fabrics, and wood veneers efficiently. Demand for modular construction and custom furniture is growing due to rapid urbanization and evolving consumer lifestyles. The increase in residential and commercial renovation activities further fuels adhesive consumption.

Instance: U.S. residential construction spending reached $917.9 billion in 2024, up 5.9% from 2023 (Census Bureau), supporting growth in building materials, including adhesives.

Restrain:

-

Health and Environmental Regulations on VOC Emissions, which may hamper the Market Growth

Solvent-based spray adhesives release volatile organic compounds (VOCs), which are harmful to human health and the environment. Regulations by the Environmental Protection Agency (EPA) and other global bodies restrict VOC emissions, increasing compliance costs for manufacturers. Transitioning to low-VOC or water-based alternatives requires investment in R&D and may face performance trade-offs, especially in heavy-duty applications.

Opportunities:

-

Rising Demand from Emerging Markets and E-Commerce Boom Creates an Opportunity for the Market

Emerging economies in the Asia-Pacific and Latin America are witnessing rapid industrialization, infrastructure development, and consumer goods production. Additionally, the e-commerce boom is increasing the demand for protective packaging and assembly adhesives. Growth in these regions offers untapped potential for manufacturers to localize production and expand distribution channels, which drive the spray adhesives market trends.

Instance: Henkel opened an Innovation Center in Shanghai in 2024 to develop custom adhesive solutions for Asia-Pacific markets, supporting regional demand across construction and electronics industries.the

Segment Analysis:

By Type

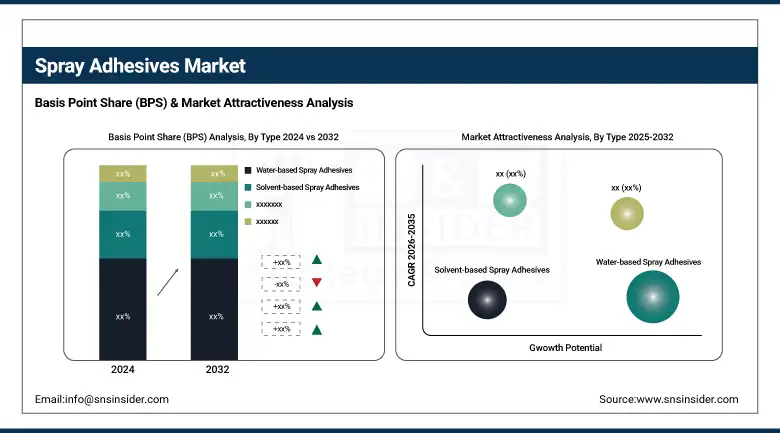

Water-based spray Adhesives dominate the segment with an estimated 42% market share in 2024. Their demand is driven by increasing regulations on VOC emissions, especially in North America and Europe. These adhesives are widely used in furniture, packaging, and DIY applications due to their safer formulation, lower Odor, and easier cleanup. Their eco-friendly nature is appealing to manufacturers aiming to meet green certification standards.

Hot Melt Spray Adhesives are the fastest-growing sub-segment. Their demand is rising in the automotive, textile, and electronics sectors, primarily due to their fast bonding speed and minimal drying time. They also allow clean, mess-free applications and support high-speed manufacturing processes, making them increasingly popular in industrial automation environments.

By Chemistry

Acrylic-Based Spray Adhesives held the dominant market share of around 34% in 2024. These are favored for their excellent resistance to UV, aging, and moisture, making them ideal for outdoor applications and construction projects. Their versatility across substrates like plastics, fabrics, and metals has led to widespread adoption in signage, insulation panels, and decorative laminates.

Polyurethane-Based Spray Adhesives are the fastest-growing in this category. Known for superior elasticity and chemical resistance, they are in high demand for structural bonding in automotive and aerospace applications. Their strong adhesion to varied materials and compatibility with high-temperature conditions enhance their value in demanding industrial use cases..

By Application

In 2024, commercial roofing held the largest share of the Spray Adhesives market, comprising 48% of the global market. This is largely attributed to the common use of anchors in office buildings, hospitals, retail centers, or schools, where workers must often access a rooftop to service an HVAC unit, sign, or other equipment. These are frequently required to have OSHA-compliant fall protection for the life and safety compliance needs of the building. In addition, there's a surge of retrofitting commercial property rooftops with solar panels and energy systems that are adding to the demand for certified rooftop anchors.

By Application

Furniture & Upholstery applications lead the market with approximately 30% share in 2024. Spray adhesives are commonly used to bond foam, fabric, and wooden materials efficiently, which speeds up mass production. Rising demand for customized and modular furniture particularly in urban housing, has increased consumption in this sector.

Automotive & Transportation is witnessing the fastest growth. The segment is benefiting from increased automobile production, greater focus on vehicle interior comfort, and the shift from mechanical to adhesive bonding to reduce weight. Spray adhesives are used in headliners, carpets, sound insulation, and seating areas, where strong and flexible bonding is essential.

By End-Use Industry

Construction remains the largest end-use industry, contributing about 35% of global revenue in 2024. Spray adhesives are vital in roofing insulation, flooring, wall paneling, and drywall installations. With rising global construction activities, especially in residential and infrastructure segments, the market continues to expand steadily.

Aerospace is the fastest-growing end-use segment. This is due to a growing need for lightweight, durable materials that meet stringent safety and performance standards. Spray adhesives are increasingly being used for interior cabin bonding, panel assembly, and insulation in aircraft. Their contribution to fuel efficiency through lightweight assembly adds to their attractiveness in this high-tech sector.

Regional Analysis:

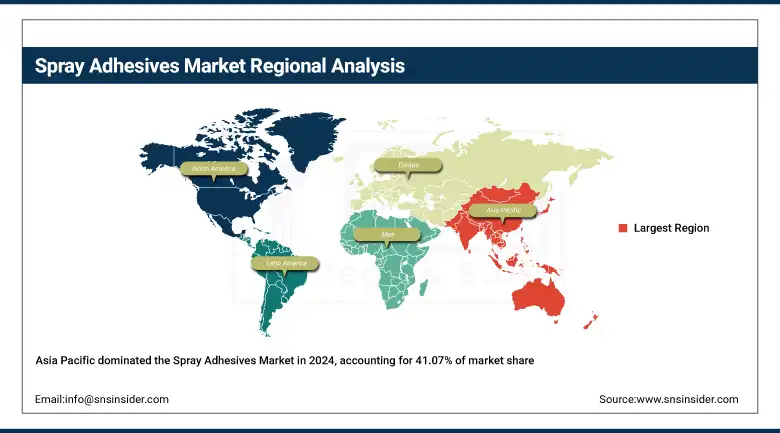

Asia Pacific held the Spray Adhesives market share largest market share, around 41.07%, 2024. It is due to its vast and expanding industrial base. Countries like China, India, Vietnam, and Indonesia are witnessing massive infrastructure projects, growth in furniture manufacturing, and a surge in automotive production, all of which require extensive adhesive applications. Additionally, low-cost manufacturing and the availability of raw materials have attracted major players to establish production facilities in the region. The construction boom across both residential and commercial sectors further boosts demand for spray adhesives in flooring, insulation, and wall systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

For instance, in June 2024, Keck Chimie introduced a new water-based adhesive tailored for Asia’s growing mattress industry, enhancing sustainability by reducing VOC emissions and improving indoor air quality. This type of region-specific product innovation showcases why Asia Pacific remains the dominant force in this market.

The North America region is the fastest-growing market. It is due to its robust automotive, aerospace, and residential renovation industries. The region is also characterized by a strong emphasis on safety and environmental standards, which has accelerated the demand for low-VOC and eco-friendly adhesive formulations. Technological advancements in spray systems, coupled with consistent government regulations favoring non-toxic materials, have spurred innovation among manufacturers. In 2024, a key milestone was achieved when a U.S.-based firm launched a new line of low-VOC bonding adhesives specifically for EPDM and TPO roofing applications. These products not only comply with stringent air quality regulations but also provide improved performance and faster cure times, making them a preferred choice for North American contractors and builders.

Europe maintains a significant share of the spray adhesives market, driven by strict environmental regulations, high standards for indoor air quality, and the region’s leadership in sustainable construction and automotive innovation. Countries such as Germany, France, Italy, and the Netherlands are promoting green buildings and eco-certified construction materials, boosting demand for low-emission, water-based spray adhesives. The rise in modular construction and refurbishment of old housing stock across Europe further strengthens the market for spray adhesives used in insulation, wall linings, and flooring. In a notable development, in early 2025, a leading European adhesive company announced the expansion of its production facility in Belgium, focusing on solvent-free spray adhesives to align with the EU Green Deal targets. This move highlights Europe’s commitment to reducing carbon footprints while encouraging technological innovation in adhesive solutions.

Key Players:

Major Spray Adhesives companies are 3M, H.B. Fuller, Henkel, Arkema, Sika AG, Avery Dennison Corporation, Bostik, ITW Performance Polymers, Ashland, Pidilite Industries, Huntsman Corporation, Worthen Industries, Spray-Lock Inc., FastenMaster, Quilosa, Quin Global, Tensor Global, Permabond, Trim-Lok, Gluefast Company Inc.

Recent Development:

-

In 2024 3M introduced its Fastbond Pressure Sensitive Adhesive 1049, a water-based, solvent-free spray adhesive integrated with the advanced PowerCore portable cylinder system. This product enhances application efficiency with strong initial tack, reduces material waste, and aligns with sustainability objectives through low VOC emissions.

-

In 2024, Pidilite’s joint venture, ICA Pidilite, entered into a licensing agreement focused on UV adhesive technology. This strategic move supports the development of UV-cured spray adhesives, offering faster curing times and enhanced bonding performance for industrial applications.

| Report Attributes | Details |

| Market Size in 2024 | USD 6.95 Billion |

| Market Size by 2032 | USD 11.30 Billion |

| CAGR | CAGR of6.27% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type: Water-based Spray Adhesives, Solvent-based Spray Adhesives, Hot Melt Spray Adhesives, Others (e.g., reactive, UV-cured adhesives) • By Chemistry: Epoxy, Polyurethane, Acrylic, Synthetic Rubber, Others (e.g., silicone, vinyl acetate) • By Application: Furniture & Upholstery, Automotive & Transportation, Building & Construction, Packaging, Others (e.g., textiles, DIY crafts) •By End-Use Industry: Construction, Automotive, Aerospace, Marine, Others (e.g., consumer goods, manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | 3M, H.B. Fuller, Henkel, Arkema, Sika AG, Avery Dennison Corporation, Bostik, ITW Performance Polymers, Ashland, Pidilite Industries, Huntsman Corporation, Worthen Industries, Spray-Lock Inc., FastenMaster, Quilosa, Quin Global, Tensor Global, Permabond, Trim-Lok, Gluefast Company Inc. |

Frequently Asked Questions

Water-based adhesives are used in furniture and crafts, solvent-based in automotive, and hot-melt in packaging and construction.

Rising demand for lightweight materials, eco-friendly adhesives, and fast-curing bonding solutions are key growth drivers.

Major applications include furniture & upholstery, automotive interiors, building insulation, and packaging.

Asia Pacific leads the market due to rapid industrialization, booming construction, and strong automotive production.

The Spray Adhesives Market was valued at approximately USD 6.95 billion in 2024 and is projected to grow at a CAGR of over 6.27% through 2032.

Get in Touch