Warfarin Sensitivity Test Market Report Scope & Overview:

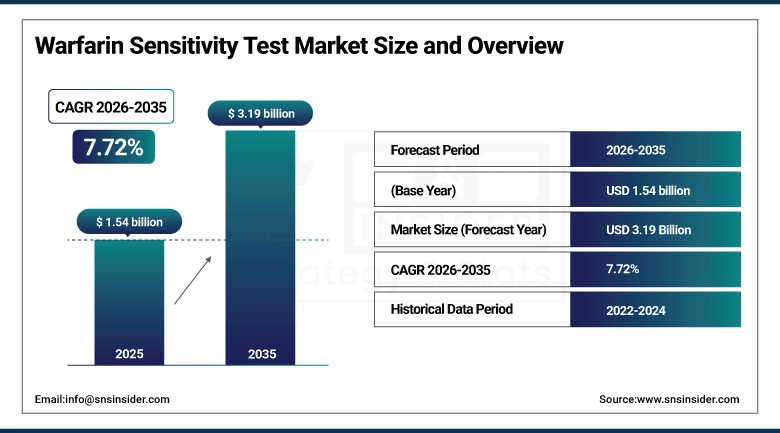

The Warfarin Sensitivity Test Market size is valued at USD 1.54 Billion in 2025 and is projected to reach USD 3.19 Billion by 2035, growing at a CAGR of 7.72% during the forecast period 2026–2035.

Market Insights for the Warfarin Sensitivity Test Market give detailed insights into innovations in pharmacogenomics, rising trends of precision medicine, and the increased use of genetic testing in healthcare settings. Some of the key drivers that will propel market growth include the rising incidence rate of heart diseases, the growing requirement for reducing unwanted reactions to drugs, heightened awareness regarding genotype-based dosing, and ongoing developments in molecular diagnostics.

The use of warfarin sensitivity testing across healthcare systems is expected to support Billions of anticoagulant therapy patients annually, with increasing adoption across hospitals, diagnostic laboratories, and specialized genetic testing centers in 2025.

Market Size and Forecast:

-

Market Size in 2025: USD 1.54 Billion

-

Market Size by 2035: USD 3.19 Billion

-

CAGR: 7.72% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Warfarin Sensitivity Test Market - Request Free Sample Report

Warfarin Sensitivity Test Market Trends:

-

Rising prevalence of cardiovascular diseases and increasing use of anticoagulant therapy are driving strong demand for warfarin sensitivity testing to improve patient safety and treatment outcomes.

-

Growing adoption of personalized medicine and pharmacogenomics is accelerating the use of genetic testing to enable genotype-guided dosing and reduce adverse drug reactions.

-

Increasing awareness among healthcare providers regarding variability in patient response to warfarin is boosting integration of genetic testing into clinical decision-making workflows.

-

Advancements in molecular diagnostics technologies, including PCR and next-generation sequencing, are enhancing accuracy, speed, and scalability of warfarin sensitivity testing.

-

Expanding use of multi-gene panel testing is gaining momentum as it improves dose prediction accuracy compared to single-gene testing approaches.

-

Rising implementation of clinical guidelines and regulatory support for pharmacogenomic testing is encouraging broader adoption across developed healthcare systems.

-

Growing integration of AI-driven decision support tools and digital health platforms is transforming anticoagulant management through real-time dose optimization and predictive analytics.

-

Increasing shift toward decentralized and point-of-care genetic testing is improving accessibility and turnaround time, particularly in hospital and diagnostic center settings.

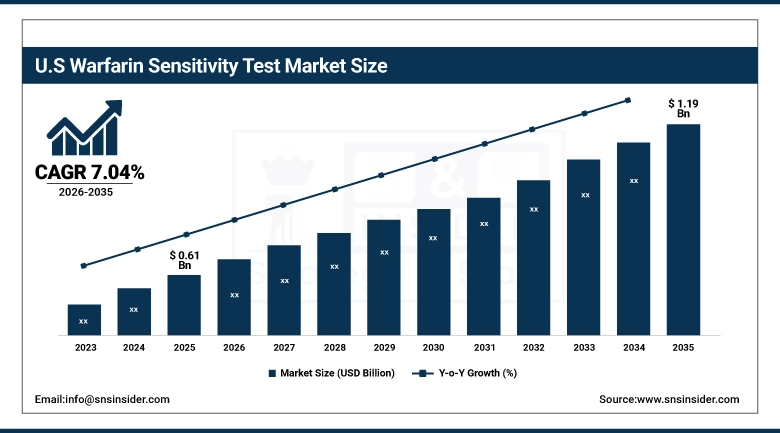

U.S. Warfarin Sensitivity Test Market Insights:

The Warfarin Sensitivity Test Market in the United States is projected to grow from USD 0.61 Billion in 2025 to USD 1.19 Billion by 2035, at a CAGR of 7.04%. The expansion in the market would be driven by an increased incidence of heart disease, higher use of pharmacogenomic tests, increased importance of personalized medicine, growing use of genotype-based drug dosage and the need to minimize adverse drug reactions and improve the outcome of anticoagulation therapy.

Warfarin Sensitivity Test Market Growth Drivers:

-

Rising prevalence of cardiovascular diseases and increasing use of anticoagulant therapies are driving strong demand for warfarin sensitivity testing to improve dosing accuracy and reduce adverse drug reactions.

The increasing use of personalized medicine and pharmacogenomics will greatly contribute to greater usage of genetics tests in the clinical practice. Healthcare providers are paying more attention to avoiding mistakes when prescribing drugs and protecting the patients, which leads to increased spending on new molecular diagnostics, such as PCR and next generation sequencing. Widespread clinical guidelines and reimbursement opportunities for genotype-based therapies are promoting the adoption of warfarin sensitivity tests.

Over 55% of advanced healthcare institutions are now incorporating or evaluating pharmacogenomic testing in anticoagulant management as of 2025.

Warfarin Sensitivity Test Market Restraints:

-

Continued reliance on conventional clinical dosing methods and limited awareness of pharmacogenomic testing are restraining the widespread adoption of warfarin sensitivity testing.

The Warfarin Sensitivity Testing Market is hampered by the continued reliance on conventional trial and error methodologies for warfarin dosage and the gradual inclusion of genetic testing in the clinical practice process. The high cost of genetic tests, the low levels of insurance cover, and the lack of established clinical guidelines in some geographical locations limit its implementation and widespread uptake. Competition posed by other anticoagulant drugs such as the DOACs further hinders the growth of this market.

Warfarin Sensitivity Test Market Opportunities:

-

Expanding integration of pharmacogenomics into mainstream healthcare systems is creating significant opportunities for warfarin sensitivity testing.

More focus on precision medicines and value-based healthcare approaches is resulting in a wider use of genetic testing for dosing in anticoagulation therapy. Healthcare professionals and testing manufacturers are actively working on developing scalable genomics tests, clinical decision support tools in the cloud environment, and EHRs to help make testing more accessible. In addition, partnerships among diagnostic test manufacturers, hospitals, and research centers are leading to faster creation of highly effective multigene tests and real-time dosing algorithms.

Over 50% of large healthcare networks are expected to integrate pharmacogenomic testing into routine clinical workflows by 2035, creating substantial long-term market expansion opportunities.

Warfarin Sensitivity Test Market Segmentation Analysis:

-

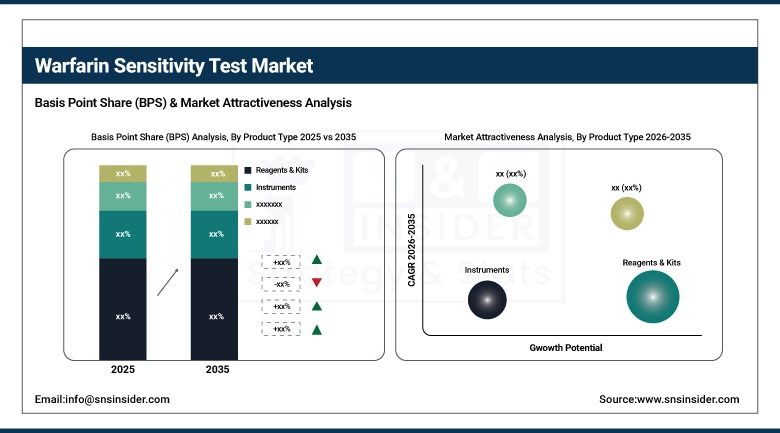

By Product Type, Reagents & Kits held the largest market share of 58.25% in 2025, while Software & Services is expected to grow at the fastest CAGR of 9.01% during 2026–2035.

-

By Technology, PCR-based Testing dominated with a 52.05% market share in 2025, while DNA Sequencing is projected to grow at the fastest CAGR of 8.96% during 2026–2035.

-

By Gene Type, CYP2C9 Testing held the largest share of 41.85% in 2025, while Combined Gene Testing is expected to grow at the fastest CAGR of 9.40% during 2026–2035.

-

By Application, Diagnostic Laboratories dominated with a 46.85% market share in 2025, while Hospitals are projected to grow at the fastest CAGR of 8.32% during 2026–2035.

-

By End-User, Hospitals & Clinics held the largest share of 49.30% in 2025, while Diagnostic Centers are expected to grow at the fastest CAGR of 8.60% during 2026–2035.

By Product Type, Reagents & Kits Dominate While Software & Services Grows Rapidly:

The Reagents & Kits sub-segment accounted for the largest share in the market. This is mainly attributed to its pivotal importance within the testing processes of warfarin sensitivity. The need for regular testing of warfarin sensitivity through the application of pharmacogenomic tests creates a sustained demand for the product.

Software & Services is the fastest-growing sub-segment within the market. The growing use of digital health technology, clinical decision-making systems, and laboratory information management systems has contributed immensely to the growth of this segment.

By Technology, PCR-based Testing Dominates While DNA Sequencing Grows Rapidly:

PCR-based Testing segment dominated the market one since it offered clinical accuracy and effectiveness with regard to costs, making it popular among diagnostic labs performing genetic tests. Accuracy of this technology in identifying gene variants including CYP2C9 and VKORC1 contributes significantly to its domination.

DNA Sequencing is currently the fastest-growing market segment due to the rising need for highly accurate and multi-gene testing. This is mainly due to the growing trend toward personalized medicine, and the development of next-generation DNA sequencing technologies.

By Gene Type, CYP2C9 Testing Dominates While Combined Gene Testing Grows Rapidly:

CYP2C9 Testing segment dominated the market due to its importance in the warfarin metabolization prediction process. It enjoys a significant share in the market owing to its highly validated clinical application in the development of dosing optimization strategies.

Combined Gene Testing is the fastest-growing segment, as there is an increasing trend toward comprehensive gene analysis for the determination of effective dose and prevention of side effects. The growing adoption of clinical guidelines for pharmacogenomics further promotes its uptake.

Bottom of Form

By Technology Type, PCR-based Testing Dominates While DNA Sequencing Grows Rapidly:

PCR-based Testing segment dominated the market due to their clinical acceptance, high reliability, and cost-effectiveness. PCR-based tests have the capacity to reliably identify critical genetic variants responsible for the metabolism of warfarin, combined with their fast-processing speed and laboratory standardization, to guarantee dominance in the market.

DNA Sequencing is the fastest-growing market segment owing to the rising requirement for high-level identification and multi-genetic variants analysis. Rising acceptance for precision medicine approaches and developments in next-generation sequencing technology is fueling growth in this market segment.

By End-User, Hospitals & Clinics Dominate While Diagnostic Centers Grow Rapidly:

Hospitals & Clinics segment dominated the market owing to their central role in patient care delivery and strong integration of pharmacogenomic testing into routine anticoagulant therapy management. Their ability to combine diagnostic services with clinical decision-making workflows ensures consistent demand for warfarin sensitivity testing across large patient populations.

Diagnostic Centers are the fastest-growing segment, driven by increasing outsourcing of genetic testing services, rising demand for specialized diagnostic infrastructure, and growing availability of advanced molecular testing platforms.

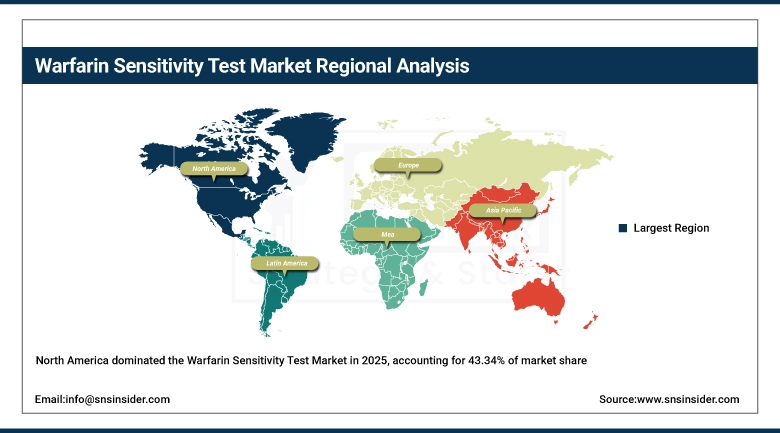

Warfarin Sensitivity Test Market Regional Analysis:

North America Warfarin Sensitivity Test Market Insights:

The North America Warfarin Sensitivity Test Market is a is dominated, holding a 43.34% share in 2025. Region has significant and robust demand due to the presence of several cardiovascular diseases cases, robust healthcare infrastructure in place, and advanced adoption of practices of precision medicine. Extensive use of pharmacogenomics in clinical processes carried out in hospitals and diagnostic laboratories in the country ensures steady growth in the market in the United States and Canada. Extensive use of genotype-guided dosing for anticoagulants along with robust knowledge amongst practitioners regarding preventive measures from drug reactions is enhancing the market further. Constant innovation in molecular diagnostics and strong reimbursement structure for genetic tests is further fueling growth in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Warfarin Sensitivity Test Market Insights:

Warfarin Sensitivity Test in the United States has witnessed high development of the healthcare industry, rapid adoption of pharmacogenomics, and wide acceptance of anticoagulants amongst large numbers of patients. Emphasis on precision medicine along with growing integration of genetic testing in electronic health records and clinical decision support systems is driving the market in hospitals and diagnostics laboratories.

Asia-Pacific Warfarin Sensitivity Test Market Insights:

The Asia-Pacific Warfarin Sensitivity Test Market is the fastest-growing region, projected to expand at a 8.96% CAGR during the forecast period. Factors such as an increase in the prevalence of cardiovascular diseases, developments in the healthcare infrastructure, and the growing awareness of pharmacogenomic testing in emerging countries such as China, India, Japan, and South Korea have led to growth in the industry. Improvements in diagnostic techniques, significant investments in molecular testing labs, and greater accessibility to healthcare services have been facilitating the expansion of the industry. Moreover, the increasing emphasis of the government on health care outcomes and the gradual acceptance of precision medicine practices have also helped propel the regional market's growth.

China Warfarin Sensitivity Test Market Insights:

The China Warfarin Sensitivity Test Market is fueled by the fast development of healthcare infrastructure, the increasing incidence of cardiovascular diseases, and advancements in medical technology. The strong support of the government toward the application of precision medicine and investments in molecular diagnostic labs, have facilitated the integration of pharmacogenomic testing. In addition, the expansion of hospitals, along with physician knowledge about genotype-based anticoagulation therapy, has contributed to the market's development.

Europe Warfarin Sensitivity Test Market Insights:

The Europe Warfarin Sensitivity Test Market benefits from sophisticated healthcare infrastructures, robust regulatory policies, and high levels of adoption of evidence-based clinical practices. Nations such as Germany, France, and the UK have increasingly been integrating pharmacogenomic tests within the process of anticoagulation therapy management to ensure patient safety and minimize the risk of drug interactions. The region's commitment to personalized treatment approaches, together with the expansion of genetic testing reimbursement within multiple nations' healthcare systems, is boosting market uptake.

Germany Warfarin Sensitivity Test Market Insights:

The Germany Warfarin Sensitivity Test Market can be described as one that exhibits a highly developed medical healthcare system, along with clinical accuracy and application of molecular diagnostics. Germany’s approach to personalized medicine coupled with the high level of stringency when it comes to clinical standards has resulted in an increased use of pharmacogenomic testing for hospitals’ anticoagulant therapy regimens.

Latin America Warfarin Sensitivity Test Market Insights:

The Latin America Warfarin Sensitivity Test Market is witnessing gradual growth driven by rising prevalence of cardiovascular conditions, improving healthcare infrastructure, and increasing access to advanced diagnostic services in countries such as Brazil, Mexico, and Argentina. Growing adoption of modern laboratory technologies and expanding private healthcare investments are supporting the uptake of pharmacogenomic testing in urban medical centers. However, limited reimbursement coverage and uneven access to advanced diagnostics across rural regions continue to moderate adoption rates.

Middle East & Africa Warfarin Sensitivity Test Market Insights:

The Middle East & Africa Warfarin Sensitivity Test Market is witnessing growth due to advancements in healthcare facilities, prevalence of cardiovascular diseases, and development in diagnostic technology. Countries such as UAE, Saudi Arabia, and South Africa are spearheading implementation of pharmacogenomic tests due to their efforts in upgrading hospitals and establishing dedicated laboratories for conducting tests. There is growing importance placed on enhancing clinical outcomes and minimizing medication-related side effects.

Warfarin Sensitivity Test Market Competitive Landscape:

F. Hoffmann-La Roche Ltd. is a leading player in the warfarin sensitivity test market, with a strong presence in molecular diagnostics, PCR-based testing platforms, and integrated laboratory solutions. The company’s competitive strength lies in its advanced diagnostic ecosystems, high-throughput testing technologies, and distribution network across hospitals and reference laboratories. Roche focuses on enabling precision medicine through reliable genetic testing solutions that support genotype-guided anticoagulant dosing and improved patient safety outcomes.

-

In June 2025, Roche expanded its molecular diagnostics portfolio by enhancing its PCR-based pharmacogenomic testing solutions integrated with automated lab workflows across major European and North American diagnostic networks, improving efficiency in clinical genotype interpretation and reporting.

Thermo Fisher Scientific Inc. is a major provider of life sciences tools and molecular diagnostic technologies, playing a critical role in warfarin sensitivity testing through DNA sequencing platforms, PCR systems, and genetic analysis workflows. The company’s strength lies in its comprehensive portfolio of genomic instruments, reagents, and software solutions that support high-precision pharmacogenomic testing. Thermo Fisher is widely adopted in clinical laboratories and research institutions for its scalable and automated solutions that enable efficient multi-gene testing and advanced genomic analysis. Its continuous innovation in sequencing technologies and laboratory automation supports expanding adoption of personalized medicine approaches.

-

In July 2025, Thermo Fisher Scientific expanded its next-generation sequencing and pharmacogenomics workflow solutions across several clinical diagnostic laboratories in North America and Asia-Pacific, enhancing multi-gene testing capabilities for anticoagulant therapy optimization.

Abbott Laboratories is a prominent player in the warfarin sensitivity test market, offering advanced molecular diagnostics platforms, automated testing systems, and integrated healthcare solutions. The company’s competitive advantage lies in its strong presence in clinical diagnostics, combined with its focus on fast, reliable, and scalable genetic testing technologies. Abbott supports pharmacogenomic applications through its molecular diagnostic systems that enable improved anticoagulant therapy management and reduced risk of adverse drug reactions. Its emphasis on integrating diagnostics with clinical decision-support tools enhances adoption across hospitals and diagnostic centers.

-

In August 2025, Abbott Laboratories strengthened its molecular diagnostics portfolio by expanding deployment of automated genetic testing platforms across hospital networks in Europe and North America, supporting faster pharmacogenomic testing for anticoagulant therapy optimization.

Warfarin Sensitivity Test Market Key Players:

Some of the Warfarin Sensitivity Test Market Companies are:

-

F. Hoffmann-La Roche Ltd.

-

Thermo Fisher Scientific Inc.

-

Abbott Laboratories

-

Illumina Inc.

-

QIAGEN N.V.

-

Siemens Healthineers AG

-

Bio-Rad Laboratories Inc.

-

Becton Dickinson and Company (BD)

-

Danaher Corporation (Cepheid)

-

Agilent Technologies Inc.

-

Myriad Genetics Inc.

-

Eurofins Scientific SE

-

Quest Diagnostics Incorporated

-

Laboratory Corporation of America Holdings (LabCorp)

-

GenMark Diagnostics Inc.

-

Agena Bioscience Inc.

-

Eurolyser Diagnostica GmbH

-

TrimGen Corporation

-

ACON Laboratories Inc.

-

CoaguSense Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.54 Billion |

| Market Size by 2035 | USD 3.19 Billion |

| CAGR | CAGR of 7.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Reagents & Kits, Instruments, Software & Services, Others) • By Technology (PCR-based Testing, DNA Sequencing, Microarray, Others) • By Gene Type (CYP2C9 Testing, VKORC1 Testing, Combined Gene Testing, Others) • By Application (Diagnostic Laboratories,Hospitals, Research Institutes, Others) • By End User (Hospitals & Clinics, Diagnostic Centers, Academic & Research Organizations, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., Abbott Laboratories, Illumina Inc., QIAGEN N.V., Siemens Healthineers AG, Bio-Rad Laboratories Inc., Becton Dickinson and Company (BD), Danaher Corporation (Cepheid), Agilent Technologies Inc., Myriad Genetics Inc., Eurofins Scientific SE, Quest Diagnostics Incorporated, Laboratory Corporation of America Holdings (LabCorp), GenMark Diagnostics Inc., Agena Bioscience Inc., Eurolyser Diagnostica GmbH, TrimGen Corporation, ACON Laboratories Inc., CoaguSense Inc. |

Frequently Asked Questions

North America dominated with a 43.34% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 8.96% during 2026–2035.

Reagents & Kits dominated with a 58.25% share in 2025, while Software & Services are projected to grow at the fastest CAGR of 9.01% during 2026–2035.

Growth is driven by rising prevalence of cardiovascular diseases and increasing use of anticoagulant therapies, along with growing adoption of pharmacogenomic testing to improve patient safety and treatment outcomes.

The market is valued at USD 1.54 Billion in 2025 and is projected to reach USD 3.19 Billion by 2035.

The Warfarin Sensitivity Test Market is projected to grow at a CAGR of 7.72% during 2026–2035.

Get in Touch