Thin Client Market Report Scope & Overview:

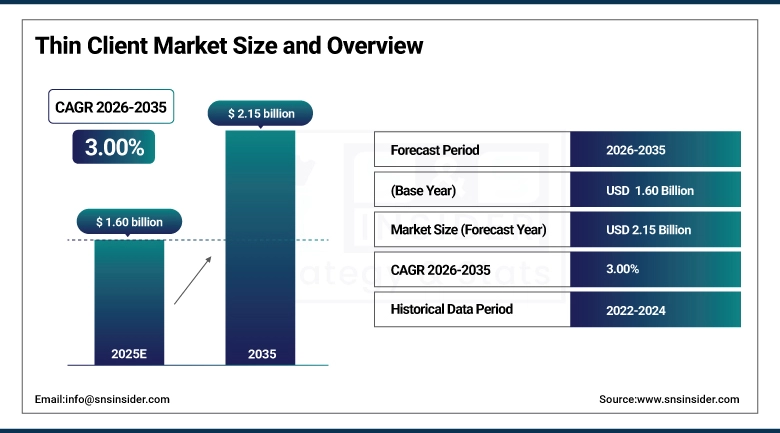

The Thin Client Market Size was valued at USD 1.60 Billion in 2025 and is expected to reach USD 2.15 Billion by 2035, growing at a CAGR of 3.00% over the forecast period of 2026–2035.

Thin clients are not a new concept they have been a fixture of enterprise IT for decades but the context around them has shifted considerably. What once looked like a niche play for cost-conscious IT departments is now a natural fit for the way organisations increasingly think about computing: centralised, cloud-connected, and built around security rather than local processing power. The rise of Virtual Desktop Infrastructure as a mainstream enterprise architecture, combined with a post-pandemic shift toward hybrid working, has given thin clients a second wind. When the compute happens on a server or in the cloud, the endpoint device needs to do very little and thin clients are purpose-built for exactly that role.

In 2024, the commercial segment spanning BFSI, education, and healthcare — accounted for over 48% of U.S. thin client market share, as organisations in those sectors prioritised centralised management, regulatory compliance, and reduced IT overhead over local processing capability.

Thin Client Market Size and Growth Forecast:

- Market Size in 2025: USD 1.60 Billion

- Market Size by 2035: USD 2.15 Billion

- CAGR: 3.00% from 2025 to 2035

- Base Year: 2025

- Forecast Period: 2026–2035

- Historical Data: 2021–2023

To Get more information on Thin Client Market - Request Free Sample Report

Key Trends in the Thin Client Market:

- Centralised computing is becoming the default architecture in mid-to-large enterprises — IT teams are consolidating data processing, cutting hardware sprawl, and pushing management out to a central platform where patching and provisioning can happen at scale.

- Hybrid and remote work has permanently changed endpoint requirements. Thin clients offer a way to give distributed employees secure access to enterprise applications without putting sensitive data on local hardware that may be lost or stolen.

- Security is a genuine differentiator rather than a checkbox. With no local storage and minimal local processing, thin clients have a materially smaller attack surface than traditional PCs, which matters in sectors where data breach consequences are severe.

- VDI adoption from VMware, Citrix, and Microsoft Azure Virtual Desktop is directly correlated with thin client demand each new VDI deployment creates endpoint refresh opportunities that thin client vendors are well positioned to capture.

- Energy efficiency has moved from a nice-to-have to a procurement criterion. Thin clients typically draw 4–15W versus 65–250W for traditional desktops, and that gap shows up meaningfully in total cost of ownership calculations at enterprise scale.

- Device-as-a-Service and subscription models are making it easier for mid-market organisations to access thin client infrastructure without large upfront capital commitments, widening the addressable customer base beyond large enterprises.

U.S. Thin Client Market Size Outlook:

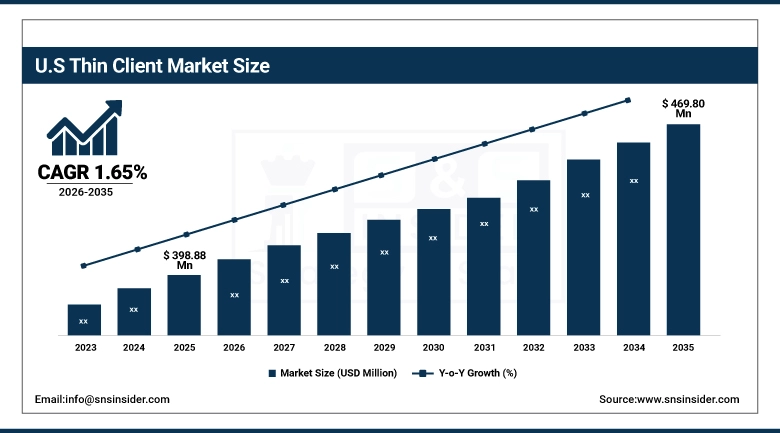

The U.S. Thin Client Market was valued at USD 398.88 Million in 2025 and is projected to grow up to 469.80 Million till 2035 at a CAGR of 1.65 % over the forecast period 2026-2035. The U.S. market sits at an interesting point. It is the most mature thin client geography in the world large enterprises and government agencies have been running thin client deployments for years which means growth comes more from technology refresh cycles, VDI platform upgrades, and expansion into new verticals than from converting first-time buyers. Healthcare is probably the most active growth vertical right now, as hospital systems deal with the twin pressures of HIPAA compliance and the need to provide clinicians with fast, secure access to EHR systems from anywhere in the facility.

Thin Client Market Growth Drivers:

- Cloud Virtualizations, Security Priorities, and the Economics of Centralised IT

The fundamental driver of thin client demand is the shift toward VDI and cloud-hosted desktop environments. When a company moves its desktop workloads to a centralised server or cloud platform, the logic of maintaining expensive, locally-powerful endpoint hardware weakens considerably. A thin client that can render a VDI session reliably, boot quickly, and stay secure without local data storage does the job at a fraction of the capital and maintenance cost. IT departments can push software updates, security patches, and configuration changes from a single console rather than touching hundreds or thousands of individual machines. For large organisations with distributed workforces, that operational simplification has real dollar value.

Thin Client Market Restraints:

- Network Dependency, Legacy Compatibility, and Performance Ceilings

The single biggest practical objection to thin client deployment is network dependency. A thin client is only as good as its connection to the server or cloud infrastructure behind it — latency, packet loss, or downtime at the network or server level translates immediately into degraded user experience. For organisations in locations with unreliable connectivity, or for use cases that require offline capability, this is a genuine disqualifying factor rather than a minor inconvenience.

Thin Client Market Opportunities:

- Edge Computing, 5G Connectivity, DaaS Models, and Emerging Market Digitisation

Edge computing represents one of the more interesting structural opportunities for thin client vendors. As processing migrates closer to where data is generated factory floors, retail locations, logistics hubs there is demand for compact, rugged, low-maintenance endpoint devices that can connect to local edge nodes without requiring full desktop computing capability. Thin clients fit that description reasonably well, and vendors who develop edge-optimised form factors stand to capture meaningful share as edge deployment scales. 5G is a related enabler faster, lower-latency mobile connectivity reduces one of the historically valid objections to thin clients in mobile and field use cases. As 5G coverage expands, the performance case for mobile thin clients in sectors like field services, logistics, and healthcare becomes more compelling. BYOD and DaaS model adoption also opens the market to mid-market customers who have historically been excluded by upfront capital requirements.

Thin Client Market Segment:

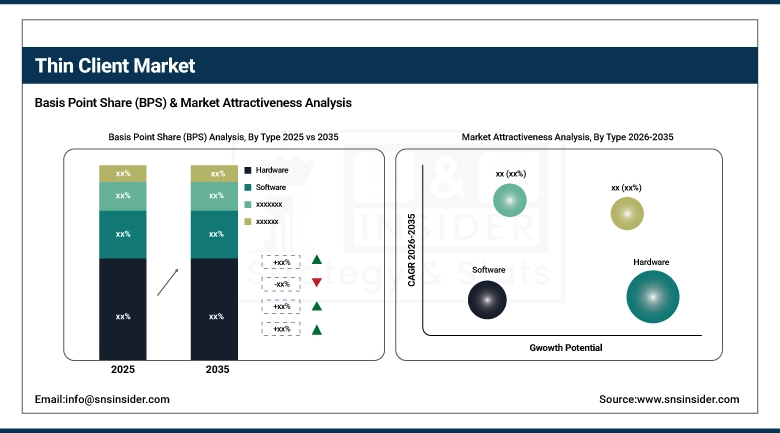

- By Type: In 2025, hardware dominated with 39.5% share; the services segment is expected to witness the highest CAGR during 2026–2035.

- By Form Factor: In 2025, standalone thin clients led with 48.7% share; the mobile segment is projected to register the fastest growth during 2026–2035.

- By Application: In 2025, education led with 24.5% share; the healthcare segment is expected to experience the fastest CAGR during 2026–2035.

By Type: Hardware Leads with 39.5% Share; Services Segment to Grow Fastest

Hardware held the largest share of the thin client market in 2025 at 39.5%, which is straightforward to explain: the physical device is the entry point for any thin client deployment, and enterprises across BFSI, healthcare, and government have been actively refreshing legacy desktop infrastructure with thin client hardware as their VDI deployments have matured. The services segment is forecast to grow at the highest CAGR through 2035, and that trajectory reflects how the market is maturing. As hardware deployment has become more standardised, the value conversation is shifting toward managed services, cloud integration, endpoint security management, and DaaS models that bundle hardware, software, and support into subscription contracts.

By Form Factor: Standalone Clients Dominate at 48.7%; Mobile Segment Grows Fastest

Standalone thin clients held 48.7% market share in 2025 and remain the dominant form factor for good reasons. Corporate offices, contact centres, educational institutions, and government agencies all have large numbers of fixed workstations that need to be managed centrally, and the standalone form factor essentially a small box that sits on or under a desk and connects to a monitor is the most cost-effective way to deliver that. It is easy to deploy, easy to replace, and compatible with virtually any monitor or peripheral setup. Mobile thin clients are growing fastest, driven by the structural shift toward hybrid and remote work that has reshaped enterprise computing since 2020. Employees who move between office, home, and client sites need portable devices that can securely access enterprise VDI environments from any network.

By Application: Education Leads at 24.5% Share; Healthcare to Experience Rapid Growth

The education sector's 24.5% market share in 2025 reflects a decade of investment in centralised computing for schools and universities. The argument for thin clients in education is compelling: a school district or university system can manage hundreds or thousands of endpoints from a central IT team, push curriculum software updates instantly, maintain consistent security configurations across all devices, and achieve meaningful cost savings compared with maintaining a conventional PC fleet. Healthcare is the fastest-growing application segment, and the dynamics are not hard to understand. Hospitals and health systems are under sustained pressure on two fronts simultaneously: data security and operational efficiency. HIPAA compliance requires strict controls over how patient data is stored and accessed; thin clients, which hold no local data, are a natural fit for that requirement.

Thin Client Market – Regional Analysis:

North America Thin Client Market Insights:

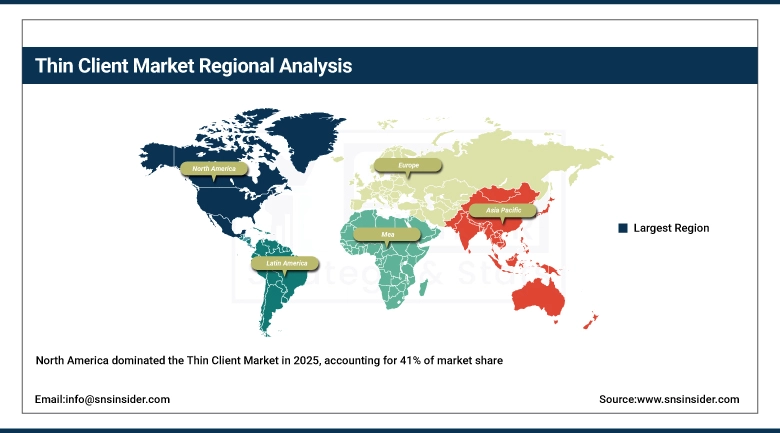

North America held an estimated 41% of the global thin client market in 2025, a leadership position built on decades of enterprise IT investment and a regulatory environment that consistently pushes organisations toward more secure, centrally managed computing architectures. The U.S. drives the region its mature VDI market, strong DaaS adoption, and high IT spending per employee create a durable base for thin client demand. BFSI and healthcare are the most active verticals in North America: banks and financial services firms have been standardizing on thin client infrastructure for branch and back-office operations for years, while hospitals are in the middle of a broad shift toward centralised IT that is driving endpoint refresh activity. Canada follows a broadly similar pattern at smaller scale, with public sector digitization programmes adding government as a meaningful demand category.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Thin Client Market Insights:

Asia-Pacific is the fastest-growing region, projected to expand at a CAGR of 11.4% from 2025 to 2035 a rate that reflects the scale of digital transformation investment happening across the region. China is the largest individual market within APAC: government digitisation programmes, education modernisation, and enterprise VDI adoption are all contributing to strong thin client demand. State-backed initiatives to replace imported computing infrastructure with domestically manufactured alternatives are also creating tailwinds for local thin client vendors. India is a growing market, with both the public and private sectors investing in cloud-based IT infrastructure that creates natural demand for centrally managed endpoints. Southeast Asian markets particularly Vietnam and Singapore — are seeing increased thin client adoption as their BFSI and healthcare sectors modernise.

Europe Thin Client Market Insights:

Europe shows steady growth underpinned by two consistent forces: GDPR compliance requirements and the ongoing modernisation of enterprise IT infrastructure in both Western and Eastern European markets. GDPR has made data residency and endpoint security a boardroom-level concern for European companies, and thin clients' architecture no local data storage, centralised management aligns well with what compliance officers want from an endpoint. Germany leads the European market, driven by its large industrial and enterprise base, high IT spending, and strong public sector digitalisation programmes. The UK, France, and the Benelux countries follow with established thin client deployments in BFSI and healthcare. Eastern European markets are earlier-stage but growing as EU digital infrastructure programmes channel investment into government and public institution IT modernisation.

Middle East & Africa and Latin America Thin Client Market Insights:

Both regions are at earlier stages of thin client adoption than the major markets but are growing from that base. In the Middle East, the UAE and Saudi Arabia are the primary markets, where smart city projects, government cloud initiatives, and financial sector modernisation are creating deployment opportunities. Saudi Arabia's Vision 2030 programme explicitly targets digital transformation in government and education, both of which are natural thin client use cases. In Latin America, Brazil and Mexico lead, with BFSI and education driving most of the activity. The cost efficiency argument for thin clients lower upfront hardware cost, lower power consumption, longer device life resonates particularly well in markets where IT budgets are constrained and total cost of ownership is scrutinised closely.

Thin Client Market Competitive Landscape:

Dell Technologies is the largest thin client vendor globally, a position it has held since its acquisition of Wyse Technology in 2012. The Wyse product line gave Dell a purpose-built thin client hardware portfolio that it has since integrated with its broader enterprise IT services, cloud management tools, and VDI partnerships with VMware and Citrix. Dell's scale gives it advantages in distribution, enterprise account relationships, and the ability to bundle thin client hardware with adjacent products — servers, networking, storage, and managed services in ways that smaller competitors cannot easily replicate.

- In 2024: Dell Technologies launched its next-generation Wyse thin client series featuring enhanced security capabilities, improved cloud integration, and performance optimizations’ specifically targeted at enterprise VDI environments.

HP Inc. occupies the second position in the global thin client market, with a hardware portfolio spanning the HP t-series and Elite thin client lines. HP's approach has been to target enterprise customers with a combination of strong Windows and Linux OS support, tight VDI platform integration, and device management through its HP Anyware software platform. Its market presence is particularly strong in BFSI and healthcare, where its security-focused marketing resonates with buyers whose compliance requirements make endpoint security a priority rather than an afterthought.

- In 2024: HP unveiled its Elite series thin clients with enhanced dual-OS support for Windows and Linux environments, optimised specifically for hybrid work deployment patterns and high-density VDI configurations.

Lenovo Group Limited has been building its thin client position through the ThinkCentre Tiny series, which positions thin and ultra-small form factor devices as versatile endpoints for both virtualised and local computing scenarios. Lenovo's global manufacturing scale and strong enterprise relationships particularly in Asia-Pacific and Europe give it distribution advantages. Its DaaS programme has been gaining traction with customers looking for subscription-based endpoint procurement models that reduce upfront capital expenditure.

- In 2024: Lenovo expanded its ThinkCentre Tiny series with enhanced VDI compatibility, improved security features, and lighter form factor options specifically designed for enterprise remote work deployments.

IGEL Technology occupies a distinctive position in the market as a software-defined thin client vendor. Rather than selling hardware, IGEL sells its operating system — IGEL OS — which can be installed on a wide range of commodity hardware to turn it into a managed thin client endpoint. This approach gives customers flexibility to extend the life of existing hardware while gaining the centralised management and security benefits of a true thin client architecture. IGEL OS 12, released in 2024, represented a significant platform refresh that improved cloud connectivity, endpoint security capabilities, and support for modern VDI and DaaS services.

- In 2024: IGEL introduced IGEL OS 12, a next-generation thin client software platform with strengthened security architecture, expanded cloud service compatibility, and enhanced centralised endpoint management capabilities.

Thin Client Companies are:

-

HP Inc.

-

Lenovo Group Limited

-

IGEL Technology

-

10ZiG Technology

-

Samsung Electronics

-

Fujitsu Limited

-

Acer Inc.

-

VXL Instruments

-

Wyse Technology (Dell subsidiary)

-

Stratodesk

-

Atrust Computer Corporation

-

Chip PC Technologies

-

ClearCube Technology

-

Neoware (acquired by Acer)

-

Prostar Computer Inc.

-

Praim

-

LG Electronics

-

VIA Technologies

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.60 Billion |

| Market Size by 2035 | USD 2.15 Billion |

| CAGR | CAGR of 3.00% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hardware, Software, Services) • By Form Factor (Standalone, With Monitor, Mobile) • By Application (Healthcare, Retail, Education, BFSI, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dell Technologies, HP Inc., Lenovo Group Limited, IGEL Technology, NComputing, 10ZiG Technology, Samsung Electronics, Fujitsu Limited, Acer Inc., VXL Instruments, Wyse Technology (Dell subsidiary), Stratodesk, Atrust Computer Corporation, Chip PC Technologies, ClearCube Technology, Neoware (acquired by Acer), Prostar Computer Inc., Praim, LG Electronics, VIA Technologies. |

Frequently Asked Questions

North America dominated the Thin client Market in 2025.

The Hardware segment dominated the Thin client Market in 2025.

The major growth factor of the Thin Client Market is the rising adoption of cloud computing and virtualization technologies, driving demand for secure, cost-efficient, and centrally managed computing solutions.

Thin Client Market was valued at USD 1.60 Billion in 2025 and is expected to reach USD 2.15 Billion by 2035.

The Thin client Market is expected to grow at a CAGR of 3.00% during 2026-2035.

Get in Touch