Urea Cycle Disorder Market Report Scope & Overview:

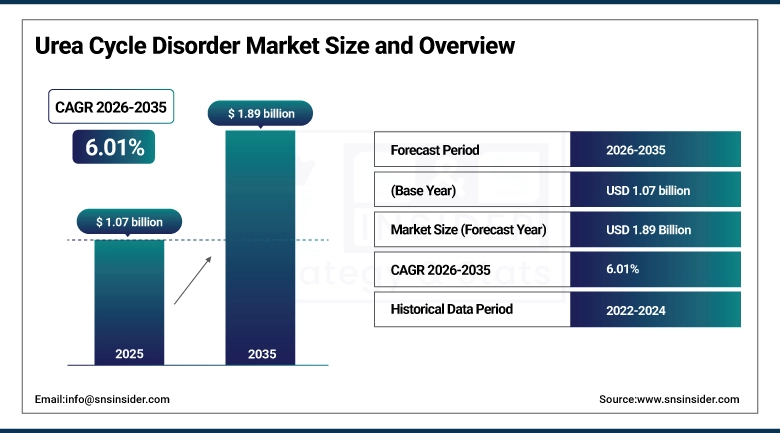

The Urea Cycle Disorder Market size is valued at USD 1.07 Billion in 2025 and is projected to reach USD 1.89 Billion by 2035, growing at a CAGR of 6.01% during the forecast period 2026–2035.

The Urea Cycle Disorder Market Analysis report presents an extensive assessment of market dynamics, therapeutic advancements, and treatment trends. The increasing number of cases of rare metabolic diseases, increased use of nitrogen scavengers, expanded newborn screening programs, and advances in gene therapy research are key factors driving steady growth in the market from 2026 to 2035.

Global prescriptions for Urea Cycle Disorder -related therapies exceeded 2.5 million annually in 2025, driven by improved diagnostic infrastructure, rising awareness among clinicians, and supportive rare disease policies.

Market Size and Forecast:

-

Market Size in 2025: USD 1.07 Billion

-

Market Size by 2035: USD 1.89 Billion

-

CAGR: 6.01% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Urea Cycle Disorder Market - Request Free Sample Report

Urea Cycle Disorder Market Trends:

-

Gene therapy and RNA-based treatments are emerging as transformative, curative options.

-

Nitrogen scavenger drugs remain the dominant therapy, supported by amino acid supplements.

-

Expansion of newborn screening programs is improving early diagnosis and treatment initiation.

-

Hospitals and specialty clinics continue to dominate end-user adoption, especially for acute care.

-

Specialty pharmacies hold the largest distribution share, but online pharmacies are growing rapidly.

-

Dietary management with medical foods remains essential as supportive therapy.

-

High treatment costs and limited patient access in developing regions remain key challenges.

-

Increasing clinical trials and R&D investments are accelerating innovation in rare disease therapeutics.

U.S. Urea Cycle Disorder Market Insights:

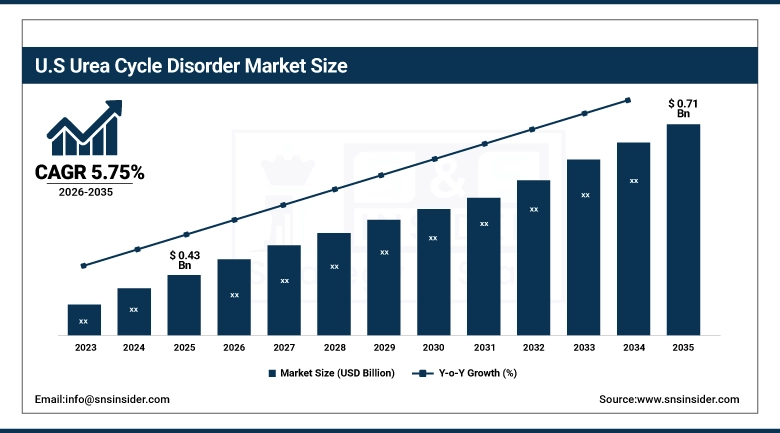

The U.S. Urea Cycle Disorder Market is projected to grow from USD 0.43 Billion in 2025 to USD 0.71 Billion by 2035, at a CAGR of 5.75%. The growth is being fuelled by the increasing prevalence of rare metabolic disorders, expansion in the use of newborn screening, strong acceptance of nitrogen scavenger and amino acid supplementation drugs, and rapid advancements in novel therapeutic modalities including gene therapy, RNA, and enzyme replacement.

Urea Cycle Disorder Market Growth Drivers:

-

Rising prevalence of rare genetic metabolic disorders and increasing newborn screening programs driving demand for early diagnosis and treatment of Urea Cycle Disorders.

Increasing incidences of urea cycle disorders, coupled with greater understanding about the presence of congenital metabolic disorders, is driving growth within the UCD market. There is an increasing trend of hospitals, specialized treatment centers, and neonatal units utilizing more sophisticated forms of testing and treatment, including the use of nitrogen scavengers, amino acid therapy, and newer genetic treatments, for the effective management of ammonia poisoning and avoiding severe consequences associated with such conditions.

Above 60% of specialized metabolic disorder treatment centers are increasingly adopting advanced UCD management protocols, supported by improved diagnostic infrastructure, genetic counseling services, and multidisciplinary care approaches.

Urea Cycle Disorder Market Restraints:

-

High cost of advanced orphan drugs and limited accessibility of gene-based therapies restraining widespread adoption of Urea Cycle Disorder treatments.

The high cost of treatment from nitrogen scavenger medication, therapeutic medical food products, and new gene therapy is one of the major factors that restrain the growth of the UCD market. Reimbursement issues in a few emerging nations and scarcity of this ailment are other hurdles for commercialization on a larger scale. Furthermore, the need for continuous care throughout life adds to the financial burden, thus restricting its accessibility in poor nations.

More than 55% of Urea Cycle Disorder treatment programs globally are constrained by high therapy costs, limited reimbursement coverage, and restricted access to advanced orphan drugs, limiting widespread adoption across emerging healthcare systems.

Urea Cycle Disorder Market Opportunities:

-

Rapid advancements in gene therapy, enzyme replacement technologies, and personalized medicine creating significant growth opportunities in the Urea Cycle Disorder market.

Growing development of next-generation gene editing platforms, mRNA-based therapies, and enzyme replacement solutions presents strong opportunities for long-term and potentially curative treatment of UCD. Pharmaceutical companies focusing on precision medicine and targeted metabolic correction are expected to benefit from increasing regulatory support for orphan drug development. Improvements in genetic diagnostics, biomarker identification, and personalized treatment approaches are further enabling early intervention and expanding the addressable patient pool, supporting sustained market expansion.

Over 50% of rare disease research initiatives are increasingly focusing on gene therapy, enzyme replacement, and personalized medicine approaches for Urea Cycle Disorders, creating significant opportunities for curative and next-generation treatment development.

Urea Cycle Disorder Market Segmentation Analysis:

-

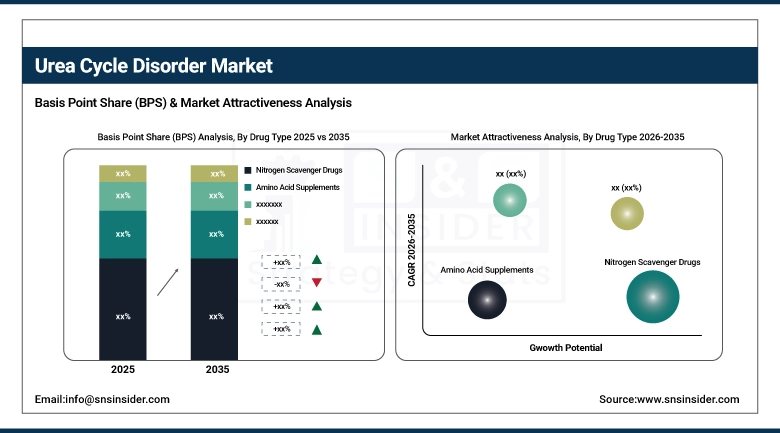

By Drug Type, Nitrogen Scavenger Drugs held the largest market share of 52.45% in 2025, while Emerging / Pipeline Therapies are expected to grow at the fastest CAGR of 8.12% during 2026–2035.

-

By End User, Hospitals held the largest share of 45.23% in 2025, while Homecare Settings are expected to grow at the fastest CAGR of 7.39% during the forecast period.

-

By Distribution Channel, Hospital Pharmacies dominated with 50.33% market share in 2025, whereas Online Pharmacies are projected to record the fastest CAGR of 7.87% through 2026–2035.

-

By Treatment Type, Pharmacological Therapy accounted for the highest market share of 55.47% in 2025, while Gene Therapy are expected to grow at the fastest CAGR of 8.07% during the forecast period.

By Drug Type, Nitrogen Scavenger Drugs Dominate While Emerging / Pipeline Therapies Grow Rapidly:

Nitrogen Scavenger Drugs was the most dominating segment in the global market owing to their proven track record as first line treatments for managing ammonia levels in patients with Urea Cycle Disorder. The popularity of such drugs is primarily attributed to the fact that they are highly effective in preventing hyperammonaemia and minimizing life-threatening conditions associated with it.

Emerged / Pipeline Therapies was the fastest growing segment owing to the latest developments in gene therapy, enzyme replacement, and precision medication. Major players in the pharmaceutical industry are focusing on developing novel therapies to target the primary reason behind Urea Cycle Disorders.

By End User, Hospitals Dominate While Homecare Settings Grow Rapidly:

Hospitals segment dominated the market due to their central role in diagnosis, acute care management, and long-term monitoring of Urea Cycle Disorder patients. Hospitals remain the primary treatment hub for managing severe hyperammonemia episodes, initiating nitrogen scavenger therapy, and providing multidisciplinary care involving metabolic specialists, genetic counselors, and critical care teams.

Homecare Settings are the fastest-growing segment, driven by increasing preference for long-term disease management outside hospital environments. Growing adoption of oral nitrogen scavenger drugs, improved patient monitoring tools, and rising awareness of chronic disease self-management are enabling patients to receive ongoing care at home.

By Distribution Channel, Hospital Pharmacies Dominate While Online Pharmacies Grow Rapidly:

Hospital Pharmacies held the highest share due to better integration with inpatient services and immediate access to life-saving UCD drugs. Hospital Pharmacies are responsible for dispensing scavengers and other emergency medicines that are crucial for treating metabolic disorders.

The Online Pharmacies segment is witnessing the fastest growth, fueled by growing adoption of digital health solutions and better availability of rare disease medications. Increasing use of e-prescription, convenience of doorstep delivery, and expanding online pharmacies are driving the trend.

By Treatment Type, Pharmacological Therapy Dominates While Gene Therapy Grows Rapidly:

The Pharmacological Therapy segment held a strong position within the market owing to the involvement of this treatment in maintaining the ammonia concentration in patients suffering from Urea Cycle Disorder. Nitrogen scavengers, amino acid replacement therapy, and diet are some commonly used treatments within the segment.

Gene Therapy is the fastest growing segment due to the rise in research on the curative methods of treatment for metabolic disorders. Innovations in the field of gene editing technology and viral vectors have helped achieve success in developing therapies for genetic diseases.

Urea Cycle Disorder Market Regional Analysis:

North America Urea Cycle Disorder Market Insights:

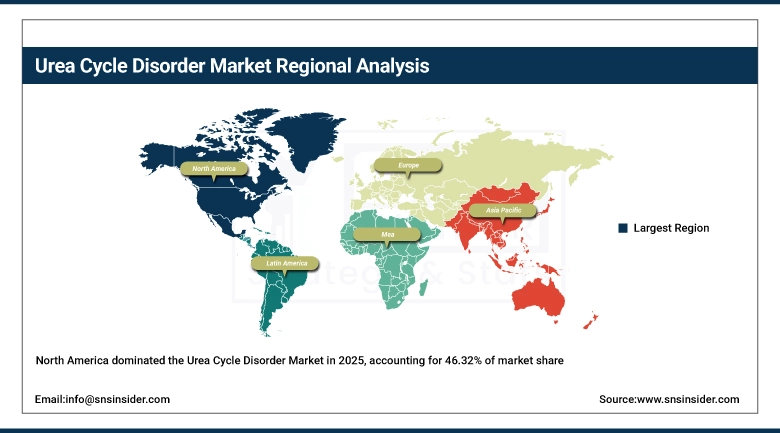

North America has a dominant presence in the UCD market, accounting for almost 46.32% of its global market share in 2025. This growth is backed by a superior healthcare system, funding for rare diseases, and the use of nitrogen scavenger medications and amino acids. The treatment is primarily provided in hospitals and specialized medical centers, with specialty pharmacies ensuring that treatments for rare diseases are accessible. The increasing trend of newborn screenings, skilled clinicians, and favorable reimbursement models have contributed to the dominance of North America in this market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Urea Cycle Disorder Market Insights:

The United States has the largest market share in North America for UCD treatment due to superior diagnostic facilities, high health expenditure, and increased use of pharmaceuticals. The key players in the United States are Horizon Therapeutics and Ultragenyx with their existing medicines and pipeline drugs. Increasing cases of rare metabolic diseases, growing number of specialty centers, and FDA orphan drug policies will drive market growth. Hospitals are leading in acute care, whereas specialty pharmacies are increasing market reach.

Asia-Pacific Urea Cycle Disorder Market Insights:

Asia-Pacific has the highest CAGR forecast of 7.44%. The growth will be spurred by increased awareness, improved health care facilities, and governmental policies towards the management of rare diseases. India and China will drive the growth due to increased newborn screening procedures and research in metabolic disorders. Specialty centers and hospitals are improving their services, whereas online pharmacies are making medicines available. While market share in terms of revenue is still low compared to North America and Europe, the Asia-Pacific region is likely to drive the future growth post-2030.

China Urea Cycle Disorder Market Insights:

China represents a key market in Asia-Pacific, bolstered by efforts on the part of the government in the area of rare disease care as well as newborn screening services. The growth in health care funding along with partnerships between China and international biotechnology organizations is facilitating rapid development of nitrogen scavenger drugs and amino acids. Treatment centers are mainly based in hospitals, although online drug stores are beginning to make their presence felt.

Europe Urea Cycle Disorder Market Insights:

EU continues to maintain the steady market share for UCD, driven by well-developed rare disease regulations and newborn screening systems. Germany, France, and UK are leading in terms of use of pharmacological treatment and dietary management. Hospitals and specialist clinics remain important channels of treatment, while specialist pharmacies play an important role in providing rare disease medicines. The pipelines in EU receive regulatory and financial support from the governments, even including gene therapy options. Growth may be moderate relative to APAC, but EU remains a mature market.

Germany Urea Cycle Disorder Market Insights:

Germany represents a major European market that has been fueled by a well-developed healthcare system, a number of projects dedicated to rare diseases, and wide application of nitrogen scavenger medication. Hospitals and specialty clinics have played an essential role in patient care owing to the level of professional training among practitioners and reimbursement schemes.

Latin America Urea Cycle Disorder Market Insights:

Latin America has a relatively new role within the UCD market around the world, but it continues to develop slowly due to the gradual uptake of rare disease treatments and development of the healthcare system. The two countries that are leading the way in Latin America include Brazil and Mexico, which have benefited from governmental campaigns and partnerships with foreign biotechnology companies.

Middle East & Africa Urea Cycle Disorder Market Insights:

The Middle East and Africa region have smaller contribution in Urea Cycle Disorder market, with growth restricted by inadequate diagnostic capabilities and availability of state-of-the-art treatments. Hospitals represent the largest market segment, while specialty centers and research institutions are increasingly contributing to the treatment process. Increased health care spending in the Gulf states and partnerships with overseas biotechnology companies have enhanced availability of nitrogen scavenger medications.

Urea Cycle Disorder Market Competitive Landscape:

Horizon Therapeutics

Horizon Therapeutics is a leading U.S. biopharmaceutical company with a dominant role in the UCD market, primarily through nitrogen scavenger drugs such as Ravicti (glycerol phenylbutyrate) and Buphenyl (sodium phenylbutyrate). The company emphasizes long-term disease management, focusing on reducing hyperammonemia and improving patient quality of life. Horizon’s strong supply chain, clinician partnerships, and rare disease advocacy reinforce its leadership. Horizon’s strong supply chain, clinician partnerships, and rare disease advocacy reinforce its leadership in this niche market.

-

In January 2025, Horizon expanded access to Ravicti in Europe through new reimbursement approvals, while advancing pipeline research into next-generation ammonia-lowering therapies.

Ultragenyx Pharmaceutical

Ultragenyx Pharmaceutical is a rare disease-focused biotech company with a growing presence in the UCD market. Its portfolio includes Dojolvi® (triheptanoin) for long-chain fatty acid oxidation disorders, and pipeline therapies targeting metabolic conditions including UCD. Ultragenyx emphasizes innovation in gene therapy and RNA-based treatments, aiming for curative solutions beyond symptomatic management. Ultragenyx leverages strong clinical trial capabilities and global collaborations to accelerate development and patient access.

-

In November 2025, Ultragenyx advanced clinical trials for UX701, a gene therapy candidate for ornithine transcarbamylase (OTC) deficiency, positioning itself as a leader in next-generation UCD therapies.

Acer Therapeutics

Acer Therapeutics is a U.S.-based biotech specializing in rare diseases, with a strong focus on UCD. Its key product is Olpruva™ (sodium phenylbutyrate oral suspension), designed to improve patient compliance compared to traditional formulations. Acer’s strategy centers on enhancing accessibility and patient-friendly formulations for chronic management of UCD. Acer is actively pursuing collaborations with healthcare providers and patient advocacy groups to expand awareness and improve treatment adoption across North America and Europe.

-

In September 2025, Acer Therapeutics announced expanded commercialization of Olpruva in North America, alongside ongoing development of pipeline therapies for metabolic disorders.

Urea Cycle Disorder Market Key Players:

Some of the Urea Cycle Disorder Market Companies are:

-

Horizon Therapeutics

-

Ultragenyx Pharmaceutical

-

Acer Therapeutics

-

Recordati Rare Diseases

-

Bausch Health Companies

-

Eurocept Pharmaceuticals Holding

-

Dimension Therapeutics

-

Callitas Therapeutics

-

Poseida Therapeutics

-

Promethera Biosciences

-

Arcturus Therapeutics

-

Kaleido Biosciences

-

Akaza Biopharma

-

Evox Therapeutics

-

Dipharma SA

-

Sana Biotechnology

-

Aeglea BioTherapeutics

-

Erytech Pharma

-

Synlogic Therapeutics

-

Orphan Pacific

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.07 Billion |

| Market Size by 2035 | USD 1.89 Billion |

| CAGR | CAGR of 6.01% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Type (Nitrogen Scavenger Drugs, Amino Acid Supplements (Arginine, Citrulline), Ammonia Detox Agents, Emerging/Pipeline Therapies, Others), • By End User (Hospitals, Specialty Clinics, Homecare Settings, Research Institutes, Others), • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Specialty Pharmacies, Online Pharmacies, Others), • By Treatment Type (Pharmacological Therapy, Dietary Management (Medical Foods), Gene Therapy, Liver Transplantation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Horizon Therapeutics, Ultragenyx Pharmaceutical, Acer Therapeutics, Recordati Rare Diseases, Bausch Health Companies, Eurocept Pharmaceuticals Holding, Dimension Therapeutics, Callitas Therapeutics, Poseida Therapeutics, Promethera Biosciences, Arcturus Therapeutics, Kaleido Biosciences, Akaza Biopharma, Evox Therapeutics, Dipharma SA, Sana Biotechnology, Aeglea BioTherapeutics, Erytech Pharma, Synlogic Therapeutics, Orphan Pacific. |

Frequently Asked Questions

North America dominated with a 46.32% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 7.44% during 2026–2035.

Nitrogen Scavenger Drugs dominated with a 52.45% share in 2025, while Emerging / Pipeline Therapies are projected to grow at the fastest CAGR of 8.12% during 2026–2035.

Growth is driven by the rising prevalence of rare metabolic disorders, expanding newborn screening programs, and strong adoption of nitrogen scavenger drugs and amino acid supplements.

The market is valued at USD 1.07 Billion in 2025 and is projected to reach USD 1.89 Billion by 2035.

The Urea Cycle Disorder Market is projected to grow at a CAGR of 6.01% during 2026–2035.

Get in Touch