Thermoelectric Module Market Report Scope & Overview:

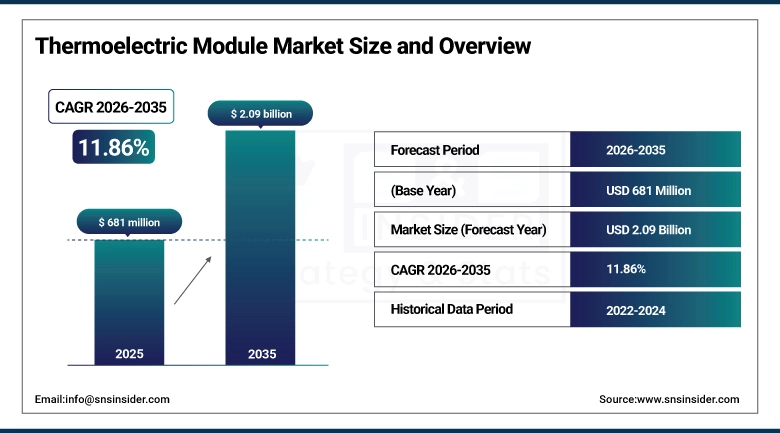

The Thermoelectric Module Market was valued at USD 681 million in 2025 and is expected to reach USD 2.09 billion by 2035, growing at a CAGR of 11.86% from 2026–2035.

A thermoelectric module refers to the device which produces electricity through temperature gradients or uses electrical energy for transferring heat without any moving components. They function very well in confined environments or areas prone to vibrations because they have a solid-state construction. Their applications have been increasing in consumer goods, electric cars, medical refrigeration, aerospace, and renewable energy sources because of the requirement for a quiet and compact cooling/heating system. Advancements in semiconductors materials such as bismuth telluride, silicon germanium and decreased costs of production have resulted in increased efficiency and facilitated novel applications. In the United States alone, their total revenue is projected to be worth about USD 597 million by 2035 as a result of their adoption of efficient thermoelectric modules in the automotive, medical, and military industries.

Thermoelectric Module Market Size and Forecast

-

Market Size in 2025: USD 681 Million

-

Market Size by 2035: USD 2.09 Billion

-

CAGR: 11.86% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Thermoelectric Module Market - Request Free Sample Report

Thermoelectric Module Market Trends

-

Rising miniaturisation of electronics pushing demand for small, silent, solid-state coolers in smartphones, wearables, and portable diagnostic instruments.

-

Accelerating EV adoption increasing per-vehicle content as battery thermal management and waste heat recovery emerge as key use cases.

-

Nano-engineered thin-film module breakthroughs documented in Nature Communications in 2025 pushing ZT values well above conventional bulk devices.

-

Growing uptake of thermoelectric generators in remote and off-grid settings where maintenance-free power from industrial waste heat has obvious value.

-

Smart city and IoT sensor networks expanding the addressable pool of low-power autonomous energy harvesting applications globally.

-

Aerospace and defense agencies investing in custom module designs for satellite thermal control, radar cooling, and soldier-worn electronics.

-

Collaborative government-industry R&D programmes in North America and Europe directing funding toward next-generation thermoelectric materials.

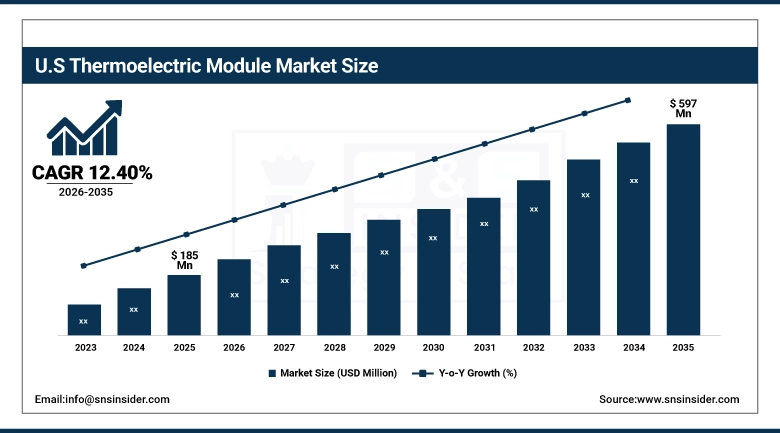

U.S. Thermoelectric Module Market was valued at USD 185 million in 2025 and is expected to reach USD 597 million by 2035 at a CAGR of 12.40%, driven by early adoption in automotive, aerospace, defense, and healthcare sectors and strong federal support for clean energy innovation.

Thermoelectric Module Market Segment Insights

-

Module Type-wise: Single Stage Modules are prevalent because of wide adaptability and seamless integration; Multi Stage Modules have been growing steadily on account of precision temperature control in aerospace industry, laser technology, and instrumentation devices.

-

Technology-wise: Bismuth Telluride accounted for the highest market share, around 72.6%, based on their efficiency at room temperatures and manufacturing process maturity; Silicon Germanium is the fastest growing technology based on high-temperature tolerance in automotive industry and outer space.

-

Functionality-wise: Cooling has the highest market share due to extensive utilization in consumer electronic devices and medical applications; Power generation is the fastest growing functionality type as initiatives towards waste heat recovery become more widespread.

-

Application-wise: Consumer Electronics dominated in 2025 with 28.83% share of the total market; Automotive was the fastest growing application segment due to rapid rise in EV production and requirement for thermal management systems in batteries.

Thermoelectric Module Market Segment Analysis

By Module Type: Single-Stage dominates, Multi-Stage grows fastest

Single-stage thermoelectric modules are the workhorse of the market, valued for their straightforward construction, cost-effective manufacture, and suitability across a wide temperature range that covers the vast majority of consumer, industrial, and medical cooling scenarios. Their compact footprint fits directly into circuit board designs, making them a natural choice as electronics shrink. Multi-stage modules stack two or more Peltier junctions to achieve temperature differentials impossible for a single stage. This capability is essential in laser diode cooling, DNA analysis instruments, and space-grade infrared detectors where precise, deep cooling determines system performance. Demand for multi-stage modules is accelerating rapidly as aerospace programmes and next-generation scientific platforms proliferate.

By Technology: Bismuth Telluride dominates, Silicon Germanium grows fastest

Bismuth telluride modules account for the overwhelming majority of commercial shipments because they operate most efficiently near room temperature, the range that matters most for cooling electronics and refrigeration. Their chemistry is well understood, manufacturing lines are mature, and a global supply chain ensures competitive pricing. Silicon germanium compounds are attracting intense R&D focus because they retain strong thermoelectric performance at temperatures above 600 degrees Celsius, making them the preferred choice for automotive exhaust heat recovery and space satellite power systems. As electric vehicles and spacecraft programmes grow, SiGe shipments are rising rapidly from a modest base, with performance gains from advanced doping and nanostructuring improving competitiveness further each year.

By Application: Consumer Electronics dominates, Automotive grows fastest

Consumer electronics sit at the top of the application table because the sheer volume of smartphones, wearables, portable refrigerators, and personal health monitors each demanding compact active cooling adds up to enormous aggregate demand. Automotive is the standout growth story. Electric vehicles now integrate thermoelectric modules for battery pack temperature control, seat-level heating and cooling, and exhaust waste heat recovery. As EV production lines scale globally and OEMs tighten energy efficiency standards, thermal management becomes a design priority rather than an afterthought, pulling demand for automotive-grade thermoelectric modules sharply higher.

Thermoelectric Module Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~80% |

|

Europe |

Germany |

~34% |

|

Asia Pacific |

China |

~48% |

|

Middle East & Africa |

UAE |

~27% |

|

Latin America |

Brazil |

~43% |

Asia Pacific Thermoelectric Module Market Insights

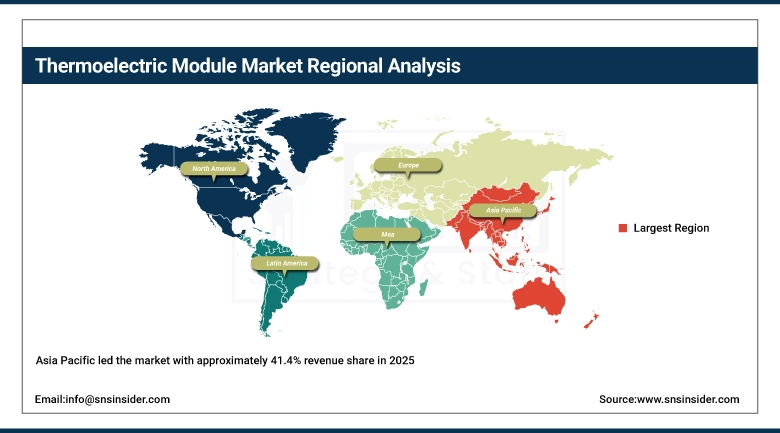

Asia Pacific led the market with approximately 41.4% revenue share in 2025. China, Japan, and South Korea drive volume through electronics manufacturing, while a dense supply chain for thermoelectric materials keeps regional producers’ cost-competitive globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Thermoelectric Module Market Insights

North America is forecast to register the highest regional CAGR of 12.4% through 2035, buoyed by strong EV programmes, federal clean energy incentives, and deep demand from defense and aerospace sectors where module reliability is non-negotiable.

Europe Thermoelectric Module Market Insights

The European market is moving at a steady pace, with automotive sustainability regulations and Europe's strong position in energy recovery from industries providing support. The German automotive and precision engineering industries account for the highest consumption within Europe.

Thermoelectric Module Market Growth Drivers:

-

Global push for energy efficiency and emission reduction making waste heat recovery a commercial priority across automotive, industrial, and power generation sectors.

Each thermoelectric generator generates electricity from energy which was previously lost as waste heat, without requiring any kind of fuel input, maintenance shutdowns, and even noise. In an era where governments impose stricter standards on carbon emissions, this solution appeals to both industrial power plants and automotive manufacturers, forming a stable demand chain independent of market fluctuations.

The Nature Communications report in 2025 regarding the fabrication of thin films of nanoscale thermoelectric materials with much greater ZT numbers compared to their solid counterparts is undoubtedly a significant event that bridges the gap between lab results and practical applications.

Thermoelectric Module Market Restraints

-

Relatively low coefficient of performance compared to conventional vapour-compression refrigeration limits adoption in high-load cooling applications where energy costs dominate.

For applications requiring significant cooling capacity, compressor-based systems remain far more energy-efficient per unit of heat moved. Thermoelectric modules occupy a strong niche where size, noise, vibration, and maintenance matter more than raw efficiency, but this does constrain addressable market volume outside those specific conditions.

Thermoelectric Module Market Opportunities

-

Advanced material research and wearable health-monitoring devices opening new revenue streams for thin, flexible thermoelectric modules.

Flexible and thin-film thermoelectric modules suitable for wearable skin temperature regulation and on-body energy harvesting represent an emerging product category with few incumbent competitors and a large addressable base in consumer health and sports performance markets. Simultaneously, continued doping and nanostructuring advances in bismuth telluride and skutterudite materials promise meaningful efficiency gains that would expand the range of applications where thermoelectric modules become cost-competitive with conventional systems.

Recent Developments:

-

2024: Ferrotec Corporation released an advanced line of multi-stage modules suitable for use in aerospace and military sectors due to high reliability at wide temperature range cycling.

-

2024: Laird Thermal Systems started production of low profile micro-modules aimed primarily at wearable and portable healthcare device market applications with restricted space on circuit boards.

Thermoelectric Module Market Key Players

-

Ferrotec Holdings Corporation

-

Laird Thermal Systems

-

II-VI Marlow (Coherent)

-

KELK Ltd.

-

TEC Microsystems GmbH

-

Crystal Ltd.

-

RMT Ltd.

-

Guangdong Fuxin Technology Co. Ltd.

-

CUI Devices

-

Kryotherm Industries

-

Phononic Inc.

-

Merit Technology Group

-

TE Technology Inc.

-

Thermonamic Electronics (Jiangxi) Corp. Ltd.

-

Z-MAX Co. Ltd.

-

Micropelt GmbH

-

Yamaha Corporation

-

Kyocera Corporation

-

Gentherm Incorporated

-

Alphabet Energy Inc.

Thermoelectric Module Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 681 Million |

| Market Size by 2035 | USD 2.09 Billion |

| CAGR | CAGR of 11.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Module Type (Single-Stage, Multi-Stage, Micro Modules, Others) • By Technology (Bismuth Telluride, Silicon Germanium, Lead Telluride, Others) • By Functionality (Cooling, Heating, Power Generation) • By Application (Consumer Electronics, Automotive, Aerospace and Defense, Medical Devices, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Ferrotec Holdings Corporation, Laird Thermal Systems, II-VI Marlow (Coherent) KELK Ltd., TEC Microsystems GmbH, Crystal Ltd., RMT Ltd., Guangdong Fuxin, Technology Co. Ltd., CUI Devices,Kryotherm Industries, Phononic Inc., Merit Technology Group, TE Technology Inc., Thermonamic Electronics (Jiangxi) Corp. Ltd., Z-MAX Co. Ltd., Micropelt GmbH, Yamaha Corporation, Kyocera Corporation, Gentherm Incorporated, Alphabet Energy Inc. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Thermoelectric Module Market in 2025 with approximately 41.4% of revenues, anchored by China, Japan, and South Korea through high-volume electronics manufacturing and a well-established thermoelectric materials supply chain.

Ans: Automotive is the fastest-growing application, driven by surging EV production requiring battery thermal management, seat conditioning, and waste heat recovery systems that benefit directly from thermoelectric module technology.

Ans: Single-Stage Modules dominated the market in 2025 owing to their wide applicability, straightforward integration, and cost competitiveness across consumer electronics, medical devices, and industrial cooling applications globally.

Ans: The Thermoelectric Module Market was valued at USD 681 million in 2025.

Ans: The Thermoelectric Module Market is expected to grow at a CAGR of 11.86% from 2026 to 2035.

Get in Touch