Telecom Electronic Manufacturing Services Market Report Scope & Overview:

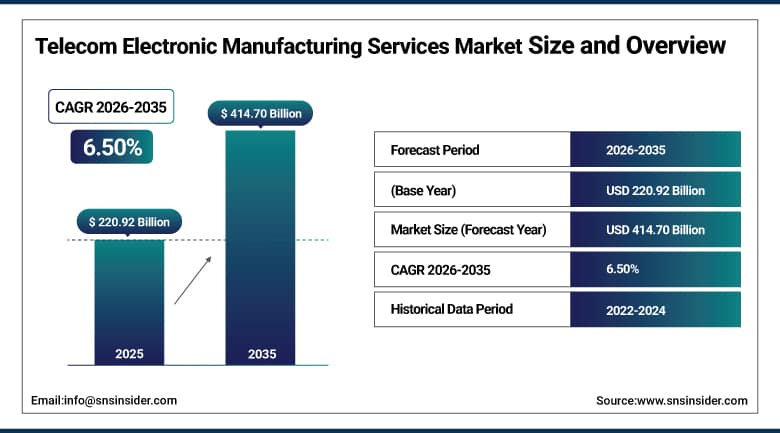

The Telecom Electronic Manufacturing Services Market was valued at USD 220.92 Billion in 2025 and is expected to reach USD 414.70 Billion by 2035, growing at a CAGR of 6.50% from 2026 to 2035.

Telecom electronic manufacturing services (EMS) encompass the full spectrum of contract design, fabrication, assembly, testing, and supply chain management activities performed by specialized outsourcing partners on behalf of telecommunications equipment original equipment manufacturers whose core competencies in system architecture, wireless technology, and software differentiation make the outsourcing of hardware manufacturing operations both economically rational and strategically beneficial. The telecom EMS market differs from general-purpose electronic manufacturing services in the particularly stringent performance requirements of the components produced, where telecommunications equipment including 5G base station radios, core network switches, optical transport equipment, and satellite communication terminals must satisfy exacting electrical specifications for signal quality, frequency precision.

Foxconn Technology Group, the world's largest contract electronics manufacturer, announced expanded telecom infrastructure manufacturing capacity at its Guiyang and Shenzhen facilities in 2025 to serve growing 5G base station component assembly demand from Ericsson and Nokia whose supply chain strategies increasingly leverage Foxconn's manufacturing scale and process automation capability for radio unit production. The expansion included automated SMT assembly lines optimized for 5G massive MIMO radio unit PCB complexity, integrated RF testing infrastructure calibrated for millimetre wave antenna array characterization, and supply chain management systems enabling just-in-time component delivery coordination across Foxconn's global procurement network. The strategic partnership between Foxconn and major Nordic telecom OEMs reflected the growing trend toward deeper EMS partner integration within telecom equipment supply chains.

Market Size and Forecast

-

Market Size in 2026E: USD 233.84 Billion

-

Market Size by 2035: USD 414.70 Billion

-

CAGR: 6.50% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Telecom Electronic Manufacturing Services Market - Request Free Sample Report

Telecom Electronic Manufacturing Services Market Trends

-

Increasing 5G infrastructure manufacturing complexity is driving stronger partnerships between telecom OEMs and EMS providers for advanced RF assembly and testing.

-

Open RAN adoption is expanding EMS opportunities by increasing demand for interoperable and white-box telecom equipment manufacturing.

-

Nearshoring and supply chain regionalization are accelerating telecom EMS investments to improve supply chain resilience and reduce geopolitical risks.

-

AI-powered quality control and process automation are enhancing manufacturing efficiency through automated inspection, yield optimization, and predictive production analytics.

-

Sustainable manufacturing practices are becoming a key competitive differentiator as telecom OEMs prioritize low-carbon production and energy-efficient EMS operations.

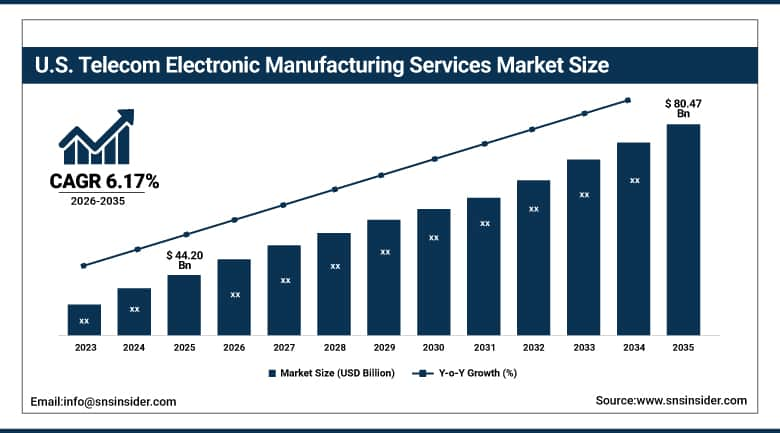

The U.S. Telecom Electronic Manufacturing Services Market Outlook

The U.S. Telecom Electronic Manufacturing Services Market was valued at approximately USD 44.20 Billion in 2025 and is expected to reach approximately USD 80.47 Billion by 2035, growing at a CAGR of approximately 6.17%.

The United States is the largest national telecom EMS market within North America, anchored by the domestic operations of major EMS providers including Jabil, Flex Ltd., Celestica, Sanmina, Plexus Corp., and Benchmark Electronics whose telecom-focused manufacturing capabilities serve U.S.-headquartered and multinational telecom OEMs. The U.S. 5G deployment investment cycle, driven by spectrum auction proceeds deployment, spectrum sharing agreements, and FCC incentive programmes for rural connectivity, sustains equipment procurement at AT&T, Verizon, and T-Mobile that flows through to EMS production volumes. The CHIPS and Science Act and the Infrastructure Investment and Jobs Act are collectively stimulating domestic electronics manufacturing investment that is expanding U.S. telecom EMS capacity and capability beyond what market demand.

Sanmina Corporation opened a new manufacturing facility in Austin, Texas in August 2025, expanding its telecommunications division production capacity to serve growing 5G infrastructure equipment demand from Ericsson and other telecom OEM customers whose supply chain strategies prioritized North American manufacturing for equipment destined for U.S. and Canadian network deployments. The facility incorporated advanced automated assembly capability including selective soldering, automated optical inspection, and system-level test infrastructure for complex network equipment chassis and high-density PCB assemblies. The Austin location's proximity to major semiconductor design centres and its access to Texas's competitive manufacturing labor market supported Sanmina's nearshoring strategy for telecom customers seeking domestic supply chain alternatives to Asian-concentrated EMS production.

Telecom Electronic Manufacturing Services Market Segment Analysis

-

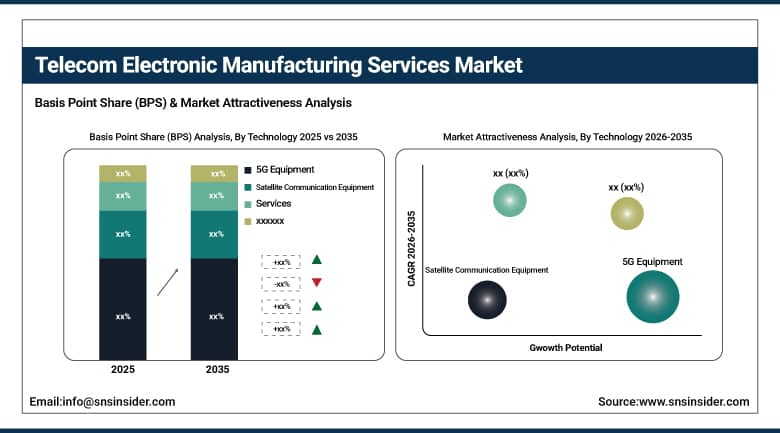

By Technology, the 5G equipment segment dominated the Telecom EMS market in 2025, while the satellite communication equipment segment is the fastest growing technology during 2026 to 2035.

-

By Service Type, the electronic manufacturing services (EMS) segment dominated the telecom electronic manufacturing services market with approximately 68.4% revenue share in 2025, while the design services segment is the fastest growing service type during 2026 to 2035.

-

By Product Type, the transceivers & transmitters segment dominated the Telecom EMS market with the largest revenue share in 2025, while the base station equipment segment is the fastest growing product type at a CAGR of 5.90% during 2026 to 2035.

-

By End User, the telecom OEMs segment dominated the Telecom EMS market in 2025, while the data centers segment is the fastest growing end user during 2026 to 2035.

By Technology, 5G equipment dominates, satellite communication grows fastest

5G equipment retained the dominant technology segment position in the Telecom EMS market in 2025, encompassing the radio units, baseband units, active antenna systems, small cells, and core network equipment that constitute the primary capital investment category for mobile network operators globally deploying 5G infrastructure. The EMS manufacturing content in 5G equipment is substantially higher than equivalent 4G equipment due to the increased component count in massive MIMO antenna systems, the greater complexity of 5G radio frequency front-end designs incorporating GaN power amplifiers and millimetre wave beamforming networks, and the system-level integration of digital processing, radio frequency electronics, and thermal management that characterizes 5G radio unit architecture. Satellite communication equipment is growing fastest as the LEO broadband satellite constellation programmes from SpaceX, Amazon, and European operators are creating unprecedented demand for satellite payloads, user terminals, and gateway ground station equipment that requires sophisticated EMS manufacturing capability for space-grade assembly standards and volume consumer terminal production.

By Service Type, electronic manufacturing dominates, design services grows fastest

Electronic manufacturing services generated the largest revenue share in the Telecom EMS market in 2025, encompassing the printed circuit board assembly, box build integration, complex system assembly, and packaging and fulfilment operations that constitute the highest-value portion of the EMS provider's commercial relationship with telecom OEM customers. The manufacturing services segment's dominance reflects the volume-intensive nature of telecom equipment production at the 5G deployment scale, where hundreds of millions of radio units, small cells, customer premises equipment, and network elements are being manufactured annually across the global build-out of 5G infrastructure. Design services are growing fastest as telecom OEMs increasingly engage EMS partners not just as manufacturers but as design partners who contribute design-for-manufacturability expertise, radio frequency design capability, and system integration knowledge to new product development programmes whose time-to-market competitive pressure justifies investment in EMS co-development relationships.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

42.84% |

|

Middle East & Africa |

UAE |

24.73% |

|

Latin America |

Brazil |

43.84% |

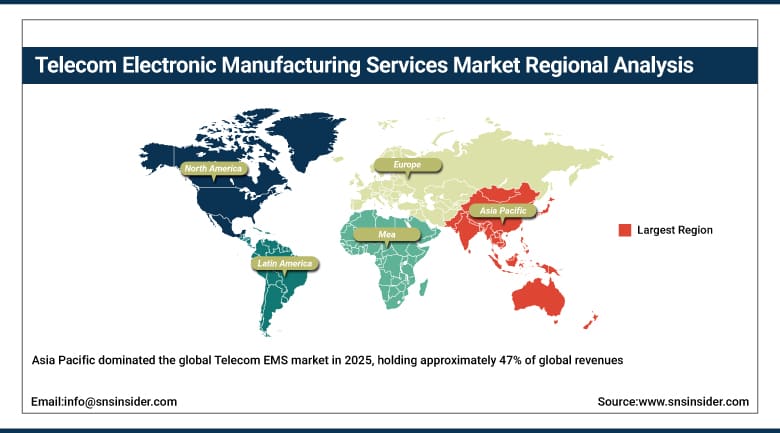

Asia Pacific Telecom Electronic Manufacturing Services Market Insights

Asia Pacific dominated the global Telecom EMS market in 2025, holding approximately 47% of global revenues, and is projected to maintain its dominant regional position through 2035 driven by China's unmatched electronics manufacturing infrastructure, the concentration of Tier 1 EMS providers including Foxconn, Wistron, and Pegatron whose manufacturing scale and process automation capability make them the preferred partners for high-volume telecom equipment production. China accounts for approximately 42.84% of Asia Pacific revenues through its domestic 5G infrastructure rollout generating both domestic and export-oriented telecom equipment production, and through the Asia Pacific concentration of global telecom OEM manufacturing. South Korea, Taiwan, Japan, and India each contribute meaningful regional demand through their telecommunications equipment manufacturing industries.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Telecom Electronic Manufacturing Services Market Insights

North America is the fastest-growing regional telecom EMS market and the second-largest by revenue. The United States accounts for approximately 84.73% of regional revenue through the concentration of major EMS providers whose telecom-focused facilities serve both domestic OEM customers and the nearshoring demand of international OEMs seeking North American manufacturing for equipment destined for U.S. and Canadian network deployments. The CHIPS Act and allied domestic manufacturing incentives are creating greenfield and capacity expansion investment in U.S. telecom EMS facilities that is progressively expanding the domestic EMS capacity available for telecom equipment production. Canada contributes supplementary North American demand through its telecom equipment manufacturing for domestic network deployments and its participation in cross-border supply chains serving U.S. telecom OEM customers.

Europe Telecom Electronic Manufacturing Services Market Insights

Europe held a prominent share of global telecom EMS revenues in 2025. Germany accounts for approximately 27.84% of European revenues through the domestic operations of Ericsson, Nokia, and their supply chain partners whose European equipment manufacturing for continental network deployments creates substantial EMS demand. The EU's European Chips Act and telecommunications sovereignty initiatives are stimulating domestic manufacturing investment that reduces European telecom equipment supply chains' dependence on Asian EMS capacity. Finland, Sweden, France, Poland, and Romania each contribute meaningful European demand through EMS facilities serving Nordic OEM customers and the growing Eastern European EMS manufacturing base serving continental European telecom and industrial customers.

MEA & Latin America Telecom Electronic Manufacturing Services Market Insights

Middle East and Latin America represent growing Telecom EMS markets where telecommunications infrastructure investment and government digital connectivity programmes are creating expanding equipment demand. The UAE leads MEA revenues at approximately 24.73% of the regional total through its advanced telecommunications infrastructure investment, its growing status as a regional data centre hub whose networking equipment procurement sustains EMS demand, and the Abu Dhabi and Dubai smart city programmes deploying advanced communications infrastructure. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large telecommunications market, growing 5G deployment investment by Claro, Vivo, and TIM Brasil, and the domestic electronics manufacturing ecosystem serving telecom OEM production requirements.

Market Dynamics

Growth Drivers: 5G network infrastructure deployment creating sustained equipment manufacturing demand and satellite communication constellation expansion adding new high-volume EMS production requirements globally.

The global 5G deployment cycle represents the most commercially significant equipment manufacturing demand event in the telecom EMS market's history, with annual 5G radio unit production volumes scaling from tens of millions in early deployment years to potentially hundreds of millions units annually at full global network density. Each successive 5G network densification phase, from initial coverage build-out to urban capacity enhancement with small cells, requires additional equipment manufacturing that sustains EMS production volumes even after primary macro base station deployment is largely complete. The concurrent deployment of LEO satellite broadband constellations requiring production of tens of thousands of satellite payloads and potentially hundreds of millions of user terminal phased array antennas represents a parallel demand driver whose manufacturing complexity and volume combine to create a strategically important new product category within the telecom EMS market.

Restraints: Supply chain component concentration and geopolitical risk in Asia Pacific and the complexity of qualifying new EMS partners to telecom equipment quality standards constrain supply chain diversification velocity.

The concentration of semiconductor component supply, PCB fabrication, and final assembly capacity for telecom equipment within a small number of Asian manufacturing hubs creates supply chain vulnerability whose commercial consequences were demonstrated by the 2020 to 2022 component shortage period when semiconductor supply disruptions caused significant telecom equipment delivery delays for Ericsson, Nokia, and Ciena whose equipment backlogs extended to multi-quarter horizons. Diversifying telecom EMS supply chains toward North American and European manufacturing locations requires qualification investment that is lengthy for complex 5G equipment whose manufacturing standards include OEM-specific process certifications, reliability testing programmes, and quality management system audits that new EMS facilities must complete before production qualification is granted.

Opportunities: Open RAN architecture creating new EMS manufacturing opportunities and nearshoring investment incentives enabling North American and European telecom EMS capacity expansion represent major commercial growth opportunities for EMS providers.

Open RAN architecture's disaggregation of the base station into separately procurable radio unit, distributed unit, and central unit software components, each potentially sourced from different vendors and manufactured by different EMS partners, is restructuring the telecom EMS competitive landscape. Traditional integrated equipment supply chains where Ericsson or Nokia designed and manufactured complete base station solutions with a small number of qualified EMS partners are progressively opening to a broader supplier ecosystem whose white-box radio unit designs and open interface standards create manufacturing opportunities for EMS providers that were previously excluded from the vertically integrated incumbent supply chain. Government manufacturing incentive programmes in the United States, European Union, India, and Japan each offer financial support for telecom electronics manufacturing capacity investment that can accelerate the business.

Recent Developments:

-

2025: Foxconn Technology Group expanded telecom infrastructure manufacturing capacity at Guiyang and Shenzhen facilities to serve 5G base station component assembly demand from Ericsson and Nokia, incorporating automated SMT assembly lines for massive MIMO radio unit PCB complexity and integrated millimetre wave antenna array RF testing infrastructure.

-

2025: Sanmina Corporation opened a new Austin, Texas manufacturing facility expanding telecommunications division capacity for 5G infrastructure equipment, incorporating advanced automated assembly and system-level test infrastructure for network equipment chassis serving nearshoring demand from telecom OEM customers prioritising North American supply chain manufacturing.

-

2024: Plexus Corp. secured a contract to provide electronic manufacturing services for Ericsson's next-generation 5G telecom equipment, supporting advanced infrastructure rollout with precision assembly and testing capabilities aligned with Ericsson's quality management requirements for network equipment deployed by major mobile operators globally.

Telecom Electronic Manufacturing Services Market Key Players are:

-

Foxconn Technology Group (Hon Hai Precision Industry Co. Ltd.)

-

Jabil Inc.

-

Flex Ltd.

-

Celestica Inc.

-

Sanmina Corporation

-

Plexus Corp.

-

Wistron Corporation

-

Benchmark Electronics Inc.

-

Kimball Electronics Inc.

-

Venture Corporation Ltd.

-

USI (Universal Scientific Industrial) Co. Ltd.

-

TTM Technologies Inc.

-

Fabrinet

-

Compal Electronics Inc.

-

Pegatron Corporation

-

Inventec Corporation

-

BYD Electronic International Company Ltd.

-

Enics Group AG

-

IMI (Integrated Micro-Electronics Inc.)

-

SMTC Corporation

Telecom Electronic Manufacturing Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 220.92 Billion |

| Market Size by 2035 | USD 414.70 Billion |

| CAGR | CAGR of 6.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Electronic Manufacturing Services, Design Services, Testing Services, Supply Chain Management Services) • By Product Type (Transceivers & Transmitters, Base Station Equipment, Printed Circuit Boards, Antennas, Network Switching Equipment, Others) • By Technology (5G Equipment, 4G/LTE Equipment, Fiber Optic Equipment, Satellite Communication Equipment, Others) • By End User (Telecom OEMs, Network Operators, Data Centers, Government & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Foxconn Technology Group (Hon Hai Precision Industry Co. Ltd.), Jabil Inc., Flex Ltd., Celestica Inc., Sanmina Corporation, Plexus Corp., Wistron Corporation, Benchmark Electronics Inc., Kimball Electronics Inc., Venture Corporation Ltd., USI (Universal Scientific Industrial) Co. Ltd., TTM Technologies Inc., Fabrinet, Compal Electronics Inc., Pegatron Corporation, Inventec Corporation, BYD Electronic International Company Ltd., Enics Group AG, IMI (Integrated Micro-Electronics Inc.), and SMTC Corporation |

Frequently Asked Questions

The Telecom Electronic Manufacturing Services Market is expected to grow at a CAGR of 6.50% from 2026 to 2035.

The Telecom Electronic Manufacturing Services Market was valued at USD 220.92 Billion in 2025.

The electronic manufacturing services segment dominated the Telecom Electronic Manufacturing Services Market in 2025.

Asia Pacific dominated the Telecom Electronic Manufacturing Services Market in 2025, holding approximately 47% of global revenues.

The primary growth factors are 5G network infrastructure deployment creating sustained equipment manufacturing demand at unprecedented scale, LEO satellite constellation expansion adding high-volume EMS production requirements, Open RAN architecture broadening the EMS partner ecosystem beyond traditional integrated OEM supply chains.

Get in Touch