Wood-Based Panel Market Report Scope & Overview:

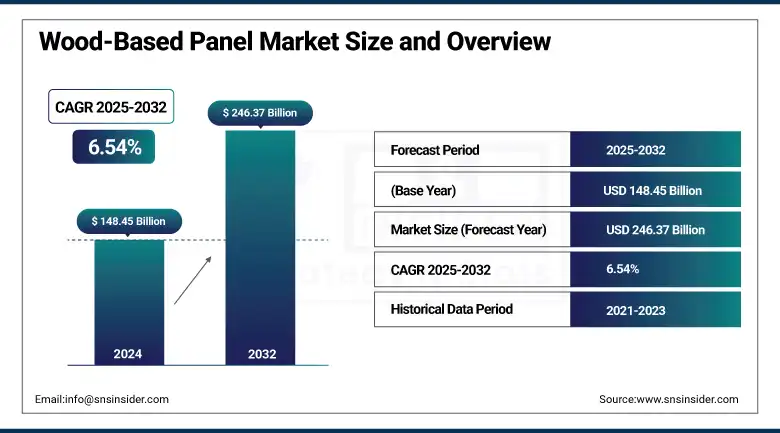

The Wood-Based Panel Market size was valued at USD 148.45 billion in 2024 and is expected to reach USD 246.37 billion by 2032, growing at a CAGR of 6.54% over the forecast period of 2025-2032.

The Global Wood-Based Panel Market is experiencing robust expansion, driven by rising demand in construction, furniture manufacturing, and interior design applications. As Part of the wider Wood Based Panel Industry, this market comprises of such engineered wood panels as medium density fiberboard (MDF), particleboard, Oriented Strand Board (OSB), plywood, and hardboard. This is a market favorite for cost, long life, and sustainability over solid wood. High rate of urbanization, along with inclination towards environment-friendly construction materials, are the leading factors driving the Wood-Based Panel Market Growth. With changing consumer and industry needs, manufacturers are working to innovate panel properties such as moisture resistance, fire retardancy, and structural strength.

To Get more information On Wood-Based Panel Market - Request Free Sample Report

Furthermore, increasing consciousness about sustainable forest products and recycling of wood fibers is further strengthening its character in the market. Wood-Based Panel Market Trends growth in modular construction and ready-to-assemble furniture has led to an increase in demand for lightweight and easy-to-install panels. Improving manufacturing processes through automation, digital control of production, and technology can also provide improvements in product quality and production efficiency. Despite the challenges posed by the recent pandemic, the Global Wood-Based Panel Market has emerging opportunities for the present and future, and innovation and sustainability will curate the future of the Engineered Wood Panels segment.

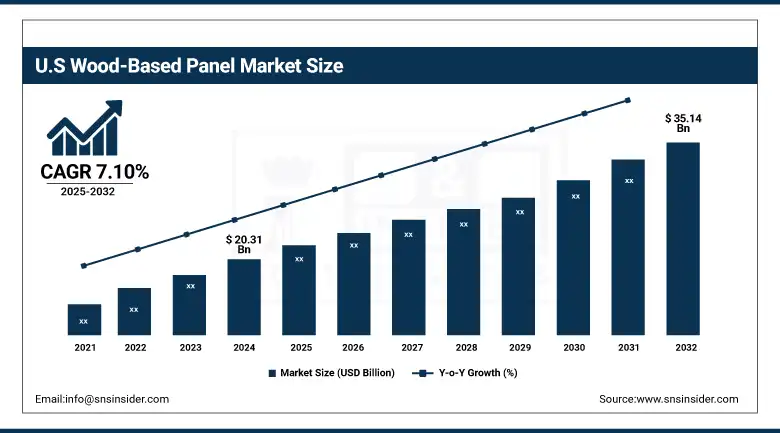

The U.S. leads the North American wood-based panel market, with a valuation of USD 20.31 billion in 2024, projected to reach USD 35.14 billion by 2032 at a CAGR of 7.10%. Growth in this area is driven by the expanding construction sector, increasing demand for engineered wood for use in buildings, and increasing application in furniture production. This increase is aided by advanced manufacturing technologies and sustainable forestry practices within the country. Moreover, increasing consumer interest in environment-friendly and low-cost materials boosts the market growth.

Wood-Based Panel Market Dynamics:

Drivers:

-

Technological Innovations Boost Durability, Safety, and Sustainability in Wood-Based Panel Manufacturing

Technological advancements in wood-based panel manufacturing technologies and the performance of wood-based panels has significantly improved, which has expanded the applications of wood-based panels. Innovation, such as the developments in moisture-resistance and fire-retardance, has made these materials usable in a broader range of settings, such as humid and fire-prone areas. Such innovations enhance durability, safety, and structural performance, helping wood-based panels become the material of choice in construction, furniture, and interior design. The introduction of advanced manufacturing processes, such as continuous press technology and resin optimization, has also helped improve production efficiency with lower emissions. The upgrades also comply with the strictest environmental regulations while responding to greater consumer demand for sustainable and high-performance construction materials, which expands the global market for engineered wood products.

In March 2025 – LIGNA 2025, set for May 26–30 in Hannover, will spotlight engineered wood as a key to sustainable construction. Celebrating its 50th year, the event will feature firms including Minda, Weinig, and Dieffenbacher showcasing AI-driven CLT lines and energy-efficient machinery. The focus is on wood’s strength, lightweight nature, and carbon-sequestration ability, promoting it as a green alternative to steel and concrete in prefabrication.

Restraint

-

Raw Material Volatility in Wood-Based Panel Industry Amid Supply Constraints and Environmental Regulations

The wood-based panel industry is a raw material-based industry, with its high dependency on timber and resins, which during crisis can be the reason of price volatility and supply disruption. Timber prices tend to vary widely as a result of seasonality, transport costs, and general demand globally, which can have a direct impact on production costs. In addition, the resins that are necessary for bonding wood fibers are made from petrochemicals, which are similarly volatile. Furthermore, new strict regulations against deforestation coupled with increasing environmental awareness have limited the opportunities to log and access quality timber. These disruptions can create bottlenecks in the supply chain, hinder production capabilities, and ultimately cut the profitability of manufacturers. These risks are leading companies to greater interest in alternative raw materials and sustainable forestry practices.

In May 2025 – Executives from Canadian lumber giants Canfor and Interfor warned of extreme wood price volatility due to anticipated U.S. tariff hikes, which may be more than double to over 34%. These steep duties could disrupt supply chains, drive up construction costs, and worsen housing affordability. While the U.S. producers might benefit, consumers are expected to face higher prices.

Wood-Based Panel Market Segmentation Analysis:

By Product

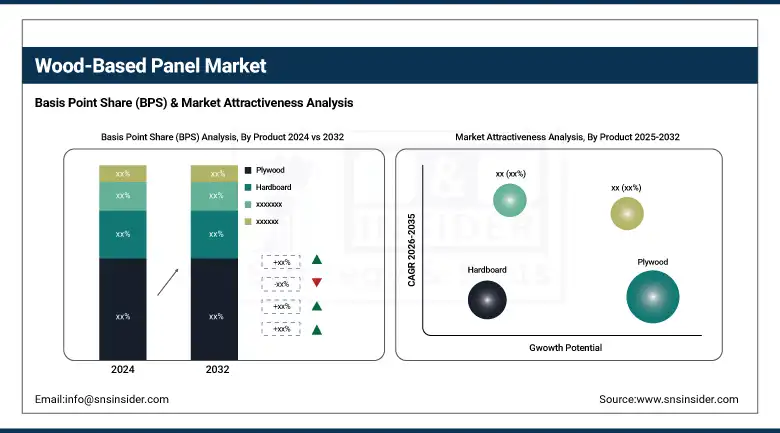

Plywood segment dominated the market and accounted for 41% of the Wood-Based Panel market share owing to superior strength, superior dimensional stability, and minimum cracking, shrinking, and warping. It is the most common of the engineered wood products used in construction, furniture, and packaging. Plywood is a versatile material with high strength and is therefore suited to work in structural applications, such as subfloors, wall sheathing, and roofs. In addition, increasing demand from developing countries, where construction and renovation activities continue to expand, further maintains its position. Additionally, an established supply chain along with the availability of plywood in different grades contributes toward maintaining plywood market leadership.

Oriented Strand Board (OSB) is witnessing the fastest growth among product segments in the wood-based panel market due to its relatively low cost (compared to plywood at least) and high strength-to-weight ratio. In North America and to an extent in Europe, OSB is becoming a replacement for plywood in many construction applications. Its price point makes it attractive to builders and developers looking for similar strength and stiffness at a lower price. Driving this is their increasing use in structural wall sheathing, flooring, and roof decking, a sector driving product adoption. Also, it is boosting the consumption of engineered wood products, such as OSB as they utilize timber resources effectively, as modern construction practices are increasingly encouraging sustainable construction.

By Application

The furniture segment led the market with a 57.1% share in 2024. Wood-based panels are extensively used in furniture production due to their uniformity, easy machinability, and cost-effectiveness compared to solid wood. Demand is extremely high for ready-to-assemble and modular furniture that primarily uses MDF, particleboard, and plywood. Residential demand for furniture has been driven by urbanization, increasing disposable income, and rapid development of the real estate sector. Furthermore, increasing preference for DIY and customized furniture solutions is further fortifying wood-based panels to dominate this application segment.

The construction segment is the fastest-growing application area for wood-based panels, driven by surging infrastructure development and residential housing projects globally. Driven by structural and non-structural applications, such as flooring, wall panels, and roofing, products such as OSB, plywood and MDF have proved to be popular materials. The green movement in building, coupled with the industry's own drive to have lower environmental impact, is also pushing for the use of engineered wood products. Additionally, the increased demand for prefabricated and modular construction techniques in which wooden based panels are integral products is further propelling the expansion of this segment.

Wood-Based Panel Market Regional Outlook:

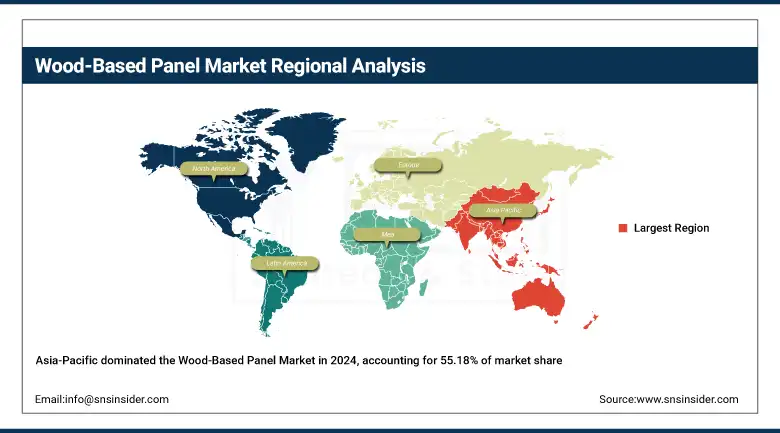

The Asia-Pacific region is dominated with a market share of over 55.18% in 2024. This dominance is primarily driven by rapid urbanization, booming construction activities, and strong demand from furniture manufacturing hubs, such as China, India, and Southeast Asian countries. Additionally, the region is blessed with access to abundant raw materials and cheap labor. The ability to further establish itself in the market is aided by the increase in the investment, including a good investment in infrastructure as well, tackle numerous leaders in panel manufacturing. In addition, the government is increasingly offering affordable housing and expanding industrial activities, which is majorly driving the growth of the region as well as its dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

China dominates the Asia-Pacific wood-based panel market due to its large manufacturing base, high consumption, and strong export network. The country benefits from Abundant raw materials, cheap labor, and a strong furniture and construction sector will be of use to the country. The demand is additionally increased due to faster urbanization and infrastructure development. Another catalyst for growth is government support for affordable housing.

North America is emerging as the fastest-growing region in the wood-based panel market due to rising demand for eco-friendly and engineered wood products. The revival in homebuilding, renovation projects, and a general consumer shift toward sustainable furniture is driving this expansion. Another key factor boosting the market growth is the technological advancements in the panel production, such as green building standards. Panel imports and domestic sales are climbing steadily in the U.S. and Canada, led by categories in MDF and OSB. Also, favorable regulations and boosted supply chain networks are driving a swift regional market growth.

Europe holds a significant share of the global wood-based panel market, backed by mature construction and furniture industries. Countries including Germany, France, and Italy are the main origin of this growth due to their long tradition in woodworking and the high demand for engineered wood in these countries. Due to its commitment to sustainability, recycling, and the only really strict rules about forest management globally, wood-based panels offer strong competition for solid wood in the region. The innovation in product design in accordance with the environmental standard, including EUTR (EU Timber Regulation) has continued to maintain the demand. Europe is still an important but low-growth market for wood-based panels.

Wood-based panel Companies are:

Kronospan, Pfleiderer Group S.A., EGGER Group, Panels & Furniture Group (PFM Group), Georgia-Pacific LLC (Koch Industries), Norbord Inc., Arauco, Ainsworth Lumber Co. Ltd., Boise Cascade Company, and Louisiana-Pacific Corporation (LP).

Recent Developments:

In May 2025, Georgia-Pacific released its 2024 “Progress With Purpose” Stewardship Report, outlining sustainability efforts across five key pillars. Key highlights include the launch of DensDeck gypsum panels to support solar installations, a No Idling policy at its Texas plant to cut emissions, and a 75% reduction in SO₂ emissions since 2010. The report emphasizes the company’s ongoing commitment to responsible resource use and environmental stewardship.

In May 2024, Wood PLC partnered with Georgia-Pacific’s Juno to implement a cutting-edge waste recovery technology capable of diverting up to 90% of municipal solid waste from landfills. Wood will handle the FEED and EPCm services for Juno’s global facility expansion and provide long-term operational support. This collaboration aims to advance sustainable waste management by recovering valuable materials like paper, plastics, metals, and biogas. The first commercial facility's design phase has already begun in the U.K.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 148.45 Billion |

| Market Size by 2032 | USD 246.37 Billion |

| CAGR | CAGR of 6.54% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (MDF, HDF, PB, OSB, Softboard, Hardboard, Plywood) • By Application (Furniture, Construction, Packaging) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kronospan, Pfleiderer Group S.A., EGGER Group, Panels & Furniture Group (PFM Group), Georgia-Pacific LLC (Koch Industries), Norbord Inc., Arauco, Ainsworth Lumber Co. Ltd., Boise Cascade Company, Louisiana-Pacific Corporation (LP) |

Frequently Asked Questions

Ans: The Asia-Pacific region dominated the Wood-Based Panel market in 2024.

Ans: The “Plywood” segment dominated the Wood-Based Panel market.

Ans: Technological Innovations Boost Durability, Safety, and Sustainability in Wood-Based Panel Manufacturing

Ans: The Wood-Based Panel market was USD 148.45 billion in 2024 and is expected to reach USD 246.37 billion by 2032.

Ans: The Wood-Based Panel market is expected to grow at a CAGR of 6.54% from 2025 to 2032.

Get in Touch