Tantalum Capacitors Market Report Scope & Overview:

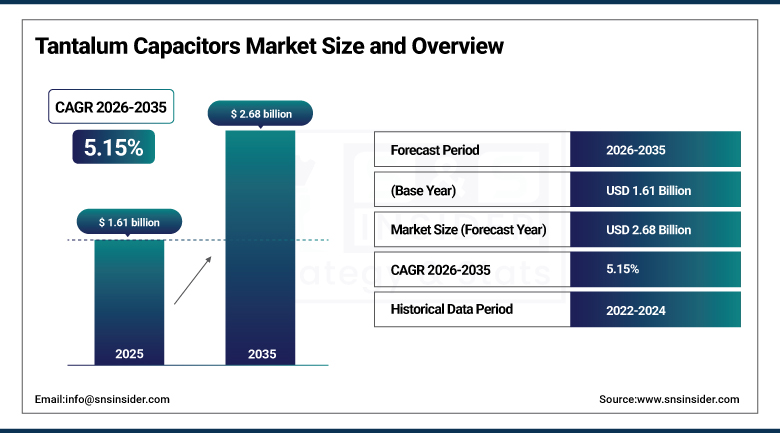

The Tantalum Capacitors Market was valued at USD 1.61 billion in 2025 and is expected to reach USD 2.68 billion by 2035, growing at a CAGR of 5.15% from 2026–2035.

The global tantalum capacitors market holds a strategically critical position in the passive components’ ecosystem, providing high-reliability, high-volumetric-efficiency, and thermally stable energy storage solutions that modern miniaturised electronics depend on for mission-critical power management. Tantalum capacitors use tantalum metal as the anode material, offering exceptionally high capacitance per unit volume relative to aluminium electrolytic alternatives, excellent frequency characteristics, and a field reliability record that makes them the component of choice wherever circuit boards shrink and performance expectations simultaneously rise. These properties make tantalum capacitors indispensable across smartphones and wearables that integrate over 1,000 capacitors per flagship device, medical implants requiring decades-long stable operation within the human body, aerospace and defence electronics demanding performance across extreme temperature ranges, and automotive ADAS and EV power management systems where component failure can compromise occupant safety.

The Tantalum Capacitors Market's 5.15% CAGR from 2026 to 2035 reflects the steady structural demand created by the electronics industry's irreversible miniaturisation trajectory and the premium performance properties of tantalum capacitors that cannot be fully replicated by ceramic or aluminium alternatives in high-reliability, space-constrained applications. The automotive segment's 10.68% CAGR, driven by ADAS, EV power management, and infotainment adoption, represents the fastest-growing demand vector that is simultaneously upgrading per-vehicle tantalum capacitor content and sustaining value growth above the market's overall volume trajectory through the forecast period.

Tantalum Capacitors Market Size and Forecast

-

Market Size in 2025: USD 1.61 Billion

-

Market Size by 2035: USD 2.68 Billion

-

CAGR: 5.15% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Tantalum Capacitors Market - Request Free Sample Report

Tantalum Capacitors Market Trends

-

High adoption rates of polymer tantalum capacitors due to their excellent ESR properties, higher ripple current capacity, and safe failure mechanism as compared to traditional MnO2 solid tantalum capacitors.

-

Increasing tantalum capacitor demand within the automotive industry due to ADAS electronics sensor fusion, electric vehicle battery management systems and power conditioning, as well as power rail filtering within infotainment systems using AEC-Q200 compliant tantalum capacitors which have the required thermal stability and reliability properties for automotive electronic circuits.

-

Higher adoption of surface mount tantalum capacitors due to the increasing popularity of automated printed circuit board assembly processes which prefer SMD components, especially in smartphone, wearable, and medical devices that require more compact PCB designs.

-

Investment in conflict-free tantalum sourcing initiatives where more than 60% of manufacturers implement sustainable tantalum sources in line with the regulations of the Dodd-Frank act and preparing for future DoD sourcing restrictions in Chinese tantalum imports starting in 2027.

-

Increased 5G infrastructure investments driving a higher adoption rate of tantalum capacitors due to their high-frequency performance, which is needed for high-speed signalling within base stations, millimetre-wave radio frequency filtering, and network equipment power conditioning.

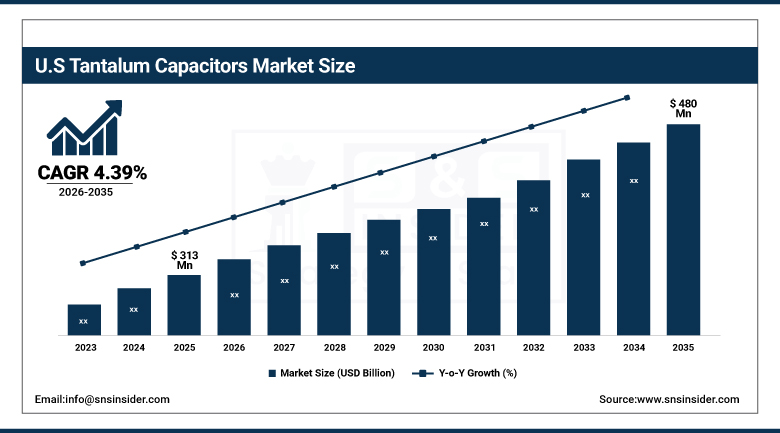

U.S. Tantalum Capacitors Market was valued at USD 313 million in 2025 and is expected to reach USD 480 million by 2035, registering a CAGR of 4.39% during 2026–2035.

The United States represents a significant tantalum capacitors market anchored by world-leading defence and aerospace electronics procurement, a large medical device manufacturing industry, and the commercial presence of leading manufacturers and distributors including KEMET (YAGEO), Vishay Intertechnology, and KYOCERA AVX. U.S. Department of Defense demand for radiation-hardened and space-qualified tantalum capacitors sustains a premium pricing tier that distinguishes the U.S. market from cost-sensitive consumer electronics procurement. Restrictions on sourcing Chinese tantalum components beginning 2027 are prompting qualification of supplies of tantalum from Australia and Brazil, shifting sourcing to supply chains of allied nations that increase security for domestic components sourcing. Capacity expansion by Vishay selectively directed at polymer tantalum products aimed specifically at the needs of AI servers is indicative of the product development expenditures necessary to fuel value growth in the U.S. market.

The March 2024 release of KEMET's T581 capacitors qualified according to MIL-PRF-32700/2 military requirements, together with distribution of Quantic Electronics' products by Powell Electronics in an aerospace and defense market expansion effort, are evidence of the high-end characteristics of the U.S. tantalum capacitor market whereby specifications within the military and medical sectors ensure healthy margins conducive to growth into 2026 to 2035.

Tantalum Capacitors Market Segment Insights

-

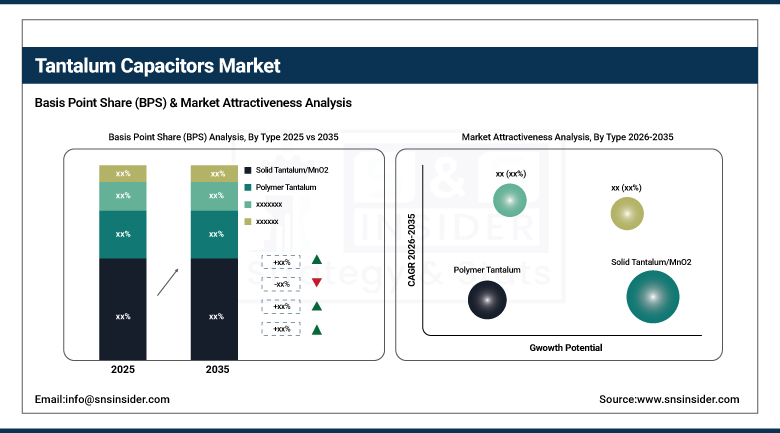

According to Type, Solid Tantalum (MnO2) dominated in 2025 due to wide application adoption and established reliability record; Polymer Tantalum is the fastest-growing type driven by low-ESR and high safety advantages in consumer and automotive applications.

-

In terms of Mount Type, Surface Mount dominated with approximately 64% market share in 2025 and is simultaneously the fastest-growing mount type at a CAGR of 6.90% through 2035, driven by PCB assembly automation and compact design requirements across all major electronics sectors.

-

By Application, Consumer Electronics dominated in 2025 as the largest end-use revenue segment; Automotive is the fastest-growing application at a CAGR of 10.68% through 2035 driven by ADAS, EV battery management, and infotainment system proliferation.

Tantalum Capacitors Market Segment Analysis

By Type: Solid Tantalum (MnO2) dominates, Polymer Tantalum grows fastest

The Solid Tantalum (MnO2) Tantalum Capacitors held the largest share of the Tantalum Capacitors Market in 2025, being the most widely used form of tantalum capacitor across the most application sectors. The solid tantalum capacitors with MnO2 electrodes are characterized by their high reliability, wide temperature range from -55°C to +125°C, good frequency characteristics, and long qualification record in such applications as automotive, industrial, and defence, where AEC-Q200 and MIL-PRF standards apply for component approval. The mature production base and widespread market availability among the manufacturers of tantalum capacitors allow making solid tantalum capacitors default choice in high-reliability electronics worldwide.

Polymer tantalum capacitors are the fastest-growing type segment through 2035, driven by demand for exceptionally low equivalent series resistance in power management ICs within consumer electronics, automotive infotainment, and telecommunications infrastructure. Polymer tantalum capacitors use a conductive polymer cathode instead of MnO2, delivering ESR values as low as 5 milliohms that enable superior switching regulator efficiency and output ripple performance.

By Mount Type: Surface Mount dominates and simultaneously grows fastest

Surface Mount tantalum capacitors dominated the Tantalum Capacitors Market in 2025 with approximately 64% of global revenues and are simultaneously the fastest-growing mount type segment with a projected CAGR of 6.90% through 2035, the unique distinction of being both the current market leader and the fastest-growing category reflecting the universal and accelerating adoption of surface mount PCB assembly across every electronics product sector. Surface mount technology enables fully automated pick-and-place assembly at dramatically higher production speeds than through-hole processes, reducing assembly costs and enabling the high-density PCB layouts that compact consumer electronics, automotive ECUs, and medical devices require. The consistent trend toward smaller form factors, thinner profiles, and higher component density on double-sided PCBs systematically favours surface mount architectures.

Tantalum capacitors using through-hole technology still have significant market presence in terms of applications for control electronics in industry, in power supplies, in aerospace and defense, and for the upkeep of older systems where through-hole mounting offers better resistance to the effects of vibration and thermal cycling stresses, which might prove too much for surface mount technology to withstand after many years of use. Through-hole technology continues to benefit from steady demand in defense and industrial markets, characterized by lengthy product cycles and cautious part selection processes.

By Application: Consumer Electronics dominates, Automotive grows fastest

Consumer Electronics dominated the Tantalum Capacitors Application segment in 2025 with the largest revenue share, reflecting the electronic intensity of modern smartphones, tablets, wearables, true wireless earbuds, and smart home devices that collectively require high-performance tantalum capacitors for power management, audio filtering, and high-frequency circuit decoupling. A modern flagship smartphone integrates over 1,000 passive components, with tantalum capacitors serving the critical power rail conditioning roles where volumetric efficiency and thermal stability are simultaneously required to meet compact form factor and multi-day battery life expectations. The continuous expansion of connected consumer electronics into new form factors including foldable smartphones and miniaturised wearable health sensors reinforces tantalum capacitor demand within this dominant segment.

The Automotive application segment is the fastest-growing tantalum capacitor end-use at a CAGR of 10.68% from 2026 to 2035, driven by three simultaneous demand vectors: the proliferation of ADAS sensor fusion electronics including radar, LiDAR, and camera systems that each require high-reliability tantalum capacitors in their power management and signal conditioning circuits; the rapid expansion of EV battery management systems requiring precision power conditioning components qualified to automotive safety integrity level standards; and the growing infotainment and connectivity system content making each new vehicle model an electronics-intensive platform consuming multiple times the passive component count of equivalent vehicles from a decade ago. The automotive tantalum capacitor content per vehicle is expanding significantly across all price segments as electrification and autonomy features cascade from luxury into mainstream models.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~80% |

|

Europe |

Germany |

~33% |

|

Asia Pacific |

China |

~48% |

|

Middle East & Africa |

UAE |

~26% |

|

Latin America |

Brazil |

~44% |

Asia Pacific Tantalum Capacitors Market Insights

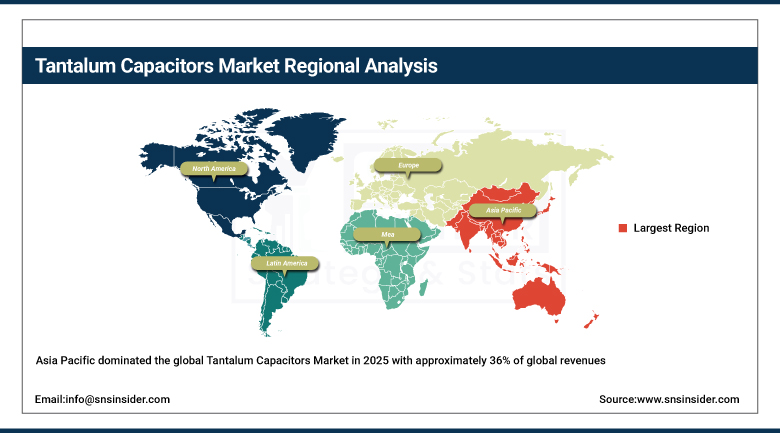

Asia Pacific dominated the global Tantalum Capacitors Market in 2025 with approximately 36% of global revenues and is projected to register the highest CAGR of 7.69% through 2035, driven by the world's largest consumer electronics manufacturing base concentrated in China, South Korea, Taiwan, and Japan, combined with rapidly expanding 5G infrastructure, growing automotive electronics production, and favourable government semiconductor manufacturing initiatives. China leads regional consumption through its massive smartphone and consumer electronics manufacturing industry, while South Korea and Taiwan's world-leading semiconductor foundries drive substantial tantalum capacitor volumes in advanced electronic components.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Tantalum Capacitors Market Insights

North America represents a high-value tantalum capacitors market driven by defence and aerospace electronics procurement, medical device manufacturing, and major tantalum capacitor producer commercial presence. The United States accounts for approximately 80% of North American revenues, supported by strong military specification demand, substantial medical implant manufacturing, and the growing AI server market where polymer tantalum capacitors are gaining adoption in high-performance power delivery network applications. DoD 2027 Chinese tantalum sourcing restrictions are catalysing supply chain qualification investments benefiting North American distributors and allied-nation qualified manufacturers.

Europe Tantalum Capacitors Market Insights

Europe is a technically sophisticated tantalum capacitors market, driven by Germany's advanced automotive electronics manufacturing sector, aerospace and defence procurement across France, the UK, and Italy, and the presence of specialist tantalum capacitor technology developers including Exxelia. European automotive OEM demand for AEC-Q200 qualified tantalum capacitors in ADAS, EV, and premium infotainment applications sustains strong revenue growth.

Latin America and MEA Tantalum Capacitors Market Insights

Latin America and MEA are growing tantalum capacitors markets, with Brazil playing a dual role as both a tantalum raw material supplier from its mineral-rich deposits and a growing consumer through its expanding electronics manufacturing sector. MEA adoption is driven by defence electronics procurement across Gulf Cooperation Council nations and growing telecommunications infrastructure investment requiring high-reliability passive components.

Tantalum Capacitors Market Growth Drivers:

-

Electronics miniaturisation and automotive electrification simultaneously expanding tantalum capacitor demand across premium performance and volume segments

The primary structural growth drivers for the Tantalum Capacitors Market are the electronics industry's unrelenting miniaturisation imperative that consistently favours tantalum's superior volumetric efficiency over ceramic and aluminium alternatives in space-constrained applications, and the automotive electrification wave that is dramatically expanding per-vehicle tantalum capacitor content through ADAS, EV battery management, and infotainment system proliferation. These two structural forces operate across different market segments but create complementary demand dynamics that collectively sustain the market's 5.15% CAGR through the forecast period.

Vishay Intertechnology's January 2025 introduction of the TSM3 series surface-mount cermet trimmers combining a compact 3 mm by 4 mm footprint with a minus 65 to plus 150 degree Celsius temperature range represents the premium performance envelope that differentiates tantalum-based passive components from commodity alternatives. KEMET's MIL-PRF-32700/2 qualified T581 capacitors and Quantic Electronics' aerospace and defence distribution expansion collectively demonstrate how leading manufacturers continuously innovate within the high-reliability passive component space to sustain premium pricing and technical barrier to substitution through the 2026 to 2035 forecast period.

Tantalum Capacitors Market Restraints:

-

Conflict mineral sourcing complexity, competition from MLCC alternatives, and raw material price volatility constraining broad market growth

A significant restraint on the Tantalum Capacitors Market is the geopolitical complexity and ethical responsibility requirements associated with tantalum raw material sourcing, particularly from the Democratic Republic of Congo and neighbouring regions classified as conflict-affected territories under Dodd-Frank Act Section 1502 reporting requirements, which add compliance cost and supply chain verification burden to all tantalum capacitor manufacturers and end-users. Multilayer ceramic capacitors continue to improve their high-capacitance performance and increasingly compete with low-end tantalum capacitors in non-critical applications where absolute reliability is less critical than cost optimisation. Raw material price volatility driven by geopolitical events, mining disruption, and semiconductor demand cycles creates gross margin unpredictability for manufacturers unable to pass through input cost spikes.

Tantalum Capacitors Market Opportunities:

-

EV power electronics content expansion, AI server power delivery network adoption, and allied-nation responsible sourcing premium positioning

The electric vehicle megatrend creates a compelling, policy-driven tantalum capacitor growth opportunity as each EV platform contains dramatically more power management electronics than an equivalent internal combustion engine vehicle, with battery management systems, on-board chargers, and DC-DC converters all specifying high-reliability capacitors meeting automotive safety standards. The AI computing infrastructure buildout, where polymer tantalum capacitors are gaining adoption in server power delivery networks for superior ESR and transient response characteristics, represents a growing and technically differentiated demand category. Manufacturers that build robust, auditable responsible sourcing credentials for conflict-free tantalum from Australia, Brazil, and allied nations will command sustainability premium pricing from European automotive OEMs and U.S. defence procurement authorities through the forecast period.

Recent Developments:

-

March 2024: KEMET introduced the first T581 capacitors qualified to Military Performance Specification MIL-PRF-32700/2, expanding its mil-spec tantalum capacitor portfolio for defence electronics procurement programmes.

-

January 2025: Vishay Intertechnology introduced the TSM3 series surface-mount cermet trimmers with a compact 3 mm footprint and wide minus 65 to plus 150 degree Celsius temperature range for space-constrained industrial, consumer, and telecom applications.

-

2025: Quantic Electronics established a distribution accord with Powell Electronics, broadening its aerospace and defence tantalum capacitor market reach across long-qualification-cycle military supply tiers.

-

2025: Orient Tantalum Industry accelerated R&D investment in polymer tantalum capacitor technology for fast-charging EV applications, positioning its portfolio for the premium automotive tantalum segment growing at 10.68% CAGR through 2035.

-

October 2025: Murata Manufacturing and QuantumScape entered a collaboration to mass-produce ceramic films for solid-state batteries, reflecting the broader passive component industry's strategic investment in next-generation energy storage materials relevant to the EV market.

Tantalum Capacitors Market Key Players

-

KEMET Corporation (YAGEO Corporation)

-

KYOCERA AVX Components Corporation

-

Vishay Intertechnology Inc.

-

Panasonic Corporation

-

Murata Manufacturing Co. Ltd.

-

TDK Corporation

-

Exxelia Group

-

NIC Components Corp.

-

Abracon LLC

-

Rohm Semiconductor

-

Sunlord Electronics Co. Ltd.

-

Cornell Dubilier Electronics Inc.

-

Hongda Electronics Corp.

-

Matsuo Electric Co. Ltd.

-

Quantic Electronics

-

Global Capacitor Group

-

Semec Technology Company Ltd.

-

Righton Ltd.

-

Talison Minerals Pvt. Ltd.

-

Vishay Draloric

Tantalum Capacitors Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.61 Billion |

| Market Size by 2035 | USD 2.68 Billion |

| CAGR | CAGR of 5.15% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Solid Tantalum/MnO2, Polymer Tantalum, Wet/Electrolytic Tantalum) • By Mount Type (Surface Mount, Through Hole) • By Application (Consumer Electronics, Telecommunications, Automotive, Medical Devices, Aerospace and Defense, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | KEMET Corporation (YAGEO Corporation), KYOCERA AVX Components Corporation, Vishay Intertechnology Inc., Panasonic Corporation Murata Manufacturing Co. Ltd., TDK Corporation, Exxelia Group, NIC Components Corp., Abracon LLC, Rohm Semiconductor, Sunlord Electronics Co. Ltd., Cornell Dubilier, Electronics Inc., Hongda Electronics Corp., Matsuo Electric Co. Ltd., Quantic Electronics, Global Capacitor Group, Semec Technology Company Ltd., Righton Ltd., Talison Minerals Pvt. Ltd., Vishay Draloric |

Frequently Asked Questions

Ans: The electronics miniaturisation trend creating sustained demand for tantalum's superior volumetric efficiency in space-constrained applications, combined with automotive electrification driving ADAS, EV battery management, and infotainment content growth at a CAGR of 10.68%, are the primary structural growth drivers through 2035.

Ans: Asia Pacific dominated with approximately 36% of global revenues in 2025 and is also the fastest-growing region at a CAGR of 7.69%, anchored by China, South Korea, Taiwan, and Japan's world-leading consumer electronics manufacturing base, expanding 5G infrastructure, and growing automotive electronics production.

Ans: Automotive is the fastest-growing application at a CAGR of 10.68% from 2026 to 2035, driven by the proliferation of ADAS sensor fusion electronics, EV battery management systems, and infotainment platforms each requiring high-reliability AEC-Q200 qualified tantalum capacitors in mission-critical automotive electronics.

Ans: Surface Mount dominated with approximately 64% of global revenues in 2025 and is also the fastest-growing mount type at a CAGR of 6.90%, driven by PCB assembly automation requirements and compact circuit board design trends across consumer electronics, automotive, and medical device manufacturing.

Ans: The Tantalum Capacitors Market was valued at USD 1.619 billion in 2025.

Ans: The Tantalum Capacitors Market is expected to grow at a CAGR of 5.15% from 2026 to 2035.

Get in Touch