UV LED Market Report Scope & Overview:

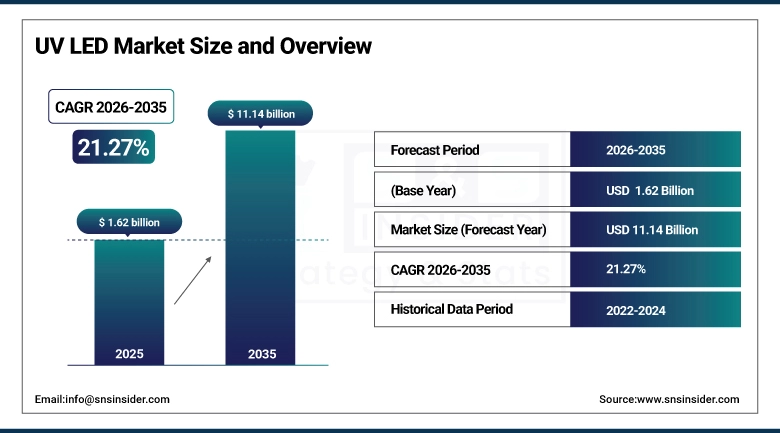

The UV LED Market was valued at USD 1.62 billion in 2025 and is expected to reach USD 11.14 billion by 2035, growing at a CAGR of 21.27% from 2026-2035.

UV LEDs have crossed the threshold from specialized research tool to commercially indispensable technology across a surprisingly wide range of industries in a relatively short time. The push has come from multiple directions at once: mercury regulations forcing a rethink of conventional UV lamp technology, the pandemic amplifying demand for non-chemical disinfection in public spaces and healthcare settings, and industrial curing applications finding that UV LEDs offer process economics that mercury lamps simply cannot match. What makes the growth trajectory so durable is that the technology keeps getting better in ways that open new applications.

The U.S. EPA's ongoing phase-out of mercury-containing UV lamps under RCRA hazardous waste regulations and alignment with the Minamata Convention on Mercury directly supports UV LED adoption. The EPA's 2023 designation of mercury lamps as hazardous waste accelerates replacement cycles globally.

UV LED Market Size and Forecast

-

Market Size in 2025: USD 1.62 Billion

-

Market Size by 2035: USD 11.14 Billion

-

CAGR: 21.27% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on UV LED Market - Request Free Sample Report

UV LED Market Trends

-

AlGaN deep UV LED quantum efficiency improvements are steadily narrowing the cost-per-photon gap with legacy mercury lamp technology, expanding the economically viable application range.

-

UV-C LED point-of-use water purifiers are gaining consumer market traction in Asia Pacific and the Middle East where water quality concerns intersect with growing purchasing power.

-

Food and beverage manufacturers are replacing chemical sanitizers with UV LED conveyor disinfection systems to eliminate chemical residues and comply with clean-label product requirements.

-

3D printing with UV-curable photopolymer resins is growing rapidly and creating a new demand stream for high-power UV LED curing modules in additive manufacturing equipment.

-

Roll-to-roll UV LED curing systems for flexible electronics and film coating are displacing UV mercury lamp systems in display manufacturing lines across Asia Pacific factories.

-

GaN-on-Si substrate technology is beginning to reduce UV LED epitaxial wafer costs, which should translate into lower device prices and broader market penetration over the forecast horizon.

-

Healthcare is exploring low-dose UV-A LED phototherapy for skin conditions including psoriasis and vitiligo as a home-use alternative to clinic-based treatment protocols.

U.S. UV LED Market Size Outlook:

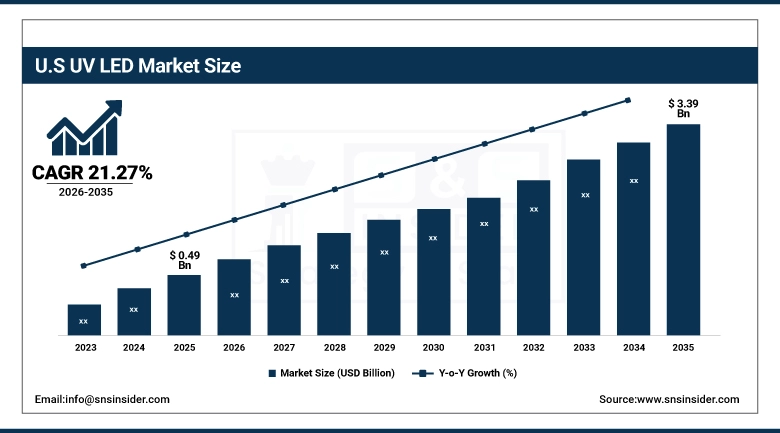

The U.S. UV LED Market was valued at USD 0.49 billion in 2025 and is expected to reach USD 3.39 billion by 2035, growing at a CAGR of 21.27% from 2026-2035. The U.S. is one of the most technically sophisticated UV LED markets in the world, though its growth rate is being outpaced by Asia Pacific on a volume basis. What distinguishes the U.S. market is the concentration of high-value application segments: specialty UV curing for printed electronics and medical device coatings, HVAC air disinfection integration in commercial building upgrades, and advanced water purification systems for municipalities facing PFAS and pathogen compliance challenges.

The U.S. Department of Defense contracted multiple UV-C LED technology development programs through DARPA and DoD SBIR grants to create deployable water disinfection and surface decontamination systems. The FDA has cleared several UV LED phototherapy devices for eczema and psoriasis home treatment.

UV LED Market Segment Analysis

-

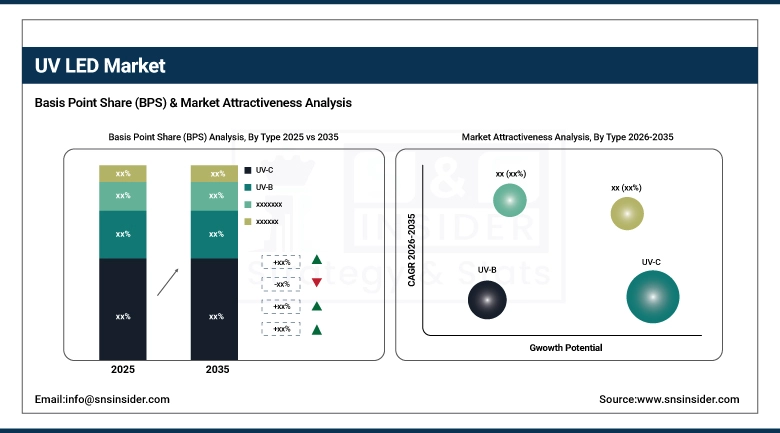

By Type, UV-C segment dominated the UV LED Market in 2025; UV-A segment fastest growing (CAGR) driven by phototherapy and counterfeit detection demand.

-

By Power Output, Below 1W segment dominated the UV LED Market in 2025; More Than 5W segment fastest growing (CAGR) for industrial and large-scale disinfection.

-

By Application, UV Curing segment dominated the UV LED Market in 2025; Disinfection & Sterilization segment fastest growing (CAGR).

-

By End Use, Industrial segment dominated the UV LED Market in 2025; Healthcare segment fastest growing (CAGR).

By Type, UV-C segment dominates the UV LED Market, UV-A segment expected to grow fastest

UV-C LEDs commanding the largest revenue share reflects where the largest commercial investments have landed: disinfection and sterilization applications in healthcare, water treatment, and food safety. UV-C wavelengths between 250 and 280 nanometers are lethal to bacteria, viruses, and other pathogens at achievable exposure doses, which makes them the functional workhorse of the disinfection market. The post-pandemic expansion of institutional air and surface disinfection programs has generated sustained procurement demand for UV-C LED modules and systems. Water utility operators are deploying UV-C LED reactors as a chlorine-free primary disinfection technology that meets EPA disinfection byproduct regulations while delivering reliable pathogen log-reduction.

UV-A LEDs are the fastest-growing segment because the expanding range of applications tapping into 315-400 nanometer wavelengths is growing faster proportionally than the already-large UV-C disinfection market. UV-A LEDs drive the core of the industrial UV curing market coating, adhesive bonding, inkjet printing, and dental composite curing where their longer wavelengths penetrate deeper into photoinitiator-containing formulations. Beyond curing, UV-A is preferred for phototherapy applications including narrowband UVB and PUVA treatments for skin conditions because it causes less acute photochemical damage than UV-C while still achieving therapeutic outcomes. Forensic analysis, counterfeit document detection, and fluorescence-based sensing are additional UV-A application domains where the segment is expanding.

By Application, UV Curing segment dominates the UV LED Market, Disinfection & Sterilization segment expected to grow fastest

UV curing retained dominant application revenue share in 2025 and is grounded in the economics of industrial production rather than health trends. Manufacturers of electronics, optical components, dental devices, automotive components, and packaging materials all rely on UV-cured adhesives and coatings because the process is fast, energy-efficient, and produces films with excellent hardness and chemical resistance. UV LED curing systems specifically have taken share from conventional mercury lamp systems because they eliminate ozone generation, run cooler, turn on and off instantly without warm-up cycles, and last tens of thousands of hours longer than mercury lamps. For continuous production line applications where lamp downtime directly impacts throughput, those operational advantages outweigh the higher upfront equipment cost of UV LED systems.

Disinfection and Sterilization is the fastest-growing application segment and the most diverse in terms of end market. Hospital surface decontamination, drinking water purification, food processing line sanitation, HVAC air treatment, and personal care device sterilization are all drawing from this segment. The common thread is demand for chemical-free, residue-free inactivation of pathogens that conventional cleaning methods cannot reliably eliminate. Municipal water authorities in the U.S. and Europe are increasingly specifying UV-C LED reactors for primary or secondary disinfection because they generate no disinfection byproducts — an important compliance advantage as EPA and EU drinking water regulations tighten around trihalomethane and haloacetic acid formation that chlorination creates.

UV LED Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

50% |

|

North America |

United States |

88% |

|

Europe |

Germany |

27% |

|

Middle East & Africa |

Israel |

32% |

|

Latin America |

Brazil |

45% |

Asia Pacific UV LED Market Insights

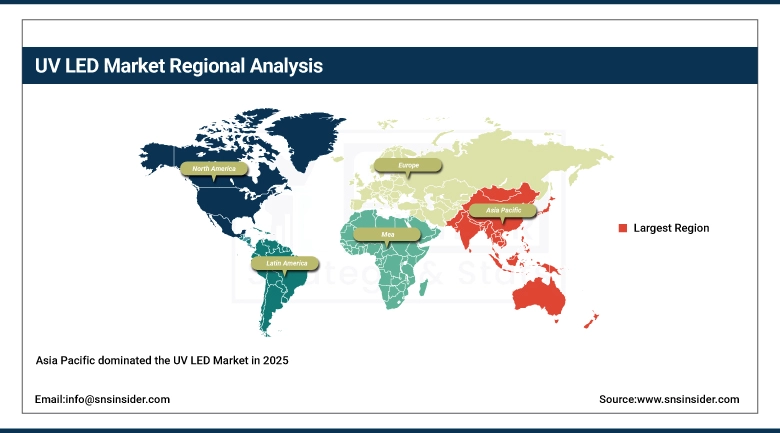

Asia Pacific dominated the UV LED Market in 2025, anchored by China's enormous semiconductor manufacturing ecosystem that drives both UV LED chip production and the most advanced UV curing application deployments in the world. Taiwan, South Korea, and Japan are home to leading UV LED epitaxial wafer producers and device manufacturers including Seoul Viosys, Nichia, and Stanley Electric whose production volumes set global market benchmarks. China's massive display panel and printed electronics industries are the largest single consumers of UV LED curing systems globally, while India's rapidly growing pharmaceutical and food processing sectors are beginning to generate meaningful disinfection application demand. Southeast Asia's growing electronics manufacturing base is adding incremental UV curing demand as production capacity shifts from China to Vietnam, Thailand, and Malaysia.

South Korea's Ministry of Trade, Industry and Energy designated UV LED as a strategic material technology under the K-Material Independence Initiative, directing R&D grants toward AlGaN deep UV LED quantum efficiency improvement. China's 14th Five-Year Plan specifically funds UV LED semiconductor manufacturing scale-up as part of domestic LED industry development.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America UV LED Market Insights

North America is expected to witness the fastest CAGR through 2035, reflecting the region's combination of strong healthcare application pull, active regulatory drivers favoring mercury-free UV technology, and significant R&D investment in next-generation UV LED performance. The U.S. water treatment market's progressive shift toward UV-C LED primary disinfection is a substantial demand driver, particularly in municipalities upgrading to avoid disinfection byproduct violations. The commercial HVAC sector's accelerating adoption of UV air disinfection following pandemic-driven indoor air quality awareness is another growing application domain. Canada's strong mining and pharmaceutical manufacturing sectors are adding UV LED sterilization demand from applications requiring reliable non-chemical contamination control in processing environments.

The U.S. EPA's WaterSense and Safe Drinking Water Act enforcement programs have accelerated municipal investment in advanced water treatment including UV disinfection. Over 400 U.S. water utilities upgraded to UV primary disinfection between 2020-2024 according to the American Water Works Association.

Europe UV LED Market Insights

Europe held approximately 20% of the global UV LED Market in 2025, with the German, Dutch, French, and Scandinavian markets contributing the largest shares through industrial UV curing, pharmaceutical sterilization, and specialty phototherapy applications. The EU's RoHS directive and alignment with the Minamata Convention on Mercury have created regulatory pressure that directly benefits UV LED suppliers as mercury lamp users seek compliant alternatives. European specialty printing and packaging companies are leading early adopters of UV LED curing systems particularly for heat-sensitive substrates including plastics and films that mercury lamp heat intensity damages and European precision optics and medical device manufacturers are expanding UV LED-cured adhesive bonding applications.

The EU Minamata Convention implementation and RoHS directive amendments restrict mercury-containing UV lamps across EU member states from 2025. The European Chemicals Agency (ECHA) has listed mercury compounds as substances of very high concern, directly accelerating UV LED adoption as a compliant replacement.

Middle East & Africa and Latin America UV LED Market Insights

The Middle East & Africa and Latin America regions represent growing UV LED markets where water treatment and food safety applications are the primary demand drivers. Israel is a notable MEA technology hub, with companies including Atlantium Technologies and Manzana Systems developing advanced UV LED water treatment systems. The UAE and Saudi Arabia's large-scale water desalination infrastructure is beginning to incorporate UV LED post-treatment disinfection at points of use. In Latin America, Brazil's food and beverage processing industry one of the largest globally is the primary UV LED adoption center, with growing use of UV-C LED conveyor disinfection and packaging sanitation systems as exporters target markets with stringent food safety requirements.

The Saudi National Water Company's water safety modernization program mandates UV disinfection at 150+ water distribution points. Brazil's ANVISA updated food production hygiene standards in 2024 now specifically recognize UV LED disinfection as an approved pathogen reduction method in food processing facilities.

Market Growth Drivers: Rising demand for mercury-free disinfection solutions and industrial curing applications accelerating global UV LED adoption

What is driving this market is not one big thing but several reinforcing forces that happen to all be pointing in the same direction at the same time. Mercury elimination is the regulatory tailwind: the Minamata Convention, EU RoHS updates, and U.S. EPA hazardous waste designations are collectively putting a sunset timeline on conventional UV mercury lamps across the most important markets. That regulatory force is pushing procurement decisions toward UV LEDs even before the performance argument fully closes the gap. At the same time, the post-pandemic institutional investment in air and surface disinfection has created a new and durable market for UV-C LED systems that did not exist at meaningful scale before 2020. Industrial UV curing is the third pillar it was the original commercial UV LED application and continues to grow as the installed base of UV LED curing systems expands and new industries discover the process benefits over conventional lamp-based alternatives.

The World Health Organization's WASH (Water, Sanitation and Hygiene) program has endorsed UV disinfection technology as a priority solution for safe water delivery in low-resource settings. WHO technical specifications for UV water treatment systems have influenced procurement in 80+ countries and now include UV LED-compatible performance criteria.

Market Restraints: High device cost and limited quantum efficiency slowing large-scale uptake of UV-C LED technology globally

UV-C LEDs face a fundamental materials challenge that is well understood but not yet fully solved: the external quantum efficiency of AlGaN-based deep UV emitters remains far below what silicon or conventional visible-wavelength GaN LEDs achieve. Getting from electrical input power to useful UV-C photons involves losses at multiple stages carrier injection, radiative recombination, light extraction through the crystal lattice and AlGaN material properties make each of those loss stages worse than the equivalent visible LED architecture. The result is that high-output UV-C LED modules cost substantially more per milliwatt of UV power delivered than comparable mercury lamp systems, which limits their adoption to applications where the operational advantages justify the premium. As long as quantum efficiency remains a constraint, cost reduction depends primarily on manufacturing scale rather than device physics progress, making the market growth rate somewhat self-limiting until a materials science breakthrough changes the efficiency equation.

Market Opportunities: Expanding water purification mandates and next-generation phototherapy applications unlocking new growth avenues for UV LED

Two of the most compelling growth opportunities in the UV LED market are converging around access to clean water and access to medical phototherapy both situations where UV LED's operational advantages over alternatives create genuine social value, not just commercial opportunity. On the water side, the regulatory tightening around drinking water contaminants in the U.S. and EU is forcing municipalities and point-of-use device manufacturers to invest in disinfection technology that UV LEDs can deliver cost-effectively at modest scales. On the medical side, home-use UV phototherapy devices cleared by the FDA represent an enormous potential market among the 125 million people globally who suffer from psoriasis, with UV LED enabling devices that are safe, controllable, and practical for daily home use. Both opportunities are at relatively early commercial stages, which means the growth runway through 2035 is long and still relatively uncontested.

Recent Developments:

-

2026: Seoul Viosys launched its enhanced Violeds UV-C LED module series with a reported 20% improvement in external quantum efficiency compared to previous generation devices, targeting point-of-use water purification and HVAC air disinfection applications where output power per watt of electricity consumed directly determines system operating cost and market competitiveness.

-

2025: Nichia Corporation unveiled a new UV-A LED series operating at 365nm and 385nm with improved flux output for industrial UV curing applications, specifically designed for high-speed inkjet printing and flexible electronics coating lines where processing speed directly determines production economics at scale.

-

2025: Crystal IS (Asahi Kasei) received NSF certification for its Klaran UV-C LED water disinfection products under NSF/ANSI Standard 55, marking the first UV LED system to earn this certification for residential point-of-use water treatment and creating a compliance pathway that is expected to accelerate adoption by U.S. water purifier manufacturers.

UV LED Companies are:

-

Seoul Viosys Co., Ltd. (Violeds)

-

Crystal IS, Inc. (Asahi Kasei)

-

Stanley Electric Co., Ltd

-

Bolb Inc

-

Nitride Semiconductors Co., Ltd

-

SETi (Sensor Electronic Technology, Inc.)

-

Honle UV America Inc

-

LG Innotek Co., Ltd

-

Epitop Optoelectronic Co., Ltd

-

DOWA Holdings Co., Ltd

-

Philips Lumileds Lighting Company

-

Osram Opto Semiconductors GmbH

-

Aquionics Inc. (Halma)

-

Ushio America Inc

-

BIO-UV Group

-

Atlantium Technologies

-

UV-C LED Systems GmbH

-

AMS Technologies AG

UV LED Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.62 Billion |

| Market Size by 2035 | USD 11.14 Billion |

| CAGR | CAGR of 21.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (UV-A, UV-B, UV-C) • By Power Output (Below 1W, 1W-5W, More Than 5W) • By Application (UV Curing, Disinfection & Sterilization, Medical Light Therapy, Counterfeit Detection, Horticulture, Others) • By End Use (Industrial, Healthcare, Agriculture, Consumer Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Seoul Viosys Co., Ltd. (Violeds), Nichia Corporation, Crystal IS, Inc. (Asahi Kasei), Stanley Electric Co., Ltd., Bolb Inc., Nitride Semiconductors Co., Ltd., SETi (Sensor Electronic Technology, Inc.), Lumex Inc., Honle UV America Inc., LG Innotek Co., Ltd., Epitop Optoelectronic Co., Ltd., DOWA Holdings Co., Ltd., Philips Lumileds Lighting Company, Osram Opto Semiconductors GmbH, Aquionics Inc. (Halma), Ushio America Inc., BIO-UV Group, Atlantium Technologies, UV-C LED Systems GmbH, and AMS Technologies AG. |

Frequently Asked Questions

Ans: Asia Pacific dominated the UV LED Market in 2025.

Ans: The Healthcare segment is expected to register the fastest CAGR in the UV LED Market.

Ans: The UV Curing segment dominated the UV LED Market in 2025

Ans: The UV LED Market was valued at USD 1.62 billion in 2025.

Ans: The UV LED Market is expected to grow at a CAGR of 21.27% from 2026 to 2035.

Get in Touch